Get E-PDF Sample Report on Sulfur Bentonite Market - Request Sample Report

The Sulfur Bentonite Market size was valued at USD 144.8 million in 2023. It is anticipated to reach USD 224.4 million by the year 2032 with a projected CAGR of 5.0% during the forecast period of 2024-2032.

The Sulfur bentonite market is growing in response to the increasing demand for sulfur-enriched fertilizers in agriculture. Sulfur Bentonite is a highly critical element that has formed an inseparable part of enhanced crop yield and more fertile soils in the agricultural sector of plant growth. Another key trend causing the development of the Sulfur bentonite market is the growing awareness of the deficiencies of sulfur in the soils, which is now gaining ground, as continually depleted levels of these important nutrients are due to modern farming practices. This has made farmers increasingly interested in Sulfur Bentonite, understanding its benefits in improving crop quality and productivity. Additionally, the increasing global population is demanding more from agricultural yields to uphold food security.

Sulfur bentonite fulfills this demand by enhancing plant growth and health, leading to increased food production. For instance, in a country like India and China, where Sulfur deficiency in the soil is a common feature, Sulfur bentonite has been hugely useful in increasing the yield and quality of crops, hence a visible benefit to the farmer and a booster for the regional food supply chains. Another major driver in the Sulfur Bentonite market could be trending toward sustainable agricultural practices. Slow release is an attribute of Sulfur Bentonite that becomes innately in line with these objectives—environmentally benign processes and soil health improvement. It gradually releases sulfur into the soil, reducing the probability of nutrient loss and ensuring its efficient utilization by plants for better crop performance. It also reduces the frequency of fertilizer applications thereby mitigating costs and environmental footprints.

Government policies and initiatives also support the Sulfur Bentonite market. Most countries subsidize and incentivize sulfur-based fertilizers to improve the agricultural yield. For instance, in the United States and most European countries, government initiatives on micronutrient fertilizers, such as Sulfur Bentonite, which improves crop health and enhances yield, have been forwarded. Similarly, in February 2024, the government-initiated actions to limit urea use, including the PM-PRANAM scheme to reduce chemical fertilizers. It promoted Sulfur-coated urea (SCU) to improve nitrogen uptake and provide Sulfur, increasing efficiency by 10-15%. Sulfur was crucial for oil seeds and pulses, covering 30.92 and 26.34 million hectares in 2020-21, with fertilizers like single super phosphate and Bentonite Sulfur meeting India's needs. Coupled with this supportive regulatory backdrop and advances in technologies related to production, such as improved granulation methods for better nutrient availability and application efficiency, the circumstances remain quite supportive of the Sulfur Bentonite market outlook.

Growing population and increasing need for higher agricultural productivity

Increasing adoption of sulfur-based fertilizers in the agriculture industry

A major driver of the Sulfur bentonite market is the ever-increasing adoption of fertilizer products containing sulfur in the agriculture industry. Increasingly, farmers try to use Sulfur Bentonite due to its potential for correcting the deficiency of sulfur content in the soil, adjudged to be a prime requisite for optimum crop growth. Sulfur helps in synthesizing amino acids and proteins in plants and hence improves overall yield and quality of crops. This has fostered increased awareness by farmers about value created by sulfur-based fertilizers in improving nutrient uptake efficiency and driving sustainable farming practices. In response, that improves demand for Sulfur Bentonite, entailing sustained agriculture performance across several regions of the world.

RESTRAIN:

Limited availability of raw materials

Strict regulations by various governments on the use of sulfur-based fertilizers

OPPORTUNITY:

Fast Growing agricultural sector

Positive Attributes of Sulfur Bentonite to Fuel Demand

CHALLENGES:

Threats to Environmental and Human Health associated with the use of Sulfur Bentonite.

By Type

Sulfur-85%

Sulfur-90%

Others

The Sulfur-90% segment contributed to the largest share of around 60% in the Sulfur Bentonite market in 2023. This range of Sulfur Bentonite has higher contents of Sulfur, particularly 90% Sulfur content preferred by Agricultural industries since it is an effective way to rectify Sulfur deficiencies in the soils, which are very essential for crop growth and yield. The Bentonite Sulfur-90% formulations have been specifically proven for their effectiveness in improving the plants' nutrient uptake and hence enhancing agricultural productivity. This is because WDG Sulfur, with the formulation, enjoys high acceptance in most parts of the globe due to proof of its efficiency in enhancing the yield and quality of crops.

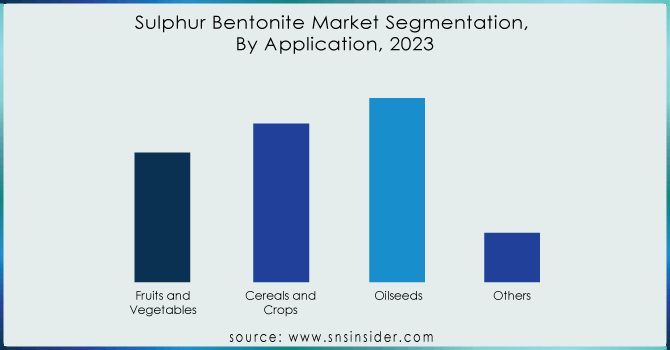

By Application

Fruits and Vegetables

Cereals and Crops

Oilseeds

Others

The Sulfur bentonite market was dominated by the oilseeds segment, which contributed a revenue share of about 38% in 2023. Sunflower, groundnut, sesame, safflower, mustard, and rapeseed, among others, are the major oilseed crops worldwide, and Sulfur bentonite provides them with additional oil content. The quality and yield of pulses is also enhanced by this product; hence, it is abetted by its important advantages accruing to the oilseeds sector. The segment of cereals and crops is likely to grow at a decent CAGR of approximately 5% during this period, which goes without saying as maize, wheat, and grains see their output increasing for global food and feed needs.

Get Customised Report as per Your Business Requirement - Enquiry Now

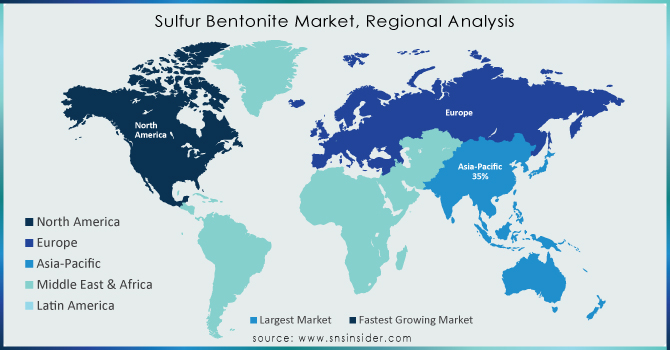

Asia Pacific dominated the Sulfur bentonite market with the largest share in 2023 with a revenue share of about 35%. Countries like China, India, and other Southeast Asian countries have vast cultivation areas for growing a range of crops. The agricultural environment in countries in Asia Pacific ranges from staples like rice and wheat to high-value fruits and vegetables. Sulfur Bentonite finds great acceptance in these agricultural practices to make the land more fertile and raise the yield of crops by compensating for the lack of sulfur. Further to this, government initiatives that emphasize sustainable farming extend the market where the use of sulfur fertilizers enhances the agriculture productivity of the country. A rapidly growing population that has an increasing demand for food means that, in turn, Asia Pacific remains central in fostering the demand for Sulfur Bentonite both to serve the country's food production and to contribute to the global food supply.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are Tiger Sul, Deepak Fertilizers, H Sulphur Corp, Devco Australia, Coogee Chemicals, National Fertilizer Limited, NTCS Group, Galaxy Sulfur, Chung Kwang, Coromandel International, and other key players mentioned in the final report.

May 2023: The Jordan Phosphate Mines Company signed an MoU with Safe Sulfur, a Canadian company specializing in the Sulfur industry, for establishing a plant in Aqaba that will produce 100,000 tons per year of SulfuR Bentonite fertilizers.

March 2023: Tiger Sul has partnered with HGS BioScience. The first product after their collaboration is Tiger Humi[K] 4%, which features a physically combined carbon and sulfur bentonite in one convenient granule.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 144.8 Million |

| Market Size by 2032 | US$ 224.4 Million |

| CAGR | CAGR of 5.0 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Sulfur-85%, Sulfur-90%, Others) •By Application (Fruits and Vegetables, Cereals and Crops, Oilseeds, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Tiger Sul, Deepak Fertilizers, H Sulphur Corp, Devco Australia, Coogee Chemicals, National Fertilizer Limited, NTCS Group, Galaxy Sulfur, Chung Kwang, Coromandel International |

| Key Drivers | Growing population and increasing need for higher agricultural productivity Increasing adoption of sulfur-based fertilizers in the agriculture industry |

| Restraints | Limited availability of raw materials Strict regulations by various governments on the use of sulfur-based fertilizers |

Ans. Asia Pacific region holds the largest market share in the Sulfur Bentonite Market during the forecast period.

Ans. Limited availability of raw materials and Strict regulations by various governments on the use of Sulfur-based fertilizers

Ans: Bentonite, the key element in the production of sulfur bentonite, is not easily available in bulk at the global level. This limited availability may cause disruptions in the supply chain, hike the cost, and dampen growth to a great extent.

Ans: Sulfur Bentonite Market size was USD 6.8 billion in 2023 and is expected to reach USD 10.55 billion by 2032.

Ans: The Sulfur Bentonite Market is expected to grow at a CAGR of 5.0%.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Sulphur Bentonite Market Segmentation, By Type

7.1 Introduction

7.2 Sulphur-85%

7.3 Sulphur-90%

7.4 Others

8. Sulphur Bentonite Market Segmentation, By Application

8.1 Introduction

8.2 Fruits and Vegetables

8.3 Cereals and Crops

8.4 Oilseeds

8.5 Others

9. Regional Analysis

9.1 Introduction

9.2 North America

9.2.1 Trend Analysis

9.2.2 North America Sulphur Bentonite Market by Country

9.2.3 North America Sulphur Bentonite Market By Type

9.2.4 North America Sulphur Bentonite Market By Application

9.2.5 USA

9.2.5.1 USA Sulphur Bentonite Market By Type

9.2.5.2 USA Sulphur Bentonite Market By Application

9.2.6 Canada

9.2.6.1 Canada Sulphur Bentonite Market By Type

9.2.6.2 Canada Sulphur Bentonite Market By Application

9.2.7 Mexico

9.2.7.1 Mexico Sulphur Bentonite Market By Type

9.2.7.2 Mexico Sulphur Bentonite Market By Application

9.3 Europe

9.3.1 Trend Analysis

9.3.2 Eastern Europe

9.3.2.1 Eastern Europe Sulphur Bentonite Market by Country

9.3.2.2 Eastern Europe Sulphur Bentonite Market By Type

9.3.2.3 Eastern Europe Sulphur Bentonite Market By Application

9.3.2.4 Poland

9.3.2.4.1 Poland Sulphur Bentonite Market By Type

9.3.2.4.2 Poland Sulphur Bentonite Market By Application

9.3.2.5 Romania

9.3.2.5.1 Romania Sulphur Bentonite Market By Type

9.3.2.5.2 Romania Sulphur Bentonite Market By Application

9.3.2.6 Hungary

9.3.2.6.1 Hungary Sulphur Bentonite Market By Type

9.3.2.6.2 Hungary Sulphur Bentonite Market By Application

9.3.2.7 Turkey

9.3.2.7.1 Turkey Sulphur Bentonite Market By Type

9.3.2.7.2 Turkey Sulphur Bentonite Market By Application

9.3.2.8 Rest of Eastern Europe

9.3.2.8.1 Rest of Eastern Europe Sulphur Bentonite Market By Type

9.3.2.8.2 Rest of Eastern Europe Sulphur Bentonite Market By Application

9.3.3 Western Europe

9.3.3.1 Western Europe Sulphur Bentonite Market by Country

9.3.3.2 Western Europe Sulphur Bentonite Market By Type

9.3.3.3 Western Europe Sulphur Bentonite Market By Application

9.3.3.4 Germany

9.3.3.4.1 Germany Sulphur Bentonite Market By Type

9.3.3.4.2 Germany Sulphur Bentonite Market By Application

9.3.3.5 France

9.3.3.5.1 France Sulphur Bentonite Market By Type

9.3.3.5.2 France Sulphur Bentonite Market By Application

9.3.3.6 UK

9.3.3.6.1 UK Sulphur Bentonite Market By Type

9.3.3.6.2 UK Sulphur Bentonite Market By Application

9.3.3.7 Italy

9.3.3.7.1 Italy Sulphur Bentonite Market By Type

9.3.3.7.2 Italy Sulphur Bentonite Market By Application

9.3.3.8 Spain

9.3.3.8.1 Spain Sulphur Bentonite Market By Type

9.3.3.8.2 Spain Sulphur Bentonite Market By Application

9.3.3.9 Netherlands

9.3.3.9.1 Netherlands Sulphur Bentonite Market By Type

9.3.3.9.2 Netherlands Sulphur Bentonite Market By Application

9.3.3.10 Switzerland

9.3.3.10.1 Switzerland Sulphur Bentonite Market By Type

9.3.3.10.2 Switzerland Sulphur Bentonite Market By Application

9.3.3.11 Austria

9.3.3.11.1 Austria Sulphur Bentonite Market By Type

9.3.3.11.2 Austria Sulphur Bentonite Market By Application

9.3.3.12 Rest of Western Europe

9.3.3.12.1 Rest of Western Europe Sulphur Bentonite Market By Type

9.3.2.12.2 Rest of Western Europe Sulphur Bentonite Market By Application

9.4 Asia-Pacific

9.4.1 Trend Analysis

9.4.2 Asia Pacific Sulphur Bentonite Market by Country

9.4.3 Asia Pacific Sulphur Bentonite Market By Type

9.4.4 Asia Pacific Sulphur Bentonite Market By Application

9.4.5 China

9.4.5.1 China Sulphur Bentonite Market By Type

9.4.5.2 China Sulphur Bentonite Market By Application

9.4.6 India

9.4.6.1 India Sulphur Bentonite Market By Type

9.4.6.2 India Sulphur Bentonite Market By Application

9.4.7 Japan

9.4.7.1 Japan Sulphur Bentonite Market By Type

9.4.7.2 Japan Sulphur Bentonite Market By Application

9.4.8 South Korea

9.4.8.1 South Korea Sulphur Bentonite Market By Type

9.4.8.2 South Korea Sulphur Bentonite Market By Application

9.4.9 Vietnam

9.4.9.1 Vietnam Sulphur Bentonite Market By Type

9.4.9.2 Vietnam Sulphur Bentonite Market By Application

9.4.10 Singapore

9.4.10.1 Singapore Sulphur Bentonite Market By Type

9.4.10.2 Singapore Sulphur Bentonite Market By Application

9.4.11 Australia

9.4.11.1 Australia Sulphur Bentonite Market By Type

9.4.11.2 Australia Sulphur Bentonite Market By Application

9.4.12 Rest of Asia-Pacific

9.4.12.1 Rest of Asia-Pacific Sulphur Bentonite Market By Type

9.4.12.2 Rest of Asia-Pacific Sulphur Bentonite Market By Application

9.5 Middle East & Africa

9.5.1 Trend Analysis

9.5.2 Middle East

9.5.2.1 Middle East Sulphur Bentonite Market by Country

9.5.2.2 Middle East Sulphur Bentonite Market By Type

9.5.2.3 Middle East Sulphur Bentonite Market By Application

9.5.2.4 UAE

9.5.2.4.1 UAE Sulphur Bentonite Market By Type

9.5.2.4.2 UAE Sulphur Bentonite Market By Application

9.5.2.5 Egypt

9.5.2.5.1 Egypt Sulphur Bentonite Market By Type

9.5.2.5.2 Egypt Sulphur Bentonite Market By Application

9.5.2.6 Saudi Arabia

9.5.2.6.1 Saudi Arabia Sulphur Bentonite Market By Type

9.5.2.6.2 Saudi Arabia Sulphur Bentonite Market By Application

9.5.2.7 Qatar

9.5.2.7.1 Qatar Sulphur Bentonite Market By Type

9.5.2.7.2 Qatar Sulphur Bentonite Market By Application

9.5.2.8 Rest of Middle East

9.5.2.8.1 Rest of Middle East Sulphur Bentonite Market By Type

9.5.2.8.2 Rest of Middle East Sulphur Bentonite Market By Application

9.5.3 Africa

9.5.3.1 Africa Sulphur Bentonite Market by Country

9.5.3.2 Africa Sulphur Bentonite Market By Type

9.5.3.3 Africa Sulphur Bentonite Market By Application

9.5.2.4 Nigeria

9.5.2.4.1 Nigeria Sulphur Bentonite Market By Type

9.5.2.4.2 Nigeria Sulphur Bentonite Market By Application

9.5.2.5 South Africa

9.5.2.5.1 South Africa Sulphur Bentonite Market By Type

9.5.2.5.2 South Africa Sulphur Bentonite Market By Application

9.5.2.6 Rest of Africa

9.5.2.6.1 Rest of Africa Sulphur Bentonite Market By Type

9.5.2.6.2 Rest of Africa Sulphur Bentonite Market By Application

9.6 Latin America

9.6.1 Trend Analysis

9.6.2 Latin America Sulphur Bentonite Market by Country

9.6.3 Latin America Sulphur Bentonite Market By Type

9.6.4 Latin America Sulphur Bentonite Market By Application

9.6.5 Brazil

9.6.5.1 Brazil Sulphur Bentonite Market By Type

9.6.5.2 Brazil Sulphur Bentonite Market By Application

9.6.6 Argentina

9.6.6.1 Argentina Sulphur Bentonite Market By Type

9.6.6.2 Argentina Sulphur Bentonite Market By Application

9.6.7 Colombia

9.6.7.1 Colombia Sulphur Bentonite Market By Type

9.6.7.2 Colombia Sulphur Bentonite Market By Application

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Sulphur Bentonite Market By Type

9.6.8.2 Rest of Latin America Sulphur Bentonite Market By Application

10. Company Profiles

10.1 Tiger Sul

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 The SNS View

10.2 Deepak Fertilizers

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 The SNS View

10.3 H Sulphur Corp

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 The SNS View

10.4 Devco Australia

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 The SNS View

10.5 Coogee Chemicals

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 The SNS View

10.6 National Fertilizer Limited

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 The SNS View

10.7 NTCS Group

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 The SNS View

10.8 Galaxy Sulfur

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 The SNS View

10.9 Chung Kwang

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 The SNS View

10.10 Coromandel International

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 The SNS View

11. Competitive Landscape

11.1 Competitive Benchmarking

11.2 Market Share Analysis

11.3 Recent Developments

11.3.1 Industry News

11.3.2 Company News

11.3.3 Mergers & Acquisitions

12. USE Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Type

Sulphur-85%

Sulphur-90%

Others

By Application

Fruits and Vegetables

Cereals and Crops

Oilseeds

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Asphalt Market size was valued at USD 249.2 million in 2023. It is expected to grow to USD 389.9 million by 2032 and grow at a CAGR of 5.1% by 2024-2032.

The Concrete Blocks and Bricks Market size was USD 377.18 billion in 2023 and is expected to Reach USD 667.12 billion by 2032 and grow at a CAGR of 6.54% over the forecast period of 2024-2032.

The Antifreeze Market size was valued at USD 5.5 Billion in 2023. It is expected to grow to USD 9.9 Billion by 2032 & grow at a CAGR of 6.9% over the forecast period of 2024-2032.

The Malonic Acid Market size was valued at USD 111.42 Million in 2023 and is expected to reach USD 142.95 Million by 2032, growing at a CAGR of 2.81% over the forecast period of 2024-2032.

The Heat-Resistant coatings market size was valued at USD 6.80 billion in 2023 and is expected to reach USD 10.60 billion by 2032 and grow at a CAGR of 5.06% over the forecast period 2024-2032.

The Pyridine Market Size was valued at USD 726.0 million in 2023 and is expected to reach USD 1142.4 million by 2032 and grow at a CAGR of 5.2% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd