To get more information on Undersea Warfare Systems Market - Request Free Sample Report

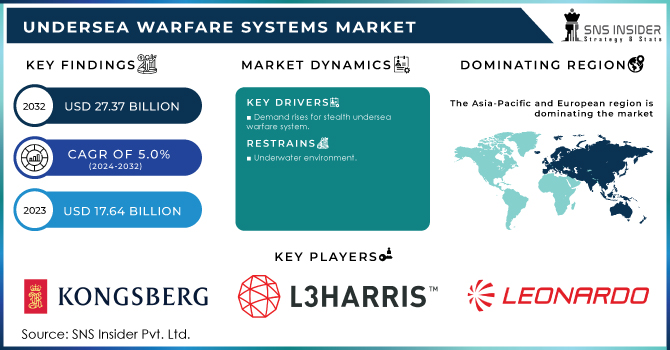

The Undersea Warfare Systems Market Size was valued at USD 17.64 billion in 2023 and is expected to reach USD 27.37 billion by 2032 with a growing CAGR of 5.0% over the forecast period 2024-2032.

Underwater tactics are means of attacking and defeating an enemy ship or fleet at sea during a conflict. The battlespace is the core idea of underwater warfare. It is a zone around a naval force in which a commander is sure of discovering, monitoring, engaging, and destroying enemies before they pose any harm to the relevant country. Surveillance (patrolling of littoral waters bounded by hostile coasts and harbors), reconnaissance which means gathering information from acoustic, electromagnetic, and optronic sensors without being detected, engagement means deploying missiles and torpedoes unanticipated by the enemy, and self-protection are all key functions of underwater warfare systems (utilizing forward-looking active sonar integrated torpedo counter systems). Underwater warfare systems must be adaptable enough to operate in complex naval battles.

Unmanned vehicles and maritime robots, stealth submarines, improved sonar detection ranges, undersea communications, and network-centric warfare, among other improvements in maritime technology, are expected to increase investment in R&D initiatives.

MARKET DYNAMICS

KEY DRIVERS

Demand rises for stealth undersea warfare system

RESTRAINTS

Underwater environment

Underwater threat protection

OPPORTUNITIES

Destroy enemy before it’s attacking

Enhance surveillance

Lightweight torpedoes

CHALLENGES

High operational cost

Endurance of submarine

IMPACT OF COVID-19

The COVID-19 crisis has created uncertainty in the submarine military industry, a sharp decline in supply chain, a decline in business confidence, and an increase in panic among customer segments. The governments of various regions have announced the complete closure and temporary closure of factories, thus having a negative impact on total production and sales. The impact of the COVID-19 epidemic has led to delays in the development of submarine warfare systems and declining tests and demonstrations and limitations on key player performance. Governments around the world have prioritized the healthcare industry to combat the COVID-19 virus, which has adversely affected the functioning of the defense industry. Epidemic closures were removed and re-introduced to curb the spread of COVID-19 infections as public services were gradually opened up in major countries such as the UK, India and Italy. Lack of components, sub-systems, and electronic systems, due to regulations related to the import and export of goods has caused production delays. The development of submarine military systems has also had an impact due to material shortages, due to production closures in China, South Korea and Taiwan. However, in the aftermath of the epidemic, improvements in the submarine systems have been observed. With the relaxation of door-closure measures, vaccination measures, and the opening of global markets, the demand for submarine military systems is expected to grow significantly in the near future.

It analyzed the submerged fighting business sector in light of frameworks, sensor frameworks, electronic help measures, and combat hardware. Sensor frameworks incorporate different sub-frameworks like sonar, radar, and optronics. Electronic help estimates comprise of three significant classes imaging frameworks, correspondence frameworks, and electronic fighting frameworks. Weapons incorporate torpedoes, land-assault voyage rockets, long range rockets, and mines. Alongside it, the report gives an in-nitty gritty market size examination of the submerged fighting business sector in light of stages like submarines, surface boats, helicopters, oceanic watch airplane, and automated frameworks. The report additionally gives an in-definite market size examination of the submerged fighting business sector in view of end-utilize, for example, maritime, airborne, and land-based. The ascent sought after for secrecy undersea fighting frameworks, the presentation of submerged drones for undersea fighting, and government backing for further developing undersea fighting abilities are the essential driving drivers in the overall undersea fighting frameworks market. Nonetheless, the functional intricacy of undersea automated frameworks, as well as the high forthright and functional costs of assault submarines, are obstructing market development. Running against the norm, the improvement of lightweight torpedoes and an expansion in the protection spending plan are probably going to produce beneficial market possibilities for overall market progression over the projection period. Different nations all over the planet are tracking down ways of acquiring conspicuousness in maritime tasks to further develop their protection abilities. As water covers more than 3/fourth of the outer layer of the earth, fortifying the naval force is fundamental to effectively safeguard land borders. U.S. authorities Maritime Undersea Fighting Place Division has granted agreements worth $ 49 million to 13 Sensors project organizations and the Sonar C15 Fast Prototyping Advancement. The 13 organizations will foster exploration techniques to apply to above warships, submarines, reconnaissance, confidential vehicles, submarines, appropriated networks, interesting fights, and airplane. Likewise, Australian Protection Priest Peter Dutton has reported a $ 1.44 billion interest in the improvement of automated submarine innovation to fortify Australia's tactical capacities in the midst of local struggles. Such advancements are supposed to animate the development of the submarine military market.

By Systems

Sensors

Electronic support measures

Armaments

By End-Use

Naval

Airborne

Land-based

By Application

Combat

C4ISR

Others

By Platforms

Submarines

Surface Ships

Maritime Patrol Aircrafts

Unmanned Systems

By Type

Weapon Systems

Communication and Surveillance Systems

Sensors and Computation Systems

Countermeasure Systems and Payload

Unmanned Underwater Vehicles

By Mode of Operation

Manned Operations

Autonomous Operations

Remotely Operations

REGIONAL ANALYSIS

The Asia-Pacific and European areas are likely to experience considerable growth during the forecast period, owing to the increasing acquisition of new submarines by naval forces as well as enhanced upgradation projects for existing submarines carried out in these regions. The increase can also be ascribed to a considerable increase in spending on improving maritime security.

Need any customization research on Undersea Warfare Systems Market - Enquiry Now

REGIONAL COVEREGE:

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

south Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

The Major Players are Kongsberg Gruppen, L3Harris Technologies Inc., General Dynamic Corporation, Leonardo S.p.A., Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation, SAAB AB, BAE Systems Plc., Thales Group and Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 17.64 Billion |

| Market Size by 2032 | US$ 27.37 Billion |

| CAGR | CAGR of 5.0% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Systems (Sensors, Electronic support measures, Armaments) • By End-Use (Naval, Airborne, Land-based) • By Application (Combat, C4ISR, Others) • By Platforms (Submarines, Surface Ships, Helicopters, Maritime Patrol Aircrafts and Unmanned Systems) • By Type (Weapon Systems, Communication and Surveillance Systems, Sensors and Computation Systems, Countermeasure Systems and Payload, Unmanned Underwater Vehicles) • By Mode of Operation (Manned Operations, Autonomous Operations, Remotely Operations) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kongsberg Gruppen, L3Harris Technologies Inc., General Dynamic Corporation, Leonardo S.p.A., Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation, SAAB AB, BAE Systems Plc., and Thales Group. |

| DRIVERS | • Demand rises for stealth undersea warfare system |

| RESTRAINTS | • Underwater environment • Underwater threat protection |

The expected CAGR of the Undersea Warfare Systems Market is 5% during the forecast period of 2023-2030.

The market size of the Undersea Warfare Systems Market is expected to reach USD 24.82 billion by 2030.

The leading Undersea Warfare Systems Market players include Kongsberg Gruppen, L3Harris Technologies Inc., General Dynamic Corporation, Leonardo S.p.A., Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation, SAAB AB, BAE Systems Plc., and Thales Group.

The Covid-19 pandemic affected the Undersea Warfare Systems Market negatively due to the supply chain disruption. The detailed analysis is included in the final report.

Asia-Pacific region is expected to show the highest growth in the Undersea Warfare Systems Market during the forecast period.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 COVID-19 Impact Analysis

4.2 Impact of Ukraine- Russia War

4.3 Impact of Ongoing Recession

4.3.1 Introduction

4.3.2 Impact on major economies

4.3.2.1 US

4.3.2.2 Canada

4.3.2.3 Germany

4.3.2.4 France

4.3.2.5 United Kingdom

4.3.2.6 China

4.3.2.7 Japan

4.3.2.8 South Korea

4.3.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Undersea Warfare Systems Market Segmentation, By Systems

8.1 Sensors

8.2 Electronic support measures

8.3 Armaments

9. Undersea Warfare Systems Market Segmentation, by End-Use

9.1 Naval

9.2 Airborne

9.3 Land-based

10. Undersea Warfare Systems Market Segmentation, by Application

10.1 Combat

10.2 C4ISR

10.3 Others

11. Undersea Warfare Systems Market Segmentation, by Platforms

11.1 Submarines

11.2 Surface Ships

11.3 Helicopters

11.4 Maritime Patrol Aircrafts

11.5 Unmanned Systems

12. Undersea Warfare Systems Market Segmentation, by Type

12.1 Weapon Systems

12.2 Communication and Surveillance Systems

12.3 Sensors and Computation Systems

12.4 Countermeasure Systems and Payload

12.5 Unmanned Underwater Vehicles

13. Undersea Warfare Systems Market Segmentation, by Mode of Operation

13.1 Manned Operations

13.2 Autonomous Operations

13.3 Remotely Operations

14. Regional Analysis

14.1 Introduction

14.2 North America

14.2.1 USA

14.2.2 Canada

14.2.3 Mexico

14.3 Europe

14.3.1 Germany

14.3.2 UK

14.3.3 France

14.3.4 Italy

14.3.5 Spain

14.3.6 The Netherlands

14.3.7 Rest of Europe

14.4 Asia-Pacific

14.4.1 Japan

14.4.2 South Korea

14.4.3 China

14.4.4 India

14.4.5 Australia

14.4.6 Rest of Asia-Pacific

14.5 The Middle East & Africa

14.5.1 Israel

14.5.2 UAE

14.5.3 South Africa

14.5.4 Rest

14.6 Latin America

14.6.1 Brazil

14.6.2 Argentina

14.6.3 Rest of Latin America

15. Company Profiles

15.1 Lockheed Martin Corporation

15.1.1 Financial

15.1.2 Products/ Services Offered

15.1.3 SWOT Analysis

15.1.4 The SNS view

15.2 Raytheon Technologies Corporation

15.3 Saab AB

15.4 Thales Group

15.5 L3Harris Technologies, Inc.

15.6 General Dynamics Corporation

15.7 Kongsberg Gruppen

15.8 Leonardo S.p.A.

15.9 Northrop Grumman Corporation

15.10 BAE Systems Plc

16. Competitive Landscape

16.1 Competitive Benchmarking

16.2 Market Share Analysis

16.3 Recent Developments

17. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Airborne Optronics Market Size was valued at USD 2.05 billion in 2023 and is expected to reach USD 5.96 billion by 2032 with a growing CAGR of 12.58% over the forecast period 2024-2032.

The Weapon Mounts Market Size was valued at USD 1.39 billion in 2023, expected to reach USD 2.75 billion by 2032 with a growing CAGR of 7.86% over the forecast period 2024-2032.

The Aircraft Computers Market Size was valued at USD 8.38 billion in 2023 and is expected to reach USD 14.10 Billion by 2032 with an emerging CAGR of 5.96% over the forecast period 2024-2032.

The Vehicle Intercom System Market Size was valued at USD 803.44 million in 2023 and is estimated to reach USD 1398.27 million by 2032 with an emerging CAGR of 6.35% over the forecast period 2024-2032.

The Unmanned Underwater Vehicles (UUV) Market Size was valued at USD 4.12 billion in 2023 and is expected to reach USD 13.29 billion by 2031 with an emerging CAGR of 15.8% over the forecast period 2024-2031.

The Drone Package Delivery System Market Size was valued at USD 441.6 million in 2023 and is projected to grow to USD 7536.2 million by 2032, with a compound annual growth rate (CAGR) of 37.08% over the forecast period from 2024 to 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd