Testing As A Service Market Report Scope & Overview:

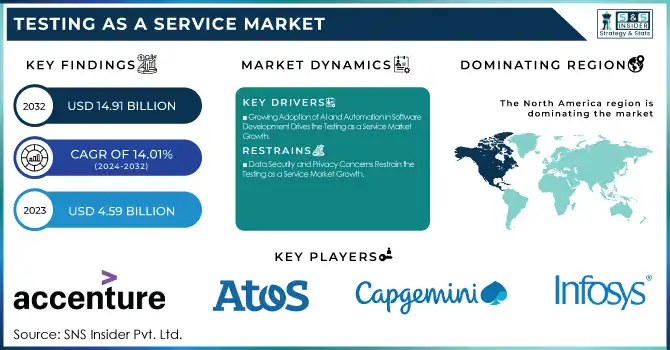

The Testing As A Service Market Size was valued at USD 4.59 Billion in 2023 and is expected to reach USD 14.91 Billion by 2032 and grow at a CAGR of 14.01% over the forecast period 2024-2032.

To get more information on Testing As A Service Market - Request Free Sample Report

The Market is expanding rapidly as businesses embrace cloud-based and AI-driven testing solutions for improved software quality and efficiency. TaaS enables companies to outsource testing, reducing costs and enhancing scalability. The adoption of automation, DevOps, and AI-powered analytics has improved testing accuracy and speed. Industries like BFSI, healthcare, and IT & telecom are leveraging TaaS for security and performance optimization. Leading providers such as IBM, Accenture, and TCS are investing in AI-driven testing platforms, making TaaS a vital component of modern software development lifecycles.

Testing As A Service Market Dynamics

Key Drivers:

-

Growing Adoption of AI and Automation in Software Development Drives the Testing as a Service Market Growth

The increasing integration of AI, machine learning, and automation in software development is a significant driver of the Testing as a Service (TaaS) Market. Companies are shifting towards cloud-based and AI-powered testing solutions to enhance software quality, accelerate time-to-market, and reduce costs. Automated testing enables continuous testing and deployment in DevOps and Agile environments, ensuring faster software releases without compromising performance. Leading providers like IBM, Accenture, and Capgemini are investing in AI-driven testing platforms to improve efficiency.

Additionally, IoT, mobile applications, and cloud-based solutions require scalable and on-demand testing services, further fueling TaaS adoption. The ability to perform real-time defect detection, predictive analytics, and self-healing automation enhances the accuracy of testing processes, making AI and automation key growth drivers. As businesses prioritize digital transformation, the demand for cost-effective, flexible, and AI-powered testing services continues to surge, driving innovation in the TaaS market.

Restrain:

-

Data Security and Privacy Concerns Restrain the Testing as a Service Market Growth

The growing concern over data security and privacy. Many businesses, particularly in industries like BFSI, healthcare, and government, handle sensitive data that requires strict compliance with regulatory frameworks such as GDPR, HIPAA, and PCI DSS. Outsourcing software testing to third-party providers increases the risk of data breaches, unauthorized access, and compliance violations.

Additionally, cloud-based testing environments can be vulnerable to cyber threats if not secured properly. Enterprises often hesitate to fully adopt TaaS solutions due to concerns about data protection, confidentiality, and legal liabilities. To address these issues, TaaS providers must implement robust encryption, multi-layer authentication, and stringent security protocols. Despite these challenges, ongoing advancements in cybersecurity and compliance-driven solutions can help mitigate risks, enabling wider adoption of TaaS in security-sensitive industries.

Opportunities

-

Expansion of Cloud-Based Testing Solutions Creates Growth Opportunities in the Testing as a Service Market

The increasing adoption of cloud-based testing solutions presents a significant opportunity in the Testing as a Service (TaaS) Market. Businesses are rapidly shifting towards SaaS-based testing platforms, enabling on-demand, scalable, and cost-efficient testing environments. Cloud-based TaaS solutions eliminate the need for expensive on-premise infrastructure, reducing operational costs while ensuring real-time collaboration among development teams worldwide. Companies like Microsoft, AWS, and Google Cloud have enhanced their cloud testing capabilities, offering integrated tools for functional, performance, and security testing.

Additionally, AI-driven analytics, containerized testing, and serverless computing are revolutionizing how software testing is conducted in cloud environments. As businesses continue migrating to hybrid and multi-cloud architectures, cloud-based testing services will drive market growth by enhancing efficiency, accessibility, and scalability.

Challenges

-

Lack of Skilled Professionals and Expertise Challenges the Testing as a Service Market Growth

The shortage of skilled professionals and expertise remains a critical challenge for the Testing as a Service (TaaS) Market. As automation, AI, and DevOps-driven testing become more complex, there is a growing demand for highly skilled testers with expertise in AI-based testing frameworks, security protocols, and cloud environments. However, the lack of proper training and upskilling programs has resulted in a talent gap, making it difficult for organizations to implement advanced testing methodologies effectively. Many enterprises face challenges in hiring and retaining professionals proficient in automated test scripting, AI-driven analytics, and cybersecurity testing.

Moreover, with the increasing adoption of IoT and mobile applications, the need for multi-platform testing experts has surged. To overcome this challenge, companies must invest in workforce training, partnerships with academic institutions, and AI-assisted testing tools. Bridging the skills gap is crucial for sustaining TaaS market growth and innovation in the evolving software testing landscape.

Testing As A Service Market Segments Analysis

By Test Type

The Functionality Testing segment accounted for the largest revenue share of 28% in 2023, driven by the increasing demand for seamless user experiences, software reliability, and compliance adherence. Functionality testing ensures that applications meet specified requirements and perform as expected across different environments. With the rapid development of mobile applications, cloud-based solutions, and AI-driven platforms, businesses are prioritizing rigorous functional testing to minimize defects before deployment.

In 2023, Microsoft introduced AI-enhanced functional testing features within Azure DevOps, streamlining software validation. Additionally, Tricentis expanded its AI-driven test automation platform, enabling end-to-end functional testing for enterprise applications.

The Security Testing segment is projected to grow at the highest CAGR of 16.17% during the forecasted period, driven by increasing concerns over cyber threats, data breaches, and regulatory compliance. As businesses shift towards cloud-based applications, IoT ecosystems, and AI-powered platforms, the need for robust security testing has surged. Enterprises are adopting penetration testing, vulnerability assessments, and compliance testing to safeguard sensitive data and mitigate cyber risks.

In 2023, IBM launched an advanced AI-powered security testing suite within its Cloud Pak for Security, enhancing real-time threat detection. Similarly, Synopsys introduced an AI-driven automated security testing platform, helping organizations identify and fix vulnerabilities in DevSecOps pipelines.

By End-use

The IT & Telecommunication segment accounted for the largest revenue share of 32% in 2023, driven by the rapid expansion of 5G networks, cloud computing, and AI-driven digital services. As telecom providers roll out next-generation connectivity solutions, the need for rigorous software testing to ensure network reliability, application performance, and cybersecurity has intensified.

Additionally, Nokia expanded its automated software testing suite for telecom infrastructure, enhancing network resilience. With the rise of IoT, edge computing, and software-defined networking (SDN), telecom companies are increasingly adopting Testing as a Service (TaaS) solutions to streamline operations, reduce downtime, and enhance customer experiences, ensuring seamless global connectivity.

The Healthcare segment is witnessing the fastest CAGR of 16.25%, driven by the growing adoption of digital health solutions, telemedicine, and AI-powered diagnostics. With stringent regulatory requirements such as HIPAA, FDA, and GDPR compliance, the demand for software testing services in the healthcare sector has surged. Healthcare providers and medical technology companies rely on TaaS solutions to ensure secure, reliable, and error-free applications for patient data management, remote monitoring, and AI-assisted diagnosis.

Additionally, Oracle launched an advanced healthcare application testing suite to improve electronic health record (EHR) system performance. As digital transformation accelerates in healthcare, security, performance, and functionality testing will remain critical, positioning TaaS as a key enabler for innovation, compliance, and patient safety in the industry.

By Deployment

The Public Cloud segment held the largest revenue share in 2023, driven by the increasing adoption of cloud-based testing solutions across enterprises, startups, and SMEs. Public cloud environments offer scalability, cost-efficiency, and seamless integration with DevOps and Agile methodologies, making them the preferred choice for Testing as a Service (TaaS) solution. Major cloud service providers such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud have significantly expanded their cloud-based testing frameworks.

The Private Cloud segment is witnessing the fastest CAGR in the forecasted period, fueled by data security concerns, regulatory compliance requirements, and the need for customized testing environments. Enterprises in industries such as BFSI, healthcare, and government prefer private cloud deployments due to their enhanced security, dedicated infrastructure, and compliance with industry-specific regulations like HIPAA, GDPR, and PCI DSS. Companies like IBM, VMware, and Oracle have strengthened their private cloud TaaS offerings to meet the growing demand.

Regional Analysis

North America held the largest market share in the Testing as a Service (TaaS) market in 2023, driven by the rapid adoption of cloud-based testing solutions, AI-driven automation, and strong IT infrastructure. The region’s dominance is attributed to the presence of major TaaS providers such as IBM, Microsoft, Accenture, and Capgemini, which continue to invest in advanced testing frameworks. The growing demand for DevOps, Agile testing, and cybersecurity compliance solutions among enterprises in sectors like BFSI, healthcare, and IT & telecom has further fueled market growth.

In 2023, Microsoft launched new AI-powered testing tools for Azure, enhancing cloud-based application testing. Similarly, Google Cloud introduced an advanced performance testing suite to improve software efficiency.

Asia Pacific is projected to witness the highest CAGR in the Testing as a Service (TaaS) market in 2023, driven by the rapid digital transformation, expansion of cloud services, and increasing adoption of AI-driven testing. Countries like China, India, Japan, and South Korea are leading the growth due to the booming IT sector, rising investments in software development, and growing reliance on mobile and web applications. Leading technology firms such as TCS, Infosys, and Wipro have significantly expanded their cloud-based and AI-powered testing solutions to cater to increasing regional demand. With government initiatives supporting digitalization, increased cloud adoption by enterprises, and a thriving startup ecosystem, Asia Pacific remains the fastest-growing region in the TaaS market, shaping the future of software testing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

Some of the major players in the Testing As A Service Market are:

-

Accenture (Accenture Test Automation Suite, Accenture Cloud Testing Services)

-

Atos SE (Atos Managed Testing Services, Atos Cloud & Security Testing)

-

Capgemini (Capgemini SmartQA, Capgemini Performance Testing Services)

-

DeviQA Solutions (DeviQA Automated Testing, DeviQA Performance & Security Testing)

-

Deloitte Touche Tohmatsu Limited (Deloitte Testing Services, Deloitte Cloud Assurance & Testing)

-

DXC Technology Company (DXC Application Testing Services, DXC Performance Engineering)

-

IBM Corporation (IBM Rational Test Workbench, IBM Cloud Testing Services)

-

Infosys Limited (Infosys Testing as a Service (TaaS), Infosys AI-Led Testing Services)

-

TATA Consultancy Services Limited (TCS Quality Engineering & Testing, TCS Assurance Services)

-

Qualitest Group (Qualitest AI-Powered Testing, Qualitest Cybersecurity Testing)

Recent Trends

-

In August 2024, Accenture expanded its collaboration with Amazon Web Services (AWS) to introduce the Accenture Responsible Artificial Intelligence (AI) Platform powered by AWS. This platform was designed to assist organizations in rapidly adopting and scaling AI responsibly, providing comprehensive services such as AI governance setup, risk assessment, generative AI testing, and compliance support.

-

In November 2024, Atos was selected to provide IT services for the Invictus Games scheduled in Canada. Atos planned to deploy 50 staff members from Europe to Canada to deliver an "adaptive and intimate" IT service for the event. This engagement underscored Atos's commitment to supporting large-scale international events with tailored IT solutions, ensuring seamless operations and enhanced experiences for participants and audiences alike.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 4.59 Billion |

| Market Size by 2032 | US$ 14.91 Billion |

| CAGR | CAGR of 14.01 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Test Type (Functionality, Performance, Compatibility, Security, Compliance, Others) • By End-Use (IT & Telecommunication, Healthcare, BFSI, Automotive, Manufacturing, Retail & Consumer Goods, Energy & Utilities, Others) • By Deployment (Public, Private, Hybrid) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Accenture, Atos SE, Capgemini, DeviQA Solutions, Deloitte Touche Tohmatsu Limited, DXC Technology Company, IBM Corporation, Infosys Limited, TATA Consultancy Services Limited, Qualitest Group. |