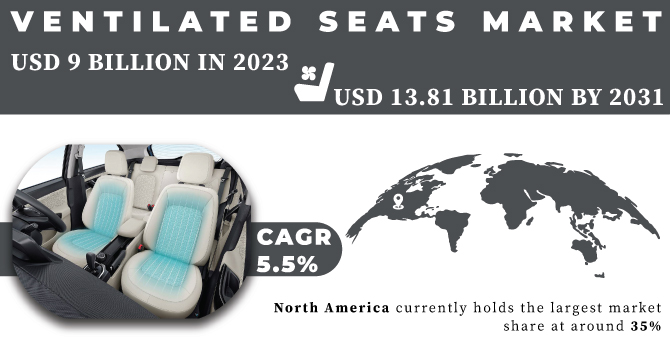

The Ventilated Seats Market Size was valued at USD 9 billion in 2023 and is expected to reach USD 14.57 billion by 2032 and grow at a CAGR of 5.5% over the forecast period 2024-2032

The demand for ventilated seats is being driven by a several of factors that prioritize comfort and luxury in the automotive industry. With rising global temperatures exceeding 40°C in some regions, staying cool behind the wheel is a growing concern for consumers. This is particularly true for long commutes or hot climates, where traditional seating can lead to discomfort and sweat. There's a marked shift in consumer preferences towards premium car features. A 2023 study found that 71% of global consumers are willing to pay extra for features that enhance comfort and convenience. Ventilated seats directly address this desire by providing a constant airflow, keeping occupants cool and dry.

Get More Information on Ventilated Seats Market - Request Sample Report

Car manufacturers are increasingly incorporating ventilated seats into mid-range and even entry-level vehicles to remain competitive. This wider adoption is driven by advancements in ventilation technology that make it more affordable to integrate into various car models. Interestingly, government initiatives promoting fuel efficiency may also play a role. Ventilated seats can be more energy-efficient than cranking up the air conditioning, potentially appealing to eco-conscious consumers and aligning with government regulations. As a result, the demand for ventilated seats is expected to rise steadily, solidifying their position as a sought-after comfort feature in the modern automobile.

MARKET DYNAMICS:

KEY DRIVERS:

The increase in consumer desire for luxury and comfy seating

An increase in the no. of automobiles in the mid-segment vehicles that include ventilated seats

The dramatic increase in the number of sales of passenger vehicles

An increase in money generated per individual will drive the market for automobile ventilated seats

The use of low-VOC TDI in automobile seats is becoming more common

Demand for chairs and covers is on the rise

Driven by a dramatic rise in passenger car sales, the ventilated seats market is experiencing a boom. Estimates indicate a near doubling of SUVs sold globally in recent years, accounting for almost half of all car sales in the US and a third in Europe. This surge in passenger vehicle ownership, particularly in hotter climates, translates to a growing consumer base seeking the comfort and convenience of ventilated seats. This technology, once confined to luxury vehicles, is now increasingly incorporated into mid-range and even entry-level cars, further propelling the ventilated seats market forward.

RESTRAINTS:

The market is predicted to grow at a slower pace because of the high costs of sophisticated seats

Variations in local climate limit its expansion

OPPORTUNITIES:

Inventions in technology have progressed

Urbanization has increased in recent decades and affordable financing options are readily available

The global market is likely to benefit from new developments in the seat design.

While urbanization has surged in recent decades, with the United Nations estimating 68% of the world's population living in cities by 2050, concerns about affordability persist. However, this trend is coupled with a rise in accessible financing options like government grants and low-interest loans. This, along with a projected 72% increase in global passenger vehicle sales by 2030, suggests a growing demand for features that enhance comfort and fuel efficiency, potentially creating a fertile market for ventilated car seats.

CHALLENGES:

Uncertainty over the demand and supply network for makers of automobile ventilated seats

Vehicle obsolescence and its accompanying rising depreciation rates are major challenges in the market

The war in Ukraine has affected the ventilated seats market, disrupting both supply and demand. Disruptions to global chip production, heavily reliant on neon gas from Ukraine, could increase component costs by up to 20% according to industry estimates. This, coupled with rising overall material costs due to the war's impact on oil prices, could translate to a 5-10% price hike for ventilated seats for car manufacturers. On the demand side, consumer confidence in war-torn Europe is likely to dampen sales of luxury features like ventilated seats, potentially leading to a 3-5% decrease in demand in the region. This could be partially offset by growth in other regions, but the overall impact on the market remains uncertain. The war's long-term influence on ventilated seat technology advancements and production costs is yet to be seen.

An economic slowdown can put the brakes on the ventilated seat market, impacting both consumer demand and manufacturer enthusiasm. During economic downturns, discretionary spending on car features tends to decline by 10-15%. This can lead to carmakers prioritizing standard features over luxury ones like ventilated seats, potentially reducing their installation rates in new models.

Additionally, with rising interest rates and overall economic uncertainty, consumers might opt for base trims or delay car purchases altogether, further impacting demand. This could be particularly impactful for high-end car segments where ventilated seats are more common. However, there's a potential silver lining. As consumers seek value during economic hardship, ventilated seats can be seen as an attractive upgrade that enhances comfort without significantly impacting fuel efficiency compared to running the air conditioner constantly.

MARKET SEGMENTATION:

Ventilated Seats Market by Sales Channel

OEM

Aftermarket

As of 2023, the Aftermarket segment holds the share at 35%. This is particularly strong in developing economies where affordability and retrofitting drive demand. However, the OEM segment is dominating the segment by holding a 65% share due to a rising preference for comfort features like ventilated seats, especially with increasing travel times and longer commutes. This trend is encouraged by a growing focus on luxury and premium car features, driven by rising disposable income.

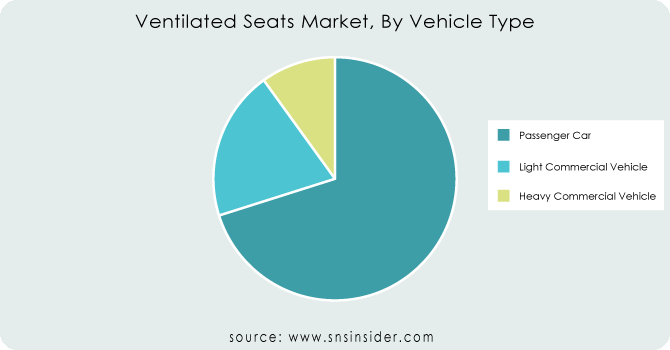

Ventilated Seats Market by Vehicle Type

Passenger Car

Light Commercial Vehicle

Heavy Commercial Vehicle

The ventilated seats market thrives on the backs of different vehicle types, each with its own growth path. Passenger cars, holding the largest share at 70.4%, are driven by rising demand for comfort features in sedans, from mid-range to luxury. This dominance reflects the focus on personal transportation and extended commutes. Light Commercial Vehicles (LCVs), at a smaller percentage, are expected to see stable growth. Factors like increasing urbanization and demand for last-mile delivery services will influence LCV adoption of ventilated seats.

The most interesting segment is Heavy Commercial Vehicles (HCVs), currently the smallest but holding the fastest growth rate around 7.3% CAGR. Stringent regulations for driver comfort and longer haul routes in hot climates are driving the rise of ventilated seats in HCVs, making the way for a more significant market share in the coming years.

Get Customized Report as per your Business Requirement - Request For Customized Report

Ventilated Seats Market by Propulsion

ICE Vehicle

Electric Vehicle

Battery Electric Vehicle

Plug-in Electric Vehicle

Hybrid Electric Vehicle

REGIONAL ANALYSIS:

The global ventilated seats market is driven by regional preferences for comfort and luxury. North America currently holds the largest market share at around 35%, likely due to established consumer demand for feature-rich vehicles and hot summer climates. However, the Asia-Pacific region is experiencing the fastest growth at a CAGR exceeding 7%. This rise is driven by a booming automotive industry, rising disposable incomes, and a growing preference for premium car features.

Interestingly, developing and emerging nations within this region are expected to witness an even steeper rise, potentially reaching a 10% CAGR by 2031. This can be attributed to government initiatives promoting domestic car manufacturing and a growing middle class with an increased desire for comfort and convenience. These trends indicate a significant shift in the ventilated seats market landscape, with developing regions becoming major players in the coming years.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

KEY PLAYERS:

Continental AG (Germany), Ford, Lear Corporation (US), Adient plc (US), Toyota Boshoku Corporation (Japan), Magna International Inc. (Canada), Gentherm (US), Dura Automotive Systems (US), Ebm Papst Group (Germany), NHK Spring CO. Ltd (Japan), Faurecia SA (France), Brose Fahrzeugteile GmbH &Co., (Germany), Dura Automotive Systems (US), and TS Tech Co., Ltd (Japan), are some of the affluent competitors with significant market share in the Ventilated Seats Market.

In March 2022, Faurecia, a major automotive supplier, inaugurated its Technology & Customer Center to focus on innovation in this area. This move signals their intent to stay ahead of the curve.

Established companies like Toyota Boshoku are focusing on premium offerings. Their ventilated seats and door trims, featured in the January 2022 launch of the Lexus LX, showcase this approach.

Lear Corporation is expanding its reach through acquisitions. In October 2021, they acquired Kongsberg Automotive's Interior Comfort Systems business unit, solidifying their position in the market.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 9 Billion |

| Market Size by 2032 | US$ 14.57 Billion |

| CAGR | CAGR of 5.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments |

|

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Continental AG (Germany), Ford, Lear Corporation (US), Adient plc (US), Toyota Boshoku Corporation (Japan), Magna International Inc. (Canada), Gentherm (US), Dura Automotive Systems (US), Ebm Papst Group (Germany), NHK Spring CO. Ltd (Japan), Faurecia SA (France), Brose Fahrzeugteile GmbH &Co., (Germany), Dura Automotive Systems (US), and TS Tech Co., Ltd (Japan), are some of the affluent competitors with significant market share in the Ventilated Seats Market. |

| Key Drivers | •The increase in consumer desire for luxury and comfy seating. •An increase in the no. of automobiles in the mid-segment vehicles that include ventilated seats. |

| RESTRAINTS | •The market is predicted to grow at a slower pace because of the high costs of sophisticated seats. •Variations in local climate limit its expansion. |

The Ventilated Seats Market Size was valued at USD 9 billion in 2023.

The growth rate of the Ventilated Seats Market is a CAGR of 5.5% over the forecast period 2024-2031.

The forecast period for the Ventilated Seats Market is 2024-2031

North America region is dominating the Ventilated Seats Market.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Ventilated Seats Market Segmentation, By Sales Channel

9.1 Introduction

9.2 Trend Analysis

9.3 On-Car Ventilated Seats

9.4 Off-Car Ventilated Seats

10. Ventilated Seats Market Segmentation, By Vehicle Type

10.1 Introduction

10.2 Trend Analysis

10.3 Passenger Car

10.4 Light Commercial Vehicle

10.5 Heavy Commercial Vehicle

11. Ventilated Seats Market Segmentation, By Propulsion

11.1 Introduction

11.2 Trend Analysis

11.3 Internal Combustion Engine

11.4 Electric Vehicle

11.5 Heavy-Duty

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America Ventilated Seats Market by Country

12.2.3 North America Ventilated Seats Market By Sales Channel

12.2.4 North America Ventilated Seats Market By Vehicle Type

12.2.5 North America Ventilated Seats Market By Propulsion

12.2.6 USA

12.2.6.1 USA Ventilated Seats Market By Sales Channel

12.2.6.2 USA Ventilated Seats Market By Vehicle Type

12.2.6.3 USA Ventilated Seats Market By Propulsion

12.2.7 Canada

12.2.7.1 Canada Ventilated Seats Market By Sales Channel

12.2.7.2 Canada Ventilated Seats Market By Vehicle Type

12.2.7.3 Canada Ventilated Seats Market By Propulsion

12.2.8 Mexico

12.2.8.1 Mexico Ventilated Seats Market By Sales Channel

12.2.8.2 Mexico Ventilated Seats Market By Vehicle Type

12.2.8.3 Mexico Ventilated Seats Market By Propulsion

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe Ventilated Seats Market by Country

12.3.2.2 Eastern Europe Ventilated Seats Market By Sales Channel

12.3.2.3 Eastern Europe Ventilated Seats Market By Vehicle Type

12.3.2.4 Eastern Europe Ventilated Seats Market By Propulsion

12.3.2.5 Poland

12.3.2.5.1 Poland Ventilated Seats Market By Sales Channel

12.3.2.5.2 Poland Ventilated Seats Market By Vehicle Type

12.3.2.5.3 Poland Ventilated Seats Market By Propulsion

12.3.2.6 Romania

12.3.2.6.1 Romania Ventilated Seats Market By Sales Channel

12.3.2.6.2 Romania Ventilated Seats Market By Vehicle Type

12.3.2.6.4 Romania Ventilated Seats Market By Propulsion

12.3.2.7 Hungary

12.3.2.7.1 Hungary Ventilated Seats Market By Sales Channel

12.3.2.7.2 Hungary Ventilated Seats Market By Vehicle Type

12.3.2.7.3 Hungary Ventilated Seats Market By Propulsion

12.3.2.8 Turkey

12.3.2.8.1 Turkey Ventilated Seats Market By Sales Channel

12.3.2.8.2 Turkey Ventilated Seats Market By Vehicle Type

12.3.2.8.3 Turkey Ventilated Seats Market By Propulsion

12.3.2.9 Rest of Eastern Europe

12.3.2.9.1 Rest of Eastern Europe Ventilated Seats Market By Sales Channel

12.3.2.9.2 Rest of Eastern Europe Ventilated Seats Market By Vehicle Type

12.3.2.9.3 Rest of Eastern Europe Ventilated Seats Market By Propulsion

12.3.3 Western Europe

12.3.3.1 Western Europe Ventilated Seats Market by Country

12.3.3.2 Western Europe Ventilated Seats Market By Sales Channel

12.3.3.3 Western Europe Ventilated Seats Market By Vehicle Type

12.3.3.4 Western Europe Ventilated Seats Market By Propulsion

12.3.3.5 Germany

12.3.3.5.1 Germany Ventilated Seats Market By Sales Channel

12.3.3.5.2 Germany Ventilated Seats Market By Vehicle Type

12.3.3.5.3 Germany Ventilated Seats Market By Propulsion

12.3.3.6 France

12.3.3.6.1 France Ventilated Seats Market By Sales Channel

12.3.3.6.2 France Ventilated Seats Market By Vehicle Type

12.3.3.6.3 France Ventilated Seats Market By Propulsion

12.3.3.7 UK

12.3.3.7.1 UK Ventilated Seats Market By Sales Channel

12.3.3.7.2 UK Ventilated Seats Market By Vehicle Type

12.3.3.7.3 UK Ventilated Seats Market By Propulsion

12.3.3.8 Italy

12.3.3.8.1 Italy Ventilated Seats Market By Sales Channel

12.3.3.8.2 Italy Ventilated Seats Market By Vehicle Type

12.3.3.8.3 Italy Ventilated Seats Market By Propulsion

12.3.3.9 Spain

12.3.3.9.1 Spain Ventilated Seats Market By Sales Channel

12.3.3.9.2 Spain Ventilated Seats Market By Vehicle Type

12.3.3.9.3 Spain Ventilated Seats Market By Propulsion

12.3.3.10 Netherlands

12.3.3.10.1 Netherlands Ventilated Seats Market By Sales Channel

12.3.3.10.2 Netherlands Ventilated Seats Market By Vehicle Type

12.3.3.10.3 Netherlands Ventilated Seats Market By Propulsion

12.3.3.11 Switzerland

12.3.3.11.1 Switzerland Ventilated Seats Market By Sales Channel

12.3.3.11.2 Switzerland Ventilated Seats Market By Vehicle Type

12.3.3.11.3 Switzerland Ventilated Seats Market By Propulsion

12.3.3.1.12 Austria

12.3.3.12.1 Austria Ventilated Seats Market By Sales Channel

12.3.3.12.2 Austria Ventilated Seats Market By Vehicle Type

12.3.3.12.3 Austria Ventilated Seats Market By Propulsion

12.3.3.13 Rest of Western Europe

12.3.3.13.1 Rest of Western Europe Ventilated Seats Market By Sales Channel

12.3.3.13.2 Rest of Western Europe Ventilated Seats Market By Vehicle Type

12.3.3.13.3 Rest of Western Europe Ventilated Seats Market By Propulsion

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific Ventilated Seats Market by Country

12.4.3 Asia-Pacific Ventilated Seats Market By Sales Channel

12.4.4 Asia-Pacific Ventilated Seats Market By Vehicle Type

12.4.5 Asia-Pacific Ventilated Seats Market By Propulsion

12.4.6 China

12.4.6.1 China Ventilated Seats Market By Sales Channel

12.4.6.2 China Ventilated Seats Market By Vehicle Type

12.4.6.3 China Ventilated Seats Market By Propulsion

12.4.7 India

12.4.7.1 India Ventilated Seats Market By Sales Channel

12.4.7.2 India Ventilated Seats Market By Vehicle Type

12.4.7.3 India Ventilated Seats Market By Propulsion

12.4.8 Japan

12.4.8.1 Japan Ventilated Seats Market By Sales Channel

12.4.8.2 Japan Ventilated Seats Market By Vehicle Type

12.4.8.3 Japan Ventilated Seats Market By Propulsion

12.4.9 South Korea

12.4.9.1 South Korea Ventilated Seats Market By Sales Channel

12.4.9.2 South Korea Ventilated Seats Market By Vehicle Type

12.4.9.3 South Korea Ventilated Seats Market By Propulsion

12.4.10 Vietnam

12.4.10.1 Vietnam Ventilated Seats Market By Sales Channel

12.4.10.2 Vietnam Ventilated Seats Market By Vehicle Type

12.4.10.3 Vietnam Ventilated Seats Market By Propulsion

12.4.11 Singapore

12.4.11.1 Singapore Ventilated Seats Market By Sales Channel

12.4.11.2 Singapore Ventilated Seats Market By Vehicle Type

12.4.11.3 Singapore Ventilated Seats Market By Propulsion

12.4.12 Australia

12.4.12.1 Australia Ventilated Seats Market By Sales Channel

12.4.12.2 Australia Ventilated Seats Market By Vehicle Type

12.4.12.3 Australia Ventilated Seats Market By Propulsion

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Ventilated Seats Market By Sales Channel

12.4.13.2 Rest of Asia-Pacific Ventilated Seats Market By Vehicle Type

12.4.13.3 Rest of Asia-Pacific Ventilated Seats Market By Propulsion

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East Ventilated Seats Market by Country

12.5.2.2 Middle East Ventilated Seats Market By Sales Channel

12.5.2.3 Middle East Ventilated Seats Market By Vehicle Type

12.5.2.4 Middle East Ventilated Seats Market By Propulsion

12.5.2.5 UAE

12.5.2.5.1 UAE Ventilated Seats Market By Sales Channel

12.5.2.5.2 UAE Ventilated Seats Market By Vehicle Type

12.5.2.5.3 UAE Ventilated Seats Market By Propulsion

12.5.2.6 Egypt

12.5.2.6.1 Egypt Ventilated Seats Market By Sales Channel

12.5.2.6.2 Egypt Ventilated Seats Market By Vehicle Type

12.5.2.6.3 Egypt Ventilated Seats Market By Propulsion

12.5.2.7 Saudi Arabia

12.5.2.7.1 Saudi Arabia Ventilated Seats Market By Sales Channel

12.5.2.7.2 Saudi Arabia Ventilated Seats Market By Vehicle Type

12.5.2.7.3 Saudi Arabia Ventilated Seats Market By Propulsion

12.5.2.8 Qatar

12.5.2.8.1 Qatar Ventilated Seats Market By Sales Channel

12.5.2.8.2 Qatar Ventilated Seats Market By Vehicle Type

12.5.2.8.3 Qatar Ventilated Seats Market By Propulsion

12.5.2.9 Rest of Middle East

12.5.2.9.1 Rest of Middle East Ventilated Seats Market By Sales Channel

12.5.2.9.2 Rest of Middle East Ventilated Seats Market By Vehicle Type

12.5.2.9.3 Rest of Middle East Ventilated Seats Market By Propulsion

12.5.3 Africa

12.5.3.1 Africa Ventilated Seats Market by Country

12.5.3.2 Africa Ventilated Seats Market By Sales Channel

12.5.3.3 Africa Ventilated Seats Market By Vehicle Type

12.5.3.4 Africa Ventilated Seats Market By Propulsion

12.5.3.5 Nigeria

12.5.3.5.1 Nigeria Ventilated Seats Market By Sales Channel

12.5.3.5.2 Nigeria Ventilated Seats Market By Vehicle Type

12.5.3.5.3 Nigeria Ventilated Seats Market By Propulsion

12.5.3.6 South Africa

12.5.3.6.1 South Africa Ventilated Seats Market By Sales Channel

12.5.3.6.2 South Africa Ventilated Seats Market By Vehicle Type

12.5.3.6.3 South Africa Ventilated Seats Market By Propulsion

12.5.3.7 Rest of Africa

12.5.3.7.1 Rest of Africa Ventilated Seats Market By Sales Channel

12.5.3.7.2 Rest of Africa Ventilated Seats Market By Vehicle Type

12.5.3.7.3 Rest of Africa Ventilated Seats Market By Propulsion

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America Ventilated Seats Market by country

12.6.3 Latin America Ventilated Seats Market By Sales Channel

12.6.4 Latin America Ventilated Seats Market By Vehicle Type

12.6.5 Latin America Ventilated Seats Market By Propulsion

12.6.6 Brazil

12.6.6.1 Brazil Ventilated Seats Market By Sales Channel

12.6.6.2 Brazil Ventilated Seats Market By Vehicle Type

12.6.6.3 Brazil Ventilated Seats Market By Propulsion

12.6.7 Argentina

12.6.7.1 Argentina Ventilated Seats Market By Sales Channel

12.6.7.2 Argentina Ventilated Seats Market By Vehicle Type

12.6.7.3 Argentina Ventilated Seats Market By Propulsion

12.6.8 Colombia

12.6.8.1 Colombia Ventilated Seats Market By Sales Channel

12.6.8.2 Colombia Ventilated Seats Market By Vehicle Type

12.6.8.3 Colombia Ventilated Seats Market By Propulsion

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Ventilated Seats Market By Sales Channel

12.6.9.2 Rest of Latin America Ventilated Seats Market By Vehicle Type

12.6.9.3 Rest of Latin America Ventilated Seats Market By Propulsion

13. Company Profiles

13.1 Continental AG (Germany)

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Products/ Services Offered

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 Lear Corporation (US)

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Products/ Services Offered

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 Ford

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Products/ Services Offered

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Toyota Boshoku Corporation (Japan)

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Products/ Services Offered

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 Magna International Inc. (Canada)

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Products/ Services Offered

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 Gentherm (US)

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Products/ Services Offered

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Dura Automotive Systems (US)

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Products/ Services Offered

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 Ebm Papst Group (Germany)

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Products/ Services Offered

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 NHK Spring CO. Ltd (Japan)

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Products/ Services Offered

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 Others

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Products/ Services Offered

13.10.4 SWOT Analysis

13.10.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Low-Speed Vehicle Market size was valued at USD 10.55 billion in 2023, and is expected to reach USD 19.31 billion by 2032, and grow at a CAGR of 6.25% over the forecast period 2024-2032.

The Automotive Actuators Market Size was USD 20.3 Billion in 2023 and is expected to reach USD 32.4 Bn by 2032, growing at a CAGR of 5.34% by 2024-2032.

The Airless Tires Market Size was valued at USD 38.85 million in 2023 and is expected to reach USD 63.44 million by 2032 and grow at a CAGR of 5.6% over the forecast period 2024-2032.

Automotive Airbag Market Size was valued at USD 19.84 Billion in 2023 and is expected to reach USD 36.66 Billion by 2032 and grow at a CAGR of 7.09% over the forecast period 2024-2032.

Automotive Filters Market Size was valued at USD 21.28 billion in 2023 and is expected to reach USD 28.15 billion by 2031 and grow at a CAGR of 3.78% over the forecast period 2024-2031.

The Automotive Electric Drive Axle Market Size was USD 11.33 Billion in 2023 and will reach USD 48.20 Bn by 2032 and grow at a CAGR of 17.46% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd