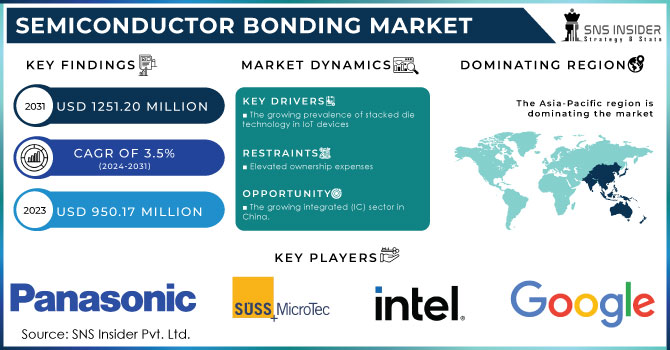

The Semiconductor Bonding Market Size was valued at USD 905.71 Million in 2023 and is expected to reach USD 1239.97 Million by 2032 and grow at a CAGR of 3.57% over the forecast period 2024-2032.

The Semiconductor Bonding Market has really gained significant momentum during 2023 and 2024 driven by government initiatives, technological innovations, and increasing adoption in different sectors. Meanwhile, governments across the world have made investing in semiconductor manufacturing a high priority through specific policies, including the U.S. CHIPS Act and Europe's "Digital Compass" program, aimed at revitalizing domestic production capabilities. Similarly, Asian economies, led by China, Japan, and South Korea, are heavily investing in semiconductor infrastructure to strengthen their supply chains. The advancement of technologies such as the introduction of advanced die-attach bonding and wafer bonding solutions have increased precision and efficiency to address the growing demand for compact, high-performance devices.

Get more information on Semiconductor Bonding Market - Request Sample Report

In 2023, the world saw significant announcements from leading industrial players. Notable examples were hybrid bonding technologies and advanced adhesives which addressed needs related to automotive applications and telecommunication. Hybrid bonding, for instance, supports next-generation applications and allows for the creation of very high-density interconnects together with better electrical performance. BE Semiconductor Industries anticipates increased demand for its hybrid bonding systems in 2025 due to shipment delays experienced in the fourth quarter, stated the chip components supplier, after the third-quarter new orders fell short of projections.

New developments in the field of wafer bonding facilitate the integration of 3D-integrated circuits by satisfying the continually increasing need for miniaturization and energy efficiency. The importance of semiconductor bonding in advancing electronics manufacturing will be ever more pivotal as industries adopt these technologies.

Future growth opportunities lie ahead in artificial intelligence, 5G, and Internet of Things applications that demand high-speed and energy-efficient semiconductor solutions. Applications for AI-powered autonomous vehicles and robotics will require advanced bonding for the performance necessary to achieve real-time data processing. In a similar manner, the growth of 5G infrastructure has expedited the demand for semiconductor bonding in high-frequency devices and power amplifiers. Furthermore, the projected installation of more than 20 billion IoT devices worldwide by 2025 underscores the critical role of bonding technologies in making smart, connected ecosystems possible.

Moreover, the statistics from both the industry and the government underpin the importance of semiconductor bonding to fulfill the demands of the rapidly changing technological world. It emphasizes that this technology has increasing relevance across different applications and will continue to grow with government and private sectors collaboration, innovation, and stability in supply chains. Bonding technologies in the semiconductor industry will be a vital aspect of continued development, ensuring challenges such as scalability, reliability, and sustainability, but unlocking growth opportunities.

KEY DRIVERS:

Rising Adoption of AI and IoT Technologies Drives Demand For Semiconductors.

In 2023, almost all of the IoT devices required advanced semiconductor bonding processes to provide enhanced functionality and durability. The need for AI-based applications like autonomous vehicles and smart home systems has necessitated compact, high-performance chips, prompting manufacturers to take on cutting-edge bonding technologies. Governments have also played a significant role, with initiatives such as South Korea's investment of USD 450 billion in semiconductor R&D by 2030, which emphasizes the importance of the sector.

IoT installations worldwide reached over 15 billion devices in 2023 and are expected to increase by 20% in 2024. The reliance of these technologies on accurate bonding techniques indicates the potential for growth in the market, given the growing need for efficiency, miniaturization, and energy optimization in semiconductor manufacturing.

Semiconductor Bonding Innovation Is On The Rise As More Electric Vehicle Manufacturing Takes Place.

Electric vehicles, which were rapidly adopted at 35% year-over-year in 2023, saw global production of more than one-third increase with generous incentives by governments. The European Union allocated a total of €20 billion in funding to promote electric vehicle infrastructure development and pointed out semiconductor reliability and efficiency. Power modules and battery management systems are the backbone of EVs, and die bonding technology plays a significant role in enhancing their performance.

The ability of bonding solutions to handle high thermal and electrical conductivity is critical because the energy efficiency and safety of EVs are of utmost importance to manufacturers. Advanced bonding techniques are expected to be used in more than 70% of EV components by 2024, making it a critical driver of the semiconductor bonding market.

RESTRAIN:

High Costs Associated With Advanced Semiconductor Bonding Technologies.

Higher costs of advanced bonding technologies are a major challenge for the semiconductor bonding industry. As manufacturers move toward hybrid and wafer-level bonding technologies, the costs are much more in terms of R&D, equipment costs, and experienced labor costs. For instance, the average price of wafer bonding equipment has increased about 25% for the year 2023 in comparison with the previous year. SMEs make up the bulk of the supply chain, but are unable to invest in such technologies due to lack of capital.

The government also, though slowly increasing its efforts, is only concentrating on large-scale projects, thereby making the smaller players fall behind. Such a cost barrier prevents mass adaptation, especially in regions where semiconductor industries are developing. Industry players are, however, seeking collaborative R&D and cost-sharing models, though the financial strain remains one of the major constraints to the growth of the market.

BY BONDING TECHNOLOGY

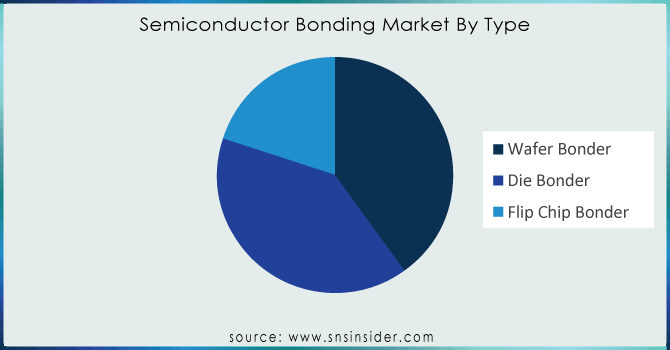

In 2023, Die Bonding Technology segment was found to be the most dominant, holding 67% of the market share. In the automotive, telecommunication, and consumer electronics space, the precision and reliability offered by die bonding technology are a must-have.

In this segment, it finds popularity because of its ability to handle high-performance requirements and advanced packaging needs-essential requirements for compact yet energy-efficient devices. Moreover, some leading-edge innovations, such as hybrid bonding, continue to be integrated into die bonding, making it an even more popular alternative among manufacturers.

In terms of growth, the Die Bonding Technology segment is expected to be the fastest growing with a CAGR of 3.60% during the forecast period from 2024 to 2032. The high demand for high-performance computing, 5G, and AI applications points to the segment's critical role in shaping the future of semiconductor bonding technologies.

BY APPLICATION

In 2023, the dominant segment was CMOS Image Sensors, which managed to capture 28% of the market share. This can be attributed to the increasingly observed adoption of CMOS sensors in smartphones, surveillance systems, and automotive cameras. These sensors have earned a huge following for providing high-resolution images with minimal power consumption.

On the other hand, the MEMS and Sensors segment is expected to grow with the fastest CAGR of 3.95% from 2024 to 2032. The versatility of MEMS devices, ranging from pressure sensors to accelerometers, is driving their demand across automotive, healthcare, and industrial sectors. Advancements in semiconductor bonding techniques are also enabling manufacturers to produce smaller, more efficient MEMS devices, making this segment a key growth driver for the overall market.

The Asia Pacific region was the largest contributor to the semiconductor bonding market in 2023, holding 43% of the market share. The dominance of this region is because of strong semiconductor manufacturing ecosystems in countries such as China, South Korea, and Taiwan, which contribute a significant percentage of the world's chip production. The government also is putting efforts, like China, which has committed USD 150 billion for semiconductor infrastructure by 2030, which will further enhance the position of the region. The growing demand for consumer electronics and automotive applications is also driving the market.

In the future, the Asia Pacific region is expected to grow at the highest CAGR of 3.69% during the forecast period from 2024 to 2032. Advancements in bonding technologies, increased foreign investments, and expanding production capacities are some of the factors that underscore the region's potential to drive the future of the Semiconductor Bonding Market.

Get Customized Report as per your Business Requirement - Request For Customized Report

Some of the major players in the Semiconductor Bonding Market are

ASM Pacific Technology (Wafer Bonder, Die Bonder)

Kulicke & Soffa (Flip Chip Bonder, Wire Bonder)

Besi (Die Attach Equipment, Flip Chip Bonder)

TDK Corporation (MEMS Bonding Tools, Wafer Process Equipment)

Panasonic Corporation (Semiconductor Bonding Machines, Die Bonder)

SUSS MicroTec (Wafer Bonding Systems, Lithography Systems)

Mycronic AB (Die Attach Systems, Flip Chip Systems)

Shinkawa Ltd. (Die Bonding Equipment, Flip Chip Bonding Systems)

Palomar Technologies (Die Bonders, Wire Bonding Equipment)

Advantest Corporation (Semiconductor Test Systems, Bonding Equipment)

Nordson Corporation (Plasma Treatment Systems, Dispensing Equipment)

Hesse Mechatronics (Ultrasonic Bonding Systems, Wire Bonders)

F&K Delvotec (Wire Bonding Machines, Die Attach Systems)

Hybond (Manual Wire Bonders, Semi-Automatic Die Bonders)

West-Bond Inc. (Semiconductor Bonders, Ball Bonders)

Mitsubishi Electric (Semiconductor Bonding Machines, Wafer Bonding Equipment)

Esec (Flip Chip Bonding Equipment, Die Bonding Machines)

MRSI Systems (Die Bonding Systems, Eutectic Bonding Systems)

Toray Engineering (Wafer Bonders, MEMS Bonding Systems)

Tokyo Electron (Semiconductor Manufacturing Equipment, Bonding Machines)

Dow Inc. (Epoxy Resins, Die Attach Materials)

Henkel AG & Co. KGaA (Adhesives, Semiconductor Bonding Materials)

3M (Thermal Interface Materials, Bonding Films)

Shin-Etsu Chemical Co. (Silicone Materials, Wafer Bonding Compounds)

Momentive Performance Materials (Advanced Adhesives, Encapsulation Materials)

Dupont (Semiconductor Dielectrics, Bonding Films)

Wacker Chemie AG (Silicones, Polymer Bonding Agents)

BASF SE (Chemicals for Wafer Processing, Bonding Compounds)

Hitachi Chemical Co. (Semiconductor Materials, Die Attach Pastes)

Indium Corporation (Solder Paste, Thermal Interface Materials)

Intel Corporation

Samsung Electronics

Taiwan Semiconductor Manufacturing Company (TSMC)

Qualcomm Inc.

Broadcom Inc.

Nvidia Corporation

Apple Inc.

Micron Technology

Advanced Micro Devices (AMD)

Sony Semiconductor Solutions

November 2024: ASM Pacific Technology and IBM have announced a renewed agreement to extend their collaboration on the joint development of the next advancement of chiplet packaging technologies. The two companies will collaborate under the agreement to advance thermocompression and hybrid bonding technology for chiplet packages, using ASM Pacific Technology's next generation of Firebird TCB and Lithobolt hybrid bonding tools.

July 2024: Kulicke and Soffa Industries Inc. in partnership with ROHM Co. Ltd. has come up with a new route to hybrid bonding by harnessing its Fluxless Thermo-Compression FTC process. Technology innovations from ROHM combined with Kulicke & Soffa's recently launched APTURA FTC system have enabled improved chip-to-wafer hybrid bonding with the innovative copper-first, CuFirst, hybrid solution.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 905.71 Million |

|

Market Size by 2032 |

USD 1239.97 Million |

|

CAGR |

CAGR of 3.57 % From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Type (Wafer Bonder, Die Bonder, Flip Chip Bonder) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

ASM Pacific Technology, Kulicke & Soffa, Besi, TDK Corporation, Panasonic Corporation, SUSS MicroTec, Mycronic AB, Shinkawa Ltd., Palomar Technologies, Advantest Corporation, Nordson Corporation, Hesse Mechatronics, F&K Delvotec, Hybond, West-Bond Inc., Mitsubishi Electric, Esec, MRSI Systems, Toray Engineering, Tokyo Electron. |

|

Key Drivers |

• Rising Adoption of AI and IoT Technologies Drives Demand For Semiconductors. |

|

Restraints |

• High Costs Associated With Advanced Semiconductor Bonding Technologies. |

Ans: Asia Pacific dominated the Semiconductor Bonding Market in 2023.

Ans: The Die Bonding Technology segment dominated the Semiconductor Bonding Market.

Ans: The major growth factors of the Semiconductor Bonding Market are Rising Adoption of AI and IoT Technologies as well as Electric Vehicle Manufacturing.

Ans: Semiconductor Bonding Market size was USD 905.71 Million in 2023 and is expected to Reach USD 1239.97 Million by 2032.

Ans: The Semiconductor Bonding Market is expected to grow at a CAGR of 3.57% during 2024-2032.

TABLE OF CONTENT

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Key Vendors and Feature Analysis, 2023

5.2 Performance Benchmarks, 2023

5.3 Integration Capabilities

5.4 Usage Statistics, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Semiconductor Bonding Market Segmentation, By Type

7.1 Chapter Overview

7.2 Wafer Bonder

7.2.1 Wafer Bonder Market Trends Analysis (2020-2032)

7.2.2 Wafer Bonder Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 Die Bonder

7.3.1 Die Bonder Market Trends Analysis (2020-2032)

7.3.2 Die Bonder Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 Flip Chip Bonder

7.4.1 Flip Chip Bonder Market Trends Analysis (2020-2032)

7.4.2 Flip Chip Bonder Market Size Estimates and Forecasts to 2032 (USD Million)

8. Semiconductor Bonding Market Segmentation, by Application

8.1 Chapter Overview

8.2 RF Devices

8.2.1 RF Devices Market Trends Analysis (2020-2032)

8.2.2 RF Devices Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 MEMS and Sensors

8.3.1 MEMS and Sensors Market Trends Analysis (2020-2032)

8.3.2 MEMS and Sensors Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 LED

8.4.1 LED Market Trends Analysis (2020-2032)

8.4.2 LED Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 3D NAND

8.5.1 3D NAND Market Trends Analysis (2020-2032)

8.5.2 3D NAND Market Size Estimates and Forecasts to 2032 (USD Million)

8.6 CMOS Image Sensors

8.6.1 CMOS Image Sensors Market Trends Analysis (2020-2032)

8.6.2 CMOS Image Sensors Market Size Estimates And Forecasts To 2032 (USD Million)

9. Semiconductor Bonding Market Segmentation, By Process Type

9.1 Chapter Overview

9.2 Die-To Wafer Bonding

9.2.1 Die-To Wafer Bonding Market Trends Analysis (2020-2032)

9.2.2 Die-To Wafer Bonding Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Die-To Die Bonding

9.3.1 Die-To Die Bonding Market Trends Analysis (2020-2032)

9.3.2 Die-To Die Bonding Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Wafer-To-Wafer Bonding

9.4.1 Wafer-To-Wafer Bonding Market Trends Analysis (2020-2032)

9.4.2 Wafer-To-Wafer Bonding Market Size Estimates and Forecasts to 2032 (USD Million)

10. Semiconductor Bonding Market Segmentation, By Bonding Technology

10.1 Chapter Overview

10.2 Die Bonding Technology

10.2.1 Die Bonding Technology Market Trends Analysis (2020-2032)

10.2.2 Die Bonding Technology Market Size Estimates and Forecasts to 2032 (USD Million)

10.3 Wafer Bonding Technology

10.3.1 Wafer Bonding Technology Market Trends Analysis (2020-2032)

10.3.2 Wafer Bonding Technology Market Size Estimates and Forecasts to 2032 (USD Million)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.2.3 North America Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.2.4 North America Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.2.5 North America Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.2.6 North America Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.2.7 USA

11.2.7.1 USA Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.2.7.2 USA Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.2.7.3 USA Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.2.7.4 USA Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.2.8 Canada

11.2.8.1 Canada Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.2.8.2 Canada Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.2.8.3 Canada Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.2.8.4 Canada Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.2.9 Mexico

11.2.9.1 Mexico Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.2.9.2 Mexico Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.2.9.3 Mexico Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.2.9.4 Mexico Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.1.3 Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.4 Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.5 Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.6 Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.1.7 Poland

11.3.1.7.1 Poland Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.7.2 Poland Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.7.3 Poland Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.7.4 Poland Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.1.8 Romania

11.3.1.8.1 Romania Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.8.2 Romania Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.8.3 Romania Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.8.4 Romania Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.9.2 Hungary Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.9.3 Hungary Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.9.4 Hungary Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.10.2 Turkey Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.10.3 Turkey Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.10.4 Turkey Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.1.11.2 Rest of Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.1.11.3 Rest of Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.1.11.4 Rest of Eastern Europe Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.2.3 Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.4 Western Europe Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.5 Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.6 Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.7 Germany

11.3.2.7.1 Germany Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.7.2 Germany Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.7.3 Germany Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.7.4 Germany Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.8 France

11.3.2.8.1 France Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.8.2 France Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.8.3 France Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.8.4 France Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.9 UK

11.3.2.9.1 UK Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.9.2 UK Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.9.3 UK Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.9.4 UK Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.10 Italy

11.3.2.10.1 Italy Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.10.2 Italy Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.10.3 Italy Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.10.4 Italy Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.11 Spain

11.3.2.11.1 Spain Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.11.2 Spain Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.11.3 Spain Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.11.4 Spain Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.12.2 Netherlands Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.12.3 Netherlands Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.12.4 Netherlands Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.13.2 Switzerland Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.13.3 Switzerland Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.13.4 Switzerland Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.14 Austria

11.3.2.14.1 Austria Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.14.2 Austria Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.14.3 Austria Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.14.4 Austria Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.3.2.15.2 Rest of Western Europe Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.3.2.15.3 Rest of Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.3.2.15.4 Rest of Western Europe Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.4.3 Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.4 Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.5 Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.6 Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.7 China

11.4.7.1 China Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.7.2 China Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.7.3 China Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.7.4 China Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.8 India

11.4.8.1 India Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.8.2 India Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.8.3 India Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.8.4 India Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.9 Japan

11.4.9.1 Japan Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.9.2 Japan Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.9.3 Japan Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.9.4 Japan Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.10 South Korea

11.4.10.1 South Korea Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.10.2 South Korea Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.10.3 South Korea Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.10.4 South Korea Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.11 Vietnam

11.4.11.1 Vietnam Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.11.2 Vietnam Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.11.3 Vietnam Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.11.4 Vietnam Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.12 Singapore

11.4.12.1 Singapore Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.12.2 Singapore Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.12.3 Singapore Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.12.4 Singapore Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.13 Australia

11.4.13.1 Australia Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.13.2 Australia Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.13.3 Australia Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.13.4 Australia Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.4.14.2 Rest of Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.4.14.3 Rest of Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.4.14.4 Rest of Asia Pacific Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.1.3 Middle East Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.4 Middle East Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.5 Middle East Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.6 Middle East Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.1.7 UAE

11.5.1.7.1 UAE Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.7.2 UAE Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.7.3 UAE Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.7.4 UAE Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.8.2 Egypt Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.8.3 Egypt Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.8.4 Egypt Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.9.2 Saudi Arabia Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.9.3 Saudi Arabia Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.9.4 Saudi Arabia Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.10.2 Qatar Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.10.3 Qatar Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.10.4 Qatar Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.1.11.2 Rest of Middle East Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.1.11.3 Rest of Middle East Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.1.11.4 Rest of Middle East Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.2.3 Africa Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.2.4 Africa Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.2.5 Africa Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.2.6 Africa Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.2.7.2 South Africa Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.2.7.3 South Africa Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.2.7.4 South Africa Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.2.8.2 Nigeria Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.2.8.3 Nigeria Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.2.8.4 Nigeria Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.5.2.9.2 Rest of Africa Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.5.2.9.3 Rest of Africa Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.5.2.9.4 Rest of Africa Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Semiconductor Bonding Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.6.3 Latin America Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.6.4 Latin America Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.6.5 Latin America Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.6.6 Latin America Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.6.7 Brazil

11.6.7.1 Brazil Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.6.7.2 Brazil Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.6.7.3 Brazil Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.6.7.4 Brazil Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.6.8 Argentina

11.6.8.1 Argentina Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.6.8.2 Argentina Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.6.8.3 Argentina Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.6.8.4 Argentina Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.6.9 Colombia

11.6.9.1 Colombia Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.6.9.2 Colombia Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.6.9.3 Colombia Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.6.9.4 Colombia Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Semiconductor Bonding Market Estimates and Forecasts, By Type (2020-2032) (USD Million)

11.6.10.2 Rest of Latin America Semiconductor Bonding Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

11.6.10.3 Rest of Latin America Semiconductor Bonding Market Estimates and Forecasts, By Process Type (2020-2032) (USD Million)

11.6.10.4 Rest of Latin America Semiconductor Bonding Market Estimates and Forecasts, By Bonding Technology (2020-2032) (USD Million)

12. Company Profiles

12.1 ASM Pacific Technology

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Kulicke & Soffa

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Besi

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 TDK Corporation

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Panasonic Corporation

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 SUSS MicroTec

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Mycronic AB

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Shinkawa Ltd.

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Palomar Technologies

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Advantest Corporation

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

BY TYPE

Wafer Bonder

Die Bonder

Flip Chip Bonder

BY PROCESS TYPE

Die-To-Wafer Bonding

Die-To-Die Bonding

Wafer-To-Wafer Bonding

BY BONDING TECHNOLOGY

Die Bonding Technology

Wafer Bonding Technology

BY APPLICATION

RF Devices

MEMS and Sensors

LED

CMOS Image Sensors

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Washing Machine Market Size was valued at USD 62.22 Billion in 2023 and is expected to reach USD 117.54 Billion by 2032 and grow at a CAGR of 7.4% over the forecast period 2024-2032.

The Automatic number plate recognition (ANPR) System Market Size was valued at USD 3.20 Billion in 2023 and is expected to grow at a CAGR of 9.10% to reach USD 7.00 Billion by 2032.

The 3D Display Market Size was valued at USD 123.17 Billion in 2023 and is expected to grow at a CAGR of 18.39% to reach USD 561.50 Billion by 2032.

The Smart Advertising Market Size was valued at USD 1.64 billion in 2023 and is expected to grow at a CAGR of 11.50% to reach USD 4.36 billion by 2032.

The Semiconductor Assembly and Packaging Services Market size was valued at USD 18.78 Billion in 2023 and expected to reach USD 35.04 Billion by 2032 with a growing CAGR of 7.19% over the forecast period 2024-2032.

The Analog Semiconductor Market Size was valued at USD 88.65 Billion in 2023 and is expected to reach USD 156.4 Billion, at a CAGR of 6.52% During 2024-2032

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd