Get More Information on Substrates Market - Request Sample Report

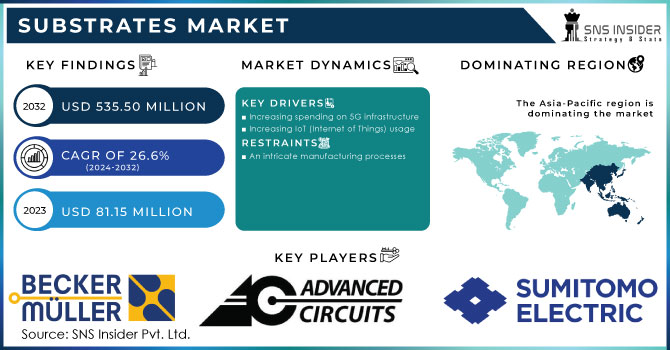

The Substrates Market Size was valued at USD 81.15 Million in 2023 and is expected to grow to USD 535.50 Million by 2032 and grow at a CAGR of 26.6% over the forecast period of 2024-2032.

The substrates market is crucial in various sectors like electronics, automotive, aerospace, and medical devices, as substrates are essential materials for thin-film deposition and coating processes. They play a crucial role in the production of semiconductors, printed circuit boards (PCBs), sensors, and other electronic components. The market offers a range of materials like glass, metal, silicon, and ceramics, all tailored to meet particular application needs. The increasing need for small, high-performing electronic devices such as smartphones, laptops, and wearables is a key factor in driving this market. As semiconductor technology progresses, materials like silicon wafers play a key role in creating smaller, more efficient, and powerful electronic components. The substrates market's growth is being directly impacted by manufacturers seeking materials with better electrical properties, thermal stability, and durability due to the shift towards miniaturization and higher performance. The increasing application of substrates in vital sectors emphasizes their significance in promoting creativity and facilitating the advancement of future technologies. Therefore, it is expected that the need for substrates will grow, particularly in areas with well-established electronics manufacturing industries like Asia-Pacific, leading to further growth in the market.

The automotive sector is experiencing a significant change fueled by the rapid growth of electric vehicles (EVs) and autonomous driving technologies, leading to a high demand for advanced substrates. Substrates play a crucial role in different automotive systems like battery management systems (BMS), advanced driver-assistance systems (ADAS), and in-vehicle infotainment systems. These systems need substrates that provide excellent electrical conductivity, heat resistance, and durability to accommodate the increasing complexity of automotive electronics. The IEA indicated that in 2022, electric vehicle sales worldwide increased to make up 14% of new car sales, compared to only 4% in 2020, showing a notable rise in the need for high-tech electronic parts. This expansion is also supported by government efforts to boost EV usage, like the European Union's Fit for 55 plan that aims to cut net greenhouse gas emissions by 55% by 2030 and prohibits the sale of internal combustion engine cars by 2035. The Bipartisan Infrastructure Law in the United States designates $7.5 Million for creating a nationwide network of EV chargers, continuing to boost the EV industry. These advancements are creating a demand for materials that can sustain high-voltage uses and guarantee safety and effectiveness in electric vehicles. In addition, the growth of ADAS in contemporary cars, providing functions such as lane departure alerts and adaptive cruise control, is anticipated to drive up the demand for substrates, specifically SiC and GaN, that are well-suited for high-power automotive uses. With automakers moving towards electrification and automation, there will be a significant increase in the need for high-performance substrates, highlighting the vital role of the substrates market in the future of the automotive industry.

Drivers

Innovation in Flexible Substrates for Solar Cells and Emerging Applications

The rise of advanced flexible substrates in renewable energy applications is becoming a key market driver in the substrates market. Flexible substrates, such as polycarbonate, are increasingly being integrated into next-generation solar technologies, particularly perovskite solar cells (PSCs), which have shown immense promise due to their flexibility, lightweight structure, and cost-effectiveness. The global shift towards sustainable energy, particularly solar power, has accelerated the demand for innovative materials capable of supporting flexible, high-performance photovoltaic (PV) applications. Polycarbonate, known for its superior flexibility and transparency, plays a crucial role in enabling lightweight solar panels for portable electronics, wearable devices, and infrastructure applications like building-integrated photovoltaics (BIPV). The ability to integrate printed electronic components onto polycarbonate substrates, combined with cost-effective, low-temperature processing, provides immense potential for scalable, low-cost solar manufacturing, driving market growth. This innovation not only supports the solar energy market, but also has ripple effects across industries relying on flexible, efficient substrates for electronic devices, pushing the substrates market to adapt to these evolving needs.An international research group demonstrated a flexible perovskite solar cell (PSC) with a 13.0% power conversion efficiency using polycarbonate substrates, marking a breakthrough in flexible PV applications. The polycarbonate, which exhibits 90% transparency in the visible spectrum, was chosen for its high glass transition temperature and low moisture absorption, outperforming traditional substrates like PET and PEN. Despite the initial challenges posed by polycarbonate's poor solvent resistance and high surface roughness, the team addressed these issues by applying a blade-coated planarization layer of ambient-curable resin, reducing the surface roughness from 1.46 µm to 23 nm and cutting the water vapor transmission rate by half. These improvements allowed for the successful deposition of precursor inks. In durability tests, the cells retained 87% efficiency after 1000 bending cycles at a radius of 20 mm. The entire manufacturing process, including the integration of SnO2 electron transport layers, perovskite layers, and Spiro-MeOTAD hole transport layers, is industrially compatible and suited for low-cost production methods. This innovation represents a leap forward in the flexible solar cell market, positioning polycarbonate substrates as an emerging solution for high-performance, lightweight PV devices .

The Emergence of Eco-Friendly Substrates in the Electronics Industry and the Focus on Sustainability

The increasing recognition of environmental concerns, specifically electronic waste (e-waste), is fueling the need for eco-friendly materials in the electronics sector. As the demand for electronic devices increases worldwide, the importance of efficient recycling methods and sustainable materials is more crucial than ever. The United Nations reported that in 2021, a massive amount of 57.4 million tons of electronic waste was generated globally, and it is predicted to increase to 74 million tons by the year 2030. Scientists have created a new degradable material to help with recycling single-use and wearable devices, as well as to make multilayered circuits more easily.This novel polyimide substrates, which is compatible with current manufacturing methods, aims to address the shortcomings of traditional substrates like Kapton. While Kapton is well-known for its superior thermal and insulating characteristics, it is challenging to recycle and handle. The light-cured polymer in the new material cures rapidly at room temperature, enabling quicker production and simpler integration into advanced electronic structures. Furthermore, the design includes ester groups in its polymer structure that are able to be dissolved in a gentle solution, allowing for the extraction of valuable metals and components from circuits. This technological progress is important because it provides a practical answer to the increasing e-waste issue and also offers a possible economic benefit by retrieving valuable materials. The environmentally friendly strategy follows the overall patterns in the substrates sector, as the need for sustainable and recyclable materials continues to influence manufacturing methods. As more companies aim to lessen their environmental footprint and comply with regulations, the creation of these unique substrates will be crucial in advancing the electronics sector.

Restraints

Striking a balance between innovation and manufacturing feasibility in substrates development.

The fast progress of technology in substrates development for flexible electronics, especially in the realms of soft robotics and the Internet of Things (IoT), poses notable market limitations that could hinder expansion. Aligning innovation with manufacturing feasibility poses a significant challenge. Especially for new substrates operations, it is important to understand that advanced technologies need to be cost-effective in order to be widely used, despite aiming to enhance material quality, yield, and decrease manufacturing expenses. The cost needed for the research and development of new materials, in addition to setting up production processes that meet strict industry standards, can be too high. This is particularly important as industries advocate for materials that can accommodate features needed for future applications such as soft robotic exoskeletons, which improve user mobility and decrease tiredness. The need for these sophisticated materials to deliver dependable performance without compromising cost-efficiency creates challenges in the market. Moreover, the incorporation of flexible hybrid electronics (FHE) into IoT devices highlights the need for superior substrates that support smooth communication and data transfer between connected devices. Nevertheless, reaching the intended level of performance using these novel materials frequently necessitates specific manufacturing methods that may not yet be fine-tuned for mass production. As a result, manufacturers might be reluctant to transition from traditional materials to new options that haven't demonstrated their dependability and cost-effectiveness in large-scale manufacturing. This unwillingness hinders market expansion and limits the advancement of materials that could bolster the growing smart technology sector. Consequently, it is necessary to find a delicate equilibrium between promoting innovation in substrates materials and guaranteeing their feasible production to meet the changing needs of the electronics industry.

by Raw Material

by 2023, Bulk Gallium Nitride (GaN) had become the dominant material in the substrates market, securing a significant revenue share of 37.51%. GaN's superior electrical properties contribute to its dominance in various applications such as power electronics and high-frequency devices, allowing for high efficiency and performance. Wolfspeed and Qorvo have recently introduced new GaN-based products that improve performance in electric vehicles and 5G technology, leading to increased market expansion. As an example, Wolfspeed launched its 200mm GaN-on-SiC wafers designed to enhance the efficiency of RF devices and power systems. Moreover, Transphorm has created advanced GaN power components that cater to the growing need for effective power transformation in renewable energy installations. The increased utilization of Bulk GaN substrates in various industries has been aided by recent progress in GaN technology, including the implementation of new fabrication methods and improvements in thermal management. These advancements reaffirm Bulk GaN's foothold in the substrates market and underscore its crucial role in driving the progress of future electronic devices, ultimately backing the shift towards more effective and environmentally friendly technology solutions.

by Application

The computing sector was the leading force in the substrates market in 2023, securing an impressive 35.44% portion of the revenue. The rise is mainly due to the growing need for high-performance computing (HPC) solutions and improvements in semiconductor technology. Intel and NVIDIA have made great progress in incorporating advanced substrates to improve the performance of their processors and GPUs. Intel's new Meteor Lake design, featuring advanced substrates materials, enables better energy efficiency and increased computing power. Furthermore, NVIDIA has launched the H100 Tensor Core GPU which utilizes cutting-edge substrates to speed up AI workloads and data-heavy applications. The demand for faster data processing and energy efficiency in data centers has been accelerated by the increased emphasis on AI and machine learning. With the growth of cloud computing, it is expected that the substrates market will see more investments in materials that support greater integration and miniaturization of components. The intersection of these technological advancements with substrates innovation highlights the crucial impact that computing applications have in influencing the future direction of the substrates market, stimulating demand and progress in different sectors.

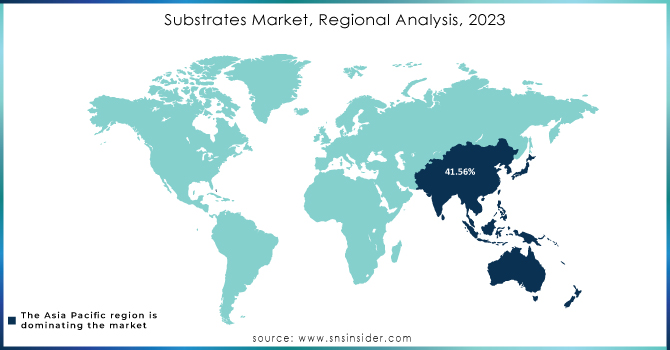

by 2023, the Asia-Pacific region had become the top contender in the substrates market, securing a notable 41.56% revenue share. The main reason for this expansion is the quick progress in technology and the large investments in semiconductor production in countries such as China, Japan, and South Korea. China's continuous efforts to strengthen its semiconductor sector have resulted in a growing need for top-notch substrates, enabling domestic producers to innovate and improve their production capacity. Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Electronics are leading the way by introducing new substrates technologies that enable advanced computing and consumer electronics. An example is the recent progress made by TSMC in enhancing its 5nm and 3nm process nodes through the use of new substrates to enhance chip performance and energy efficiency. Furthermore, Japan's dedication to growing its semiconductor industry has resulted in partnerships between local companies and international corporations, improving the substrates supply chain. The coming together of these advancements underscores the strategic significance of Asia-Pacific in the substrates market, as it remains at the forefront in manufacturing, creativity, and financial backing, influencing the worldwide arena of sophisticated electronics.

In 2023, North America emerged as the fastest-growing region in the substrates market, driven by significant technological advancements and a robust demand for high-performance materials in various applications. The region accounted for a notable share of the global substrates market, fueled by the increasing need for advanced electronics in computing, telecommunications, and automotive sectors. Companies such as GlobalWafers and Silicon Valley Microelectronics have launched innovative substrates solutions that cater to the rising demand for high-efficiency semiconductor devices. For instance, GlobalWafers announced the expansion of its manufacturing capabilities in the U.S. to produce advanced silicon wafers and engineered substrates, aligning with the growing trends in electric vehicles (EVs) and renewable energy technologies. Furthermore, the U.S. government's push to strengthen domestic semiconductor manufacturing through initiatives like the CHIPS Act has attracted investments from major players, fostering innovation and growth in the substrates market. This regulatory support, combined with a vibrant ecosystem of research institutions and tech companies, positions North America as a critical hub for substrates development, ultimately contributing to advancements in the broader electronics industry and enhancing competitiveness in global markets.

Need any customization research on Substrates Market - Enquiry Now

Key Players

some key players in the substrates market along with their product offerings:

TTM Technologies Inc. (PCB, flexible circuits, and advanced packaging solutions)

BECKER & MULLER (specialty substrates for electronic applications)

SCHALTUNGSDRUCK GMBH (printed circuit boards and hybrid substrates)

Advanced Circuits (custom PCBs and quick-turn prototyping)

Sumitomo Electric Industries Ltd (high-performance substrates for electronic devices)

Wurth Elektronik Group (Wurth Group) (electronic components and substrates)

AMD (advanced semiconductor substrates for CPUs and GPUs)

Viettel High Tech (communication substrates and electronic solutions)

NextFlex (flexible hybrid electronics and advanced substrates)

Infineon Technologies Inc. (power semiconductor substrates and integrated circuits)

LG Innotek (multi-layer ceramic substrates and advanced electronic components)

Onsemi (silicon substrates for power management and automotive applications)

NXP Semiconductors (RF and high-performance substrates for automotive and IoT)

Taiwan Semiconductor Manufacturing Company (TSMC) (advanced semiconductor substrates for chips)

Sankyo Oilless Industry Corp. (high-quality substrates for electronic applications)

Imasen Electric Industrial Co., Ltd. (ceramic substrates for automotive and industrial use)

Mitsubishi Materials Corporation (high-performance substrates and materials for electronics)

Others

Recent Development

In December 2022, AMD and Viettel High Tech successfully deployed a field test for a 5G mobile network using AMD Xilinx Zyng UltraScalet MPSoCs. With more than 130 million mobile subscribers, Viettel High Tech, the largest telecom provider in Vietnam, has a long experience of deploying new networks more quickly thanks to new 5G remote radio heads. It is intended to satisfy the rising capacity and performance requirements worldwide mobile users.

In February 2022,Project Call 7.0 (PC 7.0), the most recent request for proposals, was published NextFlex, America's Flexible Hybrid Electronics (FHE) Manufacturing Institute, in order to support Department of Defense requirements. PC 7.0 seeks to fund projects that improve the creation and use of FHE while tackling important problems with enhanced production. Since NextFlex's establishment, an estimated USD 100 million has been set aside for projected investments in FHE. After the project value for PC 7.0 exceeds USD 11.5 million (project value and investment estimates including cost), it will be worth more than USD 128 million sharing).

In July 2023, mobility technology company Magna and Onsemi, a pioneer in intelligent power and sensing technologies, announced a long-term supply agreement (LTSA) that will allow Magna to include Onsemis EliteSiC intelligent power solutions into its eDrive systems. by utilizing the industry-leading EliteSiC MOSFET technology from Onsemi, Magna eDrive systems might increase cooling performance, accelerate charging and acceleration rates, and increase the range of electric cars (EVs).

LG Innotek unveiled the 2-Metal COF in March 2023 at the International Consumer Electronics Show (CES). A semiconductor substrate package called COF (Chip on Film) connects the display to the main printed circuit board. It facilitates the shrinking of display bezels and module miniaturization in electronic products including TVs, laptops, monitors.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 81.15 Million |

| Market Size by 2032 | USD 535.50 Million |

| CAGR | CAGR of 26.6 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Raw Material (GaSb, InSb, Bulk GaN, Ga2O3, Bulk AlN, Single crystal diamond, Engineered substrates and templates) • By Application (Computing, Consumer, Industrial/Medical, Communication, Automotive, Military/Aerospace) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | TTM Technologies Inc., BECKER & MULLER, SCHALTUNGSDRUCK GMBH, Advanced Circuits, Sumitomo Electric Industries Ltd, Wurth Elektronik Group (Wurth Group), AMD, Viettel High Tech, NextFlex, Infineon Technologies Inc., LG Innotek, Onsemi, NXP Semiconductors, Taiwan Semiconductor Manufacturing Company (TSMC), Sankyo Oilless Industry Corp., Imasen Electric Industrial Co., Ltd., and Mitsubishi Materials Corporation. & Others |

| Key Drivers | • Innovation in Flexible Substrates for Solar Cells and Emerging Applications • The Emergence of Eco-Friendly Substrates in the Electronics Industry and the Focus on Sustainability |

| Restraints | • Striking a balance between innovation and manufacturing feasibility in substrates development. |

Ans: The Substrates Market grow at a CAGR of 26.6% over the forecast period of 2024-2032.

Ans: The Substrates Market size was valued at USD 81.15 Million in 2023 and is expected to grow to USD 535.50 Million by 2032

Ans: The major growth factor of the Substrates Market is the increasing demand for miniaturized and high-performance electronic devices across various industries, including computing, automotive, and consumer electronics.

Ans: Asia-Pacific dominated the Substrates Market in 2023.

Ans: The Bulk GaN segment dominated the Substrates Market.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Wafer Production Volumes, by Region (2023)

5.2 Chip Design Trends (Historic and Future)

5.3 Fab Capacity Utilization (2023)

5.4 Supply Chain Metrics

6. Competitive Landscape

6.1 List of Major Companies, by Region

6.2 Market Share Analysis, by Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Substrates Market Segmentation, by Raw Material

7.1 Chapter Overview

7.2 GaSb

7.2.1 GaSb Market Trends Analysis (2020-2032)

7.2.2 GaSb Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 InSb

7.3.1 InSb Market Trends Analysis (2020-2032)

7.3.2 InSb Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 Bulk GaN

7.4.1 Bulk GaN Market Trends Analysis (2020-2032)

7.4.2 Bulk GaN Market Size Estimates and Forecasts to 2032 (USD Million)

7.5 Ga2O3

7.5.1 Ga2O3Market Trends Analysis (2020-2032)

7.5.2 Ga2O3Market Size Estimates and Forecasts to 2032 (USD Million)

7.6 Bulk AlN

7.6.1 Bulk AlN Market Trends Analysis (2020-2032)

76.2 Bulk AlN Market Size Estimates and Forecasts to 2032 (USD Million)

7.7 Single crystal diamond

7.7.1 Single crystal diamondMarket Trends Analysis (2020-2032)

7.7.2 Single crystal diamond Market Size Estimates and Forecasts to 2032 (USD Million)

7.8 Engineered substrates and templates

7.8.1 Engineered substrates and templates Market Trends Analysis (2020-2032)

7.8.2 Engineered substrates and templates Market Size Estimates and Forecasts to 2032 (USD Million)

8. Substrates Market Segmentation, by Application

8.1 Chapter Overview

8.2 Computing

8.2.1 Computing Market Trends Analysis (2020-2032)

8.2.2 Computing Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Consumer

8.3.1 Consumer Market Trends Analysis (2020-2032)

8.3.2 Consumer Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Industrial/Medical

8.4.1 Industrial/Medical Market Trends Analysis (2020-2032)

8.4.2 Industrial/Medical Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 Communication

8.5.1 Communication Market Trends Analysis (2020-2032)

8.5.2 Communication Market Size Estimates and Forecasts to 2032 (USD Million)

8.6 Automotive

8.6.1 Automotive Market Trends Analysis (2020-2032)

8.6.2 Automotive Market Size Estimates and Forecasts to 2032 (USD Million)

8.7 Military/Aerospace

8.7.1 Military/Aerospace Market Trends Analysis (2020-2032)

8.7.2 Military/Aerospace Market Size Estimates and Forecasts to 2032 (USD Million)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.2.3 North America Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.2.4 North America Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.5 USA

9.2.5.1 USA Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.2.5.2 USA Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.6 Canada

9.2.6.1 Canada Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.2.6.2 Canada Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.2.7 Mexico

9.2.7.1 Mexico Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.2.7.2 Mexico Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.3.1.3 Eastern Europe Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.4 Eastern Europe Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.5 Poland

9.3.1.5.1 Poland Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.5.2 Poland Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.6 Romania

9.3.1.6.1 Romania Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.6.2 Romania Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.7.2 Hungary Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.8.2 Turkey Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.1.9.2 Rest of Eastern Europe Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.3.2.3 Western Europe Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.4 Western Europe Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.5 Germany

9.3.2.5.1 Germany Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.5.2 Germany Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.6 France

9.3.2.6.1 France Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.6.2 France Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.7 UK

9.3.2.7.1 UK Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.7.2 UK Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.8 Italy

9.3.2.8.1 Italy Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.8.2 Italy Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.9 Spain

9.3.2.9.1 Spain Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.9.2 Spain Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.10.2 Netherlands Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.11.2 Switzerland Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.12 Austria

9.3.2.12.1 Austria Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.12.2 Austria Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.3.2.13.2 Rest of Western Europe Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4 Asia-Pacific

9.4.1 Trends Analysis

9.4.2 Asia-Pacific Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.4.3 Asia-Pacific Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.4 Asia-Pacific Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.5 China

9.4.5.1 China Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.5.2 China Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.6 India

9.4.5.1 India Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.5.2 India Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.5 Japan

9.4.5.1 Japan Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.5.2 Japan Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.6 South Korea

9.4.6.1 South Korea Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.6.2 South Korea Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.7 Vietnam

9.4.7.1 Vietnam Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.2.7.2 Vietnam Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.8 Singapore

9.4.8.1 Singapore Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.8.2 Singapore Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.9 Australia

9.4.9.1 Australia Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.9.2 Australia Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.4.10 Rest of Asia-Pacific

9.4.10.1 Rest of Asia-Pacific Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.4.10.2 Rest of Asia-Pacific Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.1.3 Middle East Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.4 Middle East Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.5 UAE

9.5.1.5.1 UAE Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.5.2 UAE Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.6.2 Egypt Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.7.2 Saudi Arabia Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.8.2 Qatar Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.1.9.2 Rest of Middle East Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.2.3 Africa Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.2.4 Africa Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.2.5.2 South Africa Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.2.6.2 Nigeria Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.5.2.7.2 Rest of Africa Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Substrates Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.6.3 Latin America Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.6.4 Latin America Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.5 Brazil

9.6.5.1 Brazil Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.6.5.2 Brazil Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.6 Argentina

9.6.6.1 Argentina Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.6.6.2 Argentina Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.7 Colombia

9.6.7.1 Colombia Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.6.7.2 Colombia Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Substrates Market Estimates and Forecasts, by Raw Material (2020-2032) (USD Million)

9.6.8.2 Rest of Latin America Substrates Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10. Company Profiles

10.1 TTM Technologies Inc.

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 BECKER & MULLER

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 SCHALTUNGSDRUCK GMBH

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Advanced Circuits

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Sumitomo Electric Industries Ltd

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Wurth Elektronik Group

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 AMD

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Viettel High Tech

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 NextFlex

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Infineon Technologies Inc.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Raw Material

GaSb

InSb

Bulk GaN

Ga2O3

Bulk AlN

Single crystal diamond

Engineered substrates and templates

By Application

Computing

Consumer

Industrial/Medical

Communication

Automotive

Military/Aerospace

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia-Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia-Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Electrical Resistor Market Size was valued at USD 5.92 billion in 2023 and is expected to grow at a CAGR of 5.51% to reach USD 9.56 billion by 2032.

3D Holographic Market size was valued at USD 3143 million in 2023 and is expected to grow to USD 30606.48 million by 2032 and grow at a CAGR of 28.95 % over the forecast period of 2024-2032.

The LED Light Engine Market was valued at USD 45.98 billion in 2023 and is expected to reach USD 145.44 billion by 2032, growing at a CAGR of 13.69% over the forecast period 2024-2032.

The Electrical Enclosures Market size was $ 7.91 Billion in 2023 and is estimated to Reach USD 13.95 billion by 2032 and grow at a CAGR of 6.56% over the forecast period of 2024-2032.

The Programmable Robots Market was valued at USD 3.44 billion in 2023 and is expected to reach USD 13.22 billion by 2032, growing at a CAGR of 16.16% over the forecast period 2024-2032.

The Near-Eye Display Market Size was valued at USD 2.31 Billion in 2023 and is expected to grow at a CAGR of 24.90% to reach USD 17.08 Billion by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd