Get More Information on Wet Chemicals for Electronics and Semiconductor Applications Market - Request Sample Report

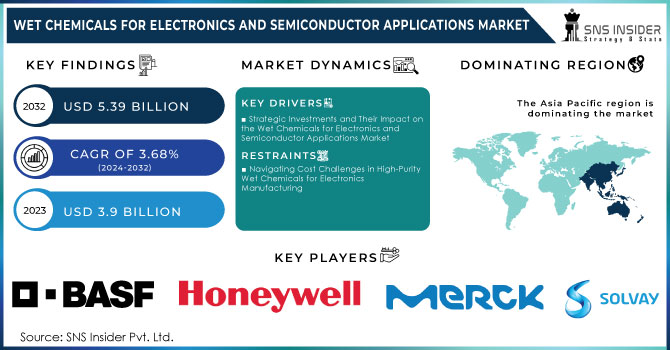

The Wet Chemicals for Electronics and Semiconductor Applications Market was valued as USD 3.9 Billion in 2023 and expected to reach at USD 5.39 Billion by 2032 and grow at a CAGR of 3.68% over the forecast period 2024-2032.

The Wet Chemicals for Electronics and Semiconductor Applications market is experiencing significant growth, driven by increasing demand for high-performance electronic components and the ongoing expansion of the semiconductor manufacturing market. As the electronics industry evolves, the need for specialized wet chemicals such as photoresists, developers, etchants, and cleansers has surged, primarily due to their critical role in semiconductor fabrication and device miniaturization.

The Wet Chemicals for Electronics and Semiconductor Applications market is experiencing significant developments driven by the increasing demand for high-purity chemicals used in semiconductor manufacturing. As the industry evolves, several factors contribute to its dynamics, highlighting trends, regional developments, and the competitive landscape.

One of the primary drivers is the rise in semiconductor production, particularly in regions like Asia Pacific, where countries such as China, Taiwan, and South Korea dominate manufacturing capabilities. This region alone contributes over 60% of the global semiconductor market, showcasing its importance in the wet chemicals segment. The growth of consumer electronics, automotive electronics, and IoT devices fuels this demand, necessitating advanced materials and chemicals to meet stringent quality requirements

In India, significant investments are being made to bolster domestic semiconductor manufacturing capabilities, aiming to reduce dependency on imports. Such governmental support and investment can potentially reshape the global supply chain and influence the wet chemicals market by boosting local demand for high-purity chemicals.

Sustainability is another crucial factor impacting the wet chemicals market. The push for eco-friendly and sustainable practices in semiconductor manufacturing is leading to innovations in wet chemical formulations. Companies are increasingly focusing on developing biodegradable and less toxic cleaning agents and etchants to minimize environmental impact This trend not only addresses regulatory pressures but also aligns with the growing consumer demand for sustainable practices across all sectors.

The competitive landscape includes notable players such as BASF SE, Kanto Chemical Co., and Linde plc, which are continuously innovating to enhance their product offerings. They are focusing on high-purity and specialty chemicals, which are essential for advanced semiconductor processes.

Additionally, the increasing collaboration between semiconductor manufacturers and chemical suppliers aims to streamline supply chains and improve the efficiency of chemical processes. The Wet Chemicals for Electronics and Semiconductor Applications market is positioned for substantial growth, supported by regional manufacturing expansions, sustainability trends, and technological advancements. Key players are actively responding to market needs, thereby enhancing the industry's capacity to meet future demands.

Drivers

Governments around the world, especially in India and the U.S., are making substantial investments in domestic semiconductor manufacturing to guarantee self-reliance in technology and improve competitiveness on a global scale. The Indian government has committed USD 10 billion to enhance its semiconductor ecosystem in order to establish a strong manufacturing foundation to cater to the increasing need for electronic devices. This effort reflects the worldwide acknowledgment of the crucial role semiconductors play in economies, leading to a significant rise in demand for high-purity wet chemicals utilized in semiconductor production. Highly pure acids, solvents, and etching solutions are essential in different manufacturing processes, such as photolithography and cleaning. The increase in semiconductor production will directly impact the wet chemicals market, as companies need dependable suppliers of specialized chemicals to uphold production standards and effectiveness. This connection emphasizes the significance of wet chemicals in semiconductor uses and points out the upcoming possibilities in this sector, set for substantial expansion with government backing for their local semiconductor sectors.

The growing emphasis on adhering to regulations is a key force in the wet chemicals industry for electronics and semiconductor uses. With increasing global environmental regulations, manufacturers are pressured to come up with innovative and sustainable practices. This change is noticeable as businesses react to consumer requests for environmentally friendly products and clear supply chains. Recent studies show that the majority of consumers prioritize sustainability, with 70% preferring products that reduce environmental impact. This tendency forces companies to adjust their products to reflect these values, leading them to incorporate biodegradable and less harmful ingredients in their range of products. Furthermore, adherence to guidelines like the European Union's REACH motivates manufacturers to prioritize the decrease of harmful substances in their liquid chemicals. This set of regulations promotes innovation and improves competition in the market by pushing companies to adapt or risk losing their market share. Therefore, the wet chemicals market is being shaped by aligning regulatory compliance with consumer preferences for sustainability, leading to growth in eco-friendly solutions for the electronics and semiconductor industries.

Restraints

The production of high-purity wet chemicals for electronics and semiconductor applications faces significant challenges due to elevated production costs. The manufacturing process demands advanced technologies and equipment to maintain strict purity levels essential for semiconductor fabrication. As a result, investments in purifiers, facilities, and oversight become capital-intensive. These increased expenses drive up the prices of high-purity wet chemicals, potentially hindering market growth and making it difficult for new manufacturers to enter the space. Smaller companies and start-ups often struggle to absorb these high costs, which can impede their competitiveness. Additionally, businesses cannot afford to halt their research and development efforts to explore innovative methods and materials while adhering to rigorous quality standards. This combination of rising manufacturing costs and reduced profit margins due to market competition restricts companies' ability to expand. Firms specializing in high-purity wet chemicals must navigate the delicate balance between achieving economies of scale and delivering top-quality products. As the market evolves, there is increasing pressure to focus on cost-efficiency and technological advancements. This necessity arises as more companies attempt to enter the market, offering alternative compounds at lower prices. Addressing the cost challenge is crucial for maximizing growth within the wet chemicals market for electronics and semiconductor applications.

by Product

Acetic acid plays a key role in the wet chemicals for electronics and semiconductor applications market, making up approximately 23% of the revenue share in 2023. Its importance in several manufacturing processes, especially semiconductor fabrication, lies in its effectiveness as a solvent and reactant. Acetic acid plays an essential role in photolithography by aiding in the creation of precise patterns on semiconductor wafers through high-quality etching solutions. As semiconductor technology progresses, the need for high-purity acetic acid is increasing due to its effectiveness in cleaning surfaces and ensuring contaminant-free wafers for efficient chip production. The increasing demand is being driven even more by the expanding electronics industry, which includes consumer electronics and IoT devices. Furthermore, the trend towards eco-friendly practices is causing manufacturers to choose acetic acid over harsher solvents as a more environmentally friendly option.

In the future, the acetic acid industry is projected to do well due to ongoing technological progress and substantial investments in semiconductor production, particularly in areas such as the U.S. and India. This trend highlights the crucial importance and future expansion possibilities of acetic acid in the wet chemicals market.

by Application

In the Wet Chemicals for Electronics and Semiconductor Applications market, cleaning applications made up around 35% of the market in 2023, emphasizing their crucial role in preserving the integrity of semiconductor devices. The cleaning procedure is essential for eliminating pollutants such as dust, organic remains, and metal particles from wafers and substrates, which is crucial for maintaining high manufacturing standards. Contaminants have the potential to negatively affect the electrical properties and overall functionality of semiconductor products, resulting in flaws and reduced output. In order to maintain impurity-free surfaces, specialized solvents and detergents are used, such as high-purity wet chemicals.Recent tendencies show an increasing need for high-tech cleaning options, especially environmentally friendly advancements that support sustainability objectives. Merck KGaA and other companies are introducing new cleaning formulas tailored for semiconductor use, focusing on thorough removal of contaminants and environmental adherence. Additionally, Enviro Tech Chemical Services is creating new formulas to reduce their impact on the environment. Moreover, companies such as Tokyo Ohka Kogyo Co. (TOK) are dedicating resources to research in order to improve the efficiency and effectiveness of cleaning through the use of advanced technologies and automation. These patterns not just show the sector's dedication to excellence but also emphasize the continuous progression towards more environmentally friendly production techniques.

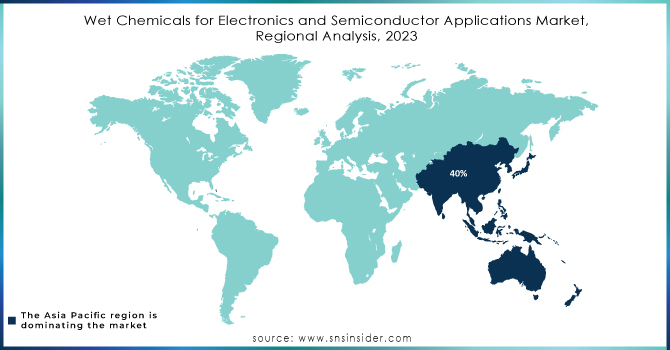

In 2023, the Asia Pacific region dominated the Wet Chemicals for Electronics and Semiconductor Applications market, capturing around 40% of the revenue. This leadership stems from a robust semiconductor manufacturing base, with major players like TSMC and Samsung bolstered by strong infrastructure and skilled labor. Additionally, the rapid growth of the electronics sector in China, Japan, and South Korea further drives demand for high-quality wet chemicals, essential for consumer electronics production. Increased investment in R&D fosters innovation in wet chemical solutions, while stringent environmental regulations push manufacturers toward eco-friendly alternatives, supported by government initiatives aimed at enhancing the semiconductor industry.

In 2023, North America emerged as the fastest-growing region in the wet chemicals for electronics and semiconductor applications market, capturing about 25% of the global market share. This rapid expansion is driven by several factors.North America is a center for technological innovation, particularly in advanced sectors like 5G, artificial intelligence, and IoT. The demand for high-purity wet chemicals essential for manufacturing processes such as cleaning, etching, and doping has surged due to the push for more sophisticated semiconductor devices. The United States has a robust semiconductor-manufacturing base that bolsters the need for wet chemicals. Ongoing investments in research and development are fostering innovation and enhancing production capabilities. Sustainability is another critical trend influencing market growth. Stricter environmental regulations are encouraging companies to implement eco-friendly alternatives, including biodegradable and less toxic wet chemicals. The increasing consumer demand for advanced electronic devices also plays a significant role, as the complexity of these products necessitates high-quality wet chemicals in their manufacturing processes. Furthermore, government initiatives, including subsidies and infrastructure investments, are further propelling market growth by promoting innovation and expansion.

Need Any Customization Research On Wet Chemicals for Electronics and Semiconductor Applications Market - Inquiry Now

Key Players

Some of the major Key Players in Wet Chemicals for Electronics and Semiconductor Applications Market who provide product and offering:

Recent Developemnt

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.9 Billion |

| Market Size by 2032 | USD 5.39 Billion |

| CAGR | CAGR of 3.68% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Acetic Acid, Hydrogen Peroxide, Hydrochloric Acid, Ammonium Hydroxide, Nitric Acid, Sulfuric Acid, Phosphoric Acid, Others) • by Application (Cleaning, Etching, PCB Manufacturing, Integrated Circuit, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Key players in the Wet Chemicals Market for Electronics and Semiconductor Applications include BASF SE, Kanto Chemical Co., Inc., Solvay S.A., Linde plc, Avantor, Inc., Honeywell International Inc., Eastman Chemical Company, Technic Inc., Wako Pure Chemical Industries, Ltd., Fujifilm Group, Entegris, Inc., Ashland Global Holdings Inc., Merck KGaA, Mitsubishi Chemical Corporation, Cabot Microelectronics Corporation, and Sumitomo Chemical Co., Ltd. |

| Key Drivers | • Strategic Investments and Their Impact on the Wet Chemicals for Electronics and Semiconductor Applications Market • Regulatory compliance is motivating sustainable practices in the wet chemicals for electronics and semiconductor applications market |

| RESTRAINTS | • Navigating Cost Challenges in High-Purity Wet Chemicals for Electronics Manufacturing |

Ans: The Wet Chemicals for Electronics and Semiconductor Applications Market was valued as USD 3.9 Billion in 2023 and expected to reach at USD 5.39 Billion by 2032.

The growing demand for advanced electronics, increasing semiconductor production, and the miniaturization of electronic devices are key drivers for the wet chemicals market, particularly in cleaning and etching processes.

Ans: The Wet Chemicals for Electronics and Semiconductor Applications grow at a CAGR of 3.68% over the forecast period of 2024-2032.

Common wet chemicals include sulfuric acid, hydrochloric acid, nitric acid, hydrogen peroxide, and various solvents and etchants used in the cleaning and etching of silicon wafers during semiconductor fabrication.

Leading companies include BASF SE, Honeywell International, Kanto Chemical, Solvay, and Avantor, which supply high-purity chemicals for semiconductor and electronics manufacturing.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Wafer Production Volumes, by Region (2023)

5.2 Chip Design Trends (Historic and Future)

5.3 Fab Capacity Utilization (2023)

5.4 Supply Chain Metrics

6. Competitive Landscape

6.1 List of Major Companies, by Region

6.2 Market Share Analysis, by Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Wet Chemicals for Electronics and Semiconductor Applications Market Segmentation, by Application

7.1 Chapter Overview

7.2 Acetic Acid

7.2.1 Acetic Acid Market Trends Analysis (2020-2032)

7.2.2 Acetic Acid Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Hydrogen Peroxide

7.3.1 Hydrogen Peroxide Market Trends Analysis (2020-2032)

7.3.2 Hydrogen Peroxide Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Ammonium Hydroxide

7.5.1 Ammonium Hydroxide Market Trends Analysis (2020-2032)

7.5.2 Ammonium Hydroxide Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Nitric Acid

7.6.1 Nitric Acid Market Trends Analysis (2020-2032)

7.6.2 Nitric Acid Market Size Estimates and Forecasts to 2032 (USD Billion)

7.7 Sulfuric Acid

7.7.1 Sulfuric Acid Market Trends Analysis (2020-2032)

7.7.2 Sulfuric Acid Market Size Estimates and Forecasts to 2032 (USD Billion)

7.8 Phosphoric Acid

7.8.1 Phosphoric Acid Market Trends Analysis (2020-2032)

7.8.2 Phosphoric Acid Market Size Estimates and Forecasts to 2032 (USD Billion)

7.9 Others

7.9.1 Others Market Trends Analysis (2020-2032)

7.9.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Wet Chemicals for Electronics and Semiconductor Applications Market Segmentation, by End User

8.1 Chapter Overview

8.2 Cleaning

8.2.1 Cleaning Market Trends Analysis (2020-2032)

8.2.2 Cleaning Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Etching

8.3.1 Etching Market Trends Analysis (2020-2032)

8.3.2 Etching Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Printed Circuit Board Manufacturing

8.4.1 Printed Circuit Board Manufacturing Market Trends Analysis (2020-2032)

8.4.2 Printed Circuit Board Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Integrated Circuit

8.5.1 Integrated Circuit Market Trends Analysis (2020-2032)

8.5.2 Integrated Circuit Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Others

8.6.1 Others Market Trends Analysis (2020-2032)

8.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.4 North America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.5.2 USA Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.6.2 Canada Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.7.2 Mexico Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.5.2 Poland Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.6.2 Romania Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.4 Western Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.5.2 Germany Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.6.2 France Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.7.2 UK Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.8.2 Italy Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.9.2 Spain Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.12.2 Austria Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4 Asia-Pacific

9.4.1 Trends Analysis

9.4.2 Asia-Pacific Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia-Pacific Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.4 Asia-Pacific Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5.2 China Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5.2 India Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5.2 Japan Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.6.2 South Korea Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.7.2 Vietnam Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.8.2 Singapore Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.9.2 Australia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.4.10 Rest of Asia-Pacific

9.4.10.1 Rest of Asia-Pacific Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia-Pacific Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.4 Middle East Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.5.2 UAE Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.4 Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.4 Latin America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.5.2 Brazil Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.6.2 Argentina Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.7.2 Colombia Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Wet Chemicals for Electronics and Semiconductor Applications Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10. Company Profiles

10.1 BASF SE

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 Kanto Chemical Co., Inc.

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Solvay S.A.

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Linde plc,

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Avantor, Inc.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Honeywell International Inc.

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 Eastman Chemical Company

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Technic Inc.

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Wako Pure Chemical Industries, Ltd.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Fujifilm Group

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

by Product

Acetic Acid

Hydrogen Peroxide

Hydrochloric Acid

Ammonium Hydroxide

Nitric Acid

Sulfuric Acid

Phosphoric Acid

Others

by Application

Cleaning

Etching

Printed Circuit Board Manufacturing

Integrated Circuit

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Stretchable Conductive Material Market was valued at USD 796.41 million in 2023 and is expected to reach USD 4510.59 million by 2032, growing at a CAGR of 21.28% over the forecast period 2024-2032.

The Multi-touch Screen Market was USD 14.46 Billion in 2023 and is expected to reach USD 41.73 Billion by 2032 and grow at a CAGR of 12.54% by 2024-2032.

The Accelerator Card Market Size was valued at USD 13.50 Billion in 2023 and it is estimated to reach USD 208.37 Billion at a CAGR of 35.57% during 2024-2032

The Interactive Projector Market was valued at USD 3.11 billion in 2023 and is expected to grow at a CAGR of 16.43% to reach USD 12.19 billion by 2032.

The Virtual Production Market Size was valued at USD 2.73 Billion in 2023 and is expected to reach USD 10.35 Billion by 2032, at 15.99% CAGR During 2024-2032

The Application-Specific Integrated Circuit Market Size is Projected to reach USD 32.12 Billion by 2032 and grow at a CAGR of 6.3% During 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd