Ventricular Assist Device Market Size Analysis:

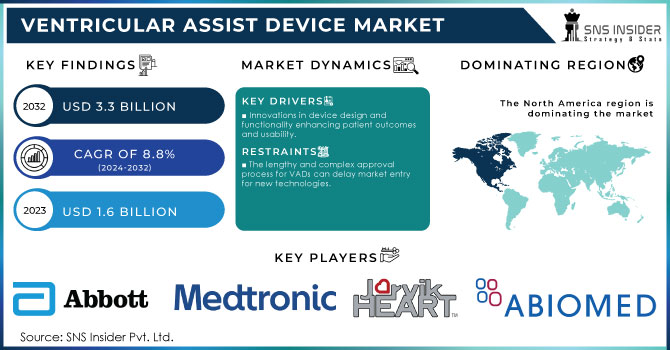

The Ventricular Assist Device Market Size was valued at USD 1.6 billion in 2023 and is expected to reach USD 3.3 billion by 2032, growing at a CAGR of 8.8% from 2024-2032.

Get More Information on Ventricular Assist Device Market - Request Sample Report

The ventricular assist device market is expanding rapidly owing to a rising incidence rate of heart failure and technological progress in the medical field. One of the leading drivers of this market expansion is the increase in cases of heart failure. Over 26 million people globally have heart failure, and over 50 % will die within five years of their initial diagnosis. Furthermore, as the population continues to age, the prevalence of cardiovascular diseases is on the rise, and it is expected that more than 8 million adults in the U.S. will have heart failure by 2030. Technological advancements such as miniaturization, increased biocompatibility, and enhanced device durability is also driving the exploitation of those current market opportunities.

Moreover, the prominent factor is that newer models of VADs show improved patient outcomes and are more straightforward to consider. As a result, both healthcare providers and their patients are increasingly embracing the use of this device. Remarkably, there is increased education campaigns about VADs, and subsequent demonstration of best patient outcomes is influencing the acceptance of these devices. Additionally, the increasing application of VADs apart from only serving as a bridge for heart transplants has increased the opportunity. Some of these applications include providing long-term therapy to patients who require it but not fit for surgery.

Over the years, there has been an increase in investment in medical-device-specified venture capital. As a result, these investments are now pushing the research and the eventual development of the next-generation VADs. All of these factors combined, are likely to justify the VAD market's explosive growth and its classification as one of the most crucial fields in the cardiovascular device market. Overall, the evolution of VADs will soon become the essential battlefield in health systems worldwide aimed at addressing heart failure.

Here's a table that illustrates how research and development (R&D) investments contribute to the growth of the Ventricular Assist Device (VAD) market:

| Research & Development Focus Area | Impact on VAD Market | Examples of Outcomes |

|---|---|---|

| Innovative Technologies | Enhances device performance and patient outcomes | Development of next-generation VADs with improved efficiency and reliability. |

| Biocompatible Materials | Reduces risk of complications and increases device longevity | Research into new materials that minimize blood clots and infection rates. |

| Miniaturization | Expands patient eligibility and usability | Creation of smaller, lighter devices suitable for a wider range of patients. |

| Integration with Wearable Tech | Allows for real-time monitoring and patient management | Development of VADs with integrated sensors for remote monitoring of patient health. |

| Long-term Studies | Validates safety and effectiveness over extended periods | Clinical trials demonstrating improved survival rates and quality of life for VAD patients. |

| Regulatory Compliance | Ensures devices meet safety standards and gain market approval | Research focused on regulatory requirements for faster approval processes. |

| Funding and Investment | Provides resources for cutting-edge research initiatives | Increased venture capital funding supporting innovative VAD development projects. |

Global Ventricular Assist Device Market Dynamics

Drivers

-

Innovations in device design and functionality enhancing patient outcomes and usability.

-

Growing elderly demographics leading to higher cardiovascular disease rates.

-

Rising venture capital and funding for the development of advanced VAD technologies.

The key driving factors that are stimulating the growth in the VAD market include the rising amount of venture capital and funding for more advanced ventricular assist devices. Currently, heart failure is one of the most important global problems due to the high morbidity and mortality rates among the affected individuals. However, presently, investors realize the great potential in terms of VD innovation due to the number of start-ups and well-known companies that are supported with considerable investments for the development of new, more potent devices. The funding assists in carrying out research in the sphere of the quality and safety improvements delivered by advancing technological devices. Furthermore, with the help of financial support, companies and labs can design smaller VADs with more biocompatible properties. This effect is achieved due to the development of modern modeling and information technology along with more advanced materials used for this type of device creation. An increasing number of VADs are made in a way to reduce complications such as thrombosis and infection. Additionally, the funds are used for clinical trials confirming the device’s efficacy after trying such technologies on various patient groups.

Moreover, elderly demographics positively impact ventricular assist device-related demand. The present aging population in developed and developing countries increases the prevalence of heart failure, a cardiovascular disease common in the elderly population. Life expectancy is anticipated to rise significantly considering it has already been impressively improved across the world. The global population aged 65 and over will grow by 2050 and amount to 1.5 billion people. Age is the most significant risk factor for heart failure, with a very rapid rise in heart failure in the advanced age. Therefore, the global need for revolutionary heart failure treatment options will essentially increase. VADs are widely used to remove the heightened rate and flush heart conditions in older patient groups. In several cases, especially when dealing with a high-risk patient group for transplantation such as the elderly, the VAD can act as a long-term solution. This growing demand condition has serious implications for the healthcare systems of the world where specific demographics stimulate market growth. Such an approach increases healthcare system support for innovative VAD technologies.

Restraints

-

The lengthy and complex approval process for VADs can delay market entry for new technologies.

-

Current devices may face issues with biocompatibility, size, and power supply, affecting usability and comfort.

-

Lack of awareness about VAD options among patients and healthcare professionals can hinder adoption.

The lack of awareness about ventricular assist devices is a substantial factor that affects the adoption of this technology in the market. Few patients with advanced heart failure are not familiar with the use of VADs. According to a study in the Journal of Cardiac Failure, about 40% of patients with advanced heart failure don’t get any information about VADs. Undoubtedly, these patients miss an excellent opportunity to benefit from a potentially life-saving therapy. The lack of awareness can also be related to healthcare providers. For instance, another study results show that only 30% of primary care providers report being well-informed regarding the latest VAD technology. The lack of information can lead to the inability to refer patients to the necessary specialists who can provide a complete evaluation and determine whether a patient is a candidate for VAD use. On the other hand, it can be suggested that healthcare providers familiar with the technology could also have incorrect information. For example, according to McNitt et al., there are many misconceptions about the benefits as well as risks associated with VAD therapy. Addressing these awareness gaps is essential for driving growth in the VAD sector and ensuring that more patients benefit from this advanced treatment option.

Ventricular Assist Device Market Segmentation Analysis

By Product

In 2023, the Left Ventricular Assist Devices (LVAD) segment led the market, accounting for more than 83.5% of the revenue. The total ventricular assist device market is expected to grow at a CAGR of 17.5% between 2021 and 2028. The rise can be associated with a large number of LVAD implantations in failing heart patients. Abbott had implanted its HEARTMATE II LVAD in over 26,600 patients across the globe. Moreover, according to a report by the American College of Cardiology, readmissions after LVAD implantation are typically costly and lengthier hospitalizations. The population of patients with late-stage heart failure is growing as therapeutic alternatives remain minimal, and as a result, the VAD market is rapidly rising. In addition, based on a report by the American Heart Association, LVAD patients’ functionality, welfare, and lifespan have also significantly improved, enhancing the rate of adoption. In addition, market participants are increasingly focusing on integrating and working with one another in order to deal with the organ shortage crisis and meet the current heightened demand for LVADs, especially for patients awaiting transplants.

| Type of VAD | Usage | Advantages | Limitations | Ideal Patient Profile |

|---|---|---|---|---|

|

Left Ventricular Assist Device (LVAD) |

Supports the left ventricle in pumping blood |

Most commonly used; effective in end-stage heart failure |

Risk of infection and bleeding; requires surgery |

Patients with weakened left heart function, often awaiting a heart transplant |

|

Right Ventricular Assist Device (RVAD) |

Supports the right ventricle in pumping blood |

Useful for patients with right heart failure |

Shorter-term support, less common |

Patients with acute right ventricular failure, typically post-cardiac surgery |

|

Biventricular Assist Device (BiVAD) |

Supports both left and right ventricles |

Provides complete heart support |

Highly invasive, complex surgery, higher cost |

Patients with severe heart failure affecting both ventricles |

|

Total Artificial Heart (TAH) |

Replaces both heart ventricles entirely |

Life-saving for patients not eligible for transplant |

Limited durability, external power source needed |

Patients with end-stage heart failure, no transplant options |

Moreover, on the other hand, the Bi-Ventricular Assist Devices will be the fastest-growing segment at a CAGR of 23.7% over the forecast period. This is attributed to their excellent effectiveness in total artificial heart transplantation.

By Type of flow

In 2023, the non-pulsatile or continuous flow segment led the VAD market, capturing 89.9% of the revenue share due to the advantages these devices offer over pulsatile VADs. Continuous flow VADs are increasingly being adopted with earlier generation VADs, as continuous flow VADs produce very minimal noise, and wear significantly fewer parts, requiring less maintenance and replacements. Such benefits have led to a continuous flow of VADs to be the sought-after treatment option, preferred by most medical researchers and physicians. Moreover, current product development in the continuous flow VAD type aims to make use of even fewer parts.

The pulsatile flow VAD segment is expected to witness the fastest growth during the forecast period. The rising incidences of heart failure and cardiovascular diseases have significantly added to the growth of this market. Pulsatile flow is a crucial factor in the ventricular assist device market, as it is as it is synonymous with the human heartbeat, and provides better hemodynamics, and therefore organs receive natural blood perfusion. Moreover, due to this, the outcomes of the devices that use pulsatile flow in bettering patient outcomes are seen to be fewer complications caused by the non-pulsatile systems. The ventricular assist device market is currently witnessing higher demands for pulsatile, technologically advanced systems that can provide cardiac support that ranges from temporary to long-term. The trend today in the VAD market shows a progressive shift towards physiologic support in the field of mechanical circulatory support.

By Design

In 2023, the implantable devices segment dominated the VAD market, capturing a significant revenue share of 75.8%. This growth is driven by long-term therapy options for patients ineligible for heart transplants. Some of the new players in the market specialize in offering a wide range of innovative solutions. FineHeart SARL, for example, is currently developing a unique novel pump in a single compact, fully implanted pulsatile-flow VAD. Another example is Abbott’s HeartMate 3 LVAD. It is the most widely used VAD with its FDA approval and its MagLev technology reduces blood damage with flow optimization. Also, implantable devices will be the fastest-growing segment during the forecast period.

By Application

In 2023, the destination therapy segment led the VAD market, accounting for more than 43.1% of the revenue. The destination therapy segment is projected to maintain the highest growth, primarily due to the surging rates of end-stage heart failure and cardiovascular diseases. Moreover, this segment is expanding owing to the high number of patients who cannot receive a heart transplant. The top leading companies in this market include Jarvik Heart Inc., Abbott, and Medtronic, and numerous of their elements are under FDA approval. Furthermore, the bridge to transplantation segment is expected to exhibit a higher CAGR for the given period. The VADs are installed in the patients for a temporary basis, about 2 to 6 months, to stabilize the patient before a transplant surgery. The adoption of VADs is increasing because it is highly effective and technological advancements, alongside fewer complications related to VADs.

Regional Insights

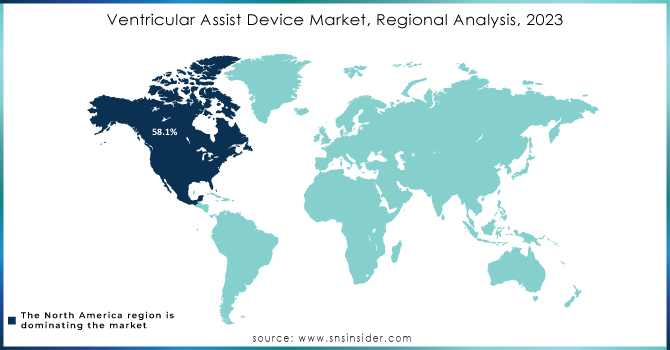

North America led the ventricular assist devices (VAD) market in 2023, holding 58.1% of the revenue share. This growth is driven by the controlled reimbursement policies, awareness of available VAD options such as bridge-to-recovery, destination therapy, and bridge-to-transplant, and a high obesity rate in the U.S. Obesity is a risk factor for heart disease, which is expected to push the need for mounted assist devices. The presence of advanced healthcare facilities in the U.S. is likely to increase treatment procedures, aiding market growth. Also, the region thrives based on insurance scheme policies that are relatively friendly to consumers to protect them from out-of-pocket expenses.

The Asia-Pacific region is expected to experience the fastest growth in the Ventricular Assist Device market, driven by a combination of technological advancements, an increasing burden of cardiovascular diseases, and expanding healthcare infrastructure. Countries like China, Japan, India, and South Korea are witnessing a rise in demand for VADs due to a growing aging population and the high prevalence of heart failure. The region benefits from substantial investments in medical technology, with governments and private sectors focusing on enhancing healthcare capabilities and improving access to advanced treatments. Furthermore, the rise of medical tourism in countries like India and Thailand is contributing to the adoption of VADs as more patients seek affordable, high-quality medical care.

Need any customization research on Ventricular Assist Devices (VAD) market - Enquiry Now

Ventricular Assist Device Market Key Players

The major key players are

-

Abbott Laboratories – (HeartMate 3 LVAD, HeartMate II LVAD)

-

Medtronic – (HVAD System, Medtronic Cardiac Resynchronization Therapy (CRT))

-

Jarvik Heart Inc. – (Jarvik 2000 LVAD, Jarvik 15mm Pediatric VAD)

-

Berlin Heart GmbH – (EXCOR Adult, EXCOR Pediatric)

-

Abiomed – (Impella 2.5, Impella CP)

-

Terumo Corporation – (DuraHeart LVAD, CAPIOX heart-lung machines)

-

Getinge AB – (Cardiohelp System, Rotaflow Centrifugal Pump)

-

LivaNova PLC – (HeartWare HVAD, Perceval Sutureless Heart Valve)

-

ReliantHeart Inc. – (HeartAssist 5 LVAD, aVAD LVAD)

-

Sun Medical Technology Research Corp. – (Toyobo LVAD, SM-LVAD System)

-

CorWave – (CorWave LVAD, CorWave membrane pump technology)

-

Evaheart, Inc. – (EVAHEART LVAD, EVAHEART 2 LVAD)

-

SynCardia Systems, LLC – (SynCardia Total Artificial Heart, SynCardia Freedom Portable Driver)

-

CardiacAssist, Inc. (TandemLife) – (TandemHeart System, LifeSPARC System)

-

NuPulseCV – (iVAS (intravascular ventricular assist system) iVAS Portable System)

-

Calon Cardio-Technology Ltd. – (MiniVAD LVAD, Calon VAD Platform)

-

Miromatrix Medical Inc.-(Bioengineered LVAD, Biomimetic Cardiac Devices)

-

CARMAT – (CARMAT Total Artificial Heart, CARMAT Hybrid Heart)

-

Windmill Cardiovascular Systems – (HeartLander LVAD, Percutaneous VAD)

-

Cirtec Medical – (VAD Engineering & Development Services, Cirtec’s Neuromodulation and Cardiac Medical Devices)

Recent Developments in the Ventricular Assist Device Market

In November 2022, Jarvik Heart, Inc. carried out a clinical trial for their ventricular assist device, Jarvik 2015, to boost their product lineup.

In September 2022, Abbott acquired Walk Vascular, LLC, a company that makes a minimally invasive system to remove blood clots using mechanical aspiration.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 1.6 billion |

| Market Size by 2032 | US$ 3.3 billion |

| CAGR | CAGR of 8.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Bridge to Transplant, Destination Therapy, Others) • By Product (Left Ventricular Assist Device, Right Ventricular Assist Device, Bi-Ventricular Assist Device, Total Artificial Heart) • By Type of Flow (Pulsatile Flow, Continuous Flow) • By Design(Implantable Ventricular Assist Device, Transcutaneous Ventricular Assist Device) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Baxter International, Pfize, Abbott Laboratories, AstraZeneca, Fresenius Kabi, Hospira, Teva Pharmaceuticals, Mylan, Merck & Co., GlaxoSmithKline, Sanofi & Other Players |

| Key Drivers | • Innovations in device design and functionality enhancing patient outcomes and usability. • Growing elderly demographics leading to higher cardiovascular disease rates. • Rising venture capital and funding for the development of advanced VAD technologies. |

| Market Restraints | • The lengthy and complex approval process for VADs can delay market entry for new technologies. • Current devices may face issues with biocompatibility, size, and power supply, affecting usability and comfort. • Lack of awareness about VAD options among patients and healthcare professionals can hinder adoption. |