Get More Information on Spine Biologics Market - Request Sample Report

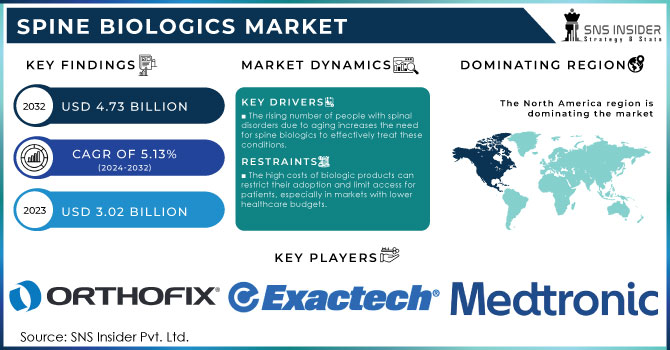

The Spine Biologics Market size was estimated at USD 3.02 billion in 2023 and is expected to reach USD 4.73 billion by 2032 at a CAGR of 5.13% during the forecast period of 2024-2032.

The factors driving the spine biologics market include personalized medicine that is tailored according to the patient’s genetics. The increasing focus on improving quality of life drives demand for minimally invasive and effective therapies. Regenerative medicine, including stem cell therapy, holds promise for innovative treatments. Government initiatives and public-private partnerships are fostering research and development, while emerging markets with growing healthcare needs offer new growth opportunities. These factors collectively contribute to the expansion of the spine biologics market. The market is increasing due to the increase in the number of old individuals who need treatment or rather the diagnosis that is having problems. The number of spine injuries among individuals who are over 50 is also in high demand because they are prone to have changes in their spine structure. They are also at an equal disadvantage in issues of their spinal and the changes. The market will therefore increase due to the above reasons that take place in the predicted period. The increase in rate of treatment in the world is also a major reason that is contributing to the increase in spine biologics market.

The spinal biologics are all the materials that can be used in case of the spine fusion surgery, spinal cord injury, and degenerative disk disease. The metals are inert materials, and therefore, they cannot stimulate the bone regeneration. According to the study published on ScienceDirect, April 2023, spinal degeneration is something that is common to human. In addition to the article, we obtain that the prevealence of the spinal degeneration is about 266 million populations (3.63 %) in 1 year across the globe.

The surgeons nowadays are dealing with advanced biological mechanisms in treating the deformities of spine, for instance, the direct lateral interbody fusion and the extreme lateral interbody fusion. According to the article published on Barrow Neurological Institute on May 2023, the extreme lateral interbody fusion is a type of a minimal invasive lumbar spinal fusion surgery where by the surgeon uses the abdomen to enter the back bone. There are several advantages of using XLIF, for instance, it has less surgery time, less blood loss, less hospital days, the surgery pain is little, and last but not least, it can be used in treating many types of the spinal disorder, for example, Lumbar spinal stenosis, mild scoliosis, and degenerative disk disease with instability.

MARKET DYNAMICS

DRIVERS

The rising number of people with spinal disorders due to aging increases the need for spine biologics to effectively treat these conditions.

Spinal disorders are becoming increasingly prevalent among the aging population, highly contributing to the demand for spine biologics. Aging is associated with degeneration of a person’s spinal structures as they age such as reduction in the bone density and elasticity of cartilages. Associated with the decrease in disc height, this causes a wide array of conditions such as osteoarthritis, spinal stenosis and degenerative disc diseases. Therefore, the need for biologics is instrumental as it offers solutions that address these degenerative biological processes and provide further therapeutic avenues. Aged persons with these spinal conditions undergo very severe and excruciating pains, limiting their physical movement and negatively affecting their life quality. They need to be treated with high technologies that can offer remedies for spinal degeneration occurring with age. They live abundantly in the world, which creates the necessity to have well-developed spine biologics. They include stem cell treatments, PRP, gene therapies among others. For instance, the use of stem cell therapy repairs worn out discs and aids in the regeneration of the spinal cells. PRP reduces inflammation in both the disc and other injuring areas accelerating the healing process.

The high rate of aging and the resultant increase the cases of spinal disorders, call for more innovative treatments in spine biologics. The aging generation is continuing to increase; thus, the cases of each of these complications will increase. Considering the current trends globally, therefore, we can deduce that the market for these biologics will keep increasing too notwithstanding the decline at twelve months rate in usage. Payloads. Hence, there is a call for more research and innovations in the same solutions to ensure all aging spinal disorders victims are given a chance to lead a normal life free from too much pain.

Technological advancements, including advanced bone grafts and stem cell therapies, are driving market growth by enhancing treatment options and patient outcomes.

The market growth in the spine biologics industry is significantly facilitated by technological advancements that expand the scope and the quality of treatments. In particular, the development of such interventions, as advanced bone grafts and, stem cell therapies have revolutionized the treatment of spinal problems. Advanced bone grafts include synthetic and bioengineered options that are more compatible and performative than the traditional ones. These grafts also allow bones to heal faster and stronger with shorter healing and recovery times. On the other hand, stem cell therapies provide a way to employ our own regenerative abilities to fix spinal problems from the inside. Consequently, such types of interventions as the culture-expanded mesenchymal bone marrow stem cells are utilized to treat spinal issues at the level of their roots. These developed forms of biologic products offer an alternative to treatments of the condition, providing lasting solutions rather than simply alleviating the symptoms.

Overall, these technologies offer both a more effective treatment for the patient and better outcomes. Moreover, by treating the conditions from the inside rather than attempting to fight the consequences, these interventions can help eliminate the causes of the problem more efficiently. Therefore, as the technologies keep developing and improving, the technologies will likewise experience growth. The technologies will keep expanding the demand for more effective solutions to spinal problems, and in so doing, they will promote greater quality of life for those affected.

RESTRAIN

The high costs of biologic products can restrict their adoption and limit access for patients, especially in markets with lower healthcare budgets.

The biologics such as advanced therapies like stem cell treatments and complex bone grafts should be more expensive than more traditional alternatives because they are typically harder to produce, requiring more sophisticated manufacturing processes and often specialized storage. In areas with limited healthcare resources, the high price of these treatments serves as an insurmountable economic barrier imposing limitations on the therapy’s availability. Thus, overall similar inequalities to those discussed previously, related to advanced surgeries and other interventions, result in the inability of healthcare systems to implement these advanced therapies as standard treatment options despite defenses about their objective feasibility. Consequently, given the context, handling the cost-related challenges of biologic products is a key to improving healthcare accessibility and ensuring that patients from different types of markets can benefit from the latest advancements in spinal care.

By Product

The spinal allografts segment dominated the market and accounted for 59.60% of the market revenue in 2023. This dominance can be attributed to the numerous benefits associated with the usage of allografts. The adoption of allografts over autografts is swiftly increasing owing to properties such as osteoconductivity and immediate structural support. In addition, allografts do not need another surgery to harvest the bone, which results in decreased surgery time and wound healing.

By End-use

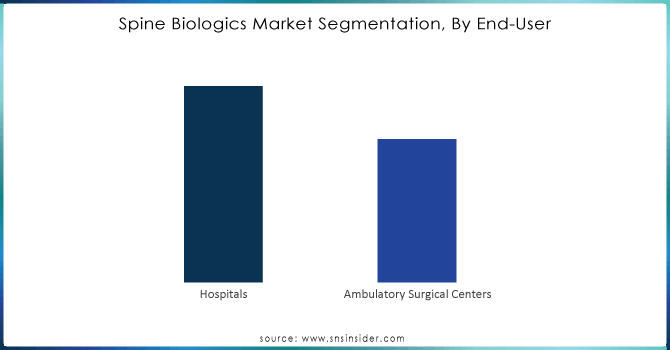

The hospital segment dominated the market and accounted for 62.4% of the market revenue in 2023. The segment is primarily driven by an increased number of spine fusion surgeries performed in these facilities. In addition, the availability of several hospitals like the George Washington University Hospital and Massachusetts General Hospital offering services for spinal surgeries is expected to boost the segment growth over the forecast period.

Need any customization research on Spine Biologics Market - Enquiry Now

REGIONAL ANALYSES

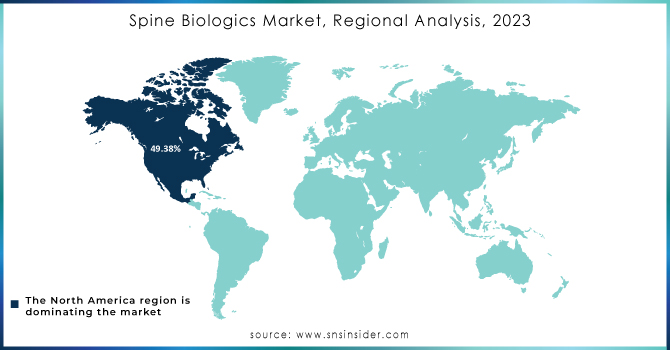

North America region dominated the market and accounted for a 49.38% share in 2023. The growth of the market can be attributed to the stable economic growth, increased adoption of minimally invasive surgeries, and rising prevalence of the spine disorders such as disc-related problems, spinal stenosis, and spondylolisthesis.

Asia Pacific region is expected to witness the fastest growth of the market due to the presence of the large patient pool and increasing awareness of biologics benefits among the patients and surgeons. The advancements in healthcare infrastructure in the Asia Pacific region, increased healthcare expenditure, and the rising number of the spine injuries, primarily due to the road accidents, are the aspects boosting the regional market.

The major players are Orthofix, DePuy Synthes (Johnson & Johnson), Exactech, Inc., Arthrex, Inc., Medtronic, Stryker, NuVasive, Inc., Organogenesis Inc., Kuros Biosciences, Zimmer Biomet, and others players

In October 2023: One of the leading providers of spine and orthopedics products, Orthofix Medical Inc., completed the full commercial launch and 510k clearance of an advanced bioactive synthetic graft, OsteoCove, for the use in orthopedic and spine procedures. This graft is available in strip and putty formats.

In July 2023: Cerapedics Inc., expanded its reservation at the Denver metro area. The agreement is expected to support the company’s other products offered on the market, with i-FACTOR bone grafts being among products for cervical spinal fusion.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.02 Billion |

| Market Size by 2032 | USD 4.73 Billion |

| CAGR | CAGR of 5.13% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Spinal Allografts, Bone Graft Substitutes, Cell-based Matrix) • By End-use (Hospitals, Outpatient Facilities) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Orthofix, DePuy Synthes (Johnson & Johnson), Exactech, Inc., Arthrex, Inc., Medtronic, Stryker, NuVasive, Inc., Organogenesis Inc., Kuros Biosciences, Zimmer Biomet |

| Key Drivers | • The rising number of people with spinal disorders due to aging increases the need for spine biologics to effectively treat these conditions. • Technological advancements, including advanced bone grafts and stem cell therapies, are driving market growth by enhancing treatment options and patient outcomes. |

| RESTRAINTS | • The high costs of biologic products can restrict their adoption and limit access for patients, especially in markets with lower healthcare budgets. |

Ans: The Spine Biologics Market is expected to grow at a CAGR of 5.13%.

Ans: Spine Biologics Market size was USD 3.02 Billion in 2023 and is expected to Reach USD 4.73 Billion by 2032.

Ans: Spinal Allografts segmentation is the dominating segment by Product in the Spine Biologics Market.

Ans: The rising number of people with spinal disorders due to aging increases the need for spine biologics to effectively treat these conditions.

Ans: North America is the dominating region in the Spine Biologics Market.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Prescription Trends, (2023), by Region

5.3 Drug Volume: Production and usage volumes of pharmaceuticals.

5.4 Healthcare Spending: Expenditure data by government, insurers, and out-of-pocket by patients

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Spine Biologics Market Segmentation, By Product

7.1 Chapter Overview

7.2 Spinal Allografts

7.2.1 Spinal Allografts Market Trends Analysis (2020-2032)

7.2.2 Spinal Allografts Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.1 Machined Bones Allograft

7.2.1.1 Machined Bones Allograft Market Trends Analysis (2020-2032)

7.2.1.2 Machined Bones Allograft Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.2 Demineralized Bone Matrix

7.2.2.1 Demineralized Bone Matrix Market Trends Analysis (2020-2032)

7.2.2.2 Demineralized Bone Matrix Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Bone Graft Substitutes

7.3.1 Bone Graft Substitutes Market Trends Analysis (2020-2032)

7.3.2 Bone Graft Substitutes Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.1 Bone Morphogenetic Proteins

7.3.1.1 Bone Morphogenetic Proteins Market Trends Analysis (2020-2032)

7.3.1.2 Bone Morphogenetic Proteins Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.2 Synthetic Bone Grafts

7.3.2.1 Synthetic Bone Grafts Market Trends Analysis (2020-2032)

7.3.2.2 Synthetic Bone Grafts Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Cell-base Matrix

7.4.1 Cell-base Matrix Market Trends Analysis (2020-2032)

7.4.2 Cell-base Matrix Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Spine Biologics Market Segmentation, By End-User

8.1 Chapter Overview

8.2 Hospitals

8.2.1 Hospitals Market Trends Analysis (2020-2032)

8.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Ambulatory Surgical Centers

8.3.1 Ambulatory Surgical Centers Market Trends Analysis (2020-2032)

8.3.2 Ambulatory Surgical Centers Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.2.4 North America Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.2.5.2 USA Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.2.6.2 Canada Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.2.7.2 Mexico Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.5.2 Poland Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.6.2 Romania Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.4 Western Europe Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.5.2 Germany Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.6.2 France Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.7.2 UK Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.8.2 Italy Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.9.2 Spain Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.12.2 Austria Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4 Asia-Pacific

9.4.1 Trends Analysis

9.4.2 Asia-Pacific Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia-Pacific Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.4 Asia-Pacific Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.5.2 China Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.5.2 India Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.5.2 Japan Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.6.2 South Korea Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.2.7.2 Vietnam Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.8.2 Singapore Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.9.2 Australia Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.4 Middle East Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.5.2 UAE Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.2.4 Africa Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Spine Biologics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.6.4 Latin America Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.6.5.2 Brazil Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.6.6.2 Argentina Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.6.7.2 Colombia Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Spine Biologics Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Spine Biologics Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10. Company Profiles

10.1 Orthofix

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 DePuy Synthes (Johnson & Johnson)

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Exactech, Inc.

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Arthrex, Inc.

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Medtronic

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Stryker

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 NuVasive, Inc.

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Organogenesis Inc.

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Kuros Biosciences

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Zimmer Biomet

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments

By Product

Spinal Allografts

Machined Bones Allograft

Demineralized Bone Matrix

Bone Graft Substitutes

Bone Morphogenetic Proteins

Synthetic Bone Grafts

Cell-base Matrix

By End-use

Hospitals

Ambulatory Surgical Centers

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Wearable Cardiac Devices Market size was USD 3.72 billion in 2023, projected to reach USD 25.71 billion by 2032, at a CAGR of 24.0% from 2024-2032.

The Legal Marijuana Market Size was valued at USD 26.0 billion in 2023 and is expected to reach USD 146.9 billion by 2032, growing at a CAGR of 21.2% over the forecast period 2024-2032.

Antiarrhythmic Drugs Market was valued at USD 1.02 billion in 2023 and is expected to reach USD 1.77 billion by 2032, growing at a CAGR of 6.30% from 2024-2032.

Ocular Drug Delivery Devices Market was valued at USD 13.03 billion in 2023, expected to reach USD 27.13 billion by 2032 at a CAGR of 8.54% from 2024-2032.

The Nicotine Replacement Therapy Market Size was valued at USD 2.83 Billion in 2023, and is expected to reach USD 4.27 Billion by 2032, and grow at a CAGR of 4.83%.

Hair Transplant Market was valued at USD 18.43 billion in 2023 and is expected to reach USD 110.06 billion by 2032, growing at a CAGR of 21.99% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd