Semiconductor Back-End Equipment Market Size

Get More Information on Semiconductor Back-End Equipment Market - Request Sample Report

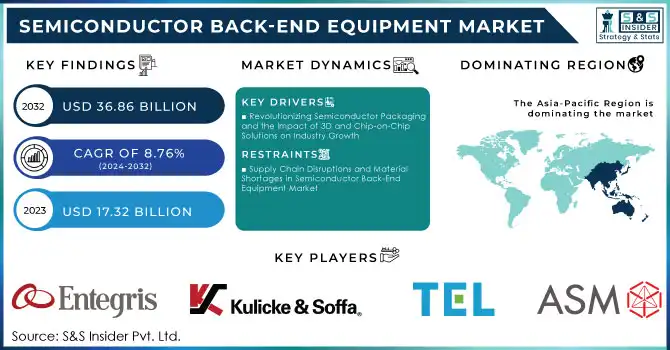

The Semiconductor Back-End Equipment Market Size was valued at USD 17.32 Billion in 2023, and is expected to reach USD 36.86 Billion by 2032, and grow at a CAGR of 8.76% over the forecast period 2024-2032.

The semiconductor back-end equipment market is experiencing significant growth, driven by the rising demand for advanced semiconductors needed for applications such as artificial intelligence (AI), 5G, and the Internet of Things (IoT). As industries push for smaller, more powerful chips, the market for advanced packaging and assembly technologies is expanding rapidly. Innovations like 3D packaging, System-in-Package (SiP), and chip-on-chip solutions are becoming essential to meet the demands of high-performance computing. Companies such as AMD and Intel are heavily investing in developing AI-driven chip technologies, propelling growth in the back-end equipment market. This growth is also fueled by the increasing importance of high-purity quartz, a critical material for chip production, which is facing rising prices due to supply chain pressures. The price of high-purity quartz has surged, with some grades reaching over USD 5,000 per ton, further driving the demand for cutting-edge back-end equipment. Asia Pacific continues to dominate the global market, with countries like China and Japan leading the charge in semiconductor production. As the semiconductor industry continues to evolve, particularly in areas like AI, autonomous systems, and high-performance computing, the semiconductor back-end equipment market is poised for substantial growth, with both technological advancements and rising production demands driving future trends.

The semiconductor industry is undergoing significant transformation, driven by advancements in energy transition, electrification, and AI. AI-powered chips are now at the forefront, enabling innovations in self-driving cars and real-time healthcare monitoring, thereby reshaping technology development. Moreover, as the world shifts towards renewable energy, semiconductors play a crucial role in electrification, powering smarter solar energy storage and electric vehicle charging systems. However, rising equipment costs may hinder market growth, as they directly impact semiconductor production costs. Macroeconomic uncertainty and reduced consumer spending are additional challenges, potentially decreasing demand for semiconductors in consumer electronics.

Semiconductor Back-End Equipment Market Dynamics

Drivers

- Revolutionizing Semiconductor Packaging and the Impact of 3D and Chip-on-Chip Solutions on Industry Growth

Technological advancements in semiconductor packaging, particularly with techniques like 3D packaging and chip-on-chip solutions, are driving substantial innovation across the industry. These cutting-edge methods enable the integration of multiple chips within a single package, improving performance while reducing space. 3D packaging, which involves stacking chips vertically and connecting them through through-silicon vias (TSVs), is gaining traction in high-performance applications such as artificial intelligence (AI), autonomous vehicles, and advanced medical technologies. This innovation is essential for meeting the growing demand for faster, more powerful, and energy-efficient devices.Chip-on-chip solutions are also becoming more prevalent, enabling the stacking of chips with minimal distance between them. This reduction in signal latency boosts overall system efficiency, which is crucial for next-gen applications like 5G, Internet of Things (IoT) devices, and data centers, where managing increasing processing power in smaller form factors is key.For instance, ASMPT has reported just a 60% utilization rate in some of its traditional equipment segments, and the high-end smartphone and industrial markets in China have shown signs of softness. Additionally, equipment sales in the foundry and logic segment, which represents a large share of wafer fab receipts, are expected to decline in 2023 after robust demand in prior years. Despite these challenges, semiconductor-packaging technologies continue to evolve, playing a critical role in shaping the future of the global semiconductor market.

Restraints

- Supply Chain Disruptions and Material Shortages in Semiconductor Back-End Equipment Market

Supply chain disruptions and material shortages continue to be significant challenges in the semiconductor back-end equipment market. The global semiconductor industry has been grappling with issues such as raw material shortages, transportation bottlenecks, and geopolitical tensions, which have intensified these constraints. A major concern is the scarcity of critical raw materials, including rare earth metals and semiconductor-grade photoresists, which are essential for manufacturing semiconductor equipment. This shortage has caused delays in production schedules and extended lead times, limiting manufacturers' ability to meet the increasing global demand for semiconductors. The U.S. government has initiated a 100-day review of the semiconductor supply chain, as highlighted in a recent White House executive order. The review focuses on critical areas such as semiconductor production, advanced packaging technologies, and rare earths. It aims to address underinvestment in domestic production, which has led to the shift of manufacturing capabilities overseas. Additionally, the executive order outlines a broader one-year review of U.S. supply chains across key sectors like defense, energy, and agriculture. This initiative is expected to enhance resilience and reduce dependency on limited global sources, which has become a critical issue due to the rising demand for AI applications and advanced consumer electronics. The growing demand for advanced technologies, such as AI and high-performance computing, has led to a surge in competition for semiconductor components, creating significant supply shortages. As AI-driven applications continue to expand, particularly in industries like automotive and healthcare, the need for semiconductor equipment has further strained supply chains. These challenges underscore the urgent need for a redefined supply strategy to improve resilience, ensuring that semiconductor back-end processes like packaging, testing, and assembly can keep pace with technological advancements.

Semiconductor Back-End Equipment Market Segment Analysis

by Type

In 2023, the Assembly and Packaging segment captured the largest revenue share, approximately 45%, in the Semiconductor Back-End Equipment market. This segment plays a crucial role in ensuring that semiconductor chips are appropriately packaged for end-use applications, facilitating their integration into consumer electronics, automotive systems, medical devices, and other technology sectors. The growth in this segment is driven by the increasing complexity of semiconductor devices, which require advanced packaging solutions to optimize performance, reduce size, and enhance power efficiency. Innovations such as 3D packaging, chip-on-chip solutions, and advanced molding techniques are driving demand for assembly and packaging equipment. Additionally, as consumer electronics, AI applications, and automotive technologies continue to evolve, the need for highly efficient, compact, and powerful semiconductors has further propelled the importance of assembly and packaging. As a result, this segment is expected to maintain a strong market presence, fueling the growth of the semiconductor back-end equipment market.

Semiconductor Back-End Equipment Market Regional Outlook

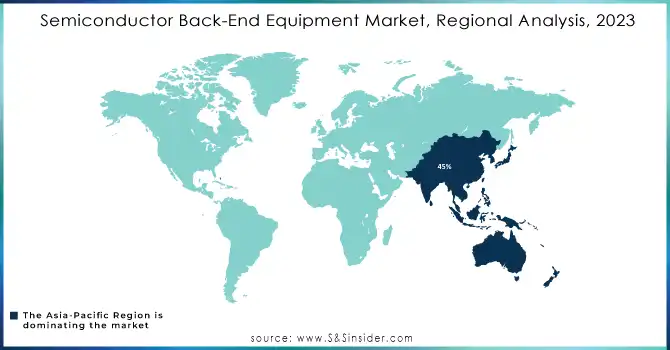

In 2023, Asia-Pacific held the largest share of the semiconductor back-end equipment market, accounting for 45%. This dominance is largely attributed to the region's well-established semiconductor manufacturing hubs. Significant investments in advanced manufacturing technologies, including metrology, testing, packaging, and assembly equipment, have strengthened its position. Asia-Pacific also benefits from a robust supply chain that provides access to essential raw materials, high-precision equipment, and a skilled workforce. The growing demand for consumer electronics, automotive electronics, AI-powered devices, and 5G infrastructure has further fueled the need for back-end equipment. Additionally, ongoing advancements in packaging technologies, such as 3D packaging and chip-on-chip solutions, continue to drive market growth in the region. These factors collectively support Asia-Pacific's dominant role in the semiconductor back-end equipment market, with continued expansion expected through 2032.

In 2023, North America emerged as the fastest-growing region in the semiconductor back-end equipment market. This rapid growth is primarily driven by the increasing demand for high-performance semiconductor devices across various sectors, including automotive, telecommunications, healthcare, and consumer electronics. North America benefits from a strong presence of key semiconductor companies and major technological advancements in semiconductor manufacturing processes. The region is also witnessing significant investments in semiconductor production and research and development, supported by government initiatives such as the CHIPS Act, aimed at boosting domestic semiconductor production and reducing reliance on foreign suppliers. The growth of AI, machine learning, and data centers further accelerates the demand for advanced packaging and testing equipment. North America's highly skilled workforce and access to cutting-edge technologies in packaging and assembly are key factors contributing to the region's fast-paced market expansion.

Need Any Customization Research On Semiconductor Back-End Equipment Market - Inquiry Now

Key Players

Some of the major players in Semiconductor Back-End Equipment Market with their product:

- ASM International (Die Bonders, Wire Bonders)

- K&S (Die Bonders, Wire Bonding Equipment)

- Tokyo Electron Limited (Testers, Wafer Bonders)

- Kulicke & Soffa (Die Attach Equipment, Wire Bonding Machines)

- Entegris (Wafer Packaging Solutions)

- Amkor Technology (Test and Assembly Equipment)

- Applied Materials (Wafer Processing Equipment)

- Nippon Avionics (Soldering Machines, Testing Equipment)

- Laminating Solutions (IC Packaging Equipment)

- Huwaei Technologies (Semiconductor Packaging & Testing)

- Schreiner Group (Packaging Solutions)

- Renesas Electronics (Back-End Process Equipment)

- STMicroelectronics (Test and Packaging Equipment)

- Micron Technology (Semiconductor Assembly Solutions)

- ASE Group (Assembly and Test Services)

- Taiwan Semiconductor Manufacturing Company (TSMC) (Back-End Testing and Packaging Solutions)

- JSR Corporation (Photoresists, Materials for Semiconductor Packaging)

- Xilinx (Packaging Solutions for Semiconductor Devices)

- Intel Corporation (Advanced Packaging Technologies)

- Samsung Electronics (Semiconductor Packaging and Assembly)

List of key suppliers of raw materials in the Semiconductor Back-End Equipment market:

- SUMCO Corporation - Silicon Wafers

- GlobalWafers Co. - Silicon Wafers

- Dow Inc. - Chemical Materials for Packaging

- BASF - Photoresists, Chemicals

- Mitsubishi Materials - Bonding Materials, Packaging Materials

- DuPont - Semiconductor Materials, Coatings

- Air Products and Chemicals - Gases for Semiconductor Fabrication

- 3M - Adhesives, Tapes, and Bonding Materials

- Linde PLC - Gases for Back-End Processes

- Henkel AG - Adhesives, Encapsulants

Recent Development

- Jun 5, 2024,Huawei is exploring the use of self-aligned quadruple patterning (SAQP) to advance its chip-making capabilities despite US sanctions. This technique, which relies on existing chip-making equipment, may allow Huawei to continue developing advanced semiconductors, raising questions about how far it can push the limits of current technology.

- June 18, 2024, STMicroelectronics has announced the construction of a new 200mm Silicon Carbide (SiC) manufacturing facility in Catania, Italy. This facility will support the mass production of SiC power devices and modules, integrating all production steps from substrate development to packaging, and is a significant part of ST's efforts to lead the global SiC ecosystem.

- May 7, 2024, Intel has partnered with 14 Japanese firms to form a research body focused on automating back-end chipmaking processes, such as packaging, with plans to implement these technologies by 2028. This collaboration is part of efforts to strengthen Japan's semiconductor supply chain.

- June 24, 2024,Entegris highlighted strong growth in demand for its semiconductor consumables, supported by AI, EVs, industrial automation, and wearable tech. Forecasts project the semiconductor industry to hit USD 1 trillion by 2030, aligning with Entegris’ 75% unit-driven sales model.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 17.32 Billion |

| Market Size by 2032 | USD 36.86 Billion |

| CAGR | CAGR of 8.76% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Metrology and Inspection, Dicing, Bonding, and Assembly and Packaging) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ASM International, K&S, Tokyo Electron Limited, Kulicke & Soffa, Entegris, Amkor Technology, Applied Materials, Nippon Avionics, Laminating Solutions, Huawei Technologies, Schreiner Group, Renesas Electronics, STMicroelectronics, Micron Technology, ASE Group, Taiwan Semiconductor Manufacturing Company (TSMC), JSR Corporation, Xilinx, Intel Corporation, and Samsung Electronics are key players in the semiconductor back-end equipment market. |

| Key Drivers | • Revolutionizing Semiconductor Packaging and the Impact of 3D and Chip-on-Chip Solutions on Industry Growth. |

| Restraints | • Supply Chain Disruptions and Material Shortages in Semiconductor Back-End Equipment Market. |