Get More Information on Semiconductor Tubing Market - Request Sample Report

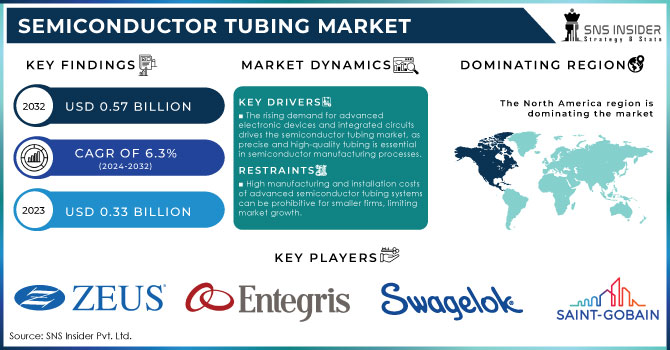

The Semiconductor Tubing Market Size was valued at USD 0.33 Billion in 2023 and is expected to reach USD 0.57 Billion by 2032 and grow at a CAGR of 6.3% over the forecast period 2024-2032.

The Semiconductor Tubing Market is essential for semiconductor manufacturing, including materials such as semiconductor quartz tubing and stainless steel tubing, necessary for high-performance uses in the ever-changing consumer electronics industry. The increasing popularity of advanced gadgets like smartphones, tablets, and wearables has led to a higher demand for dependable and top-notch tubing solutions. The Consumer Technology Association predicts that the United States will exceed USD 487 billion in consumer electronics sales by 2024, in line with the increasing manufacturing of crucial semiconductors for these products. The increasing need for chips is pushing advancements in manufacturing technologies, especially as the focus shifts to smaller nodes such as 5nm and lower. Additionally, companies are expected to see significant growth in the market for semiconductor tubing, particularly in options like fluorinated ethylene propylene (FEP) and stainless steel, as they work to follow strict cleanroom regulations to avoid contamination. The growth of the Internet of Things (IoT) and the demand for dependable semiconductor solutions to support consistent connectivity and effective data processing are driving this trend. In conclusion, the Semiconductor Tubing Market is set for strong expansion, driven by the increasing need for consumer electronics and improvements in semiconductor manufacturing technology.

The recent epigraphene discovery, the first fully functional graphene-based semiconductor globally, has major ramifications for the semiconductor industry. This new material, made from silicon carbide (SiC), has electron mobility ten times higher than regular silicon, which could allow chips to function in the terahertz frequency range. This progress coincides with projections from the U.S. Semiconductor Industry Association, which expects strong expansion in the semiconductor field with the incorporation of new materials such as graphene into production methods. As a result, there is anticipated growth in the need for specific types of semiconductor tubing, specifically stainless steel and semiconductor quartz tubing. These tubing options are crucial for upholding purity and accuracy in advanced settings. The growing emphasis on high-performance materials highlights the need for advanced tubing solutions that can endure severe conditions and prevent contamination in semiconductor manufacturing.

Drivers

The Impact of Advancements in Semiconductor Manufacturing Technology on the Semiconductor Tubing Market

Innovations in semiconductor production technology play a vital role in the Semiconductor Tubing Market, especially with the shift towards smaller fabrication nodes like 5nm and lower. This trend of shrinking in size requires specialized tubing that can handle harsh conditions and still perform well. Semiconductor quartz tubing and specialized fluoropolymers like perfluoroalkoxy alkane (PFA) and fluorinated ethylene propylene (FEP) are favored for their exceptional chemical resistance and thermal stability. These qualities are essential in semiconductor manufacturing for precise applications, as cleanliness and contamination prevention are crucial. Market analyses predict that the worldwide semiconductor tubing market will experience substantial growth due to the growing demand for top-notch materials that can meet the changing requirements of cutting-edge chip manufacturing. With manufacturers striving to make smaller, more powerful chips, the need for excellent tubing solutions is emphasized, highlighting the importance of advancements in semiconductor manufacturing technology for the market's growth. As a result, the Semiconductor Tubing Market is set to grow, fueled by the industry's ongoing pursuit of innovation and effectiveness in semiconductor manufacturing processes.

Effects of Electric Cars and Automotive Electronics on the Semiconductor Tubing market

The growth of electric vehicles (EVs) and improvements in automotive electronics are changing the automotive industry, greatly impacting the semiconductor tubing market. The U.S. government is increasingly focused on sustainability and has established ambitious objectives, such as aiming for 50% of new vehicle sales to be electric by 2030, as detailed in the Biden Administration's electric vehicle strategy. The move to electric vehicles requires incorporating sophisticated semiconductor components to improve performance, safety, and connectivity in vehicles. The need for top-notch semiconductor tubing like FEP tubing and stainless steel tubing is increasing as they are crucial in manufacturing processes needing chemical resistance and purity. The IEA stated that in 2022, the number of electric cars sold worldwide exceeded 10 Billion, showing a noteworthy 55% rise from the previous year. This increase is closely tied to the increasing need for semiconductors, which are essential for the advanced electronic systems in present-day cars. With the integration of IoT technologies and improved safety features in vehicles, the semiconductor tubing market is expected to experience significant growth due to the automotive industry's move towards more intelligent and sustainable transportation options.

Restraints

The semiconductor tubing market is experiencing fluctuating raw material costs.

In 2023, the semiconductor tubing market is encountering major obstacles caused by the unpredictable availability and prices of raw materials. Stainless steel and fluorinated ethylene propylene (FEP) are commonly used in semiconductor tubing and their prices can fluctuate due to disruptions in the global supply chain, geopolitical tensions, and rising demand from sectors like automotive and electronics. Recent reports show that the cost of stainless steel has experienced fluctuations of as much as 25% over the last year, mainly due to the increase in global demand for electric vehicles and renewable energy technologies. As per the U.S. Geological Survey, there is projected increase in the demand for vital minerals like nickel and cobalt used in batteries, which will affect the production expenses of semiconductor materials.The fluctuation of raw materials in the semiconductor tubing market causes uncertainties for manufacturers, impacting their pricing strategies and profitability. Businesses may struggle to keep supply chains stable and meet production deadlines, which could result in delays and higher expenses. The demand for innovation and high-quality product development, alongside the need to manage limitations, may impede market expansion. Therefore, stakeholders in the semiconductor tubing market need to maneuver through these complexities to maintain their business and take advantage of new opportunities in a competitive environment.

by Distribution Channel

In the year 2023, the offline distribution channel held a substantial revenue share of 53.89% in the semiconductor tubing market. The main reason for this dominance is the well-established supply chain networks and the preference of industrial clients for direct procurement and in-person interactions for sourcing specialized products. Top companies like Swagelok Company and Parker Hannifin have strengthened their traditional strategies through the introduction of new product lines and improvements to their distribution abilities. For example, Swagelok released a line of stainless steel tubing fittings to address the increasing needs of the semiconductor sector, focusing on dependability and productivity. In the meantime, Parker Hannifin increased its worldwide distribution network through the establishment of new regional offices, improving the availability of its inventive FEP tubing products. Furthermore, businesses such as NewAge Industries have dedicated their efforts to improving their brick-and-mortar presence by teaming up with nearby distributors to improve customer service and technical assistance. This focus on traditional channels allows manufacturers to establish solid connections with customers, ensuring availability of products and personalized solutions, essential in an industry marked by fast technological progress and changing customer demands. Hence, the strong performance of the offline channel highlights its crucial importance in the semiconductor tubing market.

by End User

In the year 2023, there was strong expansion in the semiconductor tubing market, with the Electronics and Semiconductors segment leading in revenue with a share of 40.56%. This rise in dominance is a result of the growing need for top-notch semiconductor parts, crucial for operating cutting-edge electronic gadgets. Firms such as Texas Instruments and Intel lead the way by launching advanced products that need specialized semiconductor tubing for effective manufacturing. Texas Instruments has just introduced a new range of high-performance microcontrollers for IoT applications, highlighting the importance of using dependable FEP tubing to ensure purity throughout the manufacturing process. Likewise, Intel revealed progress in their semiconductor manufacturing procedures, highlighting the vital importance of stainless steel tubing in maintaining peak performance and chemical durability. The increased attention on making consumer electronics smaller and more efficient is closely connected to the need for semiconductor tubing, necessary for maintaining cleanliness in the production of microchips and other parts. With advancements in 5G technology and smart devices shaping the electronics industry, the semiconductor tubing market is set to grow further as manufacturers work on developing products to meet the industries' complex needs.

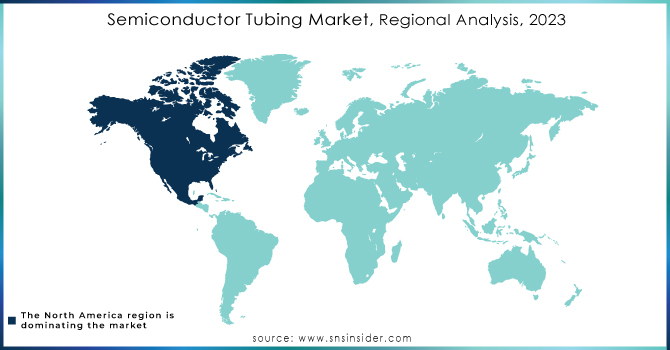

In 2023, North America held the most significant share of the semiconductor tubing market at 34.44%. The leadership in this area is mainly influenced by the advanced semiconductor manufacturing abilities, significant technology, and innovation investments in the region. Leading companies such as Applied Materials and Lam Research are at the forefront of developing new products, with Applied Materials unveiling a state-of-the-art chemical vapor deposition system that requires top-notch FEP tubing for effective processing. Moreover, the U.S. government has increased backing for semiconductor manufacturing with programs like the CHIPS Act, designed to boost local production and decrease dependence on overseas supply chains. This support from the government motivates local businesses to invest in cutting-edge semiconductor technologies, leading to increased need for specialized tubing solutions. Furthermore, Canadian companies are progressing as well, with Celestica enhancing its manufacturing capacity for electronic components that utilize semiconductor tubes in their production procedures. As semiconductor innovation thrives in North America, the need for dependable tubing solutions will increase, highlighting the vital importance of the semiconductor tubing market in advancing technology and industry growth in the region.

In 2023, the semiconductor tubing market experienced rapid growth in the Asia-Pacific region due to technological advancements and rising semiconductor component demand. Nations such as China, Japan, and South Korea lead the way by making substantial investments in semiconductor production facilities. For example, Samsung Electronics introduced a wider range of silicon carbide tubing to improve power device performance, highlighting the increasing demand for top-notch materials in semiconductor manufacturing. Furthermore, Taiwan Semiconductor Manufacturing Company (TSMC) is increasing production capacity by implementing cutting-edge FEP tubing solutions to assist its advanced fabrication plants. The increased use of 5G technology and IoT devices is driving up the need for semiconductor components, requiring advanced tubing solutions to guarantee both chemical purity and operational effectiveness. Additionally, governments in the Asia-Pacific area are putting in place favorable policies and investments to enhance their semiconductor industries, establishing them as key participants in the worldwide market. Consequently, sustained growth is projected for the semiconductor tubing market in Asia-Pacific due to innovation and expanding production capacity in the semiconductor market.

Need any customization research on Semiconductor Tubing Market - Enquiry Now

Key Players

Some of the major key players in Semiconductor Tubing market who offer their product:

Saint-Gobain Performance Plastics (Tygon Tubing)

Swagelok Company (Swagelok Tubing and Fittings)

Entegris, Inc. (Fluoropolymer Tubing)

Parker Hannifin Corporation (Parflex Tubing Solutions)

Zeus Industrial Products, Inc. (PTFE Tubing)

NewAge Industries, Inc. (Nylobrade Tubing)

Trelleborg Sealing Solutions (Thermoplastic Tubing Solutions)

NICHIAS Corporation (Fluoropolymer Tubing)

Polyflon Technology Ltd. (PTFE and FEP Tubing)

Fluorotherm Polymers, Inc. (FEP and PFA Tubing)

Freudenberg Group (Sealing Solutions and Tubing)

Optinova Group (Medical Grade Tubing)

SMC Corporation (Pneumatic Tubing Solutions)

Cole-Parmer (Pharmaceutical Tubing)

Habia Teknofluor AB (PTFE and FEP Tubing)

Victrex plc (PEEK Tubing)

Global Technology Group (Silicone Tubing)

Thermo Fisher Scientific (Laboratory Tubing)

Kynar (Arkema) (PVDF Tubing)

SABIC (Ultem Tubing)

Others

Recent Development

On August 6, 2024, researchers highlighted the significant environmental impact of Per- and polyfluoroalkyl substances (PFAS) used in semiconductor manufacturing. The study found that these compounds contribute to emissions that pose risks to human health and ecosystems, prompting calls for stricter regulations and alternative materials to mitigate their use. As the semiconductor industry faces increasing scrutiny, there is a growing push for sustainable manufacturing practices.

On January 19, 2024, researchers at the Georgia Institute of Technology introduced epigraphene, the first functional graphene-based semiconductor, offering superior electron mobility compared to silicon. This technology, produced using an argon quartz tube, could lead to terahertz processors and advances in quantum and conventional computing.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 0.33 Billion |

| Market Size by 2032 | USD 0.57 Billion |

| CAGR | CAGR of 6.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fluorinated Ethylene Propylene Tubing,Perfluoroalkoxy Tubing, Polytetrafluoroethylene Tubing, Polyvinylidene fluoride Tubing, Silicone Tubing) • By Distribution Channel (Offline, Online) • By End-User (Automotive, Electronics & Semiconductors, Healthcare & Life Sciences, Telecommunication) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Saint-Gobain Performance Plastics, Swagelok Company, Entegris, Inc., Parker Hannifin Corporation, Zeus Industrial Products, Inc., NewAge Industries, Inc., Trelleborg Sealing Solutions, NICHIAS Corporation, Polyflon Technology Ltd., Fluorotherm Polymers, Inc., Freudenberg Group, Optinova Group, SMC Corporation, Cole-Parmer, Habia Teknofluor AB, Victrex plc, Global Technology Group, Thermo Fisher Scientific, Kynar (Arkema), and SABIC. & Others |

| Key Drivers | • The Impact of Advancements in Semiconductor Manufacturing Technology on the Semiconductor Tubing Market • Effects of Electric Cars and Automotive Electronics on the Semiconductor Tubing market |

| RESTRAINTS | • The semiconductor tubing market is experiencing fluctuating raw material costs. |

Ans: The Semiconductor Tubing Market Size was valued at USD 0.33 billion in 2023 and is expected to reach USD 0.57 billion by 2032.

Ans: The semiconductor tubing Market grow at a CAGR of 6.3% over the forecast period of 2024-2032.

Ans: Major players in the semiconductor tubing market include Swagelok, Saint-Gobain, Entegris, Parker Hannifin, IDEX Health & Science, Trelleborg, SMC Corporation, Nippon Pillar, Zeus Industrial Products, and NewAge Industries, offering innovative tubing solutions.

Ans:The semiconductor manufacturing industry is the primary user, with applications in wafer processing, etching, and chemical distribution. Additionally, sectors like electronics, pharmaceuticals, and biotechnology also utilize similar tubing in cleanroom environments.

Ans: Common materials include fluoropolymers (like PTFE and PFA), stainless steel, and other high-purity plastics. These materials ensure chemical resistance, durability, and minimal contamination in semiconductor manufacturing environments.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Tubing Production and Sales Volumes, 2020-2032, by Region

5.2 Tubing Technology Adoption, by Rates

5.2 Consumer Preferences, by Region

6. Competitive Landscape

6.1 List of Major Companies, by Region

6.2 Market Share Analysis, by Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Semiconductor Tubing Market Segmentation, by Type

7.1 Chapter Overview

7.2 Fluorinated Ethylene Propylene Tubing

7.2.1 Fluorinated Ethylene Propylene Tubing Market Trends Analysis (2020-2032)

7.2.2 Fluorinated Ethylene Propylene Tubing Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Perfluoroalkoxy Tubing

7.3.1 Perfluoroalkoxy Tubing Market Trends Analysis (2020-2032)

7.3.2 Perfluoroalkoxy Tubing Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Polytetrafluoroethylene Tubing

7.4.1 Polytetrafluoroethylene Tubing Market Trends Analysis (2020-2032)

7.4.2 Polytetrafluoroethylene Tubing Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Polyvinylidene fluoride Tubing

7.5.1 Polyvinylidene fluoride Tubing Market Trends Analysis (2020-2032)

7.5.2 Polyvinylidene fluoride Tubing Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Silicone Tubing

7.5.1 Silicone Tubing Market Trends Analysis (2020-2032)

7.5.2 Silicone Tubing Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Semiconductor Tubing Market Segmentation, by Distribution Channel

8.1 Chapter Overview

8.2 Offline

8.2.1 Offline Market Trends Analysis (2020-2032)

8.2.2 Offline Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Online

8.3.1 Online Market Trends Analysis (2020-2032)

8.3.2 Online Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Semiconductor Tubing Market Segmentation, by End-User

9.1 Chapter Overview

9.2 Automotive

9.2.1 Automotive Market Trends Analysis (2020-2032)

9.2.2 Automotive Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Electronics & Semiconductors

9.3.1 Electronics & Semiconductors Market Trends Analysis (2020-2032)

9.3.2 Electronics & Semiconductors Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Healthcare & Life Sciences

9.4.1 Healthcare & Life Sciences Market Trends Analysis (2020-2032)

9.4.2 Healthcare & Life Sciences Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Telecommunication

9.5.1 Telecommunication Market Trends Analysis (2020-2032)

9.5.2 Telecommunication Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.2.4 North America Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.5 North America Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.2.6.2 USA Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.6.3 USA Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.2.7.2 Canada Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.7.3 Canada Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.2.8.2 Mexico Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.8.3 Mexico Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.6.2 Poland Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.6.3 Poland Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.7.2 Romania Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.7.3 Romania Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.4 Western Europe Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.5 Western Europe Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.6.2 Germany Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.6.3 Germany Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.7.2 France Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.7.3 France Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.8.2 UK Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.8.3 UK Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.9.2 Italy Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.9.3 Italy Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.10.2 Spain Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.10.3 Spain Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.13.2 Austria Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.13.3 Austria Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4 Asia-Pacific

10.4.1 Trends Analysis

10.4.2 Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.4 Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.5 Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.6.2 China Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.6.3 China Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.7.2 India Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.7.3 India Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.8.2 Japan Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.8.3 Japan Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.9.2 South Korea Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.9.3 South Korea Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.10.2 Vietnam Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.10.3 Vietnam Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.11.2 Singapore Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.11.3 Singapore Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.12.2 Australia Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.12.3 Australia Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.4.13 Rest of Asia-Pacific

10.4.13.1 Rest of Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia-Pacific Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.4 Middle East Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.5 Middle East Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.6.2 UAE Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.6.3 UAE Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.2.4 Africa Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.5 Africa Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Semiconductor Tubing Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.6.4 Latin America Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.5 Latin America Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.6.6.2 Brazil Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.6.3 Brazil Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.6.7.2 Argentina Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.7.3 Argentina Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.6.8.2 Colombia Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.8.3 Colombia Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Semiconductor Tubing Market Estimates and Forecasts, by Type (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Semiconductor Tubing Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Semiconductor Tubing Market Estimates and Forecasts, by End-User (2020-2032) (USD Billion)

11. Company Profiles

11.1 Saint-Gobain Performance Plastics

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Swagelok Company

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Entegris, Inc.

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Parker Hannifin Corporation

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Zeus Industrial Products, Inc.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 NewAge Industries, Inc.

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Trelleborg Sealing Solutions

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 NICHIAS Corporation

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Polyflon Technology Ltd.

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Fluorotherm Polymers, Inc.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Type

Fluorinated Ethylene Propylene Tubing

Perfluoroalkoxy Tubing

Polytetrafluoroethylene Tubing

Polyvinylidene fluoride Tubing

Silicone Tubing

By Distribution Channel

Offline

Online

By End-User

Automotive

Electronics & Semiconductors

Healthcare & Life Sciences

Telecommunication

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Active Electronic Components Market was valued at USD 323.50 billion in 2023 and is expected to reach USD 635.52 billion by 2032, growing at a CAGR of 7.81% from 2024-2032.

The Force Sensor Market Size was valued at USD 2.77 Billion in 2023 and is expected to grow at a CAGR of 5.59% to reach USD 4.50 Billion by 2032.

The Thermal Imaging Market Size was valued at USD 5.94 Billion in 2023 and is expected to grow at a CAGR of 7.67% to reach USD 11.54 Billion by 2032.

The Ultra Capacitors Market size was USD 2.75 Billion in 2023 and will Reach to USD 9.62 billion by 2032 and growing at CAGR about 15.04% by 2024-2032

The Wirewound Variable Resistors Market was valued at 1.48 Billion in 2023 and is projected to reach USD 2.48 Billion by 2032, growing at a CAGR of 4.37% from 2024 to 2032.

The 3D Metrology Market Size was valued at USD 10.88 Billion in 2023 and is expected to grow at a CAGR of 7.97% to reach USD 21.69 Billion by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd