The United States Stormwater Management Market Size was USD 7.1 billion in 2023 and is projected to grow at a CAGR of 7.8% to reach USD 13.95 billion by 2032. The environmental impact of stormwater runoff can be valuable for the U.S. stormwater management market. For instance, Research shows that over 70% of U.S. cities are struggling with aging infrastructure, driving demand for modern stormwater systems. Furthermore, increasing public awareness of water conservation and environmental sustainability has led to a rise in green infrastructure projects. Data on the adoption rates of innovative solutions, such as permeable pavements and bioretention systems, further demonstrate the evolving market dynamics.

Get more information on US Stormwater Management Market - Request Sample Report

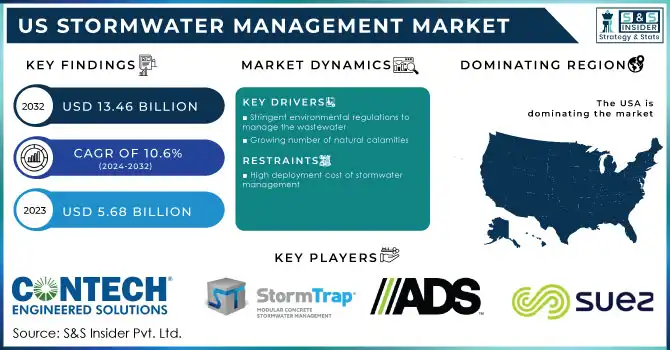

Driver:

Growing Demand for Eco-Friendly Solutions and Green Infrastructure Practices Enhances the U.S. Stormwater Management Market Growth

The increasing push for sustainability in urban planning and construction has driven the demand for eco-friendly stormwater management solutions. Green infrastructure includes rain gardens, permeable pavements, and green roofs that manage stormwater with sensitivity to the environment, reducing pollution and improving water quality. These are gaining momentum across the U.S. as municipalities seek ways to meet environmental regulations and provide more resilient infrastructure. A growing awareness of the benefits that come from better integration of nature-based systems is widening the market and encouraging innovation in the range of products available for stormwater management.

Restraint:

High Initial Installation Costs of Advanced Stormwater Management Systems Hinder Widespread Adoption in the U.S. Market

One of the primary challenges limiting the widespread adoption of advanced stormwater management systems is the high initial installation cost. Advanced technologies deal with stormwater retention systems, underground chambers, and other developed filtration solutions, which are pretty capital-intensive; hence, participation is always limited by small municipalities or those on a tight budget. While these solutions ensure long-term benefits, both environmentally and economically, the initial capital cost holds them back so big. Most organizations use either traditional systems or cheaper options, hampering the full potential of the market and development opportunities for more advanced technologies.

Opportunity:

Expanding Government Regulations and Environmental Policies Open Doors for Innovation and Growth in U.S. Stormwater Management Market

The U.S. government's increasing emphasis on environmental regulations and stormwater management policies presents significant growth opportunities for the industry. Excerpts of particular relevance to flood concerns, water pollution, and climate change show that federal and local authorities continue to tighten their stormwater management regulations, while encouraging the consideration of advanced technologies. This encourages opportunities for those firms offering different solutions for stormwater, such as sustainable urban drainage systems and real-time water quality monitoring technologies. An increase in investments in infrastructure and incentives being given for the use of eco-friendly solutions would definitely boost up market growth over the next years.

Challenge:

Climate Change and Increased Frequency of Extreme Weather Events Create Uncertainty and Strain U.S. Stormwater Management Systems

The growing impact of climate change, particularly in the form of more frequent and intense storms, presents a significant challenge for the U.S. stormwater management market. These extreme weather events comprise heavy rainfall and flash floods, which apply a lot of stress to the existing infrastructure, probably not designed for that. The element of uncertainty around this makes it rather difficult to formulate solutions that would accommodate the different rainfall patterns. Such unpredictability poses performance problems with a tendency for the systems to fail. It is compounded by the fact that the stormwater systems need continuous upgrading in order to sustain future climate-related risks.

By Service Type

In 2023, the Installation Services segment accounted for the largest share of the U.S. stormwater management market, contributing approximately 43% of the total revenue. The demand for installation services has surged due to the increasing focus on urban development, infrastructure renewal, and the need to comply with environmental regulations.

Key players such as Advanced Drainage Systems Inc. (ADS) and Contech Engineered Solutions have developed innovative products, including advanced stormwater detention and treatment systems, to meet regulatory standards. ADS, for instance, introduced its StormTech MC² system, which offers more efficient stormwater management, reducing installation time and cost.

The Annual Maintenance Services segment is expected to grow at the largest CAGR during the forecast period in the U.S. stormwater management market. As municipalities and other entities continue to adopt ever-more complex stormwater systems, regular maintenance to long-term efficiency and environmental standards becomes the norm. Companies such as Suntree Technologies Inc. and Hydro International have expanded their operations to include maintenance solutions for their respective stormwater treatment systems.

By Solution Type

In 2023, the Detention & Infiltration segment dominated the U.S. stormwater management market, holding the largest market share. This solution type is key in the management of stormwater runoff to temporarily hold it up until the surplus parts start percolating into the ground, thus causing no flooding and possible impairment to water quality. Growth in this segment is derived from the increasing requirements to deal with flooding and growing strictness in environmental laws including the Clean Water State Revolving Fund. As urbanization increases and so do flooding problems within the urban areas, detention and infiltration of stormwater has become imperative in the design for sustainable infrastructure.

The Biofiltration segment is projected to experience the largest CAGR during the forecasted period in the U.S. stormwater management market. Biofiltration systems are an evolving trend in their application, using vegetation, soil, and microorganisms for the treatment and filtration of stormwater. It is increasingly adopted in recent times due to environmental sustainability and the cost-effectiveness of such systems. Biofiltration systems definitely help to meet regulatory requirements and are increasingly finding applications in green infrastructure projects. This shift toward nature-based solutions, coupled with technological advancements and product development, has placed the biofiltration segment in a place for serious growth within the U.S. stormwater management market.

By End-user

In 2023, the Community, Government & Military segment captured the largest market share in the U.S. stormwater management market. This sector is particularly driven by a push in stringent regulations, environmental mandates, and resilient infrastructure. Therefore, local municipalities, military installations, and non-profit organizations consider advanced approaches in stormwater management in an attempt to deal with floods, polluting, or general water stressors. While it is an emerging area of great concern globally, the US military increasingly takes green infrastructure installation in military facilities for compliance requirements with an ecological perspective besides operational preparedness. Strong growth in this segment indicates the immediate need for Storm Water Management in public areas where safety, environmental sustainability, and long-term infrastructural investment come into play.

The Commercial segment is expected to grow at the largest CAGR during the forecasted period in the U.S. stormwater management market. Commercial properties and businesses are increasingly adopting stormwater management systems due to increasing pressure on environmental standards and sustainability goals. The expanding need for commercial properties to meet regulatory requirements and adopt green infrastructure practices drives the growth of this segment. Increasing trends in sustainability, conservation of water, and stormwater management in corporate strategies will help position the commercial segment for major growth in the future, as businesses work to improve their environmental footprint.

United States Dominate the Stormwater Management Market in 2023 Driven by Urbanization, Infrastructure Needs, and Stringent Regulations

In 2023, the United States dominated the stormwater management market, holding the largest market share due to its substantial infrastructure needs, increasing urbanization, and stringent environmental regulations.

This dominance is largely driven by the growing need to address stormwater runoff and flooding, particularly in large metropolitan areas, where aging infrastructure and rapid urban expansion have led to challenges in water management.

For example, cities like New York, Los Angeles, and Chicago have faced severe flooding and water pollution, prompting the adoption of advanced stormwater management systems.

The U.S. government’s regulatory push, including the Clean Water State Revolving Fund and the National Pollutant Discharge Elimination System (NPDES), has further bolstered the market by encouraging municipalities to invest in advanced stormwater solutions. These regulations, alongside rising environmental awareness, have contributed to the U.S. maintaining its leadership position in the stormwater management market.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Some of the major players in the US Stormwater Management Market are:

Contech Engineered Solutions LLCAdvanced Drainage Systems Inc.

Suez Group

AquaShield, Inc.

Triton Stormwater Solutions

Stormtrap LLC

Stormtank

Thompson Pipe Group, Inc

In January 2025, Advanced Drainage Systems, in collaboration with The Harris Poll, released an annual survey revealing that more than half of Americans are concerned about flooding in and around their homes. The survey also found that 64% of Americans believe stormwater negatively impacts their communities.

| Report Attributes | Details |

| Market Size in 2023 | US$ 5.68 Billion |

| Market Size by 2032 | US$ 13.46 Billion |

| CAGR | CAGR of 10.6% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2023-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Installation Services, Repair Services, Annual Maintenance Services, and Others) • By Solution Type (Detention & infiltration, Biofiltration, Separation, Filtration, Specialty Filters, and Others) • By End-user (Community, Government & military, commercial, Industrial, Medical and education, and others) |

| Regional Analysis/Coverage | USA |

| Company Profiles | Contech Engineered Solutions LLC, Stormtrap, Advanced drainage systems Inc., Suez Group, Hydro International UK Ltd., AquaShield, Inc., Triton Stormwater Solutions, Apex Companies LLC, Stormtank, Forterra, Inc. |

Ans: The expected CAGR of the US Stormwater Management Market during the forecast period is 8.72%.

Ans: The market size of the US Stormwater Management Market is valued at USD 5,409.29 million in 2022.

Ans: The major key players in the Stormwater Management Market are Contech Engineered Solutions LLC, Stormtrap, Advanced drainage systems Inc., Suez Group, Hydro International UK Ltd., AquaShield, Inc., Triton Stormwater Solutions, Apex Companies LLC, Stormtank, and Forterra, Inc.

Ans: US Stormwater Management Market is bifurcated into 3 major segments: 1. By Service Type 2. By Solution Type 3. By End-users.

Table Of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Flood and Disaster Mitigation Statistics

5.2 Operational and Maintenance Costs

5.3 Volume of stormwater runoff managed annually

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. US Stormwater Management Market Segmentation, By Service Type

7.1 Chapter Overview

7.2 Installation Services

7.2.1 Installation Services Market Trends Analysis (2020-2032)

7.2.2 Installation Services Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Repair Services

7.3.1 Repair Services Market Trends Analysis (2020-2032)

7.3.2 Repair Services Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Annual Maintenance Services

7.4.1 Annual Maintenance Services Market Trends Analysis (2020-2032)

7.4.2 Annual Maintenance Services Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Others

7.5.1 Others Market Trends Analysis (2020-2032)

7.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. US Stormwater Management Market Segmentation, By Solution Type

8.1 Chapter Overview

8.2 Detention & infiltration

8.2.1 Detention & infiltration Market Trends Analysis (2020-2032)

8.2.2 Detention & infiltration Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Biofiltration

8.3.1 Biofiltration Market Trends Analysis (2020-2032)

8.3.2 Biofiltration Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Separation

8.4.1 Separation Trends Analysis (2020-2032)

8.4.2 Separation Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Filtration

8.5.1 Filtration Trends Analysis (2020-2032)

8.5.2 Filtration Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Specialty Filters

8.6.1 Specialty Filters Trends Analysis (2020-2032)

8.6.2 Specialty Filters Size Estimates and Forecasts to 2032 (USD Billion)

8.7 Others

8.7.1 Others Trends Analysis (2020-2032)

8.7.2 Others Size Estimates and Forecasts to 2032 (USD Billion)

9. US Stormwater Management Market Segmentation, By End-User

9.1 Chapter Overview

9.2 Community, Government & Military

9.2.1 Community, Government & Military Market Trends Analysis (2020-2032)

9.2.2 Community, Government & Military Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Commercial

9.3.1 Commercial Market Trends Analysis (2020-2032)

9.3.2 Commercial Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Industrial

9.4.1 Industrial Market Trends Analysis (2020-2032)

9.4.2 Industrial Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Medical and Education

9.5.1 Medical and Education Market Trends Analysis (2020-2032)

9.5.2 Medical and Education Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Others

9.6.1 Others Market Trends Analysis (2020-2032)

9.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Company Profiles

10.1 Contech Engineered Solutions LLC

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 SWOT Analysis

10.2 Advanced Drainage Systems Inc.

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Suez Group

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Hydro International UK Ltd.

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 AquaShield, Inc.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Triton Stormwater Solutions

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 StormTrap LLC

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Apex Companies LLC

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Stormtank

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Thompson Pipe Group, Inc

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

MARKET SEGMENTATION

By Service Type

Installation Services

Repair Services

Annual Maintenance Services

Others

By Solution Type

Detention & infiltration

Biofiltration

Separation

Filtration

Specialty Filters

Others

By End-user

Community, Government & Military

Commercial

Industrial

Medical and Education

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest Of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Oilfield Integrity Management Market size was valued at USD 14.22 billion in 2022 and is expected to grow to USD 26.51 billion by 2030 and grow at a CAGR of 8.1 % over the forecast period of 2023-2030.

The Wind Power Market size was valued at USD 106.57 billion in 2023 and is expected to grow to USD 193.79 billion by 2032 with a growing CAGR of 6.87% over the forecast period of 2024-2032.

The Hydropower Turbine Market size was valued at USD 2.33 billion in 2023 and is expected to grow to USD 3.55 billion by 2031 and grow at a CAGR of 5.4% over the forecast period of 2024-2031.

The Battery Contract Manufacturing Market size was valued at USD 4.6 billion in 2022 and is expected to grow to USD 14.90 billion by 2030 with an emerging CAGR of 15.8% over the forecast period of 2023-2030.

The Utility Poles Market size was valued at USD 33.15 billion in 2022 and is expected to grow to USD 54.04 billion by 2030 and grow at a CAGR of 6.3% over the forecast period of 2023-2030.

The Enhanced Oil Recovery Market size was valued at USD 53.51 billion in 2023 and is expected to grow to USD 90.58 billion by 2031 and grow at a CAGR of 6.8 % over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd