Get More Information on Vitamin Ingredients Market - Request Sample Report

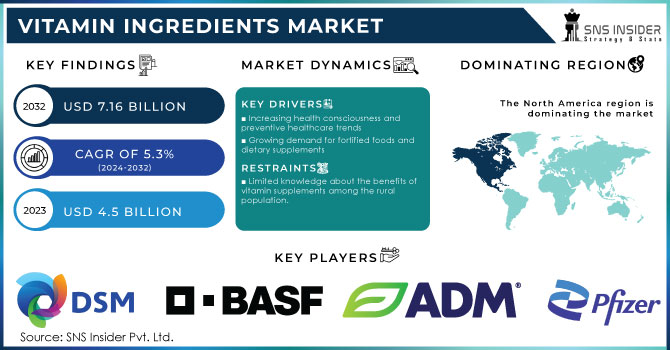

The Vitamin Ingredients Market size was USD 4.5 billion in 2023 and is expected to Reach USD 7.16 billion by 2032 and grow at a CAGR of 5.3% over the forecast period of 2024-2032.

The vitamin ingredients market is experiencing robust growth, driven by increasing health consciousness among consumers and a rising prevalence of vitamin deficiencies globally. This growing demand is further propelled by an aging population more susceptible to deficiencies, as well as the expansion of the nutraceutical and pharmaceutical industries, which utilize vitamins to enhance their products. Recent examples of companies active in the vitamin ingredients market include BASF SE, DSM, and Lonza Group AG.

According to the World Health Organization for International Public Health, chronic diseases kill nearly 41 million people globally each year. People who are vitamin deficient have a weaker immune system and are more prone to chronic disease. The rise in chronic diseases has increased people's need for vitamins, fueling the growth of vitamin ingredients.

Market Dynamics

Drivers

Increasing health consciousness and preventive healthcare trends

Growing demand for fortified foods and dietary supplements

Expanding aging population and associated health concerns

Rising disposable incomes and urbanization

Rising prevalence of lifestyle diseases and vitamin deficiencies

The rising prevalence of lifestyle diseases and vitamin deficiencies is a key driver of the vitamin ingredients market. Sedentary lifestyles, consumption of processed foods, and chronic stress contribute to poor nutritional intake, while micronutrient malnutrition and specific dietary restrictions further exacerbate the problem. With over 2 billion people worldwide suffering from deficiencies, consumers are turning to vitamin supplements to bridge the gap and prevent chronic diseases. product launches like Nestlé's "Garden of Life mykind Organics B-Complex" cater to the rising demand for targeted and plant-based vitamin solutions.

Restraints

Limited knowledge about the benefits of vitamin supplements among the rural population.

High cost of premium vitamin ingredients

Complex and time-consuming approval processes for new vitamin ingredients.

Presence of substandard and adulterated products in the market.

The presence of substandard and adulterated products in the vitamin ingredients market poses a significant restraint on its growth. Counterfeit vitamins, often containing little or no active ingredients, fillers, or even harmful substances, erode consumer trust and undermine the perceived effectiveness of legitimate products. A notable example is the case of counterfeit vitamin D supplements found in the US market in 2019. The Food and Drug Administration (FDA) issued a warning about these products, which contained dangerously high levels of vitamin D, potentially leading to serious health complications. This incident highlights the risks associated with counterfeit vitamins-

Counterfeit vitamins can cause harm due to incorrect dosage, contamination, or the presence of harmful substances.

Widespread counterfeiting undermines consumer trust in the entire vitamin market, making individuals hesitant to purchase any supplements.

Legitimate manufacturers suffer financial losses as counterfeit products divert sales and damage brand reputation.

A study published in the Journal of the American Medical Association found that 20% of herbal supplements tested contained unlisted ingredients, including pharmaceutical drugs.

Opportunities

Innovation in delivery formats and product differentiation

Growing demand for personalized nutrition and customized vitamin solutions

Expansion into emerging markets with increasing health awareness

The rising popularity of clean-label and organic vitamin products

Integration of vitamins into functional foods and beverages

Challenges

Ensuring the quality and safety of vitamin ingredients

Educating consumers about proper dosage and usage

Developing innovative and affordable vitamin formulations

Addressing environmental concerns related to vitamin production

IMPACT OF RUSSIA UKRAINE WAR

Russia's invasion of Ukraine has negatively affected the vitamin ingredients market. Russia and Ukraine are consumers, importers, and exporters of vitamin supplements. Geopolitical instability and sanctions led on Russia by countries had hampered the transport of vitamin materials. GlaxoSmithKline has suspended deliveries of supplements and vitamins into Russia as part of its efforts to cut ties with Moscow following its invasion of Ukraine. They no longer favor global sanctions. This has resulted in a decrease in vitamin supplies in Russia and many other countries. Vitamin supplement prices have risen as a result of this.

Impact of Economic Downturn:

During economic downturns, consumers tend to prioritize essential goods and cut back on discretionary spending, which can include vitamin supplements. Price-sensitive consumers may opt for lower-priced generic or private-label brands over more expensive, branded vitamin supplements. This can intensify competition and pressure profit margins for manufacturers.

Vitamin supplements’ major demand was during Covid-19 followed by Russia Ukraine war. However, the war and sanctions had led to disruption in supply chains. The demand for vitamins in pharmaceuticals is constantly increasing but the prices may fluctuate on the basis of availability of raw materials. The prices of vitamin ingredients could increase by 10-15% during a recession. If there are alternative sources of vitamin ingredients available, the impact on the market is likely to be less severe.

Market segmentation

By Type

Vitamin A

Vitamin B

Vitamin C

Vitamin D

Vitamin E

Vitamin K

By Type, vitamin C held the highest revenue share of more than 32% in 2023. Vitamin C's dominance in the vitamin ingredients market is due to its widespread recognition and diverse applications. Vitamin C is renowned for its immune-boosting properties, antioxidant benefits, and role in collagen synthesis, making it a popular choice for consumers seeking overall health and wellness support.

In Nov 2023, a product launch that exemplifies the continued popularity of vitamin C is the introduction of Lakmé's 9to5 Vitamin C+ range. This range includes a variety of skincare products such as serum, day cream, and night cream, all formulated with vitamin C to address various skin concerns like dullness, uneven skin tone, and signs of aging. This launch aligns with the growing consumer demand for high-quality, effective vitamin C products that offer comprehensive skincare benefits.

By Form

Tablets and Capsules

Powder

Others

By Form, Tablets and Capsules are anticipated to dominate the Vitamin Ingredients Market with the highest revenue share of more than 46.5% in 2023 due to their convenience, stability, variety, and familiarity with consumers. Their portable, pre-measured format requires no preparation, making them ideal for busy lifestyles. This dominance is evident in the recent (Jan 2022) launch of Nature Made's Stress Relief Gummies with Ashwagandha & Vitamin D3, highlighting the ongoing innovation in this format to cater to evolving consumer preferences for convenient and targeted vitamin supplementation.

By Source

Natural

Synthetic

By Application

Food and Beverages

Pharmaceuticals

Animal Feed

Personal Care Products

Others

Regional Analysis

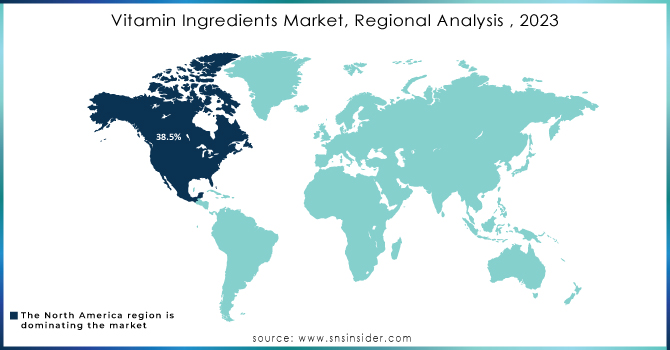

North America led the Vitamin Ingredients Market with the highest revenue share of more than 38.5% in 2023. The region boasts a highly health-conscious population that prioritizes preventive healthcare and wellness, driving a strong demand for vitamin supplements. Additionally, the high prevalence of lifestyle-related diseases like obesity, diabetes, and heart disease in North America further fuels the need for vitamins to address deficiencies and support overall health. A well-established regulatory framework for dietary supplements ensures product safety and quality, fostering consumer trust and confidence in the market. The region's reputation as a hub for research and development in the nutraceutical industry leads to the continuous launch of innovative vitamin products, catering to evolving consumer preferences. The growing aging population also seeks vitamins for healthy aging, bone health, and cognitive function, further contributing to market growth.

March 2022- A recent example of this innovation is Nature Made's launch of their "Wellblends Immune Support with Vitamin C, D3, and Zinc," aligning with consumer interest in preventive health measures.

Asia Pacific is estimated to grow at the highest CAGR during the forecast period from 2024-2031 driven by a rapidly expanding population with increasing disposable income and a growing awareness of preventive healthcare. Changing dietary habits and urbanization have led to imbalanced diets, creating a significant demand for vitamin supplements. Government initiatives promoting nutritional awareness and the rising prevalence of lifestyle diseases further contribute to this demand.

A recent example is Amway India's launch of "Nutrilite Vitamin C Cherry Plus," catering to the growing demand for convenient and palatable vitamin formats. China and India are leading the market due to their large populations and increasing health consciousness.

Need any customization research on Vitamin Ingredients Market - Enquiry Now

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

KEY PLAYERS

Koninklijke DSM N.V., BASF SE, Archer Daniels Midland Company, Pfizer Inc., Nestlé S.A., Evonik Industries AG, Ingredion Incorporated, DuPont de Nemours and Company, Bactolac Pharmaceutical Inc., Lonza Group, AIE Pharmaceuticals Inc., Atlantic Essential Products Inc., Glanbia PLC, Bluestar Adisseo Co., Dow Chemical Company, Probi AB, The Wright Group, CHR Hansen Holding A/S, Nutritional Yeast Company, Algatechnologies Ltd., Amway Corporation, and Kensing Solutions LLC.

Recent Development:

In May 2024, Evonik will be showcasing its latest nutraceutical ingredient innovations at Vitafoods Europe 2024 in Geneva, Switzerland. Among the highlights will be the introduction of AvailOm® & Boswellia for joint health, the presentation of new study results on IN VIVO BIOTICS™, and the expansion of the Healthberry® portfolio into the U.S. market.

In August 2022, Kensing, LLC, a prominent manufacturer of natural vitamin E, plant sterols, specialty esters, and high-purity anionic surfactants, and a portfolio company of One Rock Capital Partners, LLC, announced the acquisition of the amphoteric surfactants and specialty esters manufacturing operations in Hopewell, Virginia from Evonik Corporation.

In July 2022, BASF revealed plans to enhance its presence in the vitamin A market by increasing its formulation capacities at its Verbund site in Ludwigshafen. The cutting-edge facility, fully integrated into vitamin production at the site, will bolster the production of top-quality vitamin A powder products for the animal nutrition industry, reinforcing BASF's commitment to delivering excellence in its offerings.

In 2021, Bain Capital and Cinven completed the acquisition of Lonza Specialty Ingredients (LSI) for CHF 4.2 billion. This acquisition included Lonza's vitamin B3 operations, further expanding LSI's portfolio and market presence.

| Report Attributes | Details |

| Market Size in 2023 | USD 4.5 Billion |

| Market Size by 2032 | USD 7.16 Billion |

| CAGR | CAGR of 5.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Vitamin A, Vitamin B, Vitamin C, Vitamin D, Vitamin E, and Vitamin K) • By Form (Tablets and Capsules, Powder, and Others) • By Source (Natural and Synthetic) • By Application (Food and Beverages, Pharmaceuticals, Animal Feed, Personal Care Products, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Koninklijke DSM N.V., BASF SE, Archer Daniels Midland Company, Pfizer Inc., Nestlé S.A., Evonik Industries AG, Ingredion Incorporated, DuPont de Nemours and Company, Bactolac Pharmaceutical Inc., Lonza Group, AIE Pharmaceuticals Inc., Atlantic Essential Products Inc., Glanbia PLC, Bluestar Adisseo Co., Dow Chemical Company, Probi AB, The Wright Group, CHR Hansen Holding A/S, Nutritional Yeast Company, Algatechnologies Ltd., Amway Corporation, and Kensing Solutions LLC. |

| Key Drivers | • Increasing health consciousness and preventive healthcare trends • Growing demand for fortified foods and dietary supplements • Expanding aging population and associated health concerns • Rising disposable incomes and urbanization • Rising prevalence of lifestyle diseases and vitamin deficiencies |

| Market Restrain | • Limited knowledge about the benefits of vitamin supplements among the rural population. • High cost of premium vitamin ingredients • Complex and time-consuming approval processes for new vitamin ingredients. • Presence of substandard and adulterated products in the market. |

Ans: The Vitamin Ingredients Market was valued at USD 4.5 billion in 2023.

Ans: The expected CAGR of the global Vitamin Ingredients Market during the forecast period is 5.3%.

Ans: The Natural source segment is expected to grow rapidly in the Vitamin Ingredients Market from 2024-2032.

Ans: Stringent regulations, price competition, potential side effects, fluctuating raw material prices, and limited consumer awareness are key factors hindering the growth of the vitamin ingredients market.

Ans: The United States led the Vitamin Ingredients Market in North America region with highest revenue share in 2023.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Vitamin Ingredients Market Segmentation, By Type

9.1 Introduction

9.2 Trend Analysis

9.3 Vitamin A

9.4 Vitamin B

9.5 Vitamin C

9.6 Vitamin D

9.7 Vitamin E

9.8 Vitamin K

10. Vitamin Ingredients Market Segmentation, By Form

10.1 Introduction

10.2 Trend Analysis

10.3 Tablets and Capsules

10.4 Powder

10.5 Others

11. Vitamin Ingredients Market Segmentation, By Source

11.1 Introduction

11.2 Trend Analysis

11.3 Natural

11.4 Synthetic

12. Vitamin Ingredients Market Segmentation, By Application

12.1 Introduction

12.2 Trend Analysis

12.3 Food and Beverages

12.4 Pharmaceuticals

12.5 Animal Feed

12.6 Personal Care Products

12.7 Others

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 Trend Analysis

13.2.2 North America Vitamin Ingredients Market by Country

13.2.3 North America Vitamin Ingredients Market By Type

13.2.4 North America Vitamin Ingredients Market By Form

13.2.5 North America Vitamin Ingredients Market By Source

13.2.6 North America Vitamin Ingredients Market By Application

13.2.7 USA

13.2.7.1 USA Vitamin Ingredients Market By Type

13.2.7.2 USA Vitamin Ingredients Market By Form

13.2.7.3 USA Vitamin Ingredients Market By Source

13.2.7.4 USA Vitamin Ingredients Market By Application

13.2.8 Canada

13.2.8.1 Canada Vitamin Ingredients Market By Type

13.2.8.2 Canada Vitamin Ingredients Market By Form

13.2.8.3 Canada Vitamin Ingredients Market By Source

13.2.8.4 Canada Vitamin Ingredients Market By Application

13.2.9 Mexico

13.2.9.1 Mexico Vitamin Ingredients Market By Type

13.2.9.2 Mexico Vitamin Ingredients Market By Form

13.2.9.3 Mexico Vitamin Ingredients Market By Source

13.2.9.4 Mexico Vitamin Ingredients Market By Application

13.3 Europe

13.3.1 Trend Analysis

13.3.2 Eastern Europe

13.3.2.1 Eastern Europe Vitamin Ingredients Market by Country

13.3.2.2 Eastern Europe Vitamin Ingredients Market By Type

13.3.2.3 Eastern Europe Vitamin Ingredients Market By Form

13.3.2.4 Eastern Europe Vitamin Ingredients Market By Source

13.3.2.5 Eastern Europe Vitamin Ingredients Market By Application

13.3.2.6 Poland

13.3.2.6.1 Poland Vitamin Ingredients Market By Type

13.3.2.6.2 Poland Vitamin Ingredients Market By Form

13.3.2.6.3 Poland Vitamin Ingredients Market By Source

13.3.2.6.4 Poland Vitamin Ingredients Market By Application

13.3.2.7 Romania

13.3.2.7.1 Romania Vitamin Ingredients Market By Type

13.3.2.7.2 Romania Vitamin Ingredients Market By Form

13.3.2.7.3 Romania Vitamin Ingredients Market By Source

13.3.2.7.4 Romania Vitamin Ingredients Market By Application

13.3.2.8 Hungary

13.3.2.8.1 Hungary Vitamin Ingredients Market By Type

13.3.2.8.2 Hungary Vitamin Ingredients Market By Form

13.3.2.8.3 Hungary Vitamin Ingredients Market By Source

13.3.2.8.4 Hungary Vitamin Ingredients Market By Application

13.3.2.9 Turkey

13.3.2.9.1 Turkey Vitamin Ingredients Market By Type

13.3.2.9.2 Turkey Vitamin Ingredients Market By Form

13.3.2.9.3 Turkey Vitamin Ingredients Market By Source

13.3.2.9.4 Turkey Vitamin Ingredients Market By Application

13.3.2.10 Rest of Eastern Europe

13.3.2.10.1 Rest of Eastern Europe Vitamin Ingredients Market By Type

13.3.2.10.2 Rest of Eastern Europe Vitamin Ingredients Market By Form

13.3.2.10.3 Rest of Eastern Europe Vitamin Ingredients Market By Source

13.3.2.10.4 Rest of Eastern Europe Vitamin Ingredients Market By Application

13.3.3 Western Europe

13.3.3.1 Western Europe Vitamin Ingredients Market by Country

13.3.3.2 Western Europe Vitamin Ingredients Market By Type

13.3.3.3 Western Europe Vitamin Ingredients Market By Form

13.3.3.4 Western Europe Vitamin Ingredients Market By Source

13.3.3.5 Western Europe Vitamin Ingredients Market By Application

13.3.3.6 Germany

13.3.3.6.1 Germany Vitamin Ingredients Market By Type

13.3.3.6.2 Germany Vitamin Ingredients Market By Form

13.3.3.6.3 Germany Vitamin Ingredients Market By Source

13.3.3.6.4 Germany Vitamin Ingredients Market By Application

13.3.3.7 France

13.3.3.7.1 France Vitamin Ingredients Market By Type

13.3.3.7.2 France Vitamin Ingredients Market By Form

13.3.3.7.3 France Vitamin Ingredients Market By Source

13.3.3.7.4 France Vitamin Ingredients Market By Application

13.3.3.8 UK

13.3.3.8.1 UK Vitamin Ingredients Market By Type

13.3.3.8.2 UK Vitamin Ingredients Market By Form

13.3.3.8.3 UK Vitamin Ingredients Market By Source

13.3.3.8.4 UK Vitamin Ingredients Market By Application

13.3.3.9 Italy

13.3.3.9.1 Italy Vitamin Ingredients Market By Type

13.3.3.9.2 Italy Vitamin Ingredients Market By Form

13.3.3.9.3 Italy Vitamin Ingredients Market By Source

13.3.3.9.4 Italy Vitamin Ingredients Market By Application

13.3.3.10 Spain

13.3.3.10.1 Spain Vitamin Ingredients Market By Type

13.3.3.10.2 Spain Vitamin Ingredients Market By Form

13.3.3.10.3 Spain Vitamin Ingredients Market By Source

13.3.3.10.4 Spain Vitamin Ingredients Market By Application

13.3.3.11 Netherlands

13.3.3.11.1 Netherlands Vitamin Ingredients Market By Type

13.3.3.11.2 Netherlands Vitamin Ingredients Market By Form

13.3.3.11.3 Netherlands Vitamin Ingredients Market By Source

13.3.3.11.4 Netherlands Vitamin Ingredients Market By Application

13.3.3.12 Switzerland

13.3.3.12.1 Switzerland Vitamin Ingredients Market By Type

13.3.3.12.2 Switzerland Vitamin Ingredients Market By Form

13.3.3.12.3 Switzerland Vitamin Ingredients Market By Source

13.3.3.12.4 Switzerland Vitamin Ingredients Market By Application

13.3.3.13 Austria

13.3.3.13.1 Austria Vitamin Ingredients Market By Type

13.3.3.13.2 Austria Vitamin Ingredients Market By Form

13.3.3.13.3 Austria Vitamin Ingredients Market By Source

13.3.3.13.4 Austria Vitamin Ingredients Market By Application

13.3.3.14 Rest of Western Europe

13.3.3.14.1 Rest of Western Europe Vitamin Ingredients Market By Type

13.3.3.14.2 Rest of Western Europe Vitamin Ingredients Market By Form

13.3.3.14.3 Rest of Western Europe Vitamin Ingredients Market By Source

13.3.3.14.4 Rest of Western Europe Vitamin Ingredients Market By Application

13.4 Asia-Pacific

13.4.1 Trend Analysis

13.4.2 Asia-Pacific Vitamin Ingredients Market by Country

13.4.3 Asia-Pacific Vitamin Ingredients Market By Type

13.4.4 Asia-Pacific Vitamin Ingredients Market By Form

13.4.5 Asia-Pacific Vitamin Ingredients Market By Source

13.4.6 Asia-Pacific Vitamin Ingredients Market By Application

13.4.7 China

13.4.7.1 China Vitamin Ingredients Market By Type

13.4.7.2 China Vitamin Ingredients Market By Form

13.4.7.3 China Vitamin Ingredients Market By Source

13.4.7.4 China Vitamin Ingredients Market By Application

13.4.8 India

13.4.8.1 India Vitamin Ingredients Market By Type

13.4.8.2 India Vitamin Ingredients Market By Form

13.4.8.3 India Vitamin Ingredients Market By Source

13.4.8.4 India Vitamin Ingredients Market By Application

13.4.9 Japan

13.4.9.1 Japan Vitamin Ingredients Market By Type

13.4.9.2 Japan Vitamin Ingredients Market By Form

13.4.9.3 Japan Vitamin Ingredients Market By Source

13.4.9.4 Japan Vitamin Ingredients Market By Application

13.4.10 South Korea

13.4.10.1 South Korea Vitamin Ingredients Market By Type

13.4.10.2 South Korea Vitamin Ingredients Market By Form

13.4.10.3 South Korea Vitamin Ingredients Market By Source

13.4.10.4 South Korea Vitamin Ingredients Market By Application

13.4.11 Vietnam

13.4.11.1 Vietnam Vitamin Ingredients Market By Type

13.4.11.2 Vietnam Vitamin Ingredients Market By Form

13.4.11.3 Vietnam Vitamin Ingredients Market By Source

13.4.11.4 Vietnam Vitamin Ingredients Market By Application

13.4.12 Singapore

13.4.12.1 Singapore Vitamin Ingredients Market By Type

13.4.12.2 Singapore Vitamin Ingredients Market By Form

13.4.12.3 Singapore Vitamin Ingredients Market By Source

13.4.12.4 Singapore Vitamin Ingredients Market By Application

13.4.13 Australia

13.4.13.1 Australia Vitamin Ingredients Market By Type

13.4.13.2 Australia Vitamin Ingredients Market By Form

13.4.13.3 Australia Vitamin Ingredients Market By Source

13.4.13.4 Australia Vitamin Ingredients Market By Application

13.4.14 Rest of Asia-Pacific

13.4.14.1 Rest of Asia-Pacific Vitamin Ingredients Market By Type

13.4.14.2 Rest of Asia-Pacific Vitamin Ingredients Market By Form

13.4.14.3 Rest of Asia-Pacific Vitamin Ingredients Market By Source

13.4.14.4 Rest of Asia-Pacific Vitamin Ingredients Market By Application

13.5 Middle East & Africa

13.5.1 Trend Analysis

13.5.2 Middle East

13.5.2.1 Middle East Vitamin Ingredients Market by Country

13.5.2.2 Middle East Vitamin Ingredients Market By Type

13.5.2.3 Middle East Vitamin Ingredients Market By Form

13.5.2.4 Middle East Vitamin Ingredients Market By Source

13.5.2.5 Middle East Vitamin Ingredients Market By Application

13.5.2.6 UAE

13.5.2.6.1 UAE Vitamin Ingredients Market By Type

13.5.2.6.2 UAE Vitamin Ingredients Market By Form

13.5.2.6.3 UAE Vitamin Ingredients Market By Source

13.5.2.6.4 UAE Vitamin Ingredients Market By Application

13.5.2.7 Egypt

13.5.2.7.1 Egypt Vitamin Ingredients Market By Type

13.5.2.7.2 Egypt Vitamin Ingredients Market By Form

13.5.2.7.3 Egypt Vitamin Ingredients Market By Source

13.5.2.7.4 Egypt Vitamin Ingredients Market By Application

13.5.2.8 Saudi Arabia

13.5.2.8.1 Saudi Arabia Vitamin Ingredients Market By Type

13.5.2.8.2 Saudi Arabia Vitamin Ingredients Market By Form

13.5.2.8.3 Saudi Arabia Vitamin Ingredients Market By Source

13.5.2.8.4 Saudi Arabia Vitamin Ingredients Market By Application

13.5.2.9 Qatar

13.5.2.9.1 Qatar Vitamin Ingredients Market By Type

13.5.2.9.2 Qatar Vitamin Ingredients Market By Form

13.5.2.9.3 Qatar Vitamin Ingredients Market By Source

13.5.2.9.4 Qatar Vitamin Ingredients Market By Application

13.5.2.10 Rest of Middle East

13.5.2.10.1 Rest of Middle East Vitamin Ingredients Market By Type

13.5.2.10.2 Rest of Middle East Vitamin Ingredients Market By Form

13.5.2.10.3 Rest of Middle East Vitamin Ingredients Market By Source

13.5.2.10.4 Rest of Middle East Vitamin Ingredients Market By Application

13.5.3 Africa

13.5.3.1 Africa Vitamin Ingredients Market by Country

13.5.3.2 Africa Vitamin Ingredients Market By Type

13.5.3.3 Africa Vitamin Ingredients Market By Form

13.5.3.4 Africa Vitamin Ingredients Market By Source

13.5.3.5 Africa Vitamin Ingredients Market By Application

13.5.3.6 Nigeria

13.5.3.6.1 Nigeria Vitamin Ingredients Market By Type

13.5.3.6.2 Nigeria Vitamin Ingredients Market By Form

13.5.3.6.3 Nigeria Vitamin Ingredients Market By Source

13.5.3.6.4 Nigeria Vitamin Ingredients Market By Application

13.5.3.7 South Africa

13.5.3.7.1 South Africa Vitamin Ingredients Market By Type

13.5.3.7.2 South Africa Vitamin Ingredients Market By Form

13.5.3.7.3 South Africa Vitamin Ingredients Market By Source

13.5.3.7.4 South Africa Vitamin Ingredients Market By Application

13.5.3.8 Rest of Africa

13.5.3.8.1 Rest of Africa Vitamin Ingredients Market By Type

13.5.3.8.2 Rest of Africa Vitamin Ingredients Market By Form

13.5.3.8.3 Rest of Africa Vitamin Ingredients Market By Source

13.5.3.8.4 Rest of Africa Vitamin Ingredients Market By Application

13.6 Latin America

13.6.1 Trend Analysis

13.6.2 Latin America Vitamin Ingredients Market by Country

13.6.3 Latin America Vitamin Ingredients Market By Type

13.6.4 Latin America Vitamin Ingredients Market By Form

13.6.5 Latin America Vitamin Ingredients Market By Source

13.6.6 Latin America Vitamin Ingredients Market By Application

13.6.7 Brazil

13.6.7.1 Brazil Vitamin Ingredients Market By Type

13.6.7.2 Brazil Vitamin Ingredients Market By Form

13.6.7.3 Brazil Vitamin Ingredients Market By Source

13.6.7.4 Brazil Vitamin Ingredients Market By Application

13.6.8 Argentina

13.6.8.1 Argentina Vitamin Ingredients Market By Type

13.6.8.2 Argentina Vitamin Ingredients Market By Form

13.6.8.3 Argentina Vitamin Ingredients Market By Source

13.6.8.4 Argentina Vitamin Ingredients Market By Application

13.6.9 Colombia

13.6.9.1 Colombia Vitamin Ingredients Market By Type

13.6.9.2 Colombia Vitamin Ingredients Market By Form

13.6.9.3 Colombia Vitamin Ingredients Market By Source

13.6.9.4 Colombia Vitamin Ingredients Market By Application

13.6.10 Rest of Latin America

13.6.10.1 Rest of Latin America Vitamin Ingredients Market By Type

13.6.10.2 Rest of Latin America Vitamin Ingredients Market By Form

13.6.10.3 Rest of Latin America Vitamin Ingredients Market By Source

13.6.10.4 Rest of Latin America Vitamin Ingredients Market By Application

14. Company Profiles

14.1 Koninklijke DSM N.V.

14.1.1 Company Overview

14.1.2 Financial

14.1.3 Products/ Services Offered

14.1.4 SWOT Analysis

14.1.5 The SNS View

14.2 BASF SE

14.2.1 Company Overview

14.2.2 Financial

14.2.3 Products/ Services Offered

14.2.4 SWOT Analysis

14.2.5 The SNS View

14.3 Archer Daniels Midland Company

14.3.1 Company Overview

14.3.2 Financial

14.3.3 Products/ Services Offered

14.3.4 SWOT Analysis

14.3.5 The SNS View

14.4 Pfizer Inc.

14.4.1 Company Overview

14.4.2 Financial

14.4.3 Products/ Services Offered

14.4.4 SWOT Analysis

14.4.5 The SNS View

14.5 Nestlé S.A.

14.5.1 Company Overview

14.5.2 Financial

14.5.3 Products/ Services Offered

14.5.4 SWOT Analysis

14.5.5 The SNS View

14.6 Evonik Industries AG

14.6.1 Company Overview

14.6.2 Financial

14.6.3 Products/ Services Offered

14.6.4 SWOT Analysis

14.6.5 The SNS View

14.7 Ingredion Incorporated

14.7.1 Company Overview

14.7.2 Financial

14.7.3 Products/ Services Offered

14.7.4 SWOT Analysis

14.7.5 The SNS View

14.8 DuPont de Nemours and Company

14.8.1 Company Overview

14.8.2 Financial

14.8.3 Products/ Services Offered

14.8.4 SWOT Analysis

14.8.5 The SNS View

14.9 Bactolac Pharmaceutical Inc.

14.9.1 Company Overview

14.9.2 Financial

14.9.3 Products/ Services Offered

14.9.4 SWOT Analysis

14.9.5 The SNS View

14.10 Lonza Group

14.10.1 Company Overview

14.10.2 Financial

14.10.3 Products/ Services Offered

14.10.4 SWOT Analysis

14.10.5 The SNS View

14.11 AIE Pharmaceuticals Inc.

14.11.1 Company Overview

14.11.2 Financial

14.11.3 Products/ Services Offered

14.11.4 SWOT Analysis

14.11.5 The SNS View

14.12 Atlantic Essential Products Inc.

14.12.1 Company Overview

14.12.2 Financial

14.12.3 Products/ Services Offered

14.12.4 SWOT Analysis

14.12.5 The SNS View

14.13 Glanbia PLC

14.13.1 Company Overview

14.13.2 Financial

14.13.3 Products/ Services Offered

14.13.4 SWOT Analysis

14.13.5 The SNS View

14.14 Bluestar Adisseo Co.

14.14.1 Company Overview

14.14.2 Financial

14.14.3 Products/ Services Offered

14.14.4 SWOT Analysis

14.14.5 The SNS View

14.15 Dow Chemical Company

14.15.1 Company Overview

14.15.2 Financial

14.15.3 Products/ Services Offered

14.15.4 SWOT Analysis

14.15.5 The SNS View

14.16 Probi AB

14.16.1 Company Overview

14.16.2 Financial

14.16.3 Products/ Services Offered

14.16.4 SWOT Analysis

14.16.5 The SNS View

14.17 The Wright Group

14.17.1 Company Overview

14.17.2 Financial

14.17.3 Products/ Services Offered

14.17.4 SWOT Analysis

14.17.5 The SNS View

14.18 CHR Hansen Holding A/S

14.18.1 Company Overview

14.18.2 Financial

14.18.3 Products/ Services Offered

14.18.4 SWOT Analysis

14.18.5 The SNS View

14.19 Nutritional Yeast Company

14.19.1 Company Overview

14.19.2 Financial

14.19.3 Products/ Services Offered

14.19.4 SWOT Analysis

14.19.5 The SNS View

14.20 Algatechnologies Ltd.

14.20.1 Company Overview

14.20.2 Financial

14.20.3 Products/ Services Offered

14.20.4 SWOT Analysis

14.20.5 The SNS View

14.21 Amway Corporation

14.21.1 Company Overview

14.21.2 Financial

14.21.3 Products/ Services Offered

14.21.4 SWOT Analysis

14.21.5 The SNS View

14.22 Kensing Solutions LLC

14.22.1 Company Overview

14.22.2 Financial

14.22.3 Products/ Services Offered

14.22.4 SWOT Analysis

14.22.5 The SNS View

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

15.3.1 Industry News

15.3.2 Company News

15.3.3 Mergers & Acquisitions

16. Use Case and Best Practices

17. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Peppermint Tea Market size was USD 205.5 million in 2022 and is expected to Reach USD 308.2 million by 2030 and grow at a CAGR of 5.2% over the forecast period of 2023-2030.

Carob Chocolate Market Report Scope & Overview: The Carob Chocolate Market Size was esteemed

The Food Certification Market size was valued at USD 5.49 billion in 2023 and is expected to grow to USD 9.01 billion by 2032, at a CAGR of 5.69% over the forecast period of 2024-2032.

The Industrial Sugar Market Size was esteemed at USD 30.94 billion out of 2022 and is supposed to arrive at USD 41.83 billion by 2030 and develop at a CAGR of 3.84% over the forecast period 2023-2030.

Convenience Stores Market Report Scope & Overview: Convenience Stores Market Siz

The Craft Wine Market size was valued at USD 40.14 billion in 2023 and is expected to reach USD 58.63 billion by 2032 and grow at a CAGR of 5.32% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd