Semiconductor Chemicals Market Size & Overview:

Get More Information on Semiconductor Chemicals Market - Request Sample Report

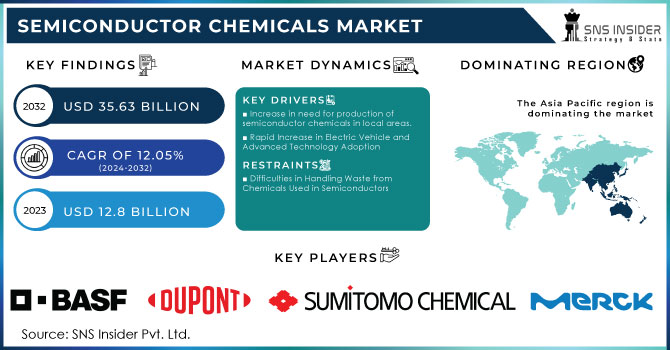

The Semiconductor Chemicals Market Size was valued at USD 12.8 Billion in 2023 and is expected to reach USD 35.63 Billion by 2032, growing at a CAGR of 12.05% during 2024-2032.

The semiconductor chemicals market is experiencing growth due to increasing demand for consumer electronics and advancements in industries like automotive, driven in part by the surge of electric vehicles (EVs). Efficient and dependable semiconductor materials, such as silicon, are essential for producing devices like smartphones, tablets, and integrated circuits.. Taiwan is crucial to this development, as Taiwan Semiconductor Manufacturing Company (TSMC) manufactures approximately half of the global microprocessor chips and leads in substantial research and development spending. The Taiwanese government's focus on the semiconductor industry as a critical economic driver is also shown through efforts such as the creation of a USD 5.4 billion fund to enhance semiconductor manufacturing capabilities. Furthermore, the rise of 5G technology and the growth of AI and IoT applications are driving the need for high-performance microprocessor chips, leading to a greater demand for advanced semiconductor chemicals. With advancements in technology and backing from government, the semiconductor chemicals market is set to experience significant growth as the industry progresses.

The growth of the semiconductor chemicals market is crucial for the broader economy, as these chemicals are essential in manufacturing products across various sectors, including healthcare, energy, agriculture, automotive, construction, and electronics. Semiconductor production relies heavily on ultra-pure electronic chemicals, which are known for their stringent purity requirements, often measured in parts per billion (ppb) or parts per trillion (ppt) levels of metal content and moisture. With over 250 chemicals utilized in semiconductor fabrication, key materials include hydrochloric acid, sulfuric acid, hydrofluoric acid, nitric acid, and several organic compounds. While multinational corporations lead the electronic chemicals sector, India is emerging with specialty manufacturers capable of meeting semiconductor manufacturing standards, although its current production has been limited due to lower demand. However, advancements in the semiconductor industry and government initiatives, such as Production-Linked Incentive (PLI) schemes, are set to significantly increase demand for electronic chemicals in India. To capitalize on this growth, Indian manufacturers must enhance their infrastructure and workforce capabilities. Achieving ultra-pure standards requires a blend of scientific precision and cultural transformation, emphasizing metal content control from raw material sourcing to production environments, including clean rooms that adhere to strict ISO classifications. Maintaining optimal conditions in these controlled environments is critical to prevent contamination, utilizing advanced filtration systems and specialized cleaning protocols. The establishment of electronic chemicals qualification labs in India is imperative to ensure adherence to global quality standards, facilitating collaboration between local manufacturers and international companies. by enhancing local capabilities and fostering a culture of continuous improvement, India can position itself as a competitive player in the global semiconductor chemicals market, which is integral to the success of the semiconductor industry as a whole.

Semiconductor Chemicals Market Dynamics

Drivers

-

Increase in need for production of semiconductor chemicals in local areas.

There is a growing demand in the semiconductor chemicals industry due to the requirement for local production of specialty gases and chemicals. With substantial investments from top companies, the demand for top-notch electronic chemicals has become more and more crucial as semiconductor production quickly grows in North America. Setting up production sites in the local area enables companies to quickly adjust to the changing demands of the semiconductor sector, guaranteeing a consistent availability of important substances such as fluorochemicals and rare gases such as krypton, xenon, and neon. This shift towards localized chemical manufacturing not only cuts down on lead times and transportation expenses but also enhances supply chain resilience, crucial for meeting stringent purity and quality demands in semiconductor production. The recent news about a significant USD 210 million investment in a new semiconductor chemicals facility in Texas showcases the trend of companies preparing to take advantage of the growing demand for specialty chemicals produced locally. This plant will produce important fluorinated chemicals and supply necessary noble gases, enhancing the strength of the distribution network. The timing is important, as shown by the semiconductor industry's continuing large investments, such as a USD 45 billion pledge for chip production in Texas. by setting up manufacturing facilities close to important semiconductor centers, companies are ready to enhance their market position and satisfy the increasing need for essential electronic chemicals used in advanced chip production, leading to significant growth in the semiconductor chemicals market.

-

Rapid Increase in Electric Vehicle and Advanced Technology Adoption

The rapid uptake of electric vehicles and advanced technologies in different industries is a crucial factor driving the semiconductor chemicals sector. The increasing global sales of electric vehicles surpassed 10 million units in 2022 and are expected to reach 14 million units in the current year, indicating a significant change in the automotive industry. The demand for advanced semiconductor components is increasing as electric vehicles' market share grows from about 4% in 2020 to an expected 18% this year. Chemicals used in semiconductors are essential for creating components that enable technologies like self-driving cars, advanced entertainment systems, and connected car functionalities. The fast-paced technological advancements in the automotive industry highlight the dependence on semiconductor chemicals and also offer substantial growth prospects in the market. The growing incorporation of advanced electronics in cars demands top-notch semiconductor materials that adhere to strict purity requirements, pushing manufacturers to improve their production capacities. As a result, the increase in electric vehicles and the wider use of technology in different industries are key elements driving the expansion of the semiconductor chemicals market, indicating a strong need for creative solutions in semiconductor production.

Restraints

-

Difficulties in Handling Waste from Chemicals Used in Semiconductors

Effectively dealing with the waste produced by semiconductor chemicals is a major task that involves significant complexities and potential dangers, requiring cautious handling to safeguard the environment and public health. The careless management, storage, or disposal of various chemicals used in semiconductor production can pose serious risks due to their hazardous and toxic nature. Polluting soil, water, and air with these substances presents significant dangers to workers, nearby communities, and ecosystems. Information from the World Counts website shows a massive surge in the generation of dangerous waste, escalating from 1 million tons in 1930 to around 400 million tons by 2000, indicating a significant 40,000% increase within one generation. This concerning pattern of increasing hazardous waste production poses important sustainability and environmental impact concerns, particularly within the semiconductor chemicals sector. With the increasing demand for semiconductor chemicals due to technological advancements and the growth of the electric vehicle industry, the importance of efficient waste management strategies is on the rise. Businesses in this industry need to focus on creating sustainable practices and technologies to reduce the risks related to dangerous waste, making sure they follow environmental laws and safeguard public health and the environment.

Semiconductor Chemicals Market - Segment Outlook

by Type

Based On Type, Acid & Base Chemicals is captured the largest share revenue in Semiconductor Chemicals Market with 39.44% in 2023 .Their main dominance stems from their crucial involvement in a range of semiconductor manufacturing procedures, such as wafer cleaning, etching, and doping, where maintaining high levels of purity is vital. Big companies in the industry are concentrating on developing products and innovating to improve what they provide. As an example, a top chemical producer recently introduced a new range of highly pure hydrofluoric acid and sulfuric acid, specifically designed for advanced semiconductor uses. This product not just fulfills strict purity criteria but also enhances efficiency in processes. Moreover, a different important contributor brought forth a new pH-neutral etching solution that reduces defects in semiconductor manufacturing, further emphasizing the significance of acid and base compounds in attaining top-notch results. Moreover, continuous R&D investments are anticipated to fuel progress in acid and base chemical formulations, meeting the changing requirements of semiconductor makers. The increasing popularity of artificial intelligence (AI) and the Internet of Things (IoT) is expected to boost the demand for these chemicals, further establishing their important role in the semiconductor chemicals market.

by End-Use

Based on End-Use, Integrated Circuits (ICS) is captured the largest share revenue in Semiconductor Chemicals with 49.22% in 2023. The demand for ICs across different applications, such as consumer electronics, automotive systems, and telecommunications, is a major factor behind this prominence. Key companies in the semiconductor chemicals industry are heavily engaging in R&D to satisfy the strict demands of IC production. For instance, a well-known chemical supplier recently introduced a new series of high-purity photoresists tailored for advanced IC lithography processes, helping manufacturers achieve better resolutions and performance enhancements. In addition, another prominent company unveiled new dielectric materials that improve the electrical characteristics of ICs, guaranteeing improved energy efficiency and functionality. The continuous development of technology, like 5G and artificial intelligence, is projected to increase the requirement for high-performance ICs, leading to a growing need for specialized semiconductor chemicals. Moreover, partnerships between semiconductor producers and chemical firms are promoting the creation of specialized chemical products, guaranteeing the growth of the integrated circuit sector in a constantly changing market environment. The significance of ICs in the semiconductor chemicals market is crucial as they form the basis of modern electronic devices.

Semiconductor Chemicals Market - Regional Analysis

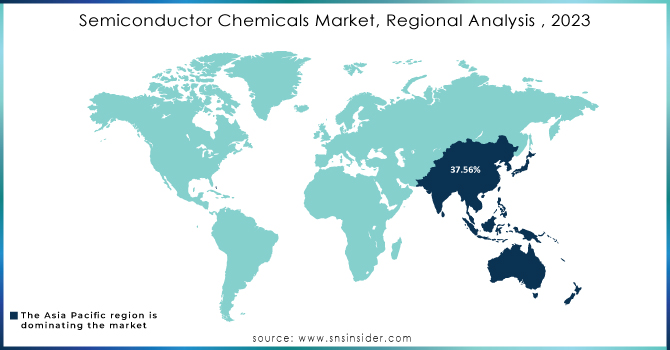

In 2023, the semiconductor chemicals market in the Asia-Pacific region accounted for a leading 37.56% market share due to sustained growth, technological progress, and a focus on meeting the increasing demand for semiconductor materials in different industries. This area is a major player in manufacturing silicon-based microprocessor chips, having a significant impact on the worldwide semiconductor industry. The strong position of South Korea, Japan, and Taiwan in semiconductor production has enhanced the region's leadership. Significantly, China's semiconductor chemicals market ranked second in Asia-Pacific largely due to strong government efforts to support the microprocessor chips sector. The strategic goals of the central government, like the Made in China 2025 campaign, aim to boost domestic semiconductor manufacturing and decrease dependence on international suppliers. The China Semiconductor Application Association forecasts that the semiconductor market in China will hit $300 billion by 2025, showcasing its strong position in the global market. Additionally, the government's funding for research and development, along with rewards for semiconductor firms, is projected to stimulate the expansion of the microprocessor sector.

In 2023, North America became the quickest-growing region in the semiconductor chemicals market due to substantial investments in local semiconductor manufacturing and technological progress. The United States, in particular, has given importance to the semiconductor industry with the CHIPS and Science Act, which provides billions to enhance local manufacturing and creativity. This new initiative has caused a rise in the need for semiconductor chemicals crucial for making chips. Large corporations like Dow Inc. and Air Products and Chemicals, Inc. have taken strategic actions by introducing new and innovative products specifically designed for the changing demands of the semiconductor sector. In 2023, Dow launched a new collection of high-performance dielectric materials aimed at improving the performance and reliability of semiconductor devices, as Air Products also revealed upgraded specialty gases for etching and deposition techniques. In addition, Intel has increased its endeavors to construct advanced manufacturing plants in various locations in the United States, necessitating a reliable source of semiconductor chemicals. These efforts highlight North America's dedication to enhancing its semiconductor supply chain and safeguarding against worldwide disruptions.

Need Any Customization Research On Semiconductor chemical Market - Inquiry Now

Key Players

Some of Major players in Semiconductor chemical Market who provide product and offering:

-

BASF SE (Electronic materials for semiconductor manufacturing, including ultra-pure chemicals and gases)

-

DuPont (Advanced photoresists and electronic materials)

-

Sumitomo Chemical Co., Ltd. (Photoresists, chemical mechanical planarization (CMP) slurries)

-

Merck KGaA (Specialty chemicals for semiconductor lithography and patterning)

-

Linde PLC (High-purity gases like argon, hydrogen, and nitrogen for semiconductor manufacturing)

-

Avantor, Inc. (High-purity process chemicals and solutions for semiconductor fabrication)

-

Air Liquide (Specialty gases like fluorine and nitrogen trifluoride for semiconductor etching)

-

Kanto Chemical Co., Inc. (High-purity chemicals for etching and cleaning semiconductor wafers)

-

JSR Corporation (Photoresists and CMP materials for semiconductor lithography)

-

Cabot Microelectronics (CMP slurries and polishing pads)

-

Entegris, Inc. (Advanced filtration and purification solutions for semiconductor processes)

-

Hitachi Chemical Co., Ltd. (CMP slurries and other chemical solutions for wafer processing)

-

Fujifilm Holding Corporation (Photoresists and high-performance chemical solutions)

-

Mitsubishi Chemical Corporation (Specialty chemicals for semiconductor processing)

-

Honeywell International Inc. (High-purity chemicals and gases for semiconductor manufacturing)

-

Others

Recent Development

-

In August 2023, BASF expanded the electronic materials R&D center in Asia Pacific to its facility in Ansan, South Korea. The new, larger facility focuses on engineering plastics and semiconductor materials, catering to local and global customers

-

In January 2023, JSR Corp. acquired additional shares of JSR Electronic Materials Korea Co., Ltd., its Korean subsidiary. The move helped JSR solidify its global position in the semiconductor chemicals business and expand its type portfolio

-

On August 2024, JSR Corporation announced plans to expand its global development and production of leading-edge photoresists by establishing a new R&D base in Japan and constructing a semiconductor photoresist plant at its subsidiary JSR Micro Korea Co., Ltd. (JMK).

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 12.8 Billion |

| Market Size by 2032 | USD 35.63 Billion |

| CAGR | CAGR of 12.05% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (High Performance Polymers ,Acid & Base Chemicals ,Adhesives,Solvents , Others) • By End-Use (Integrated Circuits (ICS) ,Discrete Semiconductor ,Optoelectronics , Sensors • By Application (Photoresist ,Etching, Deposotion, Cleaning, Doping, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, DuPont, Sumitomo Chemical Co., Ltd., Merck KGaA, Linde PLC, Avantor, Inc., Air Liquide, Kanto Chemical Co., Inc., JSR Corporation, Cabot Microelectronics, Entegris, Inc., Hitachi Chemical Co., Ltd., Fujifilm Holding Corporation, Mitsubishi Chemical Corporation, and Honeywell International Inc. & Others |

| Key Drivers | • Increase in need for production of semiconductor chemicals in local areas. • Rapid Increase in Electric Vehicle and Advanced Technology Adoption |

| RESTRAINTS | • Difficulties in Handling Waste from Chemicals Used in Semiconductors |