Small Language Model Market Report Scope & Overview:

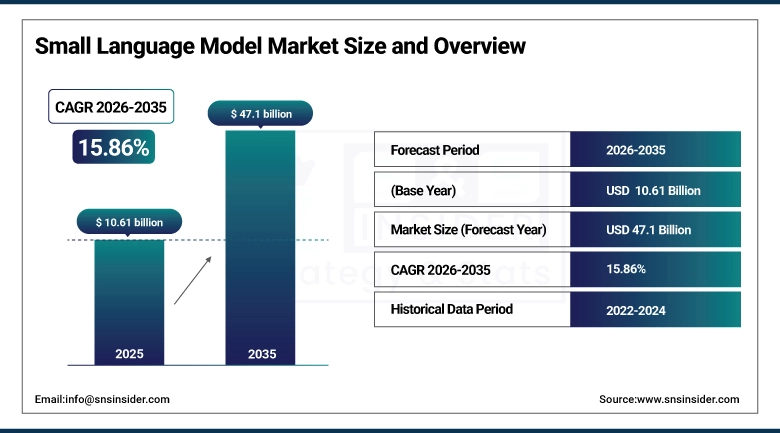

The Small Language Model Market was valued at USD 10.61 billion in 2025 and is expected to reach USD 47.1 billion by 2035, growing at a CAGR of 15.86% from 2026-2035.

The discourse around AI language models has been dominated by scale the race to build models with more parameters, more training data, and more computational infrastructure. The commercial realities of enterprise AI deployment are producing a counterweight to that trend. Large language models whose API costs run to cents per thousand tokens, whose inference latency is incompatible with real-time applications, whose general-purpose design means they know a lot about everything but not enough about any specific business's proprietary data, and whose cloud dependency creates data privacy concerns for regulated industries are not always the right tool for the job. Small language models trained on task-specific domains, fine-tunable on proprietary datasets with modest compute budgets, deployable on edge hardware, and capable of running inference on a laptop or smartphone without cloud connectivity address these constraints directly. Microsoft's Phi-2, Google's Gemma-2B, Apple's OpenELM, and Meta's Llama 3.1-8B each demonstrate that models in the 1-8 billion parameter range can match or exceed GPT-4-class performance on domain-specific tasks when appropriately trained a finding that is redirecting enterprise AI investment from API consumption to model ownership.

Microsoft's deployment of Phi-2 and Phi-3 small language models on Surface devices demonstrated on-device inference performance on 2.7 billion parameter models that matched GPT-3.5 Turbo on domain-specific benchmarks while requiring no internet connectivity and consuming 90% less energy per inference. Apple's integration of small language models for on-device Siri intelligence in iOS 18 — processing requests locally without server round-trips represents the highest-volume deployment of small language model inference in consumer technology history.

Small Language Model Market Size and Forecast

-

Market Size in 2025: USD 10.61 Billion

-

Market Size by 2035: USD 47.1 Billion

-

CAGR: 15.86% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Small Language Model Market - Request Free Sample Report

Small Language Model Market Trends

-

Quantization techniques reducing model weight precision from 32-bit to 8-bit or 4-bit integers without proportional accuracy loss are enabling SLM deployment on consumer hardware including smartphones and IoT devices whose memory and compute constraints would prohibit full-precision model inference.

-

Retrieval-Augmented Generation integration with SLMs is enabling domain-specific AI assistants that retrieve relevant information from curated knowledge bases before generating responses improving accuracy on specific knowledge domains without requiring model retraining.

-

Federated learning approaches are enabling SLMs to be trained on distributed datasets across multiple organizations without requiring data centralization — enabling healthcare, finance, and legal industry SLM development while preserving data privacy.

-

Mixture of Experts (MoE) architectures are being applied at the small model scale, enabling SLMs to maintain specialized capabilities across multiple domains without proportional parameter count increases.

-

Model merging techniques combining multiple fine-tuned SLMs through weight averaging and interpolation are enabling capability combination without additional training, creating specialized hybrid models for complex task requirements.

-

On-device SLM inference chip optimization including Apple's Neural Engine, Qualcomm's Hexagon NPU, and Samsung's Exynos NPU is enabling sustained SLM inference at smartphone battery life compatible power levels that cloud-dependent models cannot match.

-

Open-source SLM ecosystem maturity through Hugging Face's model hub hosting over 500,000 fine-tuned model variants is democratizing SLM access for developers and researchers who would otherwise require proprietary model API relationships.

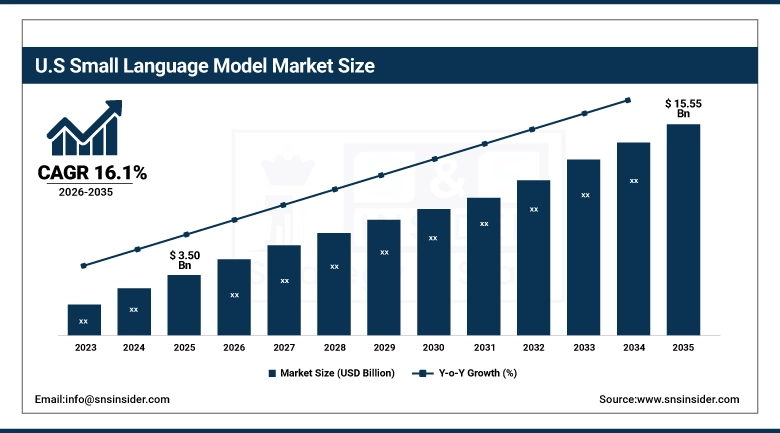

U.S. Small Language Model Market was valued at USD 3.50 billion in 2025 and is expected to reach USD 15.55 billion by 2035, growing at a CAGR of 16.1% from 2026-2035.

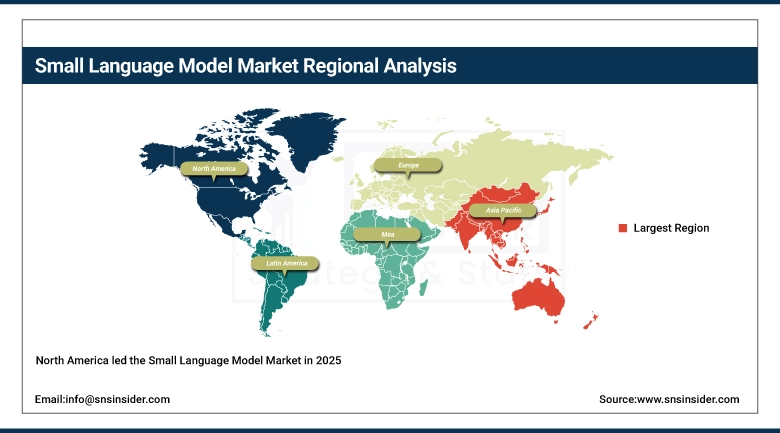

North America led the Small Language Model Market with approximately 33% revenue share in 2025, driven by the United States' concentration of AI development capability Microsoft, Google, Meta, Apple, Mistral AI, and Cohere are all building small language model families from their U.S. research bases and the enterprise technology adoption culture that is driving the practical business case for SLM deployment. The U.S. enterprise SLM market is particularly active in financial services where data privacy requirements and regulatory compliance obligations make cloud LLM API dependencies difficult to justify for sensitive document processing in healthcare where HIPAA data handling requirements create similar cloud dependency concerns and in defense and intelligence where classified data environments entirely preclude cloud-connected AI inference. The presence of edge computing hardware leaders including Qualcomm, Intel, NVIDIA, and Apple in the U.S. sustains the hardware ecosystem that makes practical SLM edge deployment possible.

Stanford University's 2024 AI Index documents that U.S. companies produced 61 notable AI models in 2023 —more than China and Europe combined with the majority designed for task-specific rather than general-purpose deployment, reflecting the commercial reality that specialized models deliver better ROI than general models for most enterprise use cases. The Hugging Face model hub's statistics show that open-source SLMs under 10B parameters account for 78% of all model download activity, with healthcare, finance, and legal as the most active fine-tuning domains.

Small Language Model Market Segment Analysis

-

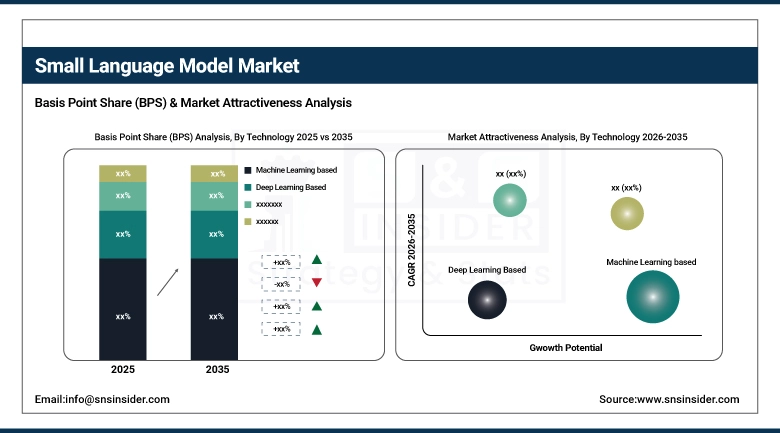

By Technology, Machine Learning-based dominated with 58% share in 2025; Deep Learning-based fastest growing at 17.84% CAGR.

-

By Deployment, Cloud dominated with 58% share in 2025; Hybrid fastest growing at 18.25% CAGR.

-

By Application/End User, Consumer dominated with 29% share in 2025; Healthcare fastest growing at 18.31% CAGR.

By Technology: Machine Learning dominates, Deep Learning growing fastest

Machine Learning-based SLMs held approximately 58% of the Small Language Model Market in 2025, reflecting the broad deployment of classical ML-based NLP approaches BERT-scale transformer models, sentence transformers, and task-specific fine-tuned models across enterprise applications where their computational efficiency, well-understood behavior, and relatively straightforward deployment economics make them the first choice for automation, classification, and information retrieval tasks. ML-based SLMs represent the technology class with the longest commercial deployment history, the most established fine-tuning tooling ecosystem, and the most accessible inference infrastructure factors that sustain their market dominance even as the capabilities of Deep Learning-based alternatives improve. Distilbert, RoBERTa-base, and ALBERT are representative ML-based SLMs whose deployment across customer service, document classification, and semantic search applications underpins this segment's commercial scale.

Deep Learning-based SLMs which include generative transformer models like Phi-2, Gemma-2B, Llama-3.1-8B, and Mistral-7B are growing at the fastest CAGR of approximately 17.84%, driven by the dramatic improvement in task performance that generative deep learning enables relative to discriminative ML approaches for complex language tasks including text generation, multi-turn dialogue, and contextual question answering. The commoditization of transformer model training through open-source frameworks (PyTorch, Transformers library) and accessible cloud computing has enabled organizations to fine-tune Deep Learning SLMs on proprietary domain data at costs measured in hundreds rather than millions of dollars creating the economic viability for specialized SLM development that was not present when foundational model training required hundreds of millions in compute investment.

By Deployment: Cloud dominates, Hybrid growing fastest

Cloud deployment held approximately 58% of the Small Language Model Market in 2025, representing the model access pathway most accessible to organizations whose data privacy requirements, technical capability, and infrastructure investment appetite favor managed service consumption over self-hosted model operation. Cloud SLM services from AWS Bedrock, Google Vertex AI, and Microsoft Azure AI model catalog provide fine-tuned SLM hosting with enterprise SLA commitments, usage-based billing, and managed inference infrastructure that eliminates the operational complexity of running model servers in self-managed environments. Cloud SLM economics are increasingly attractive as providers optimize inference costs: serving a Phi-3 mini or Gemma-2B via managed cloud API costs 70-90% less per token than equivalent GPT-4o queries, making cloud SLM the cost-efficient alternative to large model API consumption for high-volume enterprise applications.

Hybrid deployment is growing at the fastest CAGR of approximately 18.25%, reflecting the enterprise architectural pattern that combines on-device or on-premises SLM inference for sensitive or low-latency workloads with cloud LLM API access for complex tasks requiring the broader capability of full-scale models. A financial services firm might run a fine-tuned 7B parameter compliance document classifier entirely on-premises where no customer data leaves the company network, while routing complex analytical queries to a cloud-hosted LLM for tasks where privacy concerns are lower and output quality requirements are higher. This hybrid pattern is the emerging enterprise AI architecture, and it creates demand for orchestration tools, model serving infrastructure, and fine-tuning services that serve both deployment modes simultaneously.

By Application: Consumer dominates, Healthcare growing fastest

The Consumer segment held approximately 29% of the Small Language Model Market in 2025, reflecting the billions of consumer devices smartphones, smart speakers, laptops, and wearables that embed SLM inference for voice recognition, predictive text, automated replies, photo organization, and virtual assistant functions. Apple's device intelligence, Google's Gboard next-word prediction, Samsung's Bixby voice processing, and Amazon's Alexa processing offload each represent SLM deployments at consumer electronics scale, where model inference happens billions of times daily across the installed base. The growing sophistication of consumer device ML chips with 35+ TOPS of neural processing capability in flagship smartphones is enabling progressively more sophisticated on-device SLM applications that respond with sub-100ms latency without cloud connectivity.

Healthcare is expected to grow at the fastest application CAGR of approximately 18.31%, driven by the convergence of clinical necessity and data privacy requirements that make domain-specific, on-premises SLM deployment uniquely compelling for healthcare organizations. Clinical documentation automation where SLMs listen to physician-patient conversations and generate structured medical notes is the application creating the most immediate healthcare SLM demand: documentation burden consumes 2+ hours of physician time per day, SLM-powered documentation automation demonstrably reduces this burden, and the PHI-protected nature of the data requires on-premises inference that precludes cloud API alternatives for most healthcare providers. Medical knowledge SLMs fine-tuned on clinical literature, drug interaction databases, and clinical guidelines are creating AI clinical decision support that supplements physician judgment without requiring internet connectivity during care delivery.

Small Language Model Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Asia Pacific |

China |

45% |

|

Europe |

Germany |

25% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

North America SLM Market Insights

North America led the Small Language Model Market in 2025, driven by the United States' AI research leadership, enterprise technology adoption culture, and the presence of the companies defining the SLM competitive landscape. Microsoft's Phi model family released progressively from Phi-1 to Phi-3 has established a benchmark for small model performance that has shaped competitive positioning across the SLM market. Google's Gemma and Apple's OpenELM represent additional leading U.S.-headquartered SLM contributions. Enterprise demand for SLMs is most commercially developed in the U.S. market, where financial services, healthcare, and legal industry verticals have specific regulatory and operational requirements that make domain-specific SLM deployment commercially compelling at scales that no other national market approaches.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific SLM Market Insights

Asia Pacific is the fastest-growing regional Small Language Model Market, driven by China's domestic AI development investments, India's growing AI engineering talent pool, Japan's industrial AI applications, and South Korea's technology manufacturing sector. China's restrictive approach to foreign cloud AI services which creates commercial pressure toward domestically hosted AI infrastructure sustains domestic SLM development investment from companies including Baidu, Alibaba, and ByteDance whose commercial AI products require on-premises deployable models. The region's diversity of languages Chinese, Japanese, Korean, Hindi, Thai, and dozens of others create demand for multilingual SLMs that global providers do not prioritize, sustaining regional SLM development that serves language-specific market needs that English-centric global models underserve.

Europe SLM Market Insights

Europe's Small Language Model Market is growing with the EU AI Act's regulatory framework creating both compliance requirements that SLMs with transparent, documented training and behavior are better positioned to satisfy than opaque large models, and sovereignty concerns that make European organizations receptive to domestic or on-premises AI deployment over cloud AI API dependency. Mistral AI's French-headquartered SLM development with its Mistral-7B and Mixtral-8x7B models among the most commercially successful open-source SLMs represents European AI ecosystem strength in the SLM space. Germany's industrial AI applications, France's healthcare AI programs, and the Nordic countries' digital government AI investments each contribute to European SLM market development.

MEA and Latin America SLM Market Insights

The Middle East's SLM market is developing around the UAE's ambitious AI national strategy and Saudi Arabia's Vision 2030 technology investments, with Arabic-language SLM development receiving particular attention as the Gulf states seek AI capabilities that serve their linguistic and cultural context. The Technology Innovation Institute (TII) in Abu Dhabi developer of the Falcon LLM family represents the Gulf states' commitment to developing sovereign AI capabilities that don't depend on Western model providers. Latin America's SLM market is growing in Brazil and Mexico, where Portuguese and Spanish language SLM development is creating regional AI capabilities that global English-centric models underserve.

Market Growth Drivers:

Edge computing expansion and privacy-first AI demand driving sustained small language model market growth globally

The Small Language Model Market's 15.86% CAGR is driven by commercial forces that are each independently powerful. The edge computing wave IoT, autonomous vehicles, industrial robots, consumer electronics creates AI inference requirements that cloud latency and connectivity dependency make impossible to satisfy with large cloud-hosted models. Only SLMs deployable on edge hardware can meet the sub-10ms inference latency that real-time edge AI applications require. Privacy and data sovereignty requirements across healthcare, finance, legal, and government are creating regulatory incentive for on-premises AI deployment that cloud API models cannot satisfy. Cost optimization pressure from enterprises discovering that production-scale LLM API consumption is prohibitively expensive is driving architectural migration toward specialized SLMs whose inference cost is 90%+ below large model equivalents for appropriate tasks.

Market Restraints:

Performance gaps for complex reasoning tasks and fine-tuning expertise requirements limiting small language model adoption globally

Small language models' fundamental limitation is their performance ceiling on tasks requiring broad knowledge synthesis, multi-step complex reasoning, or sophisticated contextual understanding across long documents. A 7B parameter model cannot reliably perform the kind of nuanced legal analysis, complex financial modeling, or broad scientific synthesis that the most capable large language models handle with increasing confidence and for organizations whose AI use cases genuinely require these capabilities, SLMs are not viable alternatives regardless of cost and privacy advantages. The fine-tuning expertise required to achieve production-quality SLM performance for specific domains is additionally a deployment barrier general-purpose SLMs without domain-specific fine-tuning often underperform general-purpose LLM APIs for domain tasks, making the value realization of SLM adoption dependent on ML engineering capability that many organizations lack internally.

Market Opportunities:

Healthcare AI automation and industrial edge AI creating transformative small language model market growth opportunities globally

The healthcare AI documentation opportunity eliminating 2+ hours of daily physician documentation burden through ambient clinical documentation powered by medical SLMs represents one of the largest single-application commercial opportunities in the SLM market. Nuance DAX Copilot, Suki AI, and Augmedix are building managed medical documentation SLM services that operate as cloud services, but the market for on-premises medical SLMs that process PHI within the hospital network boundary without any cloud dependency is developing alongside and represents the highest-privacy segment of a very high-value application. Industrial AI applications manufacturing quality inspection, predictive maintenance, process optimization create SLM demand at the equipment and factory floor level where cloud connectivity is unreliable, latency requirements are tight, and the domain specificity of the task makes general-purpose large models unnecessary.

Recent Developments:

-

2026: Microsoft released Phi-4 Small, a 3.8-billion parameter model that achieved equivalent performance to GPT-3.5-Turbo on the MMLU academic benchmark while running inference on a mobile CPU at 30 tokens per second enabling integration into Microsoft 365 applications for on-device AI assistance that processes documents locally without transmitting content to Microsoft servers, a privacy-preserving AI feature targeting enterprise customers with strict data residency requirements.

-

2025: Google launched Gemma 3 with a 4B parameter version achieving state-of-the-art performance on multilingual benchmarks in 35 languages, with optimization specifically for on-device deployment through TensorFlow Lite and MediaPipe enabling Android developers to integrate production-quality multilingual AI directly into mobile applications without cloud API dependencies for markets where offline AI capabilities are commercially essential.

-

2025: Mistral AI released Mistral NeMo 12B under Apache 2.0 open-source license, specifically designed for enterprise fine-tuning with extended context window support up to 128k tokens, instruction-following improvements, and function calling capabilities reporting that enterprise customers using fine-tuned NeMo variants for domain-specific document processing achieved 94% accuracy on relevant tasks versus 78% from general-purpose API models, validating the ROI case for SLM fine-tuning investment.

Small Language Model Market Key Players

Some of the Small Language Model Market Companies

-

Microsoft Corporation (Phi model family)

-

Google LLC (Gemma, PaLM 2 Bison)

-

Meta Platforms Inc. (Llama 3)

-

Apple Inc. (OpenELM, Core ML)

-

Mistral AI SAS

-

Cohere Inc.

-

AI21 Labs Ltd.

-

Technology Innovation Institute (Falcon)

-

Cerebras Systems Inc.

-

Hugging Face Inc.

-

NVIDIA Corporation (Megatron)

-

IBM Corporation (Granite)

-

Samsung Electronics (Samsung AI)

-

Baidu Inc. (ERNIE Speed)

-

Alibaba Group (Qwen)

-

Amazon Web Services Inc. (Titan Lite)

-

Stability AI Ltd.

-

EleutherAI

-

Together AI Inc.

-

Perplexity AI Inc.

Small Language Model Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.61 Billion |

| Market Size by 2035 | USD 47.1 Billion |

| CAGR | CAGR of 15.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Deep Learning Based, Machine Learning Based, Rule Based System) • By Deployment (Cloud, On-premises, Hybrid) • By Application (Consumer Applications, Enterprise Applications, Healthcare, Finance, Retail, Legal, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation (Phi model family), Google LLC (Gemma, PaLM 2 Bison), Meta Platforms Inc. (Llama 3), Apple Inc. (OpenELM, Core ML), Mistral AI SAS, Cohere Inc., AI21 Labs Ltd., Technology Innovation Institute (Falcon), Cerebras Systems Inc., Hugging Face Inc., NVIDIA Corporation (Megatron), IBM Corporation (Granite), Samsung Electronics (Samsung AI), Baidu Inc. (ERNIE Speed), Alibaba Group (Qwen), Amazon Web Services Inc. (Titan Lite), Stability AI Ltd., EleutherAI, Together AI Inc., Perplexity AI Inc. |

Frequently Asked Questions

Healthcare is expected to register the fastest CAGR of approximately 18.31%.

Hybrid deployment is growing at the fastest CAGR of approximately 18.25%.

Machine Learning-based dominated with approximately 58% share; Deep Learning-based is fastest growing at 17.84% CAGR.

The Small Language Model Market was valued at USD 10.61 billion in 2025.

The Small Language Model Market is expected to grow at a CAGR of 15.86% from 2026 to 2035.

Get in Touch