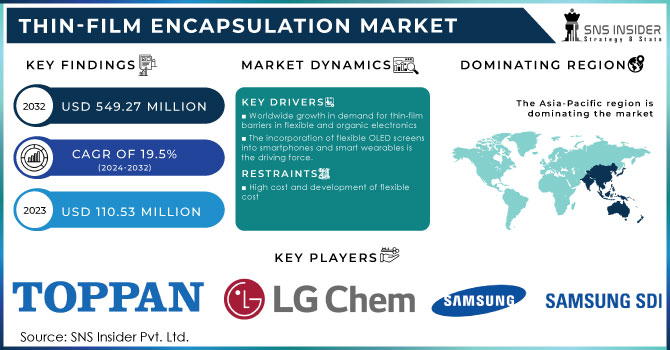

The Thin-Film Encapsulation Market size was valued at USD 110.53 million in 2023 and is expected to grow to USD 549.27 million by 2032 and grow at a CAGR Of 19.5% over the forecast period of 2024-2032. Increasing use of thin-film barriers in flexible and organic electronic devices is the major driver for the growth of the market. Another important factor driving market growth is the combination of flexible OLED displays into smartphones and also smart wearables. Strides in automation, manufacturing efficiencies, and supply chain management have also been important enablers of growth across regions.

Get More Information on Thin-Film Encapsulation Market- Request Sample Report

Drivers:

Growth of Thin-Film Encapsulation in Flexible Electronics and OLED Technologies

Demand for flexible electronics, powered by flourishing of flexible oled displays in smartphones, wearables and consumer electronics, is driving the thin-film encapsulation (tfe) market because of this property, tfe is critical for preventing environmental damage to oleds and organic electronics, such as moisture and oxygen. Organics are also being used in solar cells to improve efficiency and more recently device protection, with organic-inorganic hybrid thin-film encapsulation being used to boost stability. Technological advancements, including atomic layer deposition (ALD) and inkjet printing, are expected to fuel market growth. The rise of wearable devices and flexible OLEDs further strengthens TFE's market position, while automotive applications, like OLED lighting, expand its reach. However, flexible glass technology poses a challenge as it may replace TFE, but the technology remains vital for flexible OLEDs' future.

Restraints:

Material shortages of key compounds can break supply chains, raise costs, and slow the growing thin-film encapsulation technology.

Material shortages pose a significant challenge for the Thin-Film Encapsulation (TFE) market as TFE involves the use of specialized materials, including metal oxides and other high-performance compounds. A disruption to the supply chains of these materials would cause higher production costs and delays. For instance, the use of metal oxides, key to forming moisture barriers in TFE layers, could be impacted, leading to constraints on supply of one of the essential features as well. the Thin-film Encapsulation s has potential to delay mass manufacturing and reduce the scalability of TFE applications in key areas such as flexible electronics, OLED displays and bioelectronics.

Opportunities:

Bioelectronics integration in thin-film encapsulation offers a key opportunity as wearable devices and biosensors create new markets for TFE technologies.

The growing field of bioelectronics, including wearable health devices, biosensors, and implantable electronics, is increasingly dependent on thin-film encapsulation (TFE) technologies for protecting delicate components from environmental damage such as moisture and oxygen. TFE provides an ideal solution for bioelectronics due to its flexibility, durability, and lightweight nature, ensuring the longevity of sensitive devices. With advancements in TFE technologies, such as atomic layer deposition (ALD) and inkjet printing, manufacturers are enhancing performance while reducing costs. These innovations are expanding the application of TFE in bioelectronics, offering significant growth potential in the sector.

Challenges:

Material durability challenges for Thin-Film Encapsulation involve ensuring long-term reliability, resistance to environmental factors, and flexibility.

One of the significant challenges for the Thin-Film Encapsulation market is ensuring the long-term durability of materials used in encapsulation. The TFE technology must offer reliable protection against environmental factors such as moisture and oxygen while maintaining the necessary flexibility for flexible electronic devices like OLED displays and wearable technologies. Materials like metal oxides used in TFE structures are susceptible to degradation over time due to exposure to these elements, which can affect their protective properties. The above elements and thus the performance in terms of protection deteriorates. The researchers are exploring new materials and advanced deposition methods, such as atomic layer deposition, to overcome this problem, but these have yet to be incorporated into large-scale production. For the growth of the market, a trade-off needs to be maintained between durability vs flexibility at a lower cost.

By Technology

Plasma-enhanced chemical vapor deposition (PECVD) dominates the Thin Film Encapsulation (TFE) market, holding a significant share of around 36% in 2023. This technique is preferred because it allows for the deposition of thin films with high-quality attributes, such as improved moisture resistance, greater flexibility, and greater durability; features, which are important for OLEDs and other sensitive electronics. PECVD growth is propelled by versatility, where it is applied in diverse industries, such as electronics, automotive and bioelectronics. Its cost-effective and scalable process also contributes to its widespread adoption, making it a key technology in advancing TFE applications and ensuring the longevity of electronic devices exposed to environmental factors.

Atomic Layer Deposition (ALD) is the fastest-growing segment in the Thin Film Encapsulation (TFE) market over the forecast period from 2024 to 2032. ALD offers precise control over film thickness, uniformity, and composition, making it ideal for advanced encapsulation applications in OLED displays, bioelectronics, and flexible electronics. Its being fueled by its capability to provide conformal coatings with outstanding oxygen and moisture barrier performance, even on complex topographies. ALD is easily scalable and further developments of precursor and deposition methods will contribute to the increasing penetration of this technology into the market, making it one of the dominant technologies used in TFE applications.

By Application

The flexible OLED display segment dominated the Thin Film Encapsulation market, accounting for around 49% in 2023. This segment's growth is driven by the increasing back of rising demand for lighter, thinner and flexible display from smartphones, wearables and consumer electronics. Flexible OLED displays provide enhanced image quality, high-energy efficiency, and the possibility of curved or foldable designs, which are very appealing to consumers. TFE technology is critical in protecting OLED materials from environmental damage like moisture and oxygen, ensuring long-term durability.

The Thin-Film Photovoltaics (TFPV) segment is the fastest-growing segment in the Thin Film Encapsulation market over the forecast period 2024-2032. Driven by the increasing adoption of renewable energy sources and advancements in solar technology, thin-film photovoltaics offer advantages such as flexibility, lightweight, and cost-efficiency compared to traditional solar panels. TFE technology plays a crucial role in protecting thin-film solar cells from environmental factors like moisture and oxygen, enhancing their durability and efficiency.

Need any customization research on Thin-Film Encapsulation Market - Enquiry Now

The Asia-Pacific region dominates the Thin-Film Encapsulation market with around 50% market share in 2023, driven by rapid advancements in electronics, renewable energy, and OLED technology. Countries like China, Japan, South Korea, and India are key contributors to this growth China is beating the world in organic light-emitting diode (OLED) production and solar cell technologies, while Japan and South Korea are dominant in flexible electronics and display technologies. Its dominance in the TFE market is further strengthened by the region's established manufacturing infrastructure, ability to manufacture products in large quantities, and increasing investments in the renewable energy technology sector. Additionally, the rising demand for wearable devices and flexible displays in Asia-Pacific supports TFE's widespread adoption.

North America is the fastest-growing region in the Thin-Film Encapsulation (TFE) market over the forecast period 2024-2032. The United States, in particular, leads in the adoption of advanced display technologies, bioelectronics, and flexible OLEDs, driving demand for TFE solutions. The region's robust research and development sector, coupled with significant investments in renewable energy and flexible electronics, is accelerating market growth. Additionally, North America has a strong base of technological innovation in atomic layer deposition (ALD) and other advanced deposition techniques. Key market players and the region's emphasis on sustainability and green technologies also make it ideally suited for significant growth in the TFE market.

Some of the major key players in Thin Film Encapsulation Market along with their product:

Samsung SDI Co., Ltd. (South Korea) – (Lithium-ion batteries, OLED materials)

LG Chem (South Korea) – (Lithium-ion batteries, OLED materials)

Universal Display Corporation (USA) – (OLED technologies, phosphorescent materials)

3M (USA) – (Optical films, adhesive materials)

Applied Materials, Inc. (USA) – (Semiconductor processing equipment, display technologies)

Meyer Burger Technology AG (Switzerland) – (Solar cell production equipment)

Toray Industries, Inc. (Japan) – (Advanced materials, OLED displays)

Toppan Inc. (Japan) – (Display films, packaging materials)

Ergis Group (Poland) – (Flexible packaging films)

Veeco Instruments Inc. (USA) – (Deposition equipment, LED materials)

Kateeva (USA) – (Inkjet printing for OLED displays)

tesa (Germany) – (Adhesive tapes, display bonding solutions)

Ajinomoto Fine-Techno Co., Inc. (Japan) – (Photomasks, OLED materials)

Coat-X (Germany) – (Thin film deposition equipment)

Borealis AG (Austria) – (Polyolefins, specialty plastics)

OLED – (Organic light-emitting diode technology, display and lighting panels)

List of suppliers for the thin-film market who provide raw material and Component:

Mitsui Chemicals, Inc.

Dow Inc.

BASF

DuPont

Toray Industries, Inc.

Samsung SDI Co., Ltd.

LG Chem

28 August 2024, LG Display is exploring new ways to thin down foldable panels, trying to use black pixel define layer (PDL) samples that it purchased from Mitsubishi and other suppliers. This ingredient is important for enabling the application of CoE format technology, replacing the polarizing layer in the OLED panels, with a black PDL instead of the orange PDL normally used, will increase the efficiency of foldable OLED displays and thinness.

24 November 2024, OLED technology has focused on improving the longevity and efficiency of OLED panels, with significant advancements in Thin Film Encapsulation (TFE) technology to protect against moisture and oxygen damage. And companies such as Kateeva have led the way with inkjet printing of organic TFE (thin film encapsulation) layers, while advanced inorganic, i.e., glassy, layers are coming in to increase effectiveness and prolong the life of the OLED, particularly valuable in flexible screens and wearables.

10 January 2025, Samsung to introduce Color-filter-on-thin-film-encapsulation (CoE) to next Galaxy S26 Ultra, planned for 2026 Already utilized in Samsung foldables including the Galaxy Z Fold 3 and Z Fold 6, this tech features a revamped layout that places color filters directly above the new thin encapsulation layer, which improves screen efficiency, brightness, and other aspects of screen quality. With this, the S26 Ultra

| Report Attributes | Details |

| Market Size in 2023 | USD 110.53 Million |

| Market Size by 2032 | USD 549.27 Million |

| CAGR | CAGR of 19.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Plasma-enhanced chemical vapor deposition (PECVD), Atomic layer deposition (ALD), Inkjet Printing, Vacuum Thermal Evaporation (VTE), Other Technologies) • By Application (Flexible OLED Display, Thin-Film Photovoltaics, Flexible OLED Lighting, Other Applications) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Samsung SDI Co., Ltd. (South Korea), LG Chem (South Korea), Universal Display Corporation (USA), 3M (USA), Applied Materials, Inc. (USA), Meyer Burger Technology AG (Switzerland), Toray Industries, Inc. (Japan), Toppan Inc. (Japan), Ergis Group (Poland), Veeco Instruments Inc. (USA), Kateeva (USA), tesa (Germany), Ajinomoto Fine-Techno Co., Inc. (Japan), Coat-X (Germany), Borealis AG (Austria).,OLed. |

Ans: Thin-film Encapsulation Market is anticipated to expand by 19.5% from 2024 to 2032.

Ans: The key driver for the Thin-Film Encapsulation market is the growing demand for flexible electronics, particularly in OLED displays and renewable energy applications.

Ans: The Thin-film Encapsulation Market is estimated to reach USD 549.27 million by 2032.

Ans: Thin-film Encapsulation Market size was valued at USD 110.53 million in 2023.

Ans: The Asia-Pacific is dominating in Thin-film Encapsulation market.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Technological Adoption Rate, by Region

5.2 Manufacturing Efficiency Improvements, by Region

5.3 Supply Chain Efficiency, by Region

5.4 Material Cost Trends, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Thin-film Encapsulation Market Segmentation, by Type

7.1 Chapter Overview

7.2 Plasma-enhanced chemical vapor deposition (PECVD)

7.2.1 Plasma-enhanced chemical vapor deposition (PECVD) Market Trends Analysis (2020-2032)

7.2.2 Plasma-enhanced chemical vapor deposition (PECVD) Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 Atomic layer deposition (ALD)

7.3.1 Atomic layer deposition (ALD) Market Trends Analysis (2020-2032)

7.3.2 Atomic layer deposition (ALD) Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 Inkjet Printing

7.4.1 Inkjet Printing Market Trends Analysis (2020-2032)

7.4.2 Inkjet Printing Market Size Estimates and Forecasts to 2032 (USD Million)

7.5 Vacuum Thermal Evaporation (VTE)

7.5.1 Vacuum Thermal Evaporation (VTE) Market Trends Analysis (2020-2032)

7.5.2 Vacuum Thermal Evaporation (VTE) Market Size Estimates and Forecasts to 2032 (USD Million)

7.6 Other Technologies

7.6.1 Other Technologies Market Trends Analysis (2020-2032)

7.6.2 Other Technologies Market Size Estimates and Forecasts to 2032 (USD Million)

8. Thin-film Encapsulation Market Segmentation, by Application

8.1 Chapter Overview

8.2 Flexible OLED Display

8.2.1 Flexible OLED Display Market Trends Analysis (2020-2032)

8.2.2 Flexible OLED Display Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Thin-Film Photovoltaics

8.3.1 Thin-Film Photovoltaics Market Trends Analysis (2020-2032)

8.3.2 Thin-Film Photovoltaics Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Flexible OLED Lighting

8.4.1 Flexible OLED Lighting Market Trends Analysis (2020-2032)

8.4.2 Flexible OLED Lighting Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 Other Applications

8.5.1 Other Applications Market Trends Analysis (2020-2032)

8.5.2 Other Applications Market Size Estimates and Forecasts to 2032 (USD Million)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.2.3 North America Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.2.4 North America Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.5 USA

9.2.5.1 USA Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.2.5.2 USA Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.6 Canada

9.2.6.1 Canada Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.2.6.2 Canada Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.7 Mexico

9.2.7.1 Mexico Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.2.7.2 Mexico Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.3.1.3 Eastern Europe Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.4 Eastern Europe Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.5 Poland

9.3.1.5.1 Poland Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.5.2 Poland Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.6 Romania

9.3.1.6.1 Romania Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.6.2 Romania Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.7.2 Hungary Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.8.2 Turkey Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.1.9.2 Rest of Eastern Europe Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.3.2.3 Western Europe Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.4 Western Europe Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.5 Germany

9.3.2.5.1 Germany Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.5.2 Germany Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.6 France

9.3.2.6.1 France Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.6.2 France Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.7 UK

9.3.2.7.1 UK Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.7.2 UK Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.8 Italy

9.3.2.8.1 Italy Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.8.2 Italy Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.9 Spain

9.3.2.9.1 Spain Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.9.2 Spain Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.10.2 Netherlands Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.11.2 Switzerland Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.12 Austria

9.3.2.12.1 Austria Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.12.2 Austria Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.3.2.13.2 Rest of Western Europe Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4 Asia-Pacific

9.4.1 Trends Analysis

9.4.2 Asia-Pacific Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.4.3 Asia-Pacific Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.4 Asia-Pacific Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.5 China

9.4.5.1 China Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.5.2 China Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.6 India

9.4.5.1 India Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.5.2 India Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.5 Japan

9.4.5.1 Japan Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.5.2 Japan Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.6 South Korea

9.4.6.1 South Korea Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.6.2 South Korea Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.7 Vietnam

9.4.7.1 Vietnam Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.2.7.2 Vietnam Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.8 Singapore

9.4.8.1 Singapore Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.8.2 Singapore Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.9 Australia

9.4.9.1 Australia Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.9.2 Australia Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.10 Rest of Asia-Pacific

9.4.10.1 Rest of Asia-Pacific Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.4.10.2 Rest of Asia-Pacific Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.1.3 Middle East Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.4 Middle East Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.5 UAE

9.5.1.5.1 UAE Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.5.2 UAE Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.6.2 Egypt Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.7.2 Saudi Arabia Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.8.2 Qatar Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.1.9.2 Rest of Middle East Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.2.3 Africa Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.2.4 Africa Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.2.5.2 South Africa Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.2.6.2 Nigeria Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.5.2.7.2 Rest of Africa Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Thin-film Encapsulation Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.6.3 Latin America Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.6.4 Latin America Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.5 Brazil

9.6.5.1 Brazil Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.6.5.2 Brazil Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.6 Argentina

9.6.6.1 Argentina Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.6.6.2 Argentina Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.7 Colombia

9.6.7.1 Colombia Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.6.7.2 Colombia Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Thin-film Encapsulation Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

9.6.8.2 Rest of Latin America Thin-film Encapsulation Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10. Company Profiles

10.1 Samsung SDI Co., Ltd.

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 SWOT Analysis

10.2 LG Chem

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Universal Display Corporation

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 3M

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Applied Materials, Inc.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Meyer Burger Technology AG

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 Toray Industries, Inc.

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Toppan Inc.

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Ergis Group

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Veeco Instruments Inc.

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Technology

Plasma-enhanced chemical vapour deposition (PECVD)

Atomic layer deposition (ALD)

Inkjet Printing

Vacuum Thermal Evaporation (VTE)

Other Technologies

By Application

Flexible OLED Display

Thin-Film Photovoltaics

Flexible OLED Lighting

Other Applications

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Behavioral Biometrics Market Size was valued at USD 1.66 Billion in 2023 and is expected to grow at 26.77% CAGR to reach USD 14.00 Billion by 2032.

The Inductor Market was valued at USD 4.95 Billion in 2023 and is projected to reach USD 8.10 Billion by 2032, growing at a CAGR of 5.63% from 2024 to 2032.

The Nuclear Robots Market was valued at USD 1.82 billion in 2023 and is expected to reach USD 5.23 billion by 2032, growing at a CAGR of 12.48% over the forecast period 2024-2032.

The Semiconductor Foundry Market size is expected to be valued at USD 118.60 Billion in 2023. It is estimated to reach USD 211.34 Billion by 2032 with a CAGR of 6.63% over the forecast period 2024-2032.

The Machine-to-Machine (M2M) Market Size was valued at USD 23.62 billion in 2023 and is expected to grow at a CAGR of 4.60% to reach USD 35.40 billion by 2032.

The Smart Set-Top Box Market Size was valued at USD 32.69 billion in 2023 and is expected to grow at a CAGR of 9.2% to reach USD 66.30 billion by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd