To get more information on Ultra High Purity Metal Tubing for Semiconductor Market - Request Free Sample Report

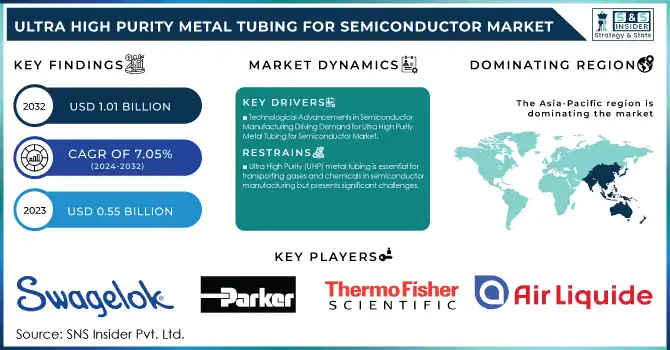

The Ultra High Purity Metal Tubing for Semiconductor Market was valued at USD 0.55 billion in 2023 and is expected to reach USD 1.01 billion by 2032 and grow at a CAGR of 7.05 % over the forecast period 2024-2032.

The Ultra High Purity Metal Tubing for Semiconductor Market is experiencing substantial growth, driven by the escalating demand for smaller, more powerful, and energy-efficient semiconductor devices. These devices are integral to sectors like consumer electronics, automotive, telecommunications, and industrial applications. UHP metal tubing plays a critical role in semiconductor fabrication by ensuring the safe transport of gases and chemicals, where even the slightest impurity can impact device performance and yield. As the global semiconductor market expands, particularly with the rise of AI, 5G, and IoT technologies, the demand for UHP materials, including UHP tubing, is surging. According to recent data from Uberant, this growth is directly correlated with the need for high-purity materials capable of withstanding extreme conditions such as ultra-high temperatures and pressures in semiconductor manufacturing. The Global Semiconductor Grade Fused Quartz Market mirrors this trend, emphasizing the increasing demand for contamination-free materials essential for advanced semiconductor production. Leading industry sources like Dockweiler and Thermo Fisher highlight UHP tubing’s significance in the development of next-generation semiconductor devices, particularly those supporting AI, 5G, and electric vehicles. Additionally, the expansion of semiconductor fabrication plants, such as the ongoing efforts by Taiwan Semiconductor Manufacturing Company, reinforces the rising demand for UHP materials. by 2032, the market is projected to continue expanding, spurred by advancements in semiconductor technologies like extreme ultraviolet (EUV) lithography and the global shift towards more energy-efficient, sustainable semiconductor production processes. In summary, the UHP metal tubing market for semiconductor manufacturing is poised for continued growth, driven by the increasing need for ultra-pure materials in the fabrication of high-performance devices. The rising emphasis on cleanroom environments and contamination control is expected to further fuel demand for UHP metal tubing, ensuring the success of next-generation semiconductor technologies.

Ultra High Purity Metal Tubing for Semiconductor Market Dynamics

Drivers

Technological advancements in semiconductor manufacturing, especially the shift towards extreme ultraviolet (EUV) lithography and the miniaturization of node sizes to 3nm and 2nm, are significantly increasing the demand for Ultra High Purity (UHP) metal tubing. As semiconductor devices become more sophisticated, particularly in emerging sectors like AI, 5G, and IoT, the need for highly precise manufacturing processes grows, requiring materials with extremely low impurity levels. UHP metal tubing plays a vital role in semiconductor production by ensuring the safe transportation of critical gases and chemicals, such as nitrogen, hydrogen, helium, and argon, which are essential for various processes in fabrication. Even trace contaminants in these gases can severely impact the manufacturing process, making contamination control a priority. For instance, nitrogen is widely used as an inerting and purging gas in semiconductor plants, protecting silicon wafers from moisture and reactive oxygen. A modern semiconductor fabrication facility can consume as much as 50,000 cubic meters of nitrogen per hour. Hydrogen is critical for annealing and deposition processes, while helium aids in heat conduction, and argon is employed in plasma etching and deposition reactions. Furthermore, the rise in semiconductor fabrication plant investments to support the increasing demand for advanced technologies is propelling the growth of UHP materials, including metal tubing. As production capabilities scale to meet the demands of next-generation devices, the need for ultra-pure materials intensifies. The importance of contamination control in cleanroom environments is crucial, as even slight improvements in yield can result in substantial profits. A one percent increase in yield can lead to an additional USD 150 million in annual profit for a semiconductor fab. As these trends continue, the UHP metal tubing market is expected to expand significantly.

Restraints

Contamination control is a key concern, as even trace impurities in gases like nitrogen, hydrogen, helium, and argon can disrupt the delicate fabrication processes, particularly at advanced nodes such as 5nm or 3nm. To avoid contamination, UHP metal tubing requires meticulous handling, cleaning, and maintenance throughout its lifecycle. Special procedures must be followed to remove particles, oils, moisture, and other contaminants that could jeopardize the quality of semiconductor devices. Maintaining contamination-free conditions involves adherence to strict cleanroom protocols, including the use of certified tools and equipment, which adds to operational complexity and costs. Additionally, regular inspections and investments in specialized equipment, such as particle counters and filtration systems, are necessary to ensure the tubing remains free of impurities. This complexity, alongside the need for well-trained operators, increases operational costs for semiconductor manufacturers. These challenges create significant hurdles for the widespread adoption and scaling of UHP metal tubing in the semiconductor.

by Type

Based on Type, The 316L segment dominated the Ultra High Purity (UHP) metal tubing for semiconductor market manufacturing , capturing around 74% of the revenue share in 2023. 316L stainless steel is highly favored due to its exceptional corrosion resistance, low carbon content, and ability to withstand high temperatures and pressures. These properties make it ideal for the rigorous demands of semiconductor fabrication, where cleanliness and purity are paramount. 316L's resistance to chloride-induced stress corrosion cracking and its ability to maintain structural integrity in harsh environments further contribute to its popularity. Additionally, the material’s ability to resist contamination, which could impact semiconductor yields, enhances its role in maintaining the precision required for advanced manufacturing processes.

by Application

The IDM (Integrated Device Manufacturer) segment dominates the Ultra High Purity (UHP) metal tubing market for semiconductor manufacturing, capturing around 59% of the revenue share in 2023. IDMs design, manufacture, and test their semiconductor products in-house, making them highly reliant on UHP metal tubing to transport essential gases and chemicals used in fabrication processes. The high purity requirements of semiconductor manufacturing, including precision in the transport of gases like nitrogen, hydrogen, and helium, are critical in IDM operations. UHP metal tubing ensures that contamination is minimized during these processes, which is vital for achieving the high performance and yield expected in advanced semiconductor devices. As the demand for smaller nodes and more complex chips grows, IDMs continue to drive market growth in UHP metal tubing.

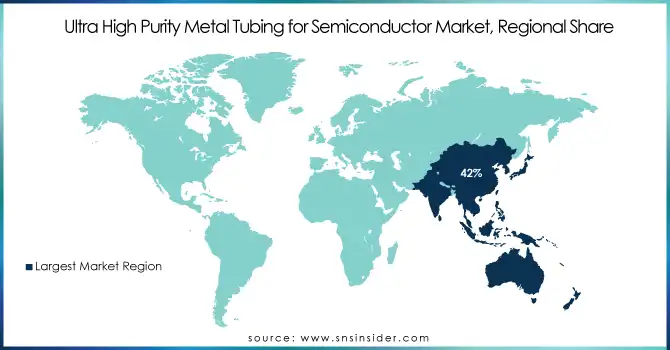

Asia-Pacific dominated the Ultra High Purity (UHP) Metal Tubing market for semiconductor market , capturing around 42% of the revenue share in 2023. This region is a key hub for semiconductor production, home to some of the world’s largest semiconductor manufacturers, including companies in South Korea, Taiwan, Japan, and China. These countries are heavily investing in cutting-edge semiconductor technologies, such as advanced nodes (3nm, 2nm), which require UHP materials for transporting gases and chemicals. The growing demand for electronics, including 5G devices, AI, and IoT applications, is further fueling the need for high-quality UHP metal tubing. Additionally, the expansion of semiconductor fabrication plants and the increasing adoption of automation and AI in production processes in Asia-Pacific are driving the market's growth. With continued technological advancements and significant investments in infrastructure, Asia-Pacific is expected to maintain its leadership in the UHP metal tubing market.

North America is poised to be the fastest-growing region in the Ultra High Purity Metal Tubing for Semiconductor Market from 2024 to 2032. This growth is driven by several key factors. First, the region is home to leading semiconductor manufacturers and fab facilities, particularly in the United States, which is heavily investing in advanced semiconductor technologies, including smaller process nodes like 3nm and 2nm. The U.S. government’s initiatives, such as the CHIPS Act, are further accelerating semiconductor production and innovation, driving demand for UHP materials. Additionally, the growing adoption of emerging technologies, including AI, 5G, and autonomous vehicles, is fueling semiconductor demand, requiring precision materials like UHP metal tubing. With increasing investments in state-of-the-art semiconductor fabs and advancements in manufacturing techniques, North America is expected to maintain rapid growth in the UHP metal tubing market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the Major Players in Ultra High Purity Metal Tubing for Semiconductor Market with their product:

List of potential Customers for Ultra High Purity (UHP) Metal Tubing for semiconductor market:

Recent Development

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 0.55 Billion |

| Market Size by 2032 | USD 1.01 Billion |

| CAGR | CAGR of 7.05% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (316L, 316L VIM/VAR) • By Application (IDM, Foundry) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Swagelok, Parker Hannifin, Thermo Fisher Scientific, Air Liquide, Fermilab, Concoa, Saint-Gobain, Gigasense, Vici Valco Instruments, Kurt J. Lesker Company, Nor-Cal Products, Mueller Industries, ULVAC, Kaysun Corporation, Manometer Technology, MATHESON, GCE Group, Aerospace & Defense, Parker Precision Fluidics, and SMC Corporation. |

| Key Drivers | • Technological Advancements in Semiconductor Manufacturing Driving Demand for Ultra High Purity Metal Tubing for Semiconductor Market. |

| Restraints | • Ultra High Purity (UHP) metal tubing is essential for transporting gases and chemicals in semiconductor manufacturing but presents significant challenges. |

Ans: The Ultra High Purity Metal Tubing for Semiconductor Market is to grow at a CAGR of 7.05% Over the Forecast Period 2024-2032.

Ans: The Ultra High Purity Metal Tubing for Semiconductor Market size was valued at USD 0.55 billion in 2023.

Ans: The growing demand for advanced semiconductor manufacturing processes and increasing adoption of UHP gas systems will drive the Ultra High Purity Metal Tubing for Semiconductor Market.

Ans: Asia-Pacific is dominating in of Ultra High Purity Metal Tubing for Semiconductor Market in 2023.

Ans: 316L is dominating in in Ultra High Purity Metal Tubing for Semiconductor Market in 2023.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Usage in Semiconductor Fabrication

5.2 Technological Advancements

5.3 Environmental Impact

5.4 Production Capacity

6. Competitive Landscape

6.1 List of Major Companies, by Region

6.2 Market Share Analysis, by Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Ultra High Purity Metal Tubing for Semiconductor Market Segmentation, by Type

7.1 Chapter Overview

7.2 316L

7.2.1 316L Market Trends Analysis (2020-2032)

7.2.2 316L Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 316L VIM/VAR

7.3.1 316L VIM/VAR Market Trends Analysis (2020-2032)

7.3.2 316L VIM/VAR Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Ultra High Purity Metal Tubing for Semiconductor Market Segmentation, by Application

8.1 Chapter Overview

8.2 IDM

8.2.1 IDM Market Trends Analysis (2020-2032)

8.2.2 IDM Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Foundry

8.3.1 Foundry Market Trends Analysis (2020-2032)

8.3.2 Foundry Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.2.4 North America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.2.5.2 USA Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.2.6.2 Canada Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.2.7.2 Mexico Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.5.2 Poland Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.6.2 Romania Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.4 Western Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.5.2 Germany Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.6.2 France Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.7.2 UK Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.8.2 Italy Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.9.2 Spain Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.12.2 Austria Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.4 Asia Pacific Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.5.2 China Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.5.2 India Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.5.2 Japan Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.6.2 South Korea Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.2.7.2 Vietnam Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.8.2 Singapore Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.9.2 Australia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.4 Middle East Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.5.2 UAE Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.2.4 Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.6.4 Latin America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.6.5.2 Brazil Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.6.6.2 Argentina Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.6.7.2 Colombia Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Ultra High Purity Metal Tubing for Semiconductor Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10. Company Profiles

10.1 Swagelok

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 SWOT Analysis

10.2 Parker Hannifin

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Thermo Fisher Scientific

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Air Liquide

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Fermilab

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Concoa

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 Saint-Gobain

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Gigasense

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Vici Valco Instruments

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Kurt J. Lesker Company

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

by Type

316L

316L VIM/VAR

by Application

IDM

Foundry

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The 5G Antennas Market Size was valued at USD 13.60 Billion in 2023 and is expected to grow at a CAGR of 12.3% to reach USD 38.41 Billion by 2032.

The Automated Test Equipment Market size was valued at $7.39 Billion in 2023 & estimated to reach $10.68 Billion by 2032 at a CAGR of 4.21% during 2024-2032

The Exoskeleton Market size was valued at USD 389.52 million in 2023 and is expected to grow to USD 1575.88 million by 2032 and grow at a CAGR of 16.8% over the forecast period of 2024-2032.

The Hearth Market was valued at USD 15.31 billion in 2023 and is expected to reach USD 22.73 billion by 2032, growing at a CAGR of 4.52% over the forecast period 2024-2032.

The Advanced Process Control Market was valued at USD 2.24 billion in 2023 and is expected to grow at a CAGR of 10.37% to reach USD 5.43 billion by 2032.

The Laser Cladding Market size is expected to be valued at USD 600 Mn in 2023 & will reach USD 1426.38 Mn by 2032 with a growing CAGR of 10.1% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd