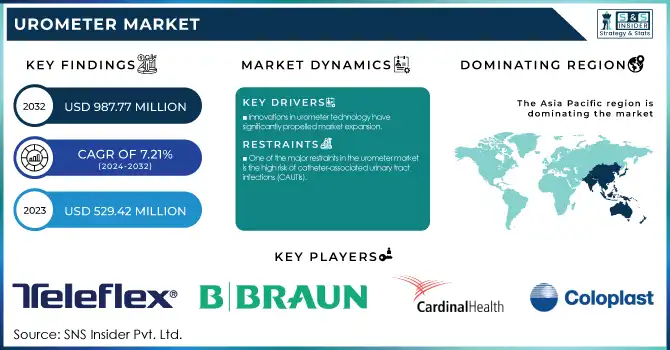

The Urometer Market was valued at USD 529.42 million in 2023 and is expected to reach USD 987.77 million by 2032, growing at a CAGR of 7.21% from 2024 to 2032.

To Get more information on Urometer Market - Request Free Sample Report

The Urometer Market report includes an in-depth analysis of the incidence and prevalence rates of conditions like kidney disease and catheter-associated infections, and it presents regional patient demographic insights. It features an overview of urometer trends in the usage between operative procedures, emergency trauma care, and palliative care, with a comparative regional classification. The study encompasses urometer sales volume and market penetration, highlighting adoption patterns in hospitals, clinics, and home healthcare. It also features healthcare spending insights differentiating between government, commercial, private, and out-of-pocket payments on urine output monitoring solutions, which makes this report distinct in terms of the breadth of statistical analysis.

Drivers

The increasing incidence of urological conditions, such as kidney stones, urinary tract infections (UTIs), and bladder dysfunctions, is a significant driver for the urometer market.

The rise in the prevalence of urological diseases like kidney stones, urinary tract infections (UTIs), and bladder dysfunctions is a major growth impetus for the urometer market. These conditions require the precise measurement of urine output to evaluate renal function and fluid status and thus render urometers indispensable for both diagnostic and therapeutic applications. The growing population of older population worldwide also heightens the incidence of these conditions, with elderly people being more prone to urological ailments. Moreover, unhealthy lifestyles, improper diet, and increasing obesity rates lead to an increased rate of urinary complications. Medical facilities globally are increasingly turning to sophisticated urometers for better patient care and enhanced diagnostic accuracy. Increasing demand for minimally invasive and effective urine monitoring technologies further propels innovation and accelerates the use of urometers in hospitals, clinics, and home healthcare.

Innovations in urometer technology have significantly propelled market expansion.

Advancements in the technology of urometers have largely driven market growth. The invention of disposable urometers solved problems related to cross-contamination and infection control, thus contributing to increased adoption within clinical environments. Additionally, the incorporation of electronic medical records (EMRs) into urometer equipment has facilitated efficient data capture and analysis, enhancing clinical decision-making. Intelligent urometers with real-time tracking capabilities are emerging as users can efficiently monitor patient information. Furthermore, developments in the field of material science have resulted in the manufacture of lightweight, easy-to-use, and longer-lasting urometers, improving patient comfort. The increasing use of automation in hospitals as well as home healthcare has driven the market for sophisticated urometers, as well. Because healthcare professionals are looking for efficiency and safety with growing concerns for patient well-being, an ongoing development in urometer technology will drive the growth in the market.

Restraint

One of the major restraints in the urometer market is the high risk of catheter-associated urinary tract infections (CAUTIs).

One of the greatest limitations in the urometer industry is the great potential for catheter-associated urinary tract infections (CAUTIs). Because urometers are utilized mostly in conjunction with urinary catheters to monitor fluid, long-term catheterization presents an increased chance for bacterial infection and complications, including sepsis, pyelonephritis, and prolonged hospitalization. CAUTIs have been found to cause a considerable number of hospital-acquired infections (HAIs), which is of concern to healthcare professionals and regulatory agencies. This has led to strict infection control measures and catheterization standards, limiting the extensive use of urometers. Moreover, patient discomfort and the potential for biofilm on catheters also discourage their long-term use. The growing demand for non-invasive urine monitoring devices and stringent regulatory norms could hamper the expansion of the urometer market in the forecast years.

Opportunities

The increasing preference for home-based healthcare presents a significant growth opportunity for the urometer market.

The growing demand for home healthcare offers a major opportunity for growth of the urometer market. Due to the increased geriatric population and the incidence of chronic conditions like kidney disorders and urinary incontinence, there is increased demand for comfortable and effective devices for monitoring urine output that can be utilized beyond hospital environments. Home healthcare diminishes hospital readmissions, reduces healthcare expenditure, and enhances patient comfort. Moreover, innovation in handheld and intelligent urometers with wireless connectivity and live monitoring capabilities is facilitating remote monitoring by patients and caregivers. Integration of digital health solutions like telemedicine and remote patient monitoring supports the adoption of home-use urometers as well. With healthcare systems moving toward decentralized care models, this segment will experience significant growth.

Challenges

One of the key challenges facing the urometer market is the complex regulatory landscape and strict compliance requirements.

One of the biggest challenges for the urometer market is the multiplicity of regulatory frameworks and strict compliance. Because urometers qualify as medical devices, manufacturers have to meet strict guidelines from regulatory organizations like the U.S. FDA, European Medicines Agency (EMA), and other local health agencies. Safety, sterility, and performance standards compliance entails rigorous testing, clinical trials, and documentation that results in exorbitant expenses and lengthy approval processes. Furthermore, constant regulatory updates necessitate that producers regularly change and validate their products, which may be time-consuming. Small and medium-sized firms, especially, might not be able to comply with these strict conditions, restricting their market entry and growth. The regulatory barriers not only delay product innovation but also affect the overall development and accessibility of sophisticated urometer solutions in various geographies.

By Product

The 500 ml segment dominated the urometer market with a 37.16% market share in 2023 because of its extensive adoption in hospitals, intensive care units (ICUs), and long-term care centers. This capacity is favored to monitor urine output precisely in seriously ill patients, especially those going through major operations, trauma rehabilitation, or extensive post-operative therapy. The bigger volume provides round-the-clock monitoring even for prolonged duration without regular draining, thereby diminishing the likelihood of urine spilling and providing a clean environment. It also conserves nursing effort by enabling attendants to monitor fluid balance effectively, which is important in averting dehydration, renal failure, and other such complications.

500 ml urometers are extensively used in closed urinary drainage systems, which are critical to infection control and preventing catheter-associated urinary tract infections (CAUTIs). Their usability with different Foley catheter configurations and patient safety regulatory focus further add to their dominance. The increasing number of hospitalizations for chronic kidney diseases, urinary incontinence, and post-operative care also raised the demand for high-capacity urometers. With better healthcare infrastructure and increased adoption in developing markets, the 500 ml segment continues to be the most popular option among acute and long-term patient care environments.

By Application

The Operative Procedures segment dominated the urometer market with the highest market share in 2023 because of the extensive adoption of urometers in surgery and post-surgery environments. Throughout complex operations, like abdominal, urological, cardiovascular, and orthopedic operations, continuous monitoring of urine output is vital in evaluating kidney performance, fluid balance, and overall patient stability. Urometers are what surgical centers and hospitals use to accurately monitor urine output, which facilitates anesthesiologists and surgeons to make decisions in real time. Increasing numbers of elective and emergency procedures, along with an aging population with chronic diseases prone to surgical interventions, considerably increased the demand for urometers. Further, stringent infection control guidelines and innovations in closed urinary drainage systems enhanced the utilization of urometers in surgical treatment. Increasing patient safety and postoperative monitoring focus helped ensure that this segment remained the leading one in 2023.

The Emergency Trauma segment is anticipated to grow the fastest in the urometer market because of increasing cases of road accidents, industrial injuries, and severe trauma requiring urgent medical care. Precise measurement of urine output is crucial in emergency care for the determination of trauma severity, control of shock, and monitoring of fluid resuscitation therapy. As more people become aware of rapid response and critical care protocols, trauma centers and hospitals are giving priority to effective urine output monitoring to improve patient outcomes. Moreover, the rising incidence of emergency admissions due to natural disasters, falls, and violence-related trauma is also propelling demand for urometers in trauma care. Technology developments, like smart and portable urometers for monitoring urine output in real-time, will drive market growth in this segment in the forecast period.

By End-Use

The Hospital segment accounted for the majority of the urometer market share in 2023 as a result of the large number of inpatient admissions, surgeries, and intensive care cases necessitating continuous monitoring of urine output. Hospitals are central points for treating severe illnesses, post-operative recovery, and critical trauma cases, all of which need precise fluid balance monitoring. Urometers are common in ICUs, general wards, and surgical departments to monitor urine output among renal patients, cardiovascular patients, and post-surgical patients. The prevention of hospital-acquired infection (HAI) has also led to the use of closed-system urometers to avoid catheter-associated urinary tract infections (CAUTIs). With improvements in hospital facilities, rising healthcare investments, and more surgeries being conducted globally, hospitals were still the leading end-use environment for urometers in 2023.

The Home Healthcare segment is forecast to register the fastest growth rate during the forecasted years based on the increased demand for patient care at home, particularly among the elderly and chronically ill patients. With a growing inclination towards value-based healthcare paradigms, patients and caregivers prefer home-use of medical devices like portable urometers for handling chronic kidney disease, urinary incontinence, and recovery following surgery without numerous hospital readmissions. Technology growth like remote-monitored smart urometers further facilitates convenience while tracking urine output at home. Supportive health policies, growing insurance coverage for home care treatments, and a surge in telemedicine usage are also driving the growth of this segment. As healthcare systems keep focusing on cost-efficient and patient-centric care, demand for home-use urometers is witness to grow in the future.

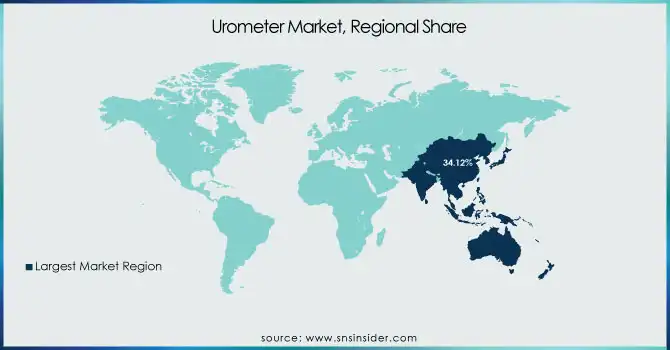

Asia Pacific dominated the urometer market with around 34.12% market share in 2023 because of its aging and high population, high incidence of chronic kidney diseases, and growing healthcare infrastructure. China, India, and Japan are experiencing a sharp rise in hospitalization cases of urological conditions, which is promoting the demand for urine output monitors. Government support for enhancing access to healthcare, along with investments in medical device production, have also contributed largely to market growth. The availability of dominant regional manufacturers of affordable urometer solutions still augments Asia Pacific's market presence. Furthermore, the greater frequency of operations in need of post-operative fluid management and higher awareness for the health of urinary tracts has ensured widespread adoption of urometers within hospitals as well as home care environments throughout the region.

The North American region is growing significantly in the urometer market as a result of its well-developed health care infrastructure, strong implementation of new medical technologies, and rising prevalence of chronic diseases like diabetes and kidney diseases. Major market players, along with ongoing product innovations such as smart urometers with real-time tracking, are driving market growth. In addition, the growing demand for home healthcare, as a result of an aging population and the trend toward value-based care, is fuelling demand for portable and easy-to-use urometer products. Favorable regulatory support toward enhancing patient care standards and robust reimbursement policies help boost market growth within the region. The increasing focus on infection control and the introduction of closed-system urometers to minimize catheter-associated infections (CAUTIs) are also among the major drivers of market adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

BD (Becton, Dickinson and Company) (BD Urometer System, BD Urine Meter)

Medline Industries, Inc. (Medline Urometer with Anti-Reflux Chamber, Medline Urine Drainage Bag with Meter)

Teleflex Incorporated (Rüsch Urine Meter Foley Catheter Tray, Rüsch EasyTap Leg Bag System)

B. Braun Melsungen AG (B. Braun Urimed 24-Hour Urine Meter, B. Braun Urimed Closed Urine Drainage System)

Cardinal Health, Inc. (Cardinal Health Urometer Foley Tray, Cardinal Health Urine Meter Drainage Bag)

Cook Medical (Cook Universal Ureteral Catheter, Cook Percutaneous Urinary Drainage Set)

Amsino International, Inc. (Amsino AMSure Urine Meter, Amsino AMSure Urinary Drainage Bag)

Hollister Incorporated (Hollister Urinary Leg Bag, Hollister Bedside Drainage Bag with Meter)

Coloplast (Coloplast Conveen Security+ Urine Meter, Coloplast Conveen Standard Urine Bag)

Medtronic plc (Covidien Argyle Urine Meter, Covidien Dover Urine Drainage Bag)

ConvaTec Group plc (ConvaTec Flexi-Seal SIGNAL Fecal Management System, ConvaTec Esteem+ Flex Convex Drainable Pouch)

Flexicare Medical Limited (Flexicare Urimeter 500, Flexicare Leg Bag System)

Nipro Medical Corporation (Nipro Urine Meter, Nipro Urinary Drainage Bag)

Vyaire Medical Inc. (AirLife Closed Suction System, AirLife Open Suction Catheter)

Amecath (Amecath Urine Meter Foley Catheter, Amecath Urinary Drainage Bag)

CooperSurgical, Inc. (Wallach Biovac Suction Pump, RUMI II Uterine Manipulator)

Prosurgics Limited (Prosurgics Urine Meter, Prosurgics Drainage Bag)

Mediplus (Mediplus UroMeter, Mediplus Urinary Drainage System)

Halyard Health, Inc. (Halyard Closed Suction System, Halyard Urine Meter Foley Tray)

Smiths Medical (Smiths Medical CADD Infusion Pump, Smiths Medical Pneupac Transport Ventilator)

Suppliers (These suppliers play a significant role in the urometer market, offering products designed for accurate urine output measurement and effective patient care.) in Urometer Market.

Angiplast Pvt. Ltd.

Dispowell Surgicals

Advin Health Care

Labtron

Oracle Medical Supplies

Medikabazaar

Advino Healthcare

SurgiKart India

Angiplast Pvt. Ltd. (Duplicate entry, please replace)

Labtron Equipment Ltd.

In April 2024, Cook Medical launched the Ascend Single-Use Flexible Ureteroscope in the United States and Canada. The new product supports Cook Medical's capability to reach more urology customers by adding its broad portfolio of stone management products.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 529.42 million |

| Market Size by 2032 | US$ 987.77 million |

| CAGR | CAGR of 7.21% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (100 ml, 200 ml, 400 ml, 450 ml, 500 ml) • By Application (Operative Procedures, Emergency Trauma, Palliative Care, Others) • By End-use (Hospital, Clinics, Home Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BD (Becton, Dickinson and Company), Medline Industries, Inc., Teleflex Incorporated, B. Braun Melsungen AG, Cardinal Health, Inc., Cook Medical, Amsino International, Inc., Hollister Incorporated, Coloplast, Medtronic plc, ConvaTec Group plc, Flexicare Medical Limited, Nipro Medical Corporation, Vyaire Medical Inc., Amecath, CooperSurgical, Inc., Prosurgics Limited, Mediplus, Halyard Health, Inc., Smiths Medical, and other players. |

Ans: The Urometer Market is expected to grow at a CAGR of 7.21% during 2024-2032.

Ans: The Urometer Market was USD 529.42 million in 2023 and is expected to reach USD 987.77 million by 2032.

Ans: The increasing incidence of urological conditions, such as kidney stones, urinary tract infections (UTIs), and bladder dysfunctions, is a significant driver for the urometer market.

Ans: The “500 ml” segment dominated the Urometer Market.

Ans: Asia Pacific dominated the Urometer Market in 2023.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence of Urinary Disorders (2023)

5.2 Urometer Utilization Trends, by Application (2023), by Region

5.3 Urometer Sales Volume and Market Penetration, by Region (2020-2032)

5.4 Healthcare Expenditure on Urometer-Based Urine Output Monitoring, by Region (2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Urometer Market Segmentation, By Product

7.1 Chapter Overview

7.2 100 ml

7.2.1 100 ml Market Trends Analysis (2020-2032)

7.2.2 100 ml Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 200 ml

7.3.1 200 ml Market Trends Analysis (2020-2032)

7.3.2 200 ml Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 400 ml

7.4.1 400 ml Market Trends Analysis (2020-2032)

7.4.2 400 ml Market Size Estimates and Forecasts to 2032 (USD Million)

7.5 450 ml

7.5.1 450 ml Market Trends Analysis (2020-2032)

7.5.2 450 ml Market Size Estimates and Forecasts to 2032 (USD Million)

7.6 500 ml

7.6.1 500 ml Market Trends Analysis (2020-2032)

7.6.2 500 ml Market Size Estimates and Forecasts to 2032 (USD Million)

8. Urometer Market Segmentation, By Application

8.1 Chapter Overview

8.2 Operative Procedures

8.2.1 Operative Procedures Market Trends Analysis (2020-2032)

8.2.2 Operative Procedures Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Emergency Trauma

8.3.1 Emergency Trauma Market Trends Analysis (2020-2032)

8.3.2 Emergency Trauma Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Palliative Care

8.4.1 Palliative Care Market Trends Analysis (2020-2032)

8.4.2 Palliative Care Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 Others

8.5.1 Others Market Trends Analysis (2020-2032)

8.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

9. Urometer Market Segmentation by End User

9.1 Chapter Overview

9.2 Hospitals

9.2.1 Hospitals Market Trends Analysis (2020-2032)

9.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Home Healthcare

9.3.1 Home Healthcare Market Trends Analysis (2020-2032)

9.3.2 Home Healthcare Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Others

9.4.1 Others Market Trends Analysis (2020-2032)

9.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.2.3 North America Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.2.4 North America Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.5 North America Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.6 USA

10.2.6.1 USA Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.2.6.2 USA Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.6.3 USA Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.7 Canada

10.2.7.1 Canada Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.2.7.2 Canada Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.7.3 Canada Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.8 Mexico

10.2.8.1 Mexico Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.2.8.2 Mexico Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.8.3 Mexico Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.1.3 Eastern Europe Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.4 Eastern Europe Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.5 Eastern Europe Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.6 Poland

10.3.1.6.1 Poland Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.6.2 Poland Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.6.3 Poland Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.7 Romania

10.3.1.7.1 Romania Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.7.2 Romania Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.7.3 Romania Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.8.2 Hungary Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.8.3 Hungary Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.9.2 Turkey Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.9.3 Turkey Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.1.10.2 Rest of Eastern Europe Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.10.3 Rest of Eastern Europe Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.2.3 Western Europe Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.4 Western Europe Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.5 Western Europe Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.6 Germany

10.3.2.6.1 Germany Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.6.2 Germany Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.6.3 Germany Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.7 France

10.3.2.7.1 France Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.7.2 France Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.7.3 France Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.8 UK

10.3.2.8.1 UK Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.8.2 UK Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.8.3 UK Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.9 Italy

10.3.2.9.1 Italy Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.9.2 Italy Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.9.3 Italy Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.10 Spain

10.3.2.10.1 Spain Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.10.2 Spain Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.10.3 Spain Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.11.2 Netherlands Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.11.3 Netherlands Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.12.2 Switzerland Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.12.3 Switzerland Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.13 Austria

10.3.2.13.1 Austria Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.13.2 Austria Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.13.3 Austria Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.3.2.14.2 Rest of Western Europe Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.14.3 Rest of Western Europe Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.4.3 Asia Pacific Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.4 Asia Pacific Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.5 Asia Pacific Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.6 China

10.4.6.1 China Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.6.2 China Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.6.3 China Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.7 India

10.4.7.1 India Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.7.2 India Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.7.3 India Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.8 Japan

10.4.8.1 Japan Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.8.2 Japan Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.8.3 Japan Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.9 South Korea

10.4.9.1 South Korea Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.9.2 South Korea Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.9.3 South Korea Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.10 Vietnam

10.4.10.1 Vietnam Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.10.2 Vietnam Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.10.3 Vietnam Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.11 Singapore

10.4.11.1 Singapore Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.11.2 Singapore Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.11.3 Singapore Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.12 Australia

10.4.12.1 Australia Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.12.2 Australia Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.12.3 Australia Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.4.13.2 Rest of Asia Pacific Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.13.3 Rest of Asia Pacific Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.1.3 Middle East Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.4 Middle East Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.5 Middle East Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.6 UAE

10.5.1.6.1 UAE Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.6.2 UAE Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.6.3 UAE Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.7.2 Egypt Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.7.3 Egypt Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.8.2 Saudi Arabia Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.8.3 Saudi Arabia Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.9.2 Qatar Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.9.3 Qatar Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.1.10.2 Rest of Middle East Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.10.3 Rest of Middle East Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.2.3 Africa Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.2.4 Africa Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.5 Africa Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.2.6.2 South Africa Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.6.3 South Africa Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.2.7.2 Nigeria Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.7.3 Nigeria Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.5.2.8.2 Rest of Africa Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.8.3 Rest of Africa Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Urometer Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.6.3 Latin America Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.6.4 Latin America Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.5 Latin America Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.6 Brazil

10.6.6.1 Brazil Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.6.6.2 Brazil Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.6.3 Brazil Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.7 Argentina

10.6.7.1 Argentina Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.6.7.2 Argentina Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.7.3 Argentina Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.8 Colombia

10.6.8.1 Colombia Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.6.8.2 Colombia Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.8.3 Colombia Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Urometer Market Estimates and Forecasts, by Product (2020-2032) (USD Million)

10.6.9.2 Rest of Latin America Urometer Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.9.3 Rest of Latin America Urometer Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11. Company Profiles

11.1 BD

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Medline Industries, Inc.

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Teleflex Incorporated

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 B. Braun Melsungen AG

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Cardinal Health, Inc.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Cook Medical

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Amsino International, Inc.

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Hollister Incorporated

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Coloplast

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Medtronic plc

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Urometer Market Key Segments:

By Product

100 ml

200 ml

400 ml

450 ml

500 ml

By Application

Operative Procedures

Emergency Trauma

Palliative Care

Others

By End-use

Hospitals

Home Healthcare

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

Synthetic Biology Market Size was valued at USD 12.5 billion in 2023 and is expected to reach USD 60.4 billion by 2032, growing at a CAGR of 19.1% over the forecast period 2024-2032.

Bladder Cancer Detection Kit Market was valued at USD 1.63 billion in 2023 and is expected to reach USD 2.99 billion by 2032, growing at a CAGR of 7.04%.

The Lancet Market size was estimated at USD 1.5 billion in 2023 and is expected to reach USD 3.72 billion by 2032 at a CAGR of 10.63% from 2024 to 2032.

Antinuclear Antibody Test Market was valued at USD 1.84 billion in 2023 and is expected to reach USD 5.38 billion by 2032, growing at a CAGR of 12.74% from 2024-2032.

The Physiotherapy Equipment Market Size was valued at USD 20.9 billion in 2023, is projected to grow at a CAGR of 6.9% to reach USD 38.2 billion by 2032.

Heating Pad Market size was valued at USD 51.78 billion in 2023 and is expected to grow to USD 81.52 billion by 2032 and grow at a CAGR of 5.19% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd