Shipbuilding Market Report Scope & Overview:

The Shipbuilding Market Size was valued at USD 161.94 billion in 2024 and is expected to reach USD 211.28 billion by 2032 with a growing CAGR of 3.38% over the forecast period 2025-2032.

Shipwrights are another term for shipbuilders. The shipbuilding industry is in charge of the design and construction of ocean-going boats all over the world. Asia-Pacific currently dominates the worldwide shipbuilding sector, followed by Europe, North America, and LAMEA. Asia-Pacific is likely to maintain its worldwide market domination, particularly in China, South Korea, and Japan, because to several distinct advantages such as relatively lower wages, significant government support, and strong forward and backward industry connectivity. Shipbuilding is a very capital-intensive business, hence significant government assistance and political stability are required to survive.

To get more information on Shipbuilding Market - Request Free Sample Report

The shipbuilding market refers to the shipbuilding process, which comprises several procedures such as designing and manufacturing ships and other floating vessels. The market manufactures large ships, particularly seagoing boats, which are used by many industries such as transportation, trading, energy, and military. The Shipbuilding Market even offers products for vessel construction and maintenance. The market is also undergoing technical improvements and upgrades in order to increase trade and transportation. Ships are designed to be versatile for a variety of functions. Increased demand for maritime transportation has higher imports and exports, resulting in increased Shipbuilding Market Growth.

Market Size and Forecast:

-

Market Size in 2024 USD 161.94 Billion

-

Market Size by 2032 USD 211.28 Billion

-

CAGR of 3.38% From 2025 to 2032

-

Base Year 2024

-

Forecast Period 2025-2032

-

Historical Data 2021-2023

Key Shipbuilding Market Trends:

-

Advancements in marine vessel engine technology improving fuel efficiency and reducing environmental impact.

-

Rising demand for ship-borne cargo transportation driven by globalization and international trade growth.

-

Adoption of high-capacity, modern vessels to meet increasing shipping and logistics needs.

-

Implementation of stricter marine safety standards, promoting development of advanced vessel designs.

-

Growing integration of automation and autonomous navigation in sea transportation to enhance efficiency and reduce human error.

Shipbuilding Market Growth Drivers:

Key drivers of the Shipbuilding Market include advances in marine vessel engine technology, which enhance efficiency, reduce emissions, and support sustainable operations. Additionally, the rising demand for ship-borne cargo transportation, fueled by globalization and expanding international trade, is boosting the need for modern, high-capacity vessels, driving consistent growth in the global shipbuilding industry.

Shipbuilding Market Restraints:

Key restraints of the Shipbuilding Market include cost fluctuations in transportation and inventory, which increase operational expenses and affect profitability. Additionally, growing concerns about marine vessels' environmental impact, such as carbon emissions, fuel consumption, and marine pollution, are pressuring shipbuilders to adopt costly sustainable technologies, creating challenges for market growth and competitiveness.

Shipbuilding Market Opportunities:

The Shipbuilding Market presents significant opportunities with the enforcement of increased marine safety standards, driving demand for advanced vessel designs and safety technologies. Additionally, the rising popularity of automation in sea transportation, including smart ships and autonomous navigation systems, offers shipbuilders growth potential by enhancing operational efficiency, reducing human error, and improving overall maritime logistics.

Shipbuilding Market Segment Analysis:

By Ship Type

In 2024, container ships dominated the shipbuilding market due to increasing global trade and demand for efficient cargo transportation. From 2025 to 2032, the passenger ships segment is expected to grow at the fastest CAGR, driven by rising tourism, cruise industry expansion, and growing demand for luxury and recreational vessels, creating significant opportunities for shipbuilders worldwide.

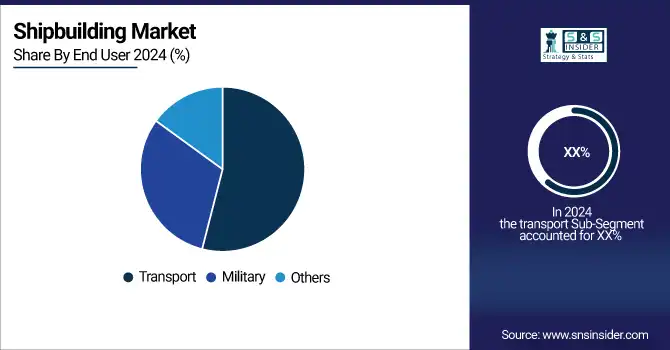

By End User

In 2024, the transport segment dominated the shipbuilding market, driven by the need for commercial cargo and logistics vessels supporting global trade. From 2025 to 2032, the military segment is expected to grow at the fastest CAGR, fueled by increased defense budgets, modernization of naval fleets, and rising demand for advanced warships and strategic maritime capabilities.

Shipbuilding Market Regional Analysis:

North America Shipbuilding Market Insights

North America’s shipbuilding market is driven by naval fleet modernization, defense spending, and demand for advanced cargo and passenger vessels. Technological advancements, stringent safety regulations, and increasing offshore energy projects further support market growth, positioning the region as a key player in both commercial and military shipbuilding sectors.

Need any customization research on Shipbuilding Market - Enquiry Now

Asia Pacific Shipbuilding Market Insights

Asia Pacific dominates global shipbuilding due to strong presence of major shipyards, rising international trade, and government support for maritime infrastructure. High demand for container ships, bulk carriers, and cruise vessels, coupled with technological innovations and cost-effective manufacturing, fuels rapid market growth across the region.

Europe Shipbuilding Market Insights

Europe’s shipbuilding market benefits from advanced engineering, stringent environmental regulations, and high-quality vessel production. Strong demand for passenger ships, cruise liners, and specialized vessels, along with investments in green shipping technologies, drives growth while maintaining the region’s reputation for precision and innovation in shipbuilding.

Latin America (LATAM) and Middle East & Africa (MEA) Shipbuilding Market Insights

The LATAM and MEA shipbuilding markets are expanding due to rising offshore oil and gas activities, port infrastructure development, and increasing maritime trade. Investments in naval modernization, cargo vessels, and regional shipyards support growth, with opportunities emerging in both commercial and defense maritime sectors.

Shipbuilding Market Key Players:

The Major Players are

-

Oshima Shipbuilding Co., Ltd.

-

Sumitomo Heavy Industries, Ltd.

-

Damen Shipyards Group

-

General Dynamics Corporation

-

Huntington Ingalls IndustriesInc.

-

Samsung Heavy Industries Co., Ltd.

-

Hyundai Heavy Industries Co., Ltd.

-

Daewoo Shipbuilding & Marine Engineering Co., Ltd.

-

China State Shipbuilding Corporation (CSSC)

-

Japan Marine United Corporation

-

Imabari Shipbuilding Co., Ltd.

-

STX Offshore & Shipbuilding Co., Ltd.

-

Mazagon Dock Shipbuilders Limited

-

Cochin Shipyard Limited

-

Austal Limited

-

Navantia S.A.

-

Mitsubishi Heavy Industries Ltd-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 161.94 Billion |

| Market Size by 2032 | USD 211.28 Billion |

| CAGR | CAGR of 3.38% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By End User (Transport and Military) • By Ship Type (Bulk Carriers, General Cargo Ships, Container Ships, Passenger Ships and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Korea Shipbuilding & Offshore Engineering Co., Ltd., Mitsubishi Heavy Industries, Ltd., Oshima Shipbuilding Co., Ltd., Sumitomo Heavy Industries, Ltd., Damen Shipyards Group, Fincantieri Group, Bae Systems Plc, General Dynamics Corporation, Huntington Ingalls Industries, Inc., Samsung Heavy Industries Co., Ltd., and other players. |