Get more information on Smart Warehousing Market - Request Free Sample Report

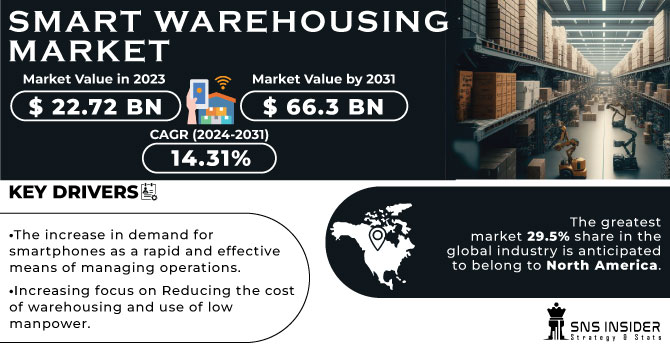

The Smart Warehousing Market Size was valued at USD 22.7 billion in 2023 and is expected to reach USD 75.7 billion by 2032 and grow at a CAGR of 14.3% over the forecast period 2024-2032.

The Smart Warehousing Market is experiencing significant growth, driven by various market dynamics that are reshaping logistics and supply chain management. Key factors include the increasing demand for automation, advancements in artificial intelligence (AI), and the necessity for real-time data analytics. Companies like Magaya and Advatix are investing heavily in smart technologies to enhance operational efficiency, reduce costs, and improve accuracy in inventory management. As organizations seek to streamline their supply chains and improve responsiveness to market demands, the implementation of smart warehousing solutions has become a pivotal strategy. This shift not only enhances productivity but also supports sustainable practices by optimizing resource utilization and reducing waste.

In recent developments, Larger KC made a strategic acquisition in April 2024 to expand its footprint by integrating a supply chain company to bolster its smart warehousing capabilities. This move underscores the ongoing trend of consolidation within the sector, as companies aim to enhance their operational capacities and expand their service offerings. Similarly, in September 2023, a new initiative focusing on building sensory-augmented smart warehouses was introduced by a consortium of innovators, aiming to incorporate advanced sensory technologies that improve inventory tracking and warehouse management. These innovations highlight the increasing integration of IoT devices, which enable enhanced connectivity and operational visibility.

Moreover, in May 2024, Advatix was recognized when its cloud-based suite was awarded as the top global innovation of the year for smart warehousing. This recognition reflects the industry's shift toward cloud technologies that facilitate scalable and flexible warehousing solutions. These platforms allow businesses to seamlessly manage their supply chains and adapt to changing market conditions, further driving the adoption of smart warehousing practices. Additionally, significant advancements in 5G technology were marked by the inauguration of Indonesia's first 5G smart warehouse and innovation center by Telkomsel and Huawei in March 2024. This facility aims to leverage high-speed connectivity to enhance operational efficiency and real-time data processing, crucial for the future of smart warehousing.

The landscape is further evolving with the introduction of AI-driven innovations in warehouse management, as seen in April 2024 with Magaya's AI-driven warehouse management solutions. By utilizing AI to automate processes and improve decision-making, companies are enhancing their ability to meet customer demands and optimize their supply chains. In March 2022, Cainiao launched an enterprise smart warehouse solution, showcasing the importance of tailored technologies designed to address specific operational challenges. These advancements indicate a robust trajectory for the smart warehousing market, characterized by continuous innovation and a growing emphasis on integrating cutting-edge technologies to enhance overall efficiency and responsiveness.

Drivers:

Growing Demand for Automation and Efficiency in Supply Chain Management Drives Smart Warehousing Market Growth

The increasing need for automation and operational efficiency in supply chain management is a significant driver for the Smart Warehousing Market. Companies are continually seeking ways to streamline operations, reduce labor costs, and minimize errors in inventory management. Automation technologies, such as robotic process automation (RPA) and advanced robotics, are transforming traditional warehousing operations by enhancing speed and accuracy. These solutions can perform repetitive tasks with greater precision than human workers, leading to reduced errors in order fulfillment and inventory tracking. Moreover, the integration of technologies like the Internet of Things (IoT) allows real-time monitoring of inventory levels and equipment performance, further optimizing warehouse operations. As businesses strive to meet the growing demands for quick delivery times and efficient inventory management, the adoption of smart warehousing solutions becomes imperative. This transition not only boosts productivity but also provides a competitive advantage in a market that increasingly prioritizes efficiency. Consequently, the demand for innovative warehousing technologies is expected to rise, propelling the growth of the Smart Warehousing Market.

Rising Integration of Advanced Technologies in Warehouse Operations Fuels Market Growth

The rapid integration of advanced technologies, including artificial intelligence (AI), machine learning, and data analytics, is significantly driving the growth of the Smart Warehousing Market. These technologies enable warehouses to optimize their operations, enhance decision-making processes, and improve overall efficiency. For instance, AI algorithms can analyze vast amounts of data to forecast demand patterns, enabling warehouses to adjust inventory levels proactively. Machine learning applications can also enhance routing and sorting processes, ensuring that products are picked and packed most efficiently. Furthermore, the utilization of data analytics allows companies to gain valuable insights into their operations, identifying bottlenecks and areas for improvement. As these technologies become more accessible and affordable, more businesses are adopting smart warehousing solutions to remain competitive in a rapidly evolving market. This technological shift not only reduces operational costs but also increases the agility of supply chains, allowing companies to respond swiftly to market changes. Consequently, the integration of advanced technologies is expected to play a crucial role in shaping the future of the Smart Warehousing Market.

Restraint:

High Initial Investment and Implementation Costs Restrain Smart Warehousing Market Growth

Despite the numerous advantages offered by smart warehousing solutions, high initial investment and implementation costs remain a significant restraint for market growth. The adoption of advanced technologies, such as automated systems, AI-driven analytics, and IoT devices, requires substantial financial outlay, which can deter smaller businesses or those with limited budgets from investing. Additionally, the costs associated with upgrading existing infrastructure to accommodate these new technologies can be prohibitive. Beyond financial constraints, the implementation phase often involves complex integration processes, necessitating specialized skills and training for staff. This can lead to temporary disruptions in operations during the transition period, further discouraging organizations from leaping smart warehousing. Consequently, many businesses may opt for incremental improvements rather than fully committing to a smart warehousing overhaul. As a result, while the long-term benefits of smart warehousing are clear, the upfront costs and challenges associated with implementation may hinder the pace of adoption in certain sectors, ultimately restraining market growth.

Opportunity:

Growing E-commerce Sector Presents Significant Opportunities for Smart Warehousing Market Expansion

The rapid growth of the e-commerce sector presents significant opportunities for the expansion of the Smart Warehousing Market. As online shopping continues to gain traction, businesses are increasingly looking for efficient ways to manage their inventory and fulfill orders quickly. Smart warehousing solutions offer the perfect answer to this challenge, enabling companies to automate various processes such as inventory tracking, order picking, and shipment scheduling. With the need for fast and accurate order fulfillment becoming paramount in the e-commerce landscape, the adoption of smart technologies is not just beneficial but essential for staying competitive. E-commerce giants are investing heavily in smart warehousing systems that allow for real-time visibility into inventory levels, enabling them to respond swiftly to changes in demand. Moreover, the ability to scale operations up or down depending on seasonal fluctuations further enhances the attractiveness of smart warehousing solutions for e-commerce businesses. As a result, the intersection of smart warehousing and the booming e-commerce sector creates a fertile ground for innovation and growth, positioning the Smart Warehousing Market for significant expansion in the coming years.

Challenge:

Supply Chain Disruptions and Changing Market Conditions Challenge Smart Warehousing Market Growth

Supply chain disruptions and rapidly changing market conditions pose a significant challenge to the growth of the Smart Warehousing Market. Events such as natural disasters, geopolitical tensions, and global pandemics can severely impact logistics and supply chain operations, leading to uncertainty and fluctuations in demand. Such disruptions can hinder the effectiveness of smart warehousing solutions, which rely on stable supply chain dynamics to operate optimally. Companies may find it challenging to implement smart warehousing strategies when faced with unpredictable supply chain conditions, leading to delays in technology adoption. Additionally, the rapid pace of market changes necessitates continuous adaptation and flexibility in warehouse operations, which can be difficult for businesses that have recently invested in smart technologies. These challenges can create a reluctance to invest in sophisticated systems if organizations are unsure about their return on investment under volatile conditions. As companies navigate these uncertainties, the challenge of maintaining operational efficiency while adapting to external pressures will be critical for the Smart Warehousing Market.

By Component

In 2023, the Solutions segment dominated the Smart Warehousing Market, accounting for a market share of approximately 45%. This dominance can be attributed to the increasing demand for comprehensive software solutions that streamline various warehouse operations, including inventory management, order fulfillment, and transportation logistics. For instance, companies are increasingly implementing warehouse management systems (WMS) that offer real-time data analytics and automation capabilities to enhance operational efficiency. Major players like Advatix have developed integrated solutions that not only optimize workflow but also provide advanced features such as predictive analytics and IoT integration. As businesses recognize the value of these solutions in achieving higher productivity and better customer service, the Solutions segment continues to grow significantly.

By Deployment Mode

In 2023, the Cloud deployment mode dominated the Smart Warehousing Market, capturing a market share of around 55%. The preference for cloud-based solutions is driven by their scalability, flexibility, and cost-effectiveness, which allow businesses to manage their warehousing operations without significant upfront investments in infrastructure. For example, companies like Magaya offer cloud-based warehouse management systems that enable real-time tracking and management of inventory, providing businesses with the agility needed to adapt to changing market demands. This deployment mode also supports remote access and collaboration, making it easier for teams to operate across multiple locations. As more organizations prioritize digital transformation, the Cloud segment is expected to maintain its leadership position in the market.

By Organization Size

In 2023, the Large Enterprises segment dominated the Smart Warehousing Market, holding a market share of approximately 60%. This predominance reflects the capability of larger organizations to invest in sophisticated smart warehousing technologies that enhance their supply chain efficiency. Large enterprises often face complex logistics challenges due to their scale and geographical reach, leading them to adopt advanced solutions such as automated guided vehicles (AGVs) and sophisticated inventory management systems. For example, major retailers and e-commerce giants have implemented smart warehousing practices to streamline their operations, enabling them to manage large volumes of inventory effectively and respond quickly to market changes. Consequently, the demand from large organizations continues to drive significant growth in this segment.

By Technology

In 2023, the IoT and Analytics technology segment dominated in the Smart Warehousing Market, accounting for a market share of about 40%. The integration of IoT devices enables warehouses to collect and analyze data in real-time, leading to improved decision-making and operational efficiency. For instance, companies are utilizing IoT sensors for tracking inventory levels and monitoring equipment performance, which allows for proactive maintenance and minimizes downtime. Additionally, analytics platforms provide valuable insights into inventory turnover rates and order fulfillment processes. Organizations like Cainiao have successfully leveraged IoT and analytics to optimize their warehouse operations, showcasing the transformative impact of these technologies on supply chain management.

By Application

In 2023, the Inventory Management application segment dominated the Smart Warehousing Market, representing a market share of around 35%. This dominance is largely due to the critical importance of efficient inventory management in reducing costs and enhancing customer satisfaction. Businesses increasingly rely on advanced inventory management systems to track stock levels in real-time, forecast demand, and manage reordering processes. For example, major retailers are implementing automated inventory management solutions that utilize barcode scanning and RFID technology to maintain accurate stock counts and streamline the replenishment process. The efficiency gains from these solutions have made inventory management a focal point for companies looking to enhance their warehousing capabilities.

By End-use Industry

In 2023, the Transportation and Logistics segment dominated the Smart Warehousing Market, holding a market share of approximately 30%. This sector's dominance can be attributed to the growing complexity of supply chains and the increasing demand for efficient logistics solutions. As companies in the transportation and logistics industry strive to optimize their operations, the adoption of smart warehousing technologies has become essential. For instance, logistics providers are implementing advanced warehouse management systems that facilitate real-time tracking of shipments and inventory, allowing for better coordination and reduced transit times. With the rise of e-commerce and the need for faster delivery services, the transportation and logistics segment continues to be a key driver of growth in the Smart Warehousing Market.

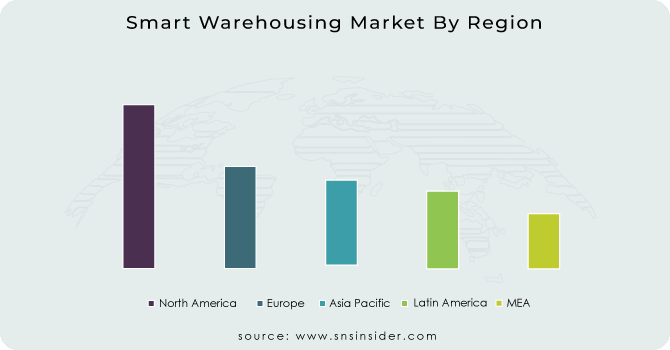

In 2023, North America dominated the Smart Warehousing Market, with a market share of around 40%. This leadership can be attributed to the rapid adoption of advanced technologies and automation solutions in the logistics and warehousing sectors. The presence of major technology companies and innovative startups in the region has also fueled market growth. For instance, companies such as Amazon and Walmart have heavily invested in smart warehousing technologies, implementing automated systems and data analytics to streamline their supply chain operations. The U.S. has seen significant advancements in warehouse robotics and IoT applications, enabling these organizations to optimize inventory management and enhance operational efficiency. Additionally, the focus on improving customer experience through faster delivery services has further driven the growth of smart warehousing solutions in North America.

Moreover, in 2023, the Asia-Pacific region emerged as the fastest-growing market for Smart Warehousing, with a CAGR of around 15% in the forecast period. The region's rapid economic growth, coupled with increasing urbanization and a booming e-commerce sector, has led to a rising demand for efficient warehousing solutions. Countries like China and India are investing heavily in technology to modernize their logistics infrastructures, which is crucial for supporting their expanding retail markets. For instance, Cainiao, the logistics arm of Alibaba, has launched initiatives to develop smart warehouses that leverage automation and big data analytics to improve inventory management and reduce delivery times. As more businesses in the Asia-Pacific region recognize the benefits of smart warehousing, the market is poised for substantial growth, driven by advancements in technology and changing consumer expectations.

Need any customization research on Smart Warehousing Market - Enquiry Now

October 2024: CelcomDigi partnered with ZTE to implement advanced solutions in smart manufacturing and smart warehousing. This collaboration aimed to enhance operational efficiency and support digital transformation across various sectors by leveraging cutting-edge technologies.

April 2024: Huawei played a significant role in the establishment of the UAE's first 5G smart warehouse. This initiative was part of a broader effort to revolutionize logistics and warehousing operations in the region, enabling faster data processing and improved connectivity for better inventory management and operational efficiency.

March 2024: Telkomsel and Huawei inaugurated Indonesia's first 5G smart warehouse and innovation center. This facility was designed to drive technological advancements in the logistics sector, showcasing the potential of 5G technology to enhance automation and streamline warehouse management processes.

3PL Central (3PL Warehouse Manager, 3PL Billing)

Blue Jay Solutions (Blue Jay WMS, Blue Jay Transportation Management)

Blue Yonder (Luminate Control Tower, Warehouse Management System)

EasyEcom (EasyEcom WMS, EasyEcom Multichannel Inventory Management)

Epicor (Epicor ERP, Epicor Advanced Warehouse Management)

Foysonis (Foysonis WMS, Foysonis Inventory Management)

Generix (Generix WMS, Generix Supply Chain Management)

IBM (IBM Sterling Supply Chain Insights, IBM Maximo)

Increff (Increff Warehouse Management System, Increff Inventory Management)

Infor (Infor CloudSuite WMS, Infor Supply Chain Management)

Korber (Korber Warehouse Management System, Korber Logistics Software)

Locus Robotics (Locus Solution, Locus Fleet Management)

Manhattan Associates (Manhattan WMS, Manhattan Active Omni)

Mantis (Mantis WMS, Mantis Inventory Management)

Microlistics (Microlistics WMS, Microlistics Inventory Control)

Oracle (Oracle Warehouse Management Cloud, Oracle SCM Cloud)

PSI Logistics (PSI Logistics Software, PSI WMS)

ShipHero (ShipHero WMS, ShipHero Fulfillment)

Softeon (Softeon WMS, Softeon Distributed Order Management)

Tecsys (Tecsys WMS, Tecsys Supply Chain Management)

| Report Attributes | Details |

| Market Size in 2023 | US$ 22.72 Billion |

| Market Size by 2031 | US$ 66.3 Billion |

| CAGR | CAGR of 14.31% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Solutions, Services) • By Deployment Mode (On-Premises, Cloud) • By Organization Size (Small and Medium Enterprises, Large Enterprises) • By Technology (IoT and Analytics, AI in Warehouse, Automated Guided Vehicles (AGV), RFID, Blockchain in Warehouse, Others) • By Application (Transport Management, Inventory Management, Order Management, Shipping Management, Others) • By Industry (Transportation and Logistics, Retail and E-commerce, Food and Beverages, Manufacturing, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Manhattan Associates, Infor, Korber, Synergy Logistics, Generix, 3PL Central, PSI Logistics, Tecsys, Oracle, SAP, PTC, Epicor, IBM, Microlistics, Vinculum, Locus Robotics, Softeon, Unicommerce, Mantis, WareIQ, Increff, ShipHero, Orderhive, Foysonis, EasyEcom, Blue Yonder, IAM Robotics, BlueJay Solutions |

| Key Drivers | • The increase in demand for smartphones as a rapid and effective means of managing operations • Increasing focus on Reducing the cost of warehousing and use of low manpower |

| Market Restraints | • There is high initial investment is required for smart warehousing. • In the disjointed supply chain and logistics sector, there are no consistent governance requirements. |

Ans: The Smart Warehousing Market size was valued at USD 22.72 billion in 2023.

Ans. The Smart Warehousing Market is to grow at a CAGR of 14.3% From 2024 to 2032.

Ans: There are three options available to purchase this report,

Features: A non-printable PDF to be accessed by just one user at a time

Features:

C: Excel Datasheet: USD 2,325

Ans. The forecast period of the Smart Warehousing Market is 2024-2032.

Ans: six segments are covered in the Smart Warehousing Market Report, By Component, By Deployment Mode, By Organization Size, By Technology, By Application, By Industry.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 Network Infrastructure Expansion, by Region

5.3 Cybersecurity Incidents, by Region (2020-2023)

5.4 Cloud Services Usage, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Smart Warehousing Market Segmentation, By Component

7.1 Chapter Overview

7.2 Hardware

7.2.1 Hardware Market Trends Analysis (2020-2032)

7.2.2 Hardware Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Solutions

7.3.1 Solutions Market Trends Analysis (2020-2032)

7.3.2 Solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Services

7.4.1 Services Market Trends Analysis (2020-2032)

7.4.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Smart Warehousing Market Segmentation, By Deployment Mode

8.1 Chapter Overview

8.2 On-Premises

8.2.1 On-Premises Market Trends Analysis (2020-2032)

8.2.2 On-Premises Market Size Estimates And Forecasts To 2032 (USD Billion)

8.3 Cloud

8.3.1 Cloud Motor Market Trends Analysis (2020-2032)

8.3.2 Cloud Motor Market Size Estimates And Forecasts To 2032 (USD Billion)

9. Smart Warehousing Market Segmentation, By Organization Size

9.1 Chapter Overview

9.2 Small and Medium Enterprises

9.2.1 Small and Medium Enterprises Market Trends Analysis (2020-2032)

9.2.2 Small and Medium Enterprises Market Size Estimates And Forecasts To 2032 (USD Billion)

9.3 Large Enterprises

9.3.1 Large Enterprises Market Trends Analysis (2020-2032)

9.3.2 Large Enterprises Market Size Estimates And Forecasts To 2032 (USD Billion)

10. Smart Warehousing Market Segmentation, By Technology

10.1 Chapter Overview

10.2 IoT and Analytics

10.2.1 IoT and Analytics Market Trends Analysis (2020-2032)

10.2.2 IoT and Analytics Market Size Estimates And Forecasts To 2032 (USD Billion)

10.3 AI in Warehouse

10.3.1 AI in Warehouse Market Trends Analysis (2020-2032)

10.3.2 AI in Warehouse Market Size Estimates And Forecasts To 2032 (USD Billion)

10.4 Automated Guided Vehicles (AGV)

10.4.1 Automated Guided Vehicles (AGV) Market Trends Analysis (2020-2032)

10.4.2 Automated Guided Vehicles (AGV) Market Size Estimates And Forecasts To 2032 (USD Billion)

10.5 RFID

10.5.1 RFID Market Trends Analysis (2020-2032)

10.5.2 RFID Market Size Estimates And Forecasts To 2032 (USD Billion)

10.6 Blockchain in Warehouse

10.6.1 Blockchain in Warehouse Market Trends Analysis (2020-2032)

10.6.2 Blockchain in Warehouse Market Size Estimates And Forecasts To 2032 (USD Billion)

10.7 Others

10.7.1 Others Market Trends Analysis (2020-2032)

10.7.2 Others Market Size Estimates And Forecasts To 2032 (USD Billion)

11. Smart Warehousing Market Segmentation, By Application

11.1 Chapter Overview

11.2 Transport Management

11.2.1 Transport Management Market Trends Analysis (2020-2032)

11.2.2 Transport Management Market Size Estimates And Forecasts To 2032 (USD Billion)

11.3 Inventory Management

11.3.1 Inventory Management Vehicles Market Trends Analysis (2020-2032)

11.3.2 Inventory Management Market Size Estimates And Forecasts To 2032 (USD Billion)

11.4 Order Management

11.4.1 Order Management Market Trends Analysis (2020-2032)

11.4.2 Order Management Market Size Estimates And Forecasts To 2032 (USD Billion)

11.5 Shipping Management

11.5.1 Shipping Management Market Trends Analysis (2020-2032)

11.5.2 Shipping Management Market Size Estimates And Forecasts To 2032 (USD Billion)

11.6 Others

11.6.1 Others Market Trends Analysis (2020-2032)

11.6.2 Others Market Size Estimates And Forecasts To 2032 (USD Billion)

12. Smart Warehousing Market Segmentation, By End-use Industry

12.1 Chapter Overview

12.2 Transportation and Logistics

12.2.1 Transportation and Logistics Market Trends Analysis (2020-2032)

12.2.2 Transportation and Logistics Market Size Estimates And Forecasts To 2032 (USD Billion)

12.3 Retail and E-commerce

12.3.1 Retail and E-commerce Market Trends Analysis (2020-2032)

12.3.2 Retail and E-commerce Market Size Estimates And Forecasts To 2032 (USD Billion)

12.3 Food and Beverages

12.3.1 Food and Beverages Market Trends Analysis (2020-2032)

12.3.2 Food and Beverages Market Size Estimates And Forecasts To 2032 (USD Billion)

12.3 Manufacturing

12.3.1 Manufacturing Market Trends Analysis (2020-2032)

12.3.2 Manufacturing Market Size Estimates And Forecasts To 2032 (USD Billion)

12.3 Healthcare

12.3.1 Healthcare Market Trends Analysis (2020-2032)

12.3.2 Healthcare Market Size Estimates And Forecasts To 2032 (USD Billion)

12.3 Others

12.3.1 Others Market Trends Analysis (2020-2032)

12.3.2 Others Market Size Estimates And Forecasts To 2032 (USD Billion)

13. Regional Analysis

13.1 Chapter Overview

13.2 North America

13.2.1 Trends Analysis

13.2.2 North America Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.2.3 North America Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.2.4 North America Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.2.5 North America Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.2.6 North America Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.2.7 North America Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.2.8 North America Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.2.9 USA

13.2.9.1 USA Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.2.9.2 USA Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.2.9.3 USA Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.2.9.4 USA Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.2.9.5 USA Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.2.9.6 USA Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.2.10 Canada

13.2.10.1 Canada Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.2.10.2 Canada Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.2.10.3 Canada Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.2.10.4 Canada Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.2.10.5 Canada Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.2.10.6 Canada Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.2.11 Mexico

13.2.11.1 Mexico Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.2.11.2 Mexico Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.2.11.3 Mexico Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.2.11.4 Mexico Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.2.11.5 Mexico Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.2.11.6 Mexico Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3 Europe

13.3.1 Eastern Europe

13.3.1.1 Trends Analysis

13.3.1.2 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.3.1.3 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.4 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.5 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.6 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.7 Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.8 Eastern Europe Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.1.9 Poland

13.3.1.9.1 Poland Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.9.2 Poland Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.9.3 Poland Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.9.4 Poland Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.9.5 Poland Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.9.6 Poland Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.1.10 Romania

13.3.1.10.1 Romania Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.10.2 Romania Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.10.3 Romania Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.10.4 Romania Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.10.5 Romania Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.10.6 Romania Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.1.11 Hungary

13.3.1.11.1 Hungary Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.11.2 Hungary Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.11.3 Hungary Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.11.4 Hungary Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.11.5 Hungary Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.11.6 Hungary Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.1.12 Turkey

13.3.1.12.1 Turkey Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.12.2 Turkey Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.12.3 Turkey Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.12.4 Turkey Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.12.5 Turkey Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.12.6 Turkey Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.1.13 Rest Of Eastern Europe

13.3.1.13.1 Rest Of Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.1.13.2 Rest Of Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.1.13.3 Rest Of Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.1.13.4 Rest Of Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.1.13.5 Rest Of Eastern Europe Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.1.13.6 Rest Of Eastern Europe Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2 Western Europe

13.3.2.1 Trends Analysis

13.3.2.2 Western Europe Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.3.2.3 Western Europe Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.4 Western Europe Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.5 Western Europe Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.6 Western Europe Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.7 Western Europe Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.8 Western Europe Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.9 Germany

13.3.2.9.1 Germany Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.9.2 Germany Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.9.3 Germany Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.9.4 Germany Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.9.5 Germany Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.9.6 Germany Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.10 France

13.3.2.10.1 France Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.10.2 France Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.10.3 France Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.10.4 France Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.10.5 France Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.10.6 France Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.11 UK

13.3.2.11.1 UK Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.11.2 UK Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.11.3 UK Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.11.4 UK Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.11.5 UK Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.11.6 UK Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.12 Italy

13.3.2.12.1 Italy Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.12.2 Italy Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.12.3 Italy Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.12.4 Italy Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.12.5 Italy Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.12.6 Italy Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.13 Spain

13.3.2.13.1 Spain Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.13.2 Spain Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.13.3 Spain Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.13.4 Spain Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.13.5 Spain Smart Warehousing Market Estimates and Forecasts, By Application (2020-2032) (USD -13824)

13.3.2.13.6 Spain Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.14 Netherlands

13.3.2.14.1 Netherlands Smart Warehousing Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.14.2 Netherlands Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.14.3 Netherlands Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.14.4 Netherlands Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.14.5 Netherlands Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.14.6 Netherlands Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.15 Switzerland

13.3.2.15.1 Switzerland Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.15.2 Switzerland Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.15.3 Switzerland Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.15.4 Switzerland Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.15.5 Switzerland Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.15.6 Switzerland Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.16 Austria

13.3.2.16.1 Austria Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.16.2 Austria Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.16.3 Austria Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.16.4 Austria Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.16.5 Austria Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.16.6 Austria Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.3.2.17 Rest Of Western Europe

13.3.2.17.1 Rest Of Western Europe Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.3.2.17.2 Rest Of Western Europe Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.3.2.17.3 Rest Of Western Europe Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.3.2.17.4 Rest Of Western Europe Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.3.2.17.5 Rest Of Western Europe Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.3.2.17.6 Rest Of Western Europe Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4 Asia Pacific

13.4.1 Trends Analysis

13.4.2 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.4.3 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.4 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.5 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.6 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.7 Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.8 Asia Pacific Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.9 China

13.4.9.1 China Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.9.2 China Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.9.3 China Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.9.4 China Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.9.5 China Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.9.6 China Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.10 India

13.4.10.1 India Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.10.2 India Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.10.3 India Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.10.4 India Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.10.5 India Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.10.6 India Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.11 Japan

13.4.11.1 Japan Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.11.2 Japan Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.11.3 Japan Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.11.4 Japan Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.11.5 Japan Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.11.6 Japan Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.12 South Korea

13.4.12.1 South Korea Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.12.2 South Korea Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.12.3 South Korea Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.12.4 South Korea Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.12.5 South Korea Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.12.6 South Korea Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.13 Vietnam

13.4.13.1 Vietnam Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.13.2 Vietnam Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.13.3 Vietnam Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.13.4 Vietnam Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.13.5 Vietnam Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.13.6 Vietnam Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.14 Singapore

13.4.14.1 Singapore Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.14.2 Singapore Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.14.3 Singapore Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.14.4 Singapore Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.14.5 Singapore Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.14.6 Singapore Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.15 Australia

13.4.15.1 Australia Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.15.2 Australia Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.15.3 Australia Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.15.4 Australia Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.15.5 Australia Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.15.6 Australia Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.4.16 Rest Of Asia Pacific

13.4.16.1 Rest Of Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.4.16.2 Rest Of Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.4.16.3 Rest Of Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.4.16.4 Rest Of Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.4.16.5 Rest Of Asia Pacific Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.4.16.6 Rest Of Asia Pacific Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5 Middle East And Africa

13.5.1 Middle East

13.5.1.1 Trends Analysis

13.5.1.2 Middle East Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.5.1.3 Middle East Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.4 Middle East Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.5 Middle East Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.6 Middle East Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.7 Middle East Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.8 Middle East Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.1.9 UAE

13.5.1.9.1 UAE Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.9.2 UAE Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.9.3 UAE Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.9.4 UAE Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.9.5 UAE Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.9.6 UAE Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.1.10 Egypt

13.5.1.10.1 Egypt Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.10.2 Egypt Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.10.3 Egypt Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.10.4 Egypt Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.10.5 Egypt Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.10.6 Egypt Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.1.11 Saudi Arabia

13.5.1.10.1 Saudi Arabia Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.11.2 Saudi Arabia Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.11.3 Saudi Arabia Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.11.4 Saudi Arabia Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.11.5 Saudi Arabia Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.11.6 Saudi Arabia Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.1.12 Qatar

13.5.1.12.1 Qatar Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.12.2 Qatar Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.12.3 Qatar Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.12.4 Qatar Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.12.5 Qatar Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.12.6 Qatar Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.1.13 Rest Of Middle East

13.5.1.13.1 Rest Of Middle East Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.1.13.2 Rest Of Middle East Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.1.13.3 Rest Of Middle East Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.1.13.4 Rest Of Middle East Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.1.13.5 Rest Of Middle East Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.1.13.6 Rest Of Middle East Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.2 Africa

13.5.2.1 Trends Analysis

13.5.2.2 Africa Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.5.2.3 Africa Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.2.4 Africa Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.2.5 Africa Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.2.6 Africa Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.2.7 Africa Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.2.8 Africa Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.2.9 South Africa

13.5.2.9.1 South Africa Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.2.9.2 South Africa Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.2.9.3 South Africa Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.2.9.4 South Africa Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.2.9.5 South Africa Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.2.9.6 South Africa Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.2.10 Nigeria

13.5.2.10.1 Nigeria Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.2.10.2 Nigeria Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.2.10.3 Nigeria Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.2.10.4 Nigeria Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.2.10.5 Nigeria Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.2.10.6 Nigeria Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.5.2.11 Rest Of Africa

13.5.2.11.1 Rest Of Africa Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.5.2.11.2 Rest Of Africa Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.5.2.11.3 Rest Of Africa Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.5.2.11.4 Rest Of Africa Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.5.2.11.5 Rest Of Africa Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.5.2.11.6 Rest Of Africa Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.6 Latin America

13.6.1 Trends Analysis

13.6.2 Latin America Smart Warehousing Market Estimates And Forecasts, By Country (2020-2032) (USD Billion)

13.6.3 Latin America Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.6.4 Latin America Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.6.5 Latin America Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.6.6 Latin America Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.6.7 Latin America Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.6.8 Latin America Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.6.9 Brazil

13.6.9.1 Brazil Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.6.9.2 Brazil Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.6.9.3 Brazil Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.6.9.4 Brazil Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.6.9.5 Brazil Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.6.9.6 Brazil Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.6.10 Argentina

13.6.10.1 Argentina Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.6.10.2 Argentina Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.6.10.3 Argentina Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.6.10.4 Argentina Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.6.10.5 Argentina Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.6.10.6 Argentina Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.6.11 Colombia

13.6.11.1 Colombia Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.6.11.2 Colombia Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.6.11.3 Colombia Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.6.11.4 Colombia Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.6.11.5 Colombia Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.6.11.6 Colombia Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

13.6.12 Rest of Latin America

13.6.12.1 Rest of Latin America Smart Warehousing Market Estimates And Forecasts, By Component (2020-2032) (USD Billion)

13.6.12.2 Rest of Latin America Smart Warehousing Market Estimates And Forecasts, By Deployment Mode (2020-2032) (USD Billion)

13.6.12.3 Rest of Latin America Smart Warehousing Market Estimates And Forecasts, By Organization Size (2020-2032) (USD Billion)

13.6.12.4 Rest of Latin America Smart Warehousing Market Estimates And Forecasts, By Technology (2020-2032) (USD Billion)

13.6.12.5 Rest of Latin America Smart Warehousing Market Estimates And Forecasts, By Application (2020-2032) (USD Billion)

13.6.12.6 Rest of Latin America Smart Warehousing Market Segmentation, By End-use Industry (2020-2032) (USD Billion)

14. Company Profile0s

14.1 Manhattan Associates

14.1.1Company Overview

14.1.2 Financial

14.1.3 Products/ Services Offered

14.1.4 SWOT Analysis

14.2 Infor

14.2.1 Company Overview

14.2.2 Financial

14.2.3 Products/ Services Offered

14.2.4 SWOT Analysis

14.3 Korber

14.3.1 Company Overview

14.3.2 Financial

14.3.3 Products/ Services Offered

14.3.4 SWOT Analysis

14.4 Synergy Logistics

14.4.1 Company Overview

14.4.2 Financial

14.4.3 Products/ Services Offered

14.4.4 SWOT Analysis

14.5 Generix

14.5.1 Company Overview

14.5.2 Financial

14.5.3 Products/ Services Offered

14.5.4 SWOT Analysis

14.6 3PL Central

14.6.1 Company Overview

14.6.2 Financial

14.6.3 Products/ Services Offered

14.6.4 SWOT Analysis

14.7 PSI Logistics

14.7.1 Company Overview

14.7.2 Financial

14.7.3 Products/ Services Offered

14.7.4 SWOT Analysis

14.8 Tecsys

14.8.1 Company Overview

14.8.2 Financial

14.8.3 Products/ Services Offered

14.8.4 SWOT Analysis

14.9 Oracle

14.9.1 Company Overview

14.9.2 Financial

14.9.3 Products/ Services Offered

14.9.4 SWOT Analysis

14.10 SAP

14.10.1 Company Overview

14.10.2 Financial

14.10.3 Products/ Services Offered

14.10.4 SWOT Analysis

15. Use Cases and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Component

Hardware

Solutions

Services

By Deployment Mode

On-Premises

Cloud

By Organization Size

Small and Medium Enterprises

Large Enterprises

By Technology

IoT and Analytics

AI in Warehouse

Automated Guided Vehicles (AGV)

RFID

Blockchain in Warehouse

Others

By Application

Transport Management

Inventory Management

Order Management

Shipping Management

Others

By End-use Industry

Transportation and Logistics

Retail and E-commerce

Food and Beverages

Manufacturing

Healthcare

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Content Services Platforms Market, valued at USD 61.9 Bn in 2023, is projected to reach USD 228.2 Bn by 2032, growing at a 15.61% CAGR from 2024 to 2032.

The Cybersecurity Market was valued at USD 195.1 billion in 2023 and is expected to reach USD 542.3 Billion by 2032, growing at a CAGR of 12.05% by 2032.

The Wireless Gas Detection Market size was valued at USD 3.02 Billion in 2023. It is estimated to hit USD 11.18 Billion by 2032 and grow at a CAGR of 15.71% over the forecast period of 2024-2032.

Social Gaming Market was valued at USD 29.48 billion in 2023 and is expected to reach USD 110.74 billion by 2032, growing at a CAGR of 15.90% from 2024-2032.

The Massive Open Online Course Market was valued at USD 23.2 billion in 2023 and is expected to reach USD 483.0 billion by 2032, growing at a CAGR of 40.14% from 2024-2032.

The Data Center Rack Market Size was valued at USD 4.46 Billion in 2023 and is expected to reach USD 9.17 Billion by 2032 and grow at a CAGR of 8.34% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd