Get more information on Smart Ticketing Market - Request Free Sample Report

Smart Ticketing Market was valued at USD 11.00 billion in 2023 and is expected to reach USD 37.57 billion by 2032, growing at a CAGR of 14.68% from 2024-2032.

The smart ticketing market is experiencing significant growth, fueled by the increasing pace of digitalization across industries. As more businesses adopt digital technologies, the demand for efficient, secure, and convenient ticketing solutions has surged, prompting a shift from traditional paper tickets to digital formats. More than 80% of respondents have used smartphones or smartwatches for contactless payments, showcasing the shift from traditional cards to mobile-first payment solutions. This transformation is driven by advancements in mobile technology and cloud-based platforms, which enable seamless, contactless access to events and services. Technologies such as Near Field Communication, QR codes, and biometric authentication further enhance this experience by improving both the speed and security of ticketing processes.

This growing demand for smart ticketing solutions is particularly evident across sectors like transportation, entertainment, sports, and tourism. In transportation, smart ticketing systems help reduce wait times, improve operational efficiency, and eliminate fraud, which is becoming increasingly important as mobility needs evolve. Similarly, in entertainment and sports, digital tickets not only streamline event access but also offer enhanced features, such as personalized experiences and better crowd management, which improve overall customer satisfaction. In 2024, Major League Soccer partnered with SeatGeek to enhance the fan ticketing experience, offering a mobile-first platform for purchasing, transferring, and reselling tickets across multiple platforms. As digitalization becomes more widespread, the adoption of contactless payment systems is accelerating, further supporting the transition to mobile and digital ticketing in these sectors.

The future of the smart ticketing market appears even more promising, with numerous opportunities for growth and innovation on the horizon. As urban areas continue to embrace smart infrastructure and IoT solutions, the integration of smart ticketing with other urban mobility platforms will create more interconnected, efficient experiences for users. Additionally, data analytics and personalized services will play a critical role in shaping customer engagement, enabling businesses to offer tailored solutions that drive new revenue streams. The rise of digital adoption in emerging markets further expands these opportunities, offering new areas for growth and innovation in the smart ticketing sector.

DRIVERS

As consumers increasingly embrace digital and mobile-first experiences, there is a growing demand for smart ticketing solutions. The convenience of electronic ticketing, accessible through smartphones, apps, and digital wallets, makes it more attractive for users who seek seamless, efficient access to services. This shift is driven by the widespread adoption of mobile technology, allowing individuals to manage tickets without the hassle of physical cards or paper tickets. Additionally, the ease of real-time updates, instant ticket purchasing, and the ability to store multiple tickets on a single device contribute to enhanced user satisfaction. As consumers prioritize convenience, speed, and digital integration in their daily lives, smart ticketing solutions are rapidly becoming the preferred choice in sectors like transportation, entertainment, and events.

Smart ticketing offers businesses and transportation operators significant cost reductions by eliminating the need for traditional ticketing systems, such as printing, distributing, and handling physical tickets. This shift lowers operational expenses related to ticket production, staff management, and maintenance of physical infrastructure. Additionally, digital ticketing systems streamline the ticket validation process, reducing queues and waiting times, and leading to improved customer satisfaction. The use of real-time data also enables operators to monitor and manage crowd flow, optimizing resources and preventing bottlenecks. With better crowd management and automated processes, smart ticketing solutions improve operational efficiency, reduce human error, and enhance scalability for growing demand. As operators seek cost-effective and streamlined solutions, the financial and logistical benefits of smart ticketing become a compelling reason for widespread adoption.

RESTRAINTS

The digital nature of smart ticketing systems creates significant concerns regarding data security and user privacy. As these systems handle sensitive personal information, such as payment details and travel preferences, they become potential targets for cyberattacks. Hackers and data breaches can compromise user data, leading to a loss of trust among consumers. This can undermine the confidence needed for the widespread adoption of smart ticketing solutions. Additionally, concerns around the storage, handling, and sharing of personal information can make consumers wary of transitioning from traditional ticketing methods to digital solutions. As a result, businesses must invest heavily in robust security measures and ensure compliance with privacy regulations to reassure users and protect their data, which can increase operational costs and slow down market growth.

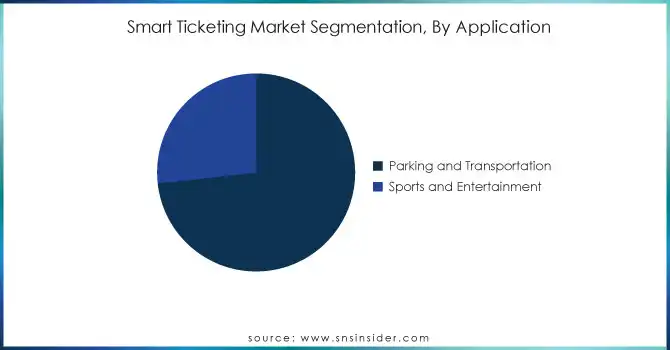

BY APPLICATION

The Parking and Transportation segment led the Smart Ticketing Market in 2023, holding around 73% of the revenue share. This dominance is driven by the increasing adoption of smart ticketing solutions for public transit and parking services. The ability to streamline payment processes, reduce operational costs, and enhance user experience has made digital ticketing a preferred choice for transportation operators and consumers alike. As urbanization and smart city initiatives grow, the demand for such solutions continues to rise.

The Sports and Entertainment segment is projected to grow at the fastest CAGR of about 16.68% from 2024 to 2032. This rapid growth is fueled by the rising demand for seamless, contactless ticketing experiences in events and sports venues. The shift towards mobile ticketing and digital solutions helps improve security, speed up entry processes, and offer personalized experiences. As sports organizations and entertainment venues embrace these technologies, the segment's growth is expected to accelerate.

BY OFFERING

The Smart Cards segment dominated the Smart Ticketing Market in 2023, accounting for approximately 37% of the revenue share. This dominance is driven by the widespread adoption of contactless smart cards in public transportation systems, where they offer ease of use, security, and cost efficiency. Smart cards provide a reliable, secure, and convenient way for users to access services, making them the preferred choice for commuters and transit operators alike. Their established presence and reliability continue to maintain their lead in the market.

The Ticket Validators segment is projected to grow at the fastest CAGR of about 17.03% from 2024 to 2032. This rapid growth is driven by the increasing need for advanced validation systems in various transport and event sectors. Ticket validators enable smooth, real-time ticket verification, reducing wait times and improving operational efficiency. As industries seek to enhance security and streamline entry processes, the demand for high-tech ticket validation solutions is expected to rise sharply, fueling the segment’s rapid expansion.

BY TECHNOLOGY

The Radio Frequency Identification segment led the Smart Ticketing Market in 2023, capturing approximately 34% of the revenue share. RFID technology has become the dominant choice for ticketing due to its ability to provide fast, contactless, and secure transactions. Widely used in transportation systems, RFID tags enable seamless entry and exit, reducing wait times and enhancing the overall user experience. Its established infrastructure and high reliability across various industries continue to drive its market dominance.

The Near Field Communication segment is expected to grow at the fastest CAGR of about 16.44% from 2024 to 2032. Near Field Communication technology allows for faster and more secure ticketing through mobile devices, providing a seamless, contactless experience for users. With the increasing popularity of smartphones and mobile wallets, NFC's ability to facilitate instant ticket purchases and access is gaining momentum. As consumers demand more convenient and secure payment solutions, Near Field Communication’s rapid adoption is poised to drive significant growth in the coming years.

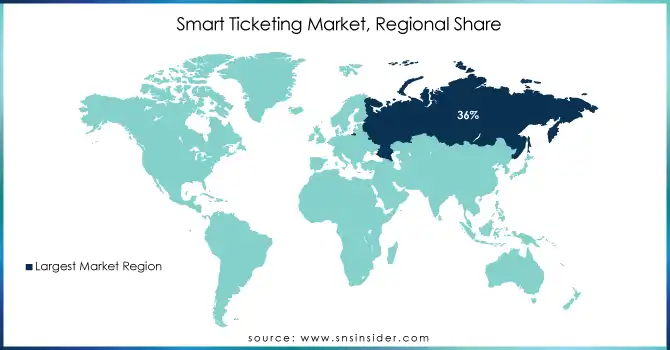

Regional Analysis

Europe dominated the Smart Ticketing Market in 2023, holding approximately 36% of the revenue share. This is primarily due to the region's advanced infrastructure and early adoption of digital ticketing solutions, particularly in public transportation. European cities have invested heavily in smart city initiatives, integrating seamless and contactless ticketing systems that cater to the increasing demand for efficiency and convenience. The established market maturity and technological integration in countries like the UK, Germany, and France continue to solidify Europe's leadership in the sector.

Asia Pacific is projected to grow at the fastest CAGR of about 17.57% from 2024 to 2032. The rapid urbanization, technological advancements, and rising smartphone penetration in countries like China, India, and Japan are key drivers of this growth. With increasing investments in smart transportation infrastructure and growing demand for efficient, digital solutions, the region is witnessing a strong push toward smart ticketing adoption. As Asia Pacific cities continue to modernize and digitize their transit systems, the market for smart ticketing solutions is expected to expand rapidly.

Need any customization research on Smart Ticketing Market - Enquiry Now

Conduent, Inc. (Mobile Ticketing Solutions, Fare Collection Systems)

Siemens (Ticket Vending Machines, Smart Ticketing Solutions)

Cammax Ltd (Ticketing Kiosks, Mobile Payment Solutions)

Infineon Technologies AG (Smart Cards, Contactless Payment Solutions)

HID Global Corporation (Smart Cards, Mobile Access Solutions)

Hitachi Rail Limited (Ticket Validation Systems, Fare Collection Solutions)

Masabi Ltd (Mobile Ticketing, Fare Collection Systems)

NXP Semiconductors (Contactless Payment Cards, Smart Ticketing Chips)

Giesecke+Devrient GmbH (Smart Cards, Secure Ticketing Solutions)

Cubic Corporation (Ticket Vending Machines, Smart Fare Collection Solutions)

Confidex Ltd. (Smart Ticketing Tags, Contactless Cards)

ASK (Smart Cards, Ticketing Solutions)

Gemalto NV (Smart Cards, Mobile Ticketing Solutions)

Xerox Corporation (Ticket Vending Machines, Ticketing Software)

Inside Secure (Contactless Payment Cards, Smart Ticketing Solutions)

Smart Card IT Solutions (Smart Ticketing Software, Fare Collection Systems)

Paragon ID (Smart Cards, Ticketing Solutions)

CGI Group (Ticketing Systems, Smart City Solutions)

Indra Sistemas (Smart Ticketing Systems, Fare Collection Solutions)

Scheidt & Bachmann (Ticketing Systems, Smart Fare Collection)

ACT (Smart Card Readers, Ticketing Solutions)

Atsuke (Mobile Ticketing Solutions, Fare Collection Systems)

Corethree (Mobile Ticketing Solutions, Fare Collection Systems)

Flowbird Group (Mobile Ticketing, Fare Collection Systems)

In 2024, Conduent Transportation was selected to upgrade the public transport network in Saint-Étienne Métropole, France. The project will introduce a contactless open payment system, enabling payments through EMV cards and NFC-enabled digital wallets like Apple Pay, Google Pay, and Samsung Pay.

In September 2024, Transport for Wales selected Hitachi as its 'Mobility as a Service' partner to digitally transform public transport across Wales

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 11.00 Billion |

| Market Size by 2032 | USD 37.57 Billion |

| CAGR | CAGR of 14.68% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Near Field Communication (NFC), Radio Frequency Identification (RFID), Quick Response Code (QR Code), Others (Cellular Networks)) • By Offering (Smart Cards, Ticket Validators, Ticketing Machine/Smart Ticketing Kiosk, E-toll, Others (wearables)) • By Application (Parking and Transportation, Sports and Entertainment) • By Component (Hardware, Software, Service) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Conduent, Inc., Siemens, Cammax Ltd, Infineon Technologies AG, HID Global Corporation, Hitachi Rail Limited, Masabi Ltd, NXP Semiconductors, Giesecke+Devrient GmbH, Cubic Corporation, Confidex Ltd., ASK, Gemalto NV, Xerox Corporation, Inside Secure, Smart Card IT Solutions, Paragon ID, CGI Group, Indra Sistemas, Scheidt & Bachmann, ACT, Atsuke, Corethree, Flowbird Group |

| Key Drivers | • Growing Consumer Preference for Digital and Mobile Ticketing Solutions • Significant Cost Savings and Enhanced Operational Efficiency for Operators |

| RESTRAINTS | • Significant Cost Savings and Enhanced Operational Efficiency for Operators |

Ans: Smart Ticketing Market was valued at USD 11.00 billion in 2023 and is expected to reach USD 37.57 billion by 2032, growing at a CAGR of 14.68% from 2024-2032.

Ans: Asia Pacific is projected to grow at a CAGR of about 17.57%.

Ans: Europe dominated the market with approximately 36% of the revenue share.

Ans: The Near Field Communication (NFC) segment is projected to grow at a CAGR of about 16.44%.

Ans: The Smart Cards segment accounted for approximately 37% of the revenue share.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 User Demographics, 2023

5.3 Integration Capabilities, by Software, 2023

5.4 Payment Method Preferences

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Smart Ticketing Market Segmentation, by Technology

7.1 Chapter Overview

7.2 Near Field Communication (NFC)

7.2.1 Near Field Communication (NFC) Market Trends Analysis (2020-2032)

7.2.2 Near Field Communication (NFC) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Radio Frequency Identification (RFID)

7.3.1 Radio Frequency Identification (RFID) Market Trends Analysis (2020-2032)

7.3.2 Radio Frequency Identification (RFID) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Quick Response Code (QR Code)

7.4.1 Quick Response Code (QR Code) Market Trends Analysis (2020-2032)

7.4.2 Quick Response Code (QR Code) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Others (Cellular Networks)

7.5.1 Others (Cellular Networks) Market Trends Analysis (2020-2032)

7.5.2 Others (Cellular Networks) Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Smart Ticketing Market Segmentation, by Application

8.1 Chapter Overview

8.2 Parking and Transportation

8.2.1 Parking and Transportation Market Trends Analysis (2020-2032)

8.2.2 Parking and Transportation Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Sports and Entertainment

8.3.1 Sports and Entertainment Market Trends Analysis (2020-2032)

8.3.2 Sports and Entertainment Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Smart Ticketing Market Segmentation, by Offering

9.1 Chapter Overview

9.2 Smart Cards

9.2.1 Smart Cards Market Trends Analysis (2020-2032)

9.2.2 Smart Cards Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Ticket Validators

9.3.1 Ticket Validators Market Trends Analysis (2020-2032)

9.3.2 Ticket Validators Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Ticketing Machine/Smart Ticketing Kiosk

9.4.1 Ticketing Machine/Smart Ticketing Kiosk Market Trends Analysis (2020-2032)

9.4.2 Ticketing Machine/Smart Ticketing Kiosk Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 E-toll

9.5.1 E-toll Market Trends Analysis (2020-2032)

9.5.2 E-toll Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Others (wearables)

9.6.1 Others (wearables) Market Trends Analysis (2020-2032)

9.6.2 Others (wearables) Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Smart Ticketing Market Segmentation, by Component

10.1 Chapter Overview

10.2 Hardware

10.2.1 Hardware Market Trends Analysis (2020-2032)

10.2.2 Hardware Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Software

10.3.1 Software Market Trends Analysis (2020-2032)

10.3.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Service

10.4.1 Service Market Trends Analysis (2020-2032)

10.4.2 Service Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.4 North America Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.5 North America Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.2.6 North America Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.7.2 USA Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.7.3 USA Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.2.7.4 USA Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.8.2 Canada Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.8.3 Canada Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.2.8.4 Canada Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.9.2 Mexico Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.9.3 Mexico Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.2.9.4 Mexico Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.7.2 Poland Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.7.3 Poland Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.7.4 Poland Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.8.2 Romania Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.8.3 Romania Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.8.4 Romania Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.4 Western Europe Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.5 Western Europe Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.6 Western Europe Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.7.2 Germany Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.7.3 Germany Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.7.4 Germany Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.8.2 France Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.8.3 France Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.8.4 France Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.9.2 UK Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.9.3 UK Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.9.4 UK Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.10.2 Italy Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.10.3 Italy Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.10.4 Italy Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.11.2 Spain Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.11.3 Spain Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.11.4 Spain Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.14.2 Austria Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.14.3 Austria Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.14.4 Austria Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.4 Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.5 Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.6 Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.7.2 China Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.7.3 China Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.7.4 China Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.8.2 India Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.8.3 India Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.8.4 India Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.9.2 Japan Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.9.3 Japan Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.9.4 Japan Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.10.2 South Korea Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.10.3 South Korea Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.10.4 South Korea Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.11.2 Vietnam Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.11.3 Vietnam Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.11.4 Vietnam Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.12.2 Singapore Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.12.3 Singapore Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.12.4 Singapore Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.13.2 Australia Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.13.3 Australia Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.13.4 Australia Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.4 Middle East Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.5 Middle East Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.6 Middle East Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.7.2 UAE Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.7.3 UAE Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.7.4 UAE Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.4 Africa Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.5 Africa Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.2.6 Africa Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Smart Ticketing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.4 Latin America Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.5 Latin America Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.6.6 Latin America Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.7.2 Brazil Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.7.3 Brazil Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.6.7.4 Brazil Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.8.2 Argentina Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.8.3 Argentina Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.6.8.4 Argentina Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.9.2 Colombia Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.9.3 Colombia Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.6.9.4 Colombia Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Smart Ticketing Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Smart Ticketing Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Smart Ticketing Market Estimates and Forecasts, by Offering (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Smart Ticketing Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

12. Company Profiles

12.1 Conduent, Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Siemens

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Cammax Ltd

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Infineon Technologies AG

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 HID Global Corporation

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Hitachi Rail Limited

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Masabi Ltd

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 NXP Semiconductors

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Giesecke+Devrient GmbH

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Cubic Corporation

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Technology

Near Field Communication (NFC)

Radio Frequency Identification (RFID)

Quick Response Code (QR Code)

Others (Cellular Networks)

By Offering

Smart Cards

Ticket Validators

Ticketing Machine/Smart Ticketing Kiosk

E-toll

Others (wearables)

By Application

Parking and Transportation

Sports and Entertainment

By Component

Hardware

Software

Service

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Cloud Compliance Market Size, valued at USD 31.20 Bn in 2023, is projected to reach USD 115.98 Bn by 2032, growing at CAGR of 16.63% during the forecast period.

Data Storage Converter Market was valued at USD 2.1 billion in 2023 and is expected to reach USD 4.98 billion by 2032, growing at a CAGR of 10.11% from 2024-2032

The Asset Management Market Size was valued at USD 484.74 Billion in 2023 and will reach USD 7287.15 Billion by 2032 and grow at a CAGR of 35.2% by 2032.

Construction Estimating Software Market was valued at USD 1.76 billion in 2023 and will reach USD 4.72 billion by 2032, growing at a CAGR of 11.61% by 2032.

The MEP Software Market was valued at USD 3.80 billion in 2023 and is expected to reach USD 9.20 Billion by 2032, growing at a CAGR of 10.34% by 2032.

The Connected Toys Market Size was valued at USD 9.67 Billion in 2023, and is expected to reach USD 53.37 Billion by 2032, and grow at a CAGR of 20.09% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd