Get More Information on Semiconductor Memory Market - Request Sample Report

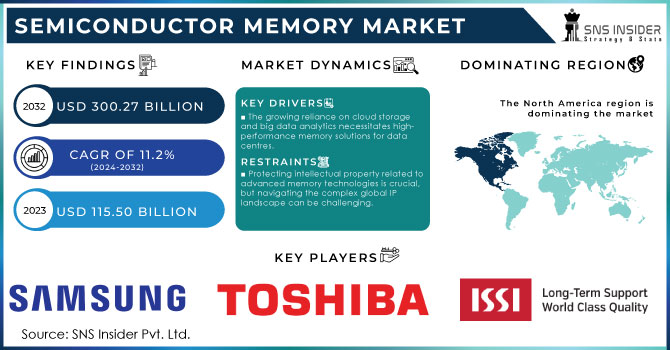

The Semiconductor Memory Market size is expected to be valued at USD 115.50 Billion in 2023. It is estimated to reach USD 300.27 Billion by 2032 with a growing CAGR of 11.2% over the forecast period 2024-2032.

The market is experience significant growth due to the increasing adoption of semiconductor components across various industries, including consumer electronics, automotive, and IT & telecom. It is an essential electronic device that serves as computer memory/chips by utilizing Integrated Circuit (IC) technology. For example, the smartphone industry, valued at $1.4 trillion in 2023, relies heavily on semiconductors like DRAM (Dynamic Random-Access Memory) for processing power and NAND Flash memory for data storage. Similarly, the automotive sector, projected to reach $5.6 trillion by 2026, which is increasingly incorporating semiconductors for advanced driver-assistance systems (ADAS) and autonomous vehicle technology. This growing demand for smarter devices, from wearables and laptops to smart appliances and industrial equipment, is propelling the entire semiconductor market forward.

| Report Attributes | Details |

|---|---|

| Key Segments | • By Type (SRAM, MRAM, DRAM, Flash ROM, Others) • By Application (Consumer Electronics, IT & Telecommunication, Automotive, Industrial, Aerospace & Defense, Medical) |

| Regional Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Samsung, IBM Corporation, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, Taiwan Semiconductor Manufacturing Company Limited, Integrated Silicon Solution Inc., Micron Technology, Inc, Macronix International Co., Ltd., SK HYNIX INC., Texas Instruments Incorporated, Infineon Technologies AG, Everspin Technologies, Inc. |

KEY DRIVERS:

The growing reliance on cloud storage and big data analytics necessitates high-performance memory solutions for data centres.

The rise of AI and ML applications requires vast memory capacities for processing complex algorithms and datasets.

The proliferation of smartphones, tablets, laptops, wearables, and Internet-of-Things (IoT) devices is driving the need for more memory.

The sheer number of devices being produced, coupled with the ever-increasing memory demands within each category, creates a massive and growing market for memory solutions. for e.g. Flagship smartphones can now boast over 12GB of RAM and 1TB of storage. Even mid-range devices pack increasingly larger capacities to handle demanding applications and high-resolution media. also, Global smartphone shipments are expected to reach nearly 1.5 billion units by 2025. Each phone demands memory for storing apps, photos, videos, and the operating system itself.

RESTRAINTS:

Protecting intellectual property related to advanced memory technologies is crucial, but navigating the complex global IP landscape can be challenging.

Capital-intensive Manufacturing can act as a barrier

Setting up and maintaining advanced semiconductor fabrication facilities requires substantial investments, creating a barrier for new entrants.

OPPORTUNITIES:

Focusing on low-power memory solutions, manufacturers can tap into a rapidly growing market while contributing to a more sustainable future.

The ever-growing demand for data storage and processing power is creating a significant environmental burden. Semiconductor memory, a crucial component in this equation, is a major contributor to energy consumption in data centres and electronic devices. Data centres face mounting electricity bills, making low-power memory solutions an attractive cost-saving option. Data centres alone account for roughly 1-3% of global electricity consumption. A significant portion of this energy goes towards powering memory chips.

CHALLENGES:

The presence of counterfeit chips can harm the reputation of legitimate manufacturers and pose security risks.

Intellectual Property (IP) Protection can be Challenging.

Protecting intellectual property related to advanced memory technologies is crucial for manufacturers, but navigating the complex global IP landscape can be challenging.

Ukraine and Russia both are major producers of raw semiconductors such as neon and palladium, which are essential for the production of memory chips and other semiconductors. Ukraine produces 90 percent of the world's semiconductor-grade neon gas, which is used in lithography to etch circuits into silicon wafers. Two Ukrainian gas production companies, Ingas and Cryoin, suspended their operations due to the conflict, which resulted in the loss of 45-54% of the sector's neon supplies. In 2021, the semiconductor industry consumed 540 tons of neon gas to support its operations. The loss of this critical raw material could significantly limit the production of memory chips and exacerbate ongoing chips.

The Economic Slowdown has had a significant impact on the semiconductor memory market, with both DRAM and NAND flash revenue expected to decline in 2023. Gartner estimates that the memory market will remain flat in 2022, but is forecast to decline by 16.2% for the year 2023. And also, consumer electronics manufacturing, which are large consumers of memory chips. Inflationary and recessionary pressures have caused a significant decline in demand for computers and smartphones in 2022, affecting global manufacturers. Due to which the shipments of major electronic products will decline in the first half of 2023.

By Type

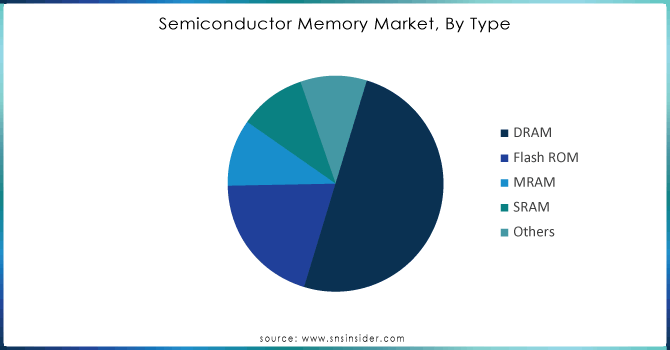

Based on Type, The DRAM segment was the market leader and accounted for more than 50% of global revenue in 2023. Dynamic Random-Access Memory, often called DRAM, plays an important role in modern computer systems due to its remarkable data access speed and responsiveness. As non-volatile solid-state memory, DRAM relies on a constant power supply to maintain stored data. As technology advances, the DRAM market remains strong, driven by growing demand for powerful computing systems, data center applications, and ever-expanding mobile devices and cloud services.

The Flash ROM segment is expected to grow at the fastest rate, growing at a CAGR of 13.8% during the forecast period 2024-2031. Flash ROM, also known as flash memory or NAND Flash, is a non-volatile semiconductor memory that can retain data even when the power supply is turned off. This feature has made it an essential part of many electronic devices, including smartphones, tablets, USB drives, digital cameras, and SSD drives.

Need any Customization as Per Your Business Requirement on Semiconductor Memory Market - Enquiry Now

By Application

Based on Application, the consumer electronics segment was the market leader and accounted for more than 30% of the global turnover in 2023. In the rapidly evolving consumer electronics environment, the demand for memory solutions that meet ever-increasing data requirements is paramount. Continuous development was characterized by the introduction of denser chips and improved memory architectures, and played a key role in meeting these growing demands. This constant evolution enables consumer electronics manufacturers to offer cutting-edge innovations and enables them to maintain a competitive edge in a fast-paced and dynamic market. In addition, the seamless integration of semiconductor chips with cloud-based services and data-driven applications has become a game changer in the consumer electronics industry.

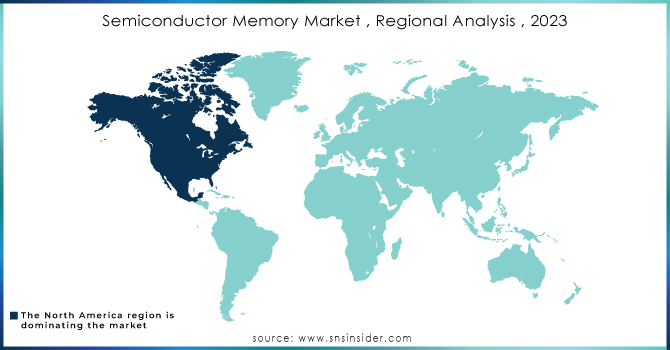

The North America is expected to grow significantly at a CAGR of 13.8%. The North American market is thriving due to the region's cutting-edge technological development. Due to the significant focus on R&D in various sectors, the demand for advanced semiconductor memory solutions is increasing, especially to support advanced applications in artificial intelligence, machine learning and data analysis. In addition, North America is an important hub for the gaming and entertainment industry, where high-performance memory is critical for delivering immersive gaming experiences and smooth content streaming. The growth of the field is further accelerated by the widespread adoption of cloud-based services and the establishment of data centres, which creates the need for advanced semiconductors that can handle the significant amount of data being produced and processed. The proliferation of self-driving vehicles and intelligent traffic systems in North America is increasing the demand for robust memory solutions that provide real-time data processing and rapid decision-making.

The Asia Pacific dominating the overall market with more than 40.0 percent market share in 2023. There are several key factors driving the market in Asia Pacific. The region is experiencing rapid economic growth with increasing consumer demand for electronic equipment. In 2023, sales of electronic devices such as laptops and smartphones exploded in the region. As a result, demand for memory-intensive products such as smartphones, tablets and smart home devices is increasing, increasing the need for advanced solid-state memory solutions. In addition, the proliferation of cloud technology and data-driven applications across various industries has increased the demand for efficient solutions that support massive computing demands. Additionally, the growth of Internet of Things (IoT) in the region is fuelling the market growth as IoT devices rely heavily on memory to store and process data. In addition, governments in several Asia Pacific countries are investing in infrastructure development, including building data centres and 5G networks, further driving demand for semiconductor memory solutions to support these initiatives.

The major key players are Samsung, IBM Corporation, TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION, Taiwan Semiconductor Manufacturing Company Limited, Integrated Silicon Solution Inc., Micron Technology, Inc, Macronix International Co., Ltd., SK HYNIX INC., Texas Instruments Incorporated, Infineon Technologies AG, Everspin Technologies, Inc., and other key players.

In May 10, 2024, Intel and UMC (United Microelectronics Corporation) announced a long-term collaboration to develop a new 12nm semiconductor process platform. This partnership leverages Intel's U.S. manufacturing capacity and UMC's foundry capabilities to address high-growth markets like mobile, networking, and communication infrastructure

In February 2023, Texas Instruments Incorporated announced that it would invest $11 billion to build its next 300 mm semiconductor wafer factory in Utah, USA. The company's goal was to expand production capacity to meet the growing demand for electronic semiconductors.

In August 2023, SK Hynix Inc. unveiled the industry's pioneering 24GB LPDDR5X DRAM mobile package, marking a significant advancement in memory technology. This cutting-edge product not only delivers superior performance but also operates with exceptional energy efficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 115.50 Billion |

| Market Size by 2032 | US$ 300.27 Billion |

| CAGR | CAGR of 11.2% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Drivers | • The growing reliance on cloud storage and big data analytics necessitates high-performance memory solutions for data centres. • The rise of AI and ML applications requires vast memory capacities for processing complex algorithms and datasets. • The proliferation of smartphones, tablets, laptops, wearables, and Internet-of-Things (IoT) devices is driving the need for more memory. |

| Restraints | • Protecting intellectual property related to advanced memory technologies is crucial, but navigating the complex global IP landscape can be challenging. • Capital-intensive Manufacturing can act as a barrier |

Ans: The expected CAGR of the Semiconductor Memory Market during the forecast period is 11.2%.

Ans: The Semiconductor Memory Market size is forecasted to surpass USD 270.0 billion by 2031.

Ans: The market is dominated by Asian companies, with key players like Samsung Electronics and SK Hynix from South Korea.

Ans: The market faces challenges like, Fluctuations in supply and demand, rising raw material costs, Geopolitical tensions impacting manufacturing.

Ans: Memory is used in various industries, including, Consumer electronics (smartphones, laptops, TVs, etc.), IT & Telecommunication (data centres, servers, networking equipment), Automotive (ADAS, self-driving cars, connected vehicles), Industrial automation, Medical devices and Aerospace & Defense.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Semiconductor Memory Market Segmentation, By Type

9.1 Introduction

9.2 Trend Analysis

9.3 SRAM

9.4 MRAM

9.5 DRAM

9.6 Flash ROM

9.7 Others

10. Semiconductor Memory Market Segmentation, By Application

10.1Introduction

10.2 Trend Analysis

10.3 Consumer Electronics

10.4 IT & Telecommunication

10.5 Automotive

10.6 Industrial

10.7 Aerospace & Defense

10.8 Medical

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Semiconductor Memory Market By Country

11.2.3 North America Semiconductor Memory Market By Type

11.2.4 North America Semiconductor Memory Market By Application

11.2.5 USA

11.2.5.1 USA Semiconductor Memory Market By Type

11.2.5.2 USA Semiconductor Memory Market By Application

11.2.6 Canada

11.2.6.1 Canada Semiconductor Memory Market By Type

11.2.6.2 Canada Semiconductor Memory Market By Application

11.2.7 Mexico

11.2.7.1 Mexico Semiconductor Memory Market By Type

11.2.7.2 Mexico Semiconductor Memory Market By Application

11.3 Europe

11.3.1 Trend Analysis

11.3.2 Eastern Europe

11.3.2.1 Eastern Europe Semiconductor Memory Market By Country

11.3.2.2 Eastern Europe Semiconductor Memory Market By Type

11.3.2.3 Eastern Europe Semiconductor Memory Market By Application

11.3.2.4 Poland

11.3.2.4.1 Poland Semiconductor Memory Market By Type

11.3.2.4.2 Poland Semiconductor Memory Market By Application

11.3.2.5 Romania

11.3.2.5.1 Romania Semiconductor Memory Market By Type

11.3.2.5.2 Romania Semiconductor Memory Market By Application

11.3.2.6 Hungary

11.3.2.6.1 Hungary Semiconductor Memory Market By Type

11.3.2.6.2 Hungary Semiconductor Memory Market By Application

11.3.2.7 Turkey

11.3.2.7.1 Turkey Semiconductor Memory Market By Type

11.3.2.7.2 Turkey Semiconductor Memory Market By Application

11.3.2.8 Rest of Eastern Europe

11.3.2.8.1 Rest of Eastern Europe Semiconductor Memory Market By Type

11.3.2.8.2 Rest of Eastern Europe Semiconductor Memory Market By Application

11.3.3 Western Europe

11.3.3.1 Western Europe Semiconductor Memory Market By Country

11.3.3.2 Western Europe Semiconductor Memory Market By Type

11.3.3.3 Western Europe Semiconductor Memory Market By Application

11.3.3.4 Germany

11.3.3.4.1 Germany Semiconductor Memory Market By Type

11.3.3.4.2 Germany Semiconductor Memory Market By Application

11.3.3.5 France

11.3.3.5.1 France Semiconductor Memory Market By Type

11.3.3.5.2 France Semiconductor Memory Market By Application

11.3.3.6 UK

11.3.3.6.1 UK Semiconductor Memory Market By Type

11.3.3.6.2 UK Semiconductor Memory Market By Application

11.3.3.7 Italy

11.3.3.7.1 Italy Semiconductor Memory Market By Type

11.3.3.7.2 Italy Semiconductor Memory Market By Application

11.3.3.8 Spain

11.3.3.8.1 Spain Semiconductor Memory Market By Type

11.3.3.8.2 Spain Semiconductor Memory Market By Application

11.3.3.9 Netherlands

11.3.3.9.1 Netherlands Semiconductor Memory Market By Type

11.3.3.9.2 Netherlands Semiconductor Memory Market By Application

11.3.3.10 Switzerland

11.3.3.10.1 Switzerland Semiconductor Memory Market By Type

11.3.3.10.2 Switzerland Semiconductor Memory Market By Application

11.3.3.11 Austria

11.3.3.11.1 Austria Semiconductor Memory Market By Type

11.3.3.11.2 Austria Semiconductor Memory Market By Application

11.3.3.12 Rest of Western Europe

11.3.3.12.1 Rest of Western Europe Semiconductor Memory Market By Type

11.3.2.12.2 Rest of Western Europe Semiconductor Memory Market By Application

11.4 Asia-Pacific

11.4.1 Trend Analysis

11.4.2 Asia Pacific Semiconductor Memory Market By Country

11.4.3 Asia Pacific Semiconductor Memory Market By Type

11.4.4 Asia Pacific Semiconductor Memory Market By Application

11.4.5 China

11.4.5.1 China Semiconductor Memory Market By Type

11.4.5.2 China Semiconductor Memory Market By Application

11.4.6 India

11.4.6.1 India Semiconductor Memory Market By Type

11.4.6.2 India Semiconductor Memory Market By Application

11.4.7 Japan

11.4.7.1 Japan Semiconductor Memory Market By Type

11.4.7.2 Japan Semiconductor Memory Market By Application

11.4.8 South Korea

11.4.8.1 South Korea Semiconductor Memory Market By Type

11.4.8.2 South Korea Semiconductor Memory Market By Application

11.4.9 Vietnam

11.4.9.1 Vietnam Semiconductor Memory Market By Type

11.4.9.2 Vietnam Semiconductor Memory Market By Application

11.4.10 Singapore

11.4.10.1 Singapore Semiconductor Memory Market By Type

11.4.10.2 Singapore Semiconductor Memory Market By Application

11.4.11 Australia

11.4.11.1 Australia Semiconductor Memory Market By Type

11.4.11.2 Australia Semiconductor Memory Market By Application

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Semiconductor Memory Market By Type

11.4.12.2 Rest of Asia-Pacific Semiconductor Memory Market By Application

11.5 Middle East & Africa

11.5.1 Trend Analysis

11.5.2 Middle East

11.5.2.1 Middle East Semiconductor Memory Market By Country

11.5.2.2 Middle East Semiconductor Memory Market By Type

11.5.2.3 Middle East Semiconductor Memory Market By Application

11.5.2.4 UAE

11.5.2.4.1 UAE Semiconductor Memory Market By Type

11.5.2.4.2 UAE Semiconductor Memory Market By Application

11.5.2.5 Egypt

11.5.2.5.1 Egypt Semiconductor Memory Market By Type

11.5.2.5.2 Egypt Semiconductor Memory Market By Application

11.5.2.5 South Africa

11.5.2.5.1 South Africa Semiconductor Memory Market By Type

11.5.2.5.2 South Africa Semiconductor Memory Market By Application

11.5.2.6 Rest of Africa

11.5.2.6.1 Rest of Africa Semiconductor Memory Market By Type

11.5.2.6.2 Rest of Africa Semiconductor Memory Market By Application

11.5.2.6 Saudi Arabia

11.5.2.6.1 Saudi Arabia Semiconductor Memory Market By Type

11.5.2.6.2 Saudi Arabia Semiconductor Memory Market By Application

11.5.2.7 Qatar

11.5.2.7.1 Qatar Semiconductor Memory Market By Type

11.5.2.7.2 Qatar Semiconductor Memory Market By Application

11.5.2.8 Rest of Middle East

11.5.2.8.1 Rest of Middle East Semiconductor Memory Market By Type

11.5.2.8.2 Rest of Middle East Semiconductor Memory Market By Application

11.5.3 Africa

11.5.3.1 Africa Semiconductor Memory Market By Country

11.5.3.2 Africa Semiconductor Memory Market By Type

11.5.3.3 Africa Semiconductor Memory Market By Application

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Semiconductor Memory Market By Country

11.6.3 Latin America Semiconductor Memory Market By Type

11.6.4 Latin America Semiconductor Memory Market By Application

11.6.5 Brazil

11.6.5.1 Brazil Semiconductor Memory Market By Type

11.6.5.2 Brazil Semiconductor Memory Market By Application

11.6.6 Argentina

11.6.6.1 Argentina Semiconductor Memory Market By Type

11.6.6.2 Argentina Semiconductor Memory Market By Application

11.6.7 Colombia

11.6.7.1 Colombia Semiconductor Memory Market By Type

11.6.7.2 Colombia Semiconductor Memory Market By Application

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Semiconductor Memory Market By Type

11.6.8.2 Rest of Latin America Semiconductor Memory Market By Application

12. Company Profiles

12.1 IBM Corporation

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 TOSHIBA ELECTRONIC DEVICES & STORAGE CORPORATION

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 Taiwan Semiconductor Manufacturing Company Limited

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Integrated Silicon Solution Inc.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Micron Technology, Inc.

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6Macronix International Co., Ltd.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 SK HYNIX INC.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8Texas Instruments Incorporated,

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Infineon Technologies AG

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Everspin Technologies, Inc.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. USE Cases and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Type

SRAM

MRAM

DRAM

Flash ROM

Others

By Application

Consumer Electronics

IT & Telecommunication

Automotive

Industrial

Aerospace & Defense

Medical

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Analog Integrated Circuit Market Size was valued at USD 79.33 billion in 2023 and is expected to reach USD 147.74 Billion by 2032 and grow at a CAGR of 7.16% over the forecast period 2024-2032.

The Traffic Sensor Market size was valued at USD 627.4 million in 2023 and is expected to grow at a CAGR of 8.5 % from 2024 to 2032, and is projected to reach US$ 1307.4 million by 2032.

The Consumer Audio Market Size was valued at USD 82.19 Billion in 2023 and is expected to grow at 14.38% CAGR to reach USD 275.36 Billion by 2032.

The LED Chip Market size was valued at USD 28.81 billion in 2023. It is expected to grow to USD 78.01 billion by 2032 and grow at a CAGR of 11.7% over the forecast period of 2024-2032.

The Holographic Display Market Size was valued at USD 2.85 Billion in 2023 and is expected to reach USD 17.71 Billion by 2032 and grow at a CAGR of 22.55% over the forecast period 2024-2032.

The Sprinkler Irrigation Market Size was valued at USD 2.43 Billion in 2023 and is expected to grow at a CAGR of 3.50% to reach USD 3.31 Billion by 2032.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd