Get More Information on Sports & Energy Drinks Market - Request Sample Report

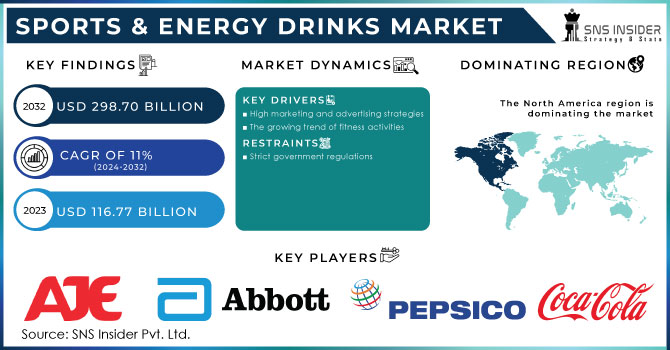

The Sports & Energy Drinks Market size was valued at USD 116.77 billion in 2023 and is expected to reach USD 298.70 billion by 2032 and grow at a CAGR of 11% over the forecast period of 2024-2032.

Sports and energy drinks can replenish glucose, fluids, and electrolytes such as sodium, potassium, magnesium, and calcium which are lost during hard exercise, as well as increase endurance.

Professional and amateur athletes utilize sports and energy drinks to increase their performance and recovery. Sports beverages contain carbohydrates, electrolytes, and fluids that assist athletes stay hydrated and energized while exercising. Casual Sports Drink Users take sports drinks on occasion, such as when they are weary or agitated. Casual sports drink users are not often aiming for the same level of performance benefits as sportspersons/athletes or recreational users. People who drink sports drinks as part of their entire health and wellness practice are classified as Lifestyle Users. Sports drinks may be used by lifestyle users to help them stay hydrated, raise their energy levels, or improve their overall mood.

KEY DRIVERS

High marketing and advertising strategies

The growing trend of fitness activities

Due to the rise of problems like high blood pressure, obesity, and many others, consumers have grown more active and participate in sports and athletic activities. Earlier, Sports and energy drinks used to be reserved for athletes and other sports professionals. But now, Consumers are looking for quick and practical dietary solutions. The demand for sports drinks and cans is increasing as a result of rising disposable income and an increase in the working population. Sports drink producers are being encouraged to develop new products that cater to changing consumer preferences by the shift in market patterns. The younger generation is particularly involved in sports and fitness.

RESTRAIN

Strict government regulations

Strict regulations on sports and energy drinks restrict sales of drinks to children below the age of 16. The Canadian government regulates these drinks under the Food and Drug Act. The act sets limits on the caffeine content of these drinks. The U.S. Food and Drug Administration (FDA) regulates sports and energy drinks under the Dietary Supplement Health and Education Act. The act does not require sports and energy drinks to be approved by the FDA before they are marketed, but it does require manufacturers to provide the FDA with knowledge about the ingredients of their products. The European Union regulates clear and accurate information about the ingredients and nutritional content of its products.

OPPORTUNITY

A growing number of fitness centers

Raising participation in sports and athletic events

The sports and energy drinks industry is constantly innovating and introducing new and innovative products. This is helping to keep the market growing by providing consumers with more choices and options. There is also rising participation in sports and athletic events, such as marathons, triathlons, and cycling races. This has further increased the demand for sports and energy drinks to help athletes perform better and recover faster.

CHALLENGES

Increase counterfeit drinks in the market

High cost of Sports & Energy Drinks

High costs can contribute to a decrease in demand for sports and energy drinks, as customers may opt for cheaper alternatives or avoid them entirely. This is especially true for low-income or budget-conscious consumers. High prices may also cause consumers' tastes to shift away from sports and energy drinks. Water, juice, or coffee are examples of beverages that consumers may convert to because they believe they are more inexpensive or healthier.

The Ukraine-Russia conflict has had an impact on the food and beverage industry. Ukraine is widely regarded as Europe's breadbasket, and the crisis there was expected to have a substantial impact on sports and energy drinks. The battle has disrupted the supply chain of materials required by manufacturers. As a result, the epidemic has raised demand for and sales of energy drinks. Despite the war in 2022, energy drink sales increased by over 15%.

Recession has declined the sales of sports and energy drinks. Energy drinks are deeply embedded in people's daily lives, which may explain why they are so resilient in a country where categories such as beer and carbonates have been steadily dropping. However, the high cost of drinks may lead to a shift in consumer preferences toward other beverages. Energy drinks sold $6 billion in the Natural Enriched and Conventional outlets in the 52 weeks ending July 16, 2023 (a 14.1% increase from 2022). The price rise of energy drinks has lessened demand; hence, production capacity may be delayed.

By Type

Sports Drinks

Energy Drinks

By distribution channel

Convenience Stores

Online Retailers

Supermarkets & Hypermarkets

other

By End-user

Sportspersons/Athletes

Recreational users

Casual sports drink users

Lifestyle users

North America is the largest market for sports and energy drinks, followed by Asia Pacific. Increased engagement in sports and other physical activities, as well as the increased popularity of energy drinks, are driving the market. The U.S. is North America's largest market for sports and energy beverages. Because of the increased popularity of sports and fitness activities in North America, market participants are introducing sports drinks with added benefits such as no sugar, low-calorie, and plant-based products.

Asia Pacific is the fastest-growing market for sports and energy drinks. The increasing disposable income of consumers in the region, as well as the growing popularity of sports and other physical activities, are driving market expansion. Consumers are dealing with difficulties such as high blood pressure, diabetes, obesity, and many others. China, India, and Japan are the Asia Pacific's major markets for sports and energy beverages.

Europe has seen significant development in sports and energy drinks, owing to increased engagement in sports and other physical activities, as well as the growing popularity of sports beverages. Germany, the United Kingdom, and France have Europe's largest sports and energy drink markets. Furthermore, when food habits and lifestyle modifications changed, customers' appetite for health and energy beverages increased.

Latin America, the Middle East, and Africa are emerging beverage markets. Brazil is Latin America's largest market for sports and energy beverages. Growing worries about health and fitness among the younger generation are prompting market participants to develop nutritionally beneficial and low-calorie goods.

Need any customization research on Sports & Energy Drinks Market - Enquiry Now

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

AJE Group, Abbott Nutrition Co., BA sports nutrition LL, The Coca-Cola Company, PepsiCo Inc., Herbalife And Energy Drinks, Inc., Monster Beverage Corporation, Red Bull GmbH, True and Energy Drinks, Glanbia plc, Now Health Group, Inc., and other key players are mentioned in the final report.

In 2022 Blast Asset LLC, a subsidiary of Monster Beverage Corporation, announced the completion of its acquisition of the assets of Vital Pharmaceuticals, Inc. and some of its subsidiaries for a price of approximately $362 million, subject to adjustments. Bang Energy drinks and a beverage production facility in Phoenix, Arizona are among the assets bought.

In 2022 PepsiCo will introduce hemp seed-infused energy drinks designed to help people relax. The drinks are available in three different flavors and have less caffeine than other Rockstar products.

In 2022 Limca, a brand of The Coca-Cola Company, introduced its first-ever variation of the sports drink "Limca Sportz" in India. The sports drink comes in lemon and lime flavors. Limca Sportz is a glucose and electrolyte-based beverage used by athletes to rehydrate.

| Report Attributes | Details |

| Market Size in 2023 | US$ 116.77 Billion |

| Market Size by 2030 | US$ 298.70 Billion |

| CAGR | CAGR of 11 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Sports Drinks, Energy Drinks) • By distribution channel (convenience stores, online retailers, supermarkets & hypermarkets, and other distribution channel types) • By End-user (Sportsperson/Athletes, Recreational users, Casual sports drink users, Lifestyle users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | AJE Group, Abbott Nutrition Co., BA sports nutrition LL, The Coca-Cola Company, PepsiCo Inc., Herbalife And Energy Drinks, Inc., Monster Beverage Corporation, Red Bull GmbH, True and Energy Drinks, Glanbia plc, Now Health Group, Inc |

| Key Drivers | • High marketing and advertising strategies • The growing trend of fitness activities |

| Market Challenges | • Increase counterfeit drinks in the market • High cost of Sports & Energy Drinks |

Ans: The Sports & Energy Drinks Market is anticipated to expand by 11% from 2024 to 2032.

Ans: USD 298.70 billion is expected to grow by 2032.

Ans: North America is dominating the Sports and Energy Drinks market.

Ans: Challenges are the Increase in counterfeit drinks in the market and the high cost of Sports and Energy Drinks.

Ans: The Sports & Energy Drinks Market size was valued at USD 116.77 billion in 2023

TABLE OF CONTENT

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of Ukraine- Russia War

4.2 Impact of Ongoing Recession

4.3. Introduction

4.3.1 Impact on Major Economies

4.3.1.1 US

4.3.1.2 Canada

4.3.1.3 Germany

4.3.1.4 France

4.3.1.5 United Kingdom

4.3.1.6 China

4.3.1.7 Japan

4.3.1.8 South Korea

4.3.1.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Sports & Energy Drinks Market Segmentation, By Type

8.1 Sports Drinks

8.2 Energy Drinks

9. Sports & Energy Drinks Market Segmentation, By Distribution Channel

9.1 convenience stores

9.2 online retailers

9.3 supermarkets & hypermarkets

9.4 other

10. Sports & Energy Drinks Market Segmentation, By End-user

10.1 Sportspersons/Athletes

10.2 Recreational users

10.3 Casual sports drink users

10.4 Lifestyle users

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Sports & Energy Drinks Market by Country

11.2.2 North America Sports & Energy Drinks Market by Type

11.2.3 North America Sports & Energy Drinks Market by Distribution Channel

11.2.4 North America Sports & Energy Drinks Market by End-user

11.2.5 USA

11.2.5.1 USA Sports & Energy Drinks Market by Type

11.2.5.2 USA Sports & Energy Drinks Market by Distribution Channel

11.2.5.3 USA Sports & Energy Drinks Market by End-user

11.2.6 Canada

11.2.6.1 Canada Sports & Energy Drinks Market by Type

11.2.6.2 Canada Sports & Energy Drinks Market by Distribution Channel

11.2.6.3 Canada Sports & Energy Drinks Market by End-user

11.2.7 Mexico

11.2.7.1 Mexico Sports & Energy Drinks Market by Type

11.2.7.2 Mexico Sports & Energy Drinks Market by Distribution Channel

11.2.7.3 Mexico Sports & Energy Drinks Market by End-user

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Eastern Europe Sports & Energy Drinks Market by Country

11.3.1.2 Eastern Europe Sports & Energy Drinks Market by Type

11.3.1.3 Eastern Europe Sports & Energy Drinks Market by Distribution Channel

11.3.1.4 Eastern Europe Sports & Energy Drinks Market by End-user

11.3.1.5 Poland

11.3.1.5.1 Poland Sports & Energy Drinks Market by Type

11.3.1.5.2 Poland Sports & Energy Drinks Market by Distribution Channel

11.3.1.5.3 Poland Sports & Energy Drinks Market by End-user

11.3.1.6 Romania

11.3.1.6.1 Romania Sports & Energy Drinks Market by Type

11.3.1.6.2 Romania Sports & Energy Drinks Market by Distribution Channel

11.3.1.6.4 Romania Sports & Energy Drinks Market by End-user

11.3.1.7 Turkey

11.3.1.7.1 Turkey Sports & Energy Drinks Market by Type

11.3.1.7.2 Turkey Sports & Energy Drinks Market by Distribution Channel

11.3.1.7.3 Turkey Sports & Energy Drinks Market by End-user

11.3.1.8 Rest of Eastern Europe

11.3.1.8.1 Rest of Eastern Europe Sports & Energy Drinks Market by Type

11.3.1.8.2 Rest of Eastern Europe Sports & Energy Drinks Market by Distribution Channel

11.3.1.8.3 Rest of Eastern Europe Sports & Energy Drinks Market by End-user

11.3.2 Western Europe

11.3.2.1 Western Europe Sports & Energy Drinks Market by Type

11.3.2.2 Western Europe Sports & Energy Drinks Market by Distribution Channel

11.3.2.3 Western Europe Sports & Energy Drinks Market by End-user

11.3.2.4 Germany

11.3.2.4.1 Germany Sports & Energy Drinks Market by Type

11.3.2.4.2 Germany Sports & Energy Drinks Market by Distribution Channel

11.3.2.4.3 Germany Sports & Energy Drinks Market by End-user

11.3.2.5 France

11.3.2.5.1 France Sports & Energy Drinks Market by Type

11.3.2.5.2 France Sports & Energy Drinks Market by Distribution Channel

11.3.2.5.3 France Sports & Energy Drinks Market by End-user

11.3.2.6 UK

11.3.2.6.1 UK Sports & Energy Drinks Market by Type

11.3.2.6.2 UK Sports & Energy Drinks Market by Distribution Channel

11.3.2.6.3 UK Sports & Energy Drinks Market by End-user

11.3.2.7 Italy

11.3.2.7.1 Italy Sports & Energy Drinks Market by Type

11.3.2.7.2 Italy Sports & Energy Drinks Market by Distribution Channel

11.3.2.7.3 Italy Sports & Energy Drinks Market by End-user

11.3.2.8 Spain

11.3.2.8.1 Spain Sports & Energy Drinks Market by Type

11.3.2.8.2 Spain Sports & Energy Drinks Market by Distribution Channel

11.3.2.8.3 Spain Sports & Energy Drinks Market by End-user

11.3.2.9 Netherlands

11.3.2.9.1 Netherlands Sports & Energy Drinks Market by Type

11.3.2.9.2 Netherlands Sports & Energy Drinks Market by Distribution Channel

11.3.2.9.3 Netherlands Sports & Energy Drinks Market by End-user

11.3.2.10 Switzerland

11.3.2.10.1 Switzerland Sports & Energy Drinks Market by Type

11.3.2.10.2 Switzerland Sports & Energy Drinks Market by Distribution Channel

11.3.2.10.3 Switzerland Sports & Energy Drinks Market by End-user

11.3.2.11.1 Austria

11.3.2.11.2 Austria Sports & Energy Drinks Market by Type

11.3.2.11.3 Austria Sports & Energy Drinks Market by Distribution Channel

11.3.2.11.4 Austria Sports & Energy Drinks Market by End-user

11.3.2.12 Rest of Western Europe

11.3.2.12.1 Rest of Western Europe Sports & Energy Drinks Market by Type

11.3.2.12.2 Rest of Western Europe Sports & Energy Drinks Market by Distribution Channel

11.3.2.12.3 Rest of Western Europe Sports & Energy Drinks Market by End-user

11.4 Asia-Pacific

11.4.1 Asia-Pacific Sports & Energy Drinks Market by Country

11.4.2 Asia-Pacific Sports & Energy Drinks Market by Type

11.4.3 Asia-Pacific Sports & Energy Drinks Market by Distribution Channel

11.4.4 Asia-Pacific Sports & Energy Drinks Market by End-user

11.4.5 China

11.4.5.1 China Sports & Energy Drinks Market by Type

11.4.5.2 China Sports & Energy Drinks Market by End-user

11.4.5.3 China Sports & Energy Drinks Market by Distribution Channel

11.4.6 India

11.4.6.1 India Sports & Energy Drinks Market by Type

11.4.6.2 India Sports & Energy Drinks Market by Distribution Channel

11.4.6.3 India Sports & Energy Drinks Market by End-user

11.4.7 Japan

11.4.7.1 Japan Sports & Energy Drinks Market by Type

11.4.7.2 Japan Sports & Energy Drinks Market by Distribution Channel

11.4.7.3 Japan Sports & Energy Drinks Market by End-user

11.4.8 South Korea

11.4.8.1 South Korea Sports & Energy Drinks Market by Type

11.4.8.2 South Korea Sports & Energy Drinks Market by Distribution Channel

11.4.8.3 South Korea Sports & Energy Drinks Market by End-user

11.4.9 Vietnam

11.4.9.1 Vietnam Sports & Energy Drinks Market by Type

11.4.9.2 Vietnam Sports & Energy Drinks Market by Distribution Channel

11.4.9.3 Vietnam Sports & Energy Drinks Market by End-user

11.4.10 Singapore

11.4.10.1 Singapore Sports & Energy Drinks Market by Type

11.4.10.2 Singapore Sports & Energy Drinks Market by Distribution Channel

11.4.10.3 Singapore Sports & Energy Drinks Market by End-user

11.4.11 Australia

11.4.11.1 Australia Sports & Energy Drinks Market by Type

11.4.11.2 Australia Sports & Energy Drinks Market by Distribution Channel

11.4.11.3 Australia Sports & Energy Drinks Market by End-user

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Sports & Energy Drinks Market by Type

11.4.12.2 Rest of Asia-Pacific Sports & Energy Drinks Market by Distribution Channel

11.4.12.3 Rest of Asia-Pacific Sports & Energy Drinks Market by End-user

11.5 Middle East & Africa

11.5.1 Middle East

11.5.1.1 Middle East Sports & Energy Drinks Market by Country

11.5.1.2 Middle East Sports & Energy Drinks Market by Type

11.5.1.3 Middle East Sports & Energy Drinks Market by Distribution Channel

11.5.1.4 Middle East Sports & Energy Drinks Market by End-user

11.5.1.5 UAE

11.5.1.5.1 UAE Sports & Energy Drinks Market by Type

11.5.1.5.2 UAE Sports & Energy Drinks Market by Distribution Channel

11.5.1.5.3 UAE Sports & Energy Drinks Market by End-user

11.5.1.6 Egypt

11.5.1.6.1 Egypt Sports & Energy Drinks Market by Type

11.5.1.6.2 Egypt Sports & Energy Drinks Market by Distribution Channel

11.5.1.6.3 Egypt Sports & Energy Drinks Market by End-user

11.5.1.7 Saudi Arabia

11.5.1.7.1 Saudi Arabia Sports & Energy Drinks Market by Type

11.5.1.7.2 Saudi Arabia Sports & Energy Drinks Market by Distribution Channel

11.5.1.7.3 Saudi Arabia Sports & Energy Drinks Market by End-user

11.5.1.8 Qatar

11.5.1.8.1 Qatar Sports & Energy Drinks Market by Type

11.5.1.8.2 Qatar Sports & Energy Drinks Market by Distribution Channel

11.5.1.8.3 Qatar Sports & Energy Drinks Market by End-user

11.5.1.9 Rest of Middle East

11.5.1.9.1 Rest of Middle East Sports & Energy Drinks Market by Type

11.5.1.9.2 Rest of Middle East Sports & Energy Drinks Market by Distribution Channel

11.5.1.9.3 Rest of Middle East Sports & Energy Drinks Market by End-user

11.5.2 Africa

11.5.2.1 Africa Transfusion Diagnostics Market by Country

11.5.2.2 Africa Sports & Energy Drinks Market by Type

11.5.2.3 Africa Sports & Energy Drinks Market by Distribution Channel

11.5.2.4 Africa Sports & Energy Drinks Market by End-user

11.5.2.5 Nigeria

11.5.2.5.1 Nigeria Sports & Energy Drinks Market by Type

11.5.2.5.2 Nigeria Sports & Energy Drinks Market by Distribution Channel

11.5.2.5.3 Nigeria Sports & Energy Drinks Market by End-user

11.5.2.6 South Africa

11.5.2.6.1 South Africa Sports & Energy Drinks Market by Type

11.5.2.6.2 South Africa Sports & Energy Drinks Market by Distribution Channel

11.5.2.6.3 South Africa Sports & Energy Drinks Market by End-user

11.5.2.7 Rest of Africa

11.5.2.7.1 Rest of Africa Sports & Energy Drinks Market by Type

11.5.2.7.2 Rest of Africa Sports & Energy Drinks Market by Distribution Channel

11.5.2.7.3 Rest of Africa Sports & Energy Drinks Market by End-user

11.6 Latin America

11.6.1 Latin America Sports & Energy Drinks Market by Country

11.6.2 Latin America Sports & Energy Drinks Market by Type

11.6.3 Latin America Sports & Energy Drinks Market by Distribution Channel

11.6.4 Latin America Sports & Energy Drinks Market by End-user

11.6.5 Brazil

11.6.5.1 Brazil Sports & Energy Drinks Market by Type

11.6.5.2 Brazil Sports & Energy Drinks Market by Distribution Channel

11.6.5.3 Brazil Sports & Energy Drinks Market by End-user

11.6.6 Argentina

11.6.6.1 Argentina Sports & Energy Drinks Market by Type

11.6.6.2 Argentina Sports & Energy Drinks Market by Distribution Channel

11.6.6.3 Argentina Sports & Energy Drinks Market by End-user

11.6.7 Colombia

11.6.7.1 Colombia Sports & Energy Drinks Market by Type

11.6.7.2 Colombia Sports & Energy Drinks Market by Distribution Channel

11.6.7.3 Colombia Sports & Energy Drinks Market by End-user

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Sports & Energy Drinks Market by Type

11.6.8.2 Rest of Latin America Sports & Energy Drinks Market by Distribution Channel

11.6.8.3 Rest of Latin America Sports & Energy Drinks Market by End-user

12. Company profile

12.1 AJE Group

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Abbott Nutrition Co

12.2.1 Company Overview

12.2.2 Financials

12.2.3 Product/Services Offered

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 BA sports nutrition LL

12.3.1 Company Overview

12.3.2 Financials

12.3.3 Product/Services Offered

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 The Coca-Cola Company

12.4.1 Company Overview

12.4.2 Financials

12.4.3 Product/Services Offered

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 PepsiCo Inc.

12.5.1 Company Overview

12.5.2 Financials

12.5.3 Product/Services Offered

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Herbalife And Energy Drinks, Inc.

12.6.1 Company Overview

12.6.2 Financials

12.6.3 Product/Services Offered

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 Monster Beverage Corporation

12.7.1 Company Overview

12.7.2 Financials

12.7.3 Product/Services Offered

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 Red Bull GmbH

12.8.1 Company Overview

12.8.2 Financials

12.8.3 Product/Services Offered

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 True and Energy Drinks

12.9.1 Company Overview

12.9.2 Financials

12.9.3 Product/Services Offered

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Glanbia plc

12.10.1 Company Overview

12.10.2 Financials

12.10.3 Product/Services Offered

12.10.4 SWOT Analysis

12.10.5 The SNS View

12.11 Now Health Group, Inc

12.11.1 Company Overview

12.11.2 Financials

12.11.3 Product/Services Offered

12.11.4 SWOT Analysis

12.11.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Collagen Supplements Market Report Scope & Overview: The Collagen Supplements Market Size was est

Squash Drinks Market Size was valued at USD 1.08 billion in 2022, and expected to reach USD 1.79 billion by 2030, and grow at a CAGR of 5.6 % over the forecast period 2023-2030.

Vegan Chocolate Confectionery Market Report Scope & Overview: Vegan Chocolate Confectionery Market

Sourdough Market Size was esteemed at USD 2.80 billion out of 2022 and is supposed to arrive at USD 6.11 billion by 2030, and develop at a CAGR of 10.25% over the forecast period 2023-2030.

The Sports & Energy Drinks Market size was valued at USD 116.77 billion in 2023 and is expected to reach USD 298.70 billion by 2032 and grow at a CAGR of 11% over the forecast period of 2024-2032.

Convenience Stores Market Report Scope & Overview: Convenience Stores Market Siz

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd