Get More Information on Tight Gas Market - Request Sample Report

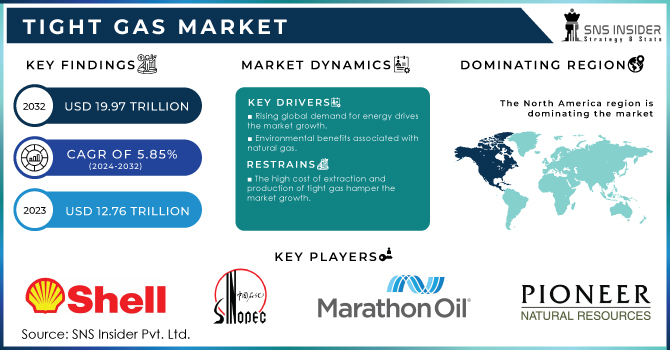

The Tight Gas Market Size was valued at USD 12.76 trillion cubic feet in 2023 and is expected to reach USD 19.97 trillion cubic feet by 2032 and grow at a CAGR of 5.85% over the forecast period 2024-2032.

The depletion of conventional gas reserves, coupled with the ever-increasing energy demand, has prompted a significant shift towards unconventional natural gas reserves, including tight gas, shale gas, and coal bed methane. Furthermore, the combustion of tight gas is considered cleaner compared to other fossil fuels like coal and petroleum products. This cleaner combustion is expected to have a positive impact in the years to come. Overall, the extraction and utilization of tight gas present a promising solution to meet the rising energy needs while minimizing environmental impact.

According to the Energy Information Administration reports that shale gas, a major component of tight gas, constituted about 75% of total U.S. natural gas production in recent years. This highlights the dominance of tight gas in the U.S. market.

The tight gas market is primarily driven by its lower extraction, processing, and commercialization costs, which are expected to significantly boost market growth. Furthermore, innovations in the extraction process, particularly hydraulic fracturing, are anticipated to further propel market expansion. Additionally, the increasing expenditure on the expansion of the oil and gas industry is poised to drive market growth. However, the presence of various harmful chemicals in the gas extraction process is expected to hinder market growth. Formaldehyde, asbestos, mercury, and hazardous/toxic air pollutants are among the harmful chemicals found in the extraction process. Moreover, the availability of alternative options like shale gas will also impact the market's growth trajectory.

EOG Resources launched a major expansion in the Barnett Shale, with a USD 1.6 billion investment to develop tight gas resources. The expansion includes the deployment of cutting-edge drilling technologies and the construction of new processing facilities.

Market Dynamics:

Drivers

Rising global demand for energy drives the market growth.

The increasing global demand for energy has led to a surge in the exploration and production of unconventional gas resources, including tight gas. This rising demand, coupled with advancements in drilling and extraction technologies, has created a favorable environment for the expansion of the tight gas market. As economies expand and urbanize, energy consumption increases, with natural gas being a preferred choice due to its relatively lower environmental impact compared to coal and oil.

The rising demand is also evident in the expansion of infrastructure to support natural gas distribution, such as new pipelines and LNG export terminals. For example, the expansion of the Sabine Pass LNG terminal in the U.S. has enabled increased exports to meet global demand. These trends underscore how the growing global appetite for energy, especially cleaner natural gas, propels the tight gas market forward.

Environmental benefits associated with natural gas.

The environmental benefits associated with natural gas, such as lower carbon emissions compared to other fossil fuels, have also contributed to the market's growth. As governments and organizations worldwide strive to reduce their carbon footprint, the demand for cleaner energy sources like natural gas continues to rise.

Restrain

The high cost of extraction and production of tight gas hamper the market growth.

One significant challenge is the high cost of extraction and production. Unlike conventional gas reserves, tight gas requires specialized drilling techniques, such as hydraulic fracturing, which can be expensive and complex. These costs can limit the profitability and viability of tight gas projects, especially in regions with limited infrastructure and access to markets.

By Type

In the tight gas market, the processed tight gas segment leads due to its higher quality and broader applicability. Processed tight gas, which has undergone treatment to remove impurities and contaminants, is preferred by industries and utilities for its reliability and efficiency. This processing ensures the gas meets stringent standards for use in power generation, chemical manufacturing, and other industrial applications. For instance, the processing of tight gas improves its energy content and reduces potential operational issues related to impurities. The higher value and versatility of processed tight gas make it more attractive to end-users compared to unprocessed tight gas, which may contain higher levels of contaminants and require additional treatment before use. As a result, processed tight gas commands a larger share of the market due to its enhanced performance and compliance with regulatory requirements.

By Application

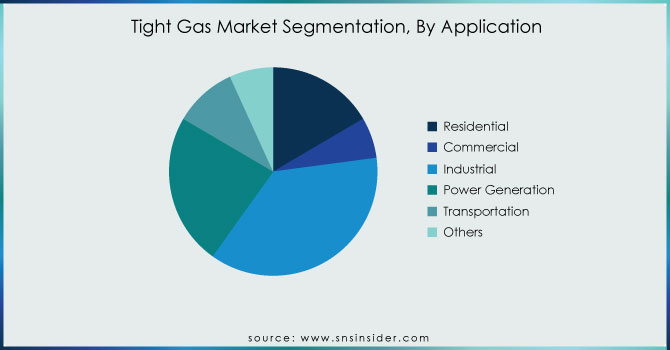

The industrial segment held the largest market share around 37% of the total volume in 2023. This growth is attributed to the increasing utilization of tight gas for various value-added outputs required in the industrial sector. For example, it is used as a feedstock for the manufacturing of fertilizers, chemicals, and other commodities. This trend has created numerous opportunities for countries rich in tight gas resources to enhance their industrial output in the coming years. Furthermore, the power generation segment is projected to experience the fastest growth in terms of volume over the forecast period. This is attributed to the global trend of transitioning from coal to gas in power plants. Tight gas combustion produces lower carbon emissions compared to other fossil fuels, making it an attractive option for several nations looking to reduce their environmental impact. As a result, the share of tight gas in the energy mix of these countries is expected to increase significantly.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Regional Analysis:

North America dominated the Tight Gas Market with the highest revenue share of about 62% in 2023. The region boasts vast reserves of tight gas, particularly in the United States and Canada. These abundant resources provide a solid foundation for North America's market dominance. Furthermore, the implementation of innovative drilling techniques, including horizontal drilling and multi-stage fracking, has significantly enhanced the efficiency and productivity of tight gas extraction. These technological advancements have allowed North American companies to tap into previously inaccessible reserves, thereby bolstering their revenue share. Another crucial factor contributing to North America's tight gas market dominance is its robust demand. The region's growing population, coupled with its heavy reliance on natural gas for power generation, industrial processes, and residential consumption, has created a consistent and substantial market for tight gas. The United States plays a significant role in driving revenue growth in this region, due to the deployment of advanced drilling technologies and the presence of abundant tight gas reserves in areas like the Permian Basin, Anadarko, Niobrara, and Bakken fields.

Asia Pacific is anticipated to grow with the highest CAGR in the tight gas market during the forecast period. Asia Pacific region boasts abundant reserves of tight gas, which has become an increasingly attractive energy source due to the depletion of conventional gas reserves. These vast reserves provide a solid foundation for the region's growth in the tight gas market. Moreover, the Asia Pacific region has witnessed a surge in energy demand, driven by rapid industrialization, urbanization, and population growth. As a result, there is a pressing need for alternative energy sources to meet this escalating demand. Tight gas, with its vast reserves and potential for extraction, has emerged as a viable solution to bridge the energy gap in the region. Additionally, advancements in drilling and extraction technologies have significantly improved the feasibility and cost-effectiveness of extracting tight gas. This has further incentivized companies to invest in the Asia Pacific region, driving market growth. China is the leading country in the Asia Pacific region. The country is focused on increasing domestic natural gas production and improving energy security in the region.

Royal Dutch Shell, Sinopec, Marathon Oil, Pioneer Natural Resources, EOG Resources, British petroleum, Exxon Mobil and Chesapeake Energy Total SA, PetroChina, Anadarko Petroleum Co., Devon Energy, and other players.

In 2024, ExxonMobil announced a USD 4 billion investment to expand its tight gas operations in the Permian Basin. This expansion includes the development of new drilling sites and the construction of additional infrastructure to increase production capacity and efficiency.

In Aug 2023, Sinopec Corp obtained certification for an additional 30.55 billion cubic meters of proven geological reserves in a deep natural gas reservoir located in the Bazhong gasfield of the Sichuan basin.

In November 2022, Marathon Oil Corporation announced its definitive purchase agreement to acquire the Eagle Ford assets of Ensign Natural Resources for a total cash consideration of $3.0 billion. The transaction is subject to customary terms and conditions, including closing adjustments, and is anticipated to be finalized by the end of 2022.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 12.76 Tillion |

| Market Size by 2032 | US$ 19.97 Tillion |

| CAGR | CAGR of 5.85% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Processed Tight Gas, Unprocessed Tight Gas) • By Application (Residential, Commercial, Industrial, Power Generation, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Royal Dutch Shell, Sinopec, Marathon Oil, Pioneer Natural Resources, EOG Resources, British petroleum, Exxon Mobil and Chesapeake Energy Total SA, PetroChina and Anadarko Petroleum Co., Devon Energy, and other players. |

| DRIVERS | • Rising global demand for energy. • Environmental benefits associated with natural gas |

| Restraints | • High cost of extraction and production of tight gas hamper the market growth. |

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Ans: The North American area had the biggest market share of 62 percent, and this is expected to continue in the future years.

Ans: Following the emergence of COVID-19, the tight gas demand has dramatically decreased. Due to the lockdown, there has been a shortage in the number of labourers, significantly hampering gas output. Furthermore, imposing lockdown has a direct impact on transportation services all over the world. Due to the scarcity of tight gas, power generation has become a big challenge. This has resulted in an upsurge in power outages in rural areas. Furthermore, the tight gas industry is experiencing daily losses as output declines. Furthermore, the implementation of lockdown has had an impact on the global import and export of tight gas.

Ans: Strict policies to protect the environment, Prolonged stages of government evaluation and Licence issuance are the restraints for Tight Gas Market.

Ans: The Tight Gas Market Size was valued at USD 12.76 trillion cubic feet in 2023 and is expected to reach USD 19.97 trillion cubic feet by 2032 and grow at a CAGR of 5.85% over the forecast period 2024-2032.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Tight Gas Market Segmentation, By Type

7.1 Introduction

7.2 Processed Tight Gas

7.3 Unprocessed Tight Gas

8. Tight Gas Market Segmentation, By Application

8.1 Introduction

8.2 Residential

8.3 Commercial

8.4 Industrial

8.5 Power Generation

8.6 Transportation

8.7 Others

9. Regional Analysis

9.1 Introduction

9.2 North America

9.2.1 Trend Analysis

9.2.2 North America Tight Gas Market by Country

9.2.3 North America Tight Gas Market By Type

9.2.4 North America Tight Gas Market By Application

9.2.5 USA

9.2.5.1 USA Tight Gas Market By Type

9.2.5.2 USA Tight Gas Market By Application

9.2.6 Canada

9.2.6.1 Canada Tight Gas Market By Type

9.2.6.2 Canada Tight Gas Market By Application

9.2.7 Mexico

9.2.7.1 Mexico Tight Gas Market By Type

9.2.7.2 Mexico Tight Gas Market By Application

9.3 Europe

9.3.1 Trend Analysis

9.3.2 Eastern Europe

9.3.2.1 Eastern Europe Tight Gas Market by Country

9.3.2.2 Eastern Europe Tight Gas Market By Type

9.3.2.3 Eastern Europe Tight Gas Market By Application

9.3.2.4 Poland

9.3.2.4.1 Poland Tight Gas Market By Type

9.3.2.4.2 Poland Tight Gas Market By Application

9.3.2.5 Romania

9.3.2.5.1 Romania Tight Gas Market By Type

9.3.2.5.2 Romania Tight Gas Market By Application

9.3.2.6 Hungary

9.3.2.6.1 Hungary Tight Gas Market By Type

9.3.2.6.2 Hungary Tight Gas Market By Application

9.3.2.7 Turkey

9.3.2.7.1 Turkey Tight Gas Market By Type

9.3.2.7.2 Turkey Tight Gas Market By Application

9.3.2.8 Rest of Eastern Europe

9.3.2.8.1 Rest of Eastern Europe Tight Gas Market By Type

9.3.2.8.2 Rest of Eastern Europe Tight Gas Market By Application

9.3.3 Western Europe

9.3.3.1 Western Europe Tight Gas Market by Country

9.3.3.2 Western Europe Tight Gas Market By Type

9.3.3.3 Western Europe Tight Gas Market By Application

9.3.3.4 Germany

9.3.3.4.1 Germany Tight Gas Market By Type

9.3.3.4.2 Germany Tight Gas Market By Application

9.3.3.5 France

9.3.3.5.1 France Tight Gas Market By Type

9.3.3.5.2 France Tight Gas Market By Application

9.3.3.6 UK

9.3.3.6.1 UK Tight Gas Market By Type

9.3.3.6.2 UK Tight Gas Market By Application

9.3.3.7 Italy

9.3.3.7.1 Italy Tight Gas Market By Type

9.3.3.7.2 Italy Tight Gas Market By Application

9.3.3.8 Spain

9.3.3.8.1 Spain Tight Gas Market By Type

9.3.3.8.2 Spain Tight Gas Market By Application

9.3.3.9 Netherlands

9.3.3.9.1 Netherlands Tight Gas Market By Type

9.3.3.9.2 Netherlands Tight Gas Market By Application

9.3.3.10 Switzerland

9.3.3.10.1 Switzerland Tight Gas Market By Type

9.3.3.10.2 Switzerland Tight Gas Market By Application

9.3.3.11 Austria

9.3.3.11.1 Austria Tight Gas Market By Type

9.3.3.11.2 Austria Tight Gas Market By Application

9.3.3.12 Rest of Western Europe

9.3.3.12.1 Rest of Western Europe Tight Gas Market By Type

9.3.2.12.2 Rest of Western Europe Tight Gas Market By Application

9.4 Asia-Pacific

9.4.1 Trend Analysis

9.4.2 Asia Pacific Tight Gas Market by Country

9.4.3 Asia Pacific Tight Gas Market By Type

9.4.4 Asia Pacific Tight Gas Market By Application

9.4.5 China

9.4.5.1 China Tight Gas Market By Type

9.4.5.2 China Tight Gas Market By Application

9.4.6 India

9.4.6.1 India Tight Gas Market By Type

9.4.6.2 India Tight Gas Market By Application

9.4.7 Japan

9.4.7.1 Japan Tight Gas Market By Type

9.4.7.2 Japan Tight Gas Market By Application

9.4.8 South Korea

9.4.8.1 South Korea Tight Gas Market By Type

9.4.8.2 South Korea Tight Gas Market By Application

9.4.9 Vietnam

9.4.9.1 Vietnam Tight Gas Market By Type

9.4.9.2 Vietnam Tight Gas Market By Application

9.4.10 Singapore

9.4.10.1 Singapore Tight Gas Market By Type

9.4.10.2 Singapore Tight Gas Market By Application

9.4.11 Australia

9.4.11.1 Australia Tight Gas Market By Type

9.4.11.2 Australia Tight Gas Market By Application

9.4.12 Rest of Asia-Pacific

9.4.12.1 Rest of Asia-Pacific Tight Gas Market By Type

9.4.12.2 Rest of Asia-Pacific Tight Gas Market By Application

9.5 Middle East & Africa

9.5.1 Trend Analysis

9.5.2 Middle East

9.5.2.1 Middle East Tight Gas Market by Country

9.5.2.2 Middle East Tight Gas Market By Type

9.5.2.3 Middle East Tight Gas Market By Application

9.5.2.4 UAE

9.5.2.4.1 UAE Tight Gas Market By Type

9.5.2.4.2 UAE Tight Gas Market By Application

9.5.2.5 Egypt

9.5.2.5.1 Egypt Tight Gas Market By Type

9.5.2.5.2 Egypt Tight Gas Market By Application

9.5.2.6 Saudi Arabia

9.5.2.6.1 Saudi Arabia Tight Gas Market By Type

9.5.2.6.2 Saudi Arabia Tight Gas Market By Application

9.5.2.7 Qatar

9.5.2.7.1 Qatar Tight Gas Market By Type

9.5.2.7.2 Qatar Tight Gas Market By Application

9.5.2.8 Rest of Middle East

9.5.2.8.1 Rest of Middle East Tight Gas Market By Type

9.5.2.8.2 Rest of Middle East Tight Gas Market By Application

9.5.3 Africa

9.5.3.1 Africa Tight Gas Market by Country

9.5.3.2 Africa Tight Gas Market By Type

9.5.3.3 Africa Tight Gas Market By Application

9.5.2.4 Nigeria

9.5.2.4.1 Nigeria Tight Gas Market By Type

9.5.2.4.2 Nigeria Tight Gas Market By Application

9.5.2.5 South Africa

9.5.2.5.1 South Africa Tight Gas Market By Type

9.5.2.5.2 South Africa Tight Gas Market By Application

9.5.2.6 Rest of Africa

9.5.2.6.1 Rest of Africa Tight Gas Market By Type

9.5.2.6.2 Rest of Africa Tight Gas Market By Application

9.6 Latin America

9.6.1 Trend Analysis

9.6.2 Latin America Tight Gas Market by Country

9.6.3 Latin America Tight Gas Market By Type

9.6.4 Latin America Tight Gas Market By Application

9.6.5 Brazil

9.6.5.1 Brazil Tight Gas Market By Type

9.6.5.2 Brazil Tight Gas Market By Application

9.6.6 Argentina

9.6.6.1 Argentina Tight Gas Market By Type

9.6.6.2 Argentina Tight Gas Market By Application

9.6.7 Colombia

9.6.7.1 Colombia Tight Gas Market By Type

9.6.7.2 Colombia Tight Gas Market By Application

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Tight Gas Market By Type

9.6.8.2 Rest of Latin America Tight Gas Market By Application

10. Company Profiles

10.1 Royal Dutch Shell

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 The SNS View

10.2 Sinopec

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 The SNS View

10.3 Marathon Oil

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 The SNS View

10.4 Pioneer Natural Resources

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 The SNS View

10.5 British Petroleum

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 The SNS View

10.6 Exxon Mobil

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 The SNS View

10.7. Chesapeake Energy Total SA

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 The SNS View

10.8 PetroChina

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 The SNS View

10.9 Anadarko Petroleum Co.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 The SNS View

10.10 Devon Energy

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 The SNS View

11. Competitive Landscape

11.1 Competitive Benchmarking

11.2 Market Share Analysis

11.3 Recent Developments

11.3.1 Industry News

11.3.2 Company News

11.3.3 Mergers & Acquisitions

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Type

Processed Tight Gas

Unprocessed Tight Gas

By Application

Residential

Commercial

Industrial

Power Generation

Transportation

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Biorationals Market size was USD 1.24 Billion in 2023 and is expected to reach USD 2.67 Billion by 2032, growing at a CAGR of 8.90 % from 2024 to 2032.

The Resin Market size was valued at USD 560 Billion in 2023. It is expected to grow to USD 861.3 Billion by 2032 and grow at a CAGR of 4.9% over the forecast period of 2024-2032.

Fire-resistant Coatings Market was valued at USD 1079.4 million in 2023 and is expected to reach USD 1478.8 million by 2032, at a CAGR of 3.6% from 2024-2032.

The Wire & Cable Compounds Market Size was USD 14.84 billion in 2023 and will reach USD 32.50 billion by 2032 and grow at a CAGR of 9.32% by 2024-2032.

The Extruders Market Size was valued at USD 10.0 billion in 2023 and is expected to reach USD 14.9 billion by 2032 and grow at a CAGR of 4.5% 2024-2032.

The Jojoba Oil Market Size was USD 140.87 million in 2023. It is estimated to hit USD 270.08 million by 2032 and grow at a CAGR of 7.50% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd