Self-supervised Learning Market Report Scope & Overview:

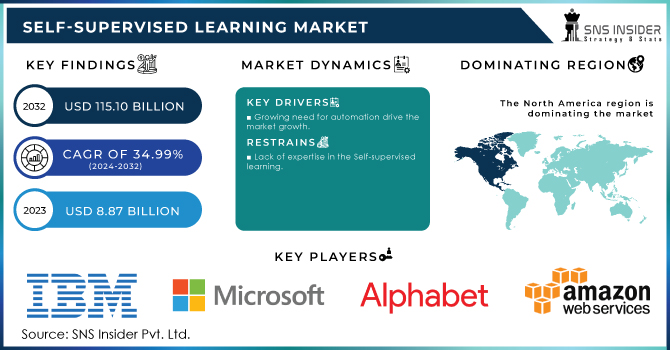

The Self-supervised Learning Market Size was valued at USD 12.23 Billion in 2023 and is expected to reach USD 171.0 Billion by 2032 and grow at a CAGR of 34.1% over the forecast period 2024-2032.

Get More Information on Self-supervised Learning Market - Request Sample Report

Self-supervised learning market is rapidly emerging as a pivotal technology in the artificial intelligence (AI) ecosystem, transforming industries by enabling machines to learn from unstructured data without extensive manual labeling. The self-supervised learning market is experiencing significant growth, driven by advancements in AI, the rising demand for automation, and the increasing volume of unstructured data generated across sectors such as healthcare, finance, retail, automotive, and more.

Growth is fueled by the increasing adoption of self-supervised learning models across various industries, including healthcare, finance, and automotive, due to their ability to work with large datasets without the need for extensive human-labeled data. In the United States, AI innovation is leading globally, with private AI investments reaching USD 67.2 billion, significantly surpassing other countries. This substantial investment landscape indicates a robust environment for the development and deployment of self-supervised learning technologies.

Furthermore, the U.S. government's emphasis on AI research and development, along with supportive policies, is expected to continue propelling the self-supervised learning market forward. The integration of self-supervised learning in various applications, such as natural language processing and computer vision, is enhancing operational efficiencies and enabling the development of innovative products, thereby contributing to the market's expansion. As organizations strive to leverage unstructured data for strategic decision-making, the demand for self-supervised learning solutions is anticipated to rise, positioning the market for sustained growth in the coming years.

Market Dynamics

Key Drivers:

-

Increasing Utilization of Unstructured Data for Enhanced Decision-Making Drives Growth in Self-Supervised Learning Market

The rapid increase in the generation of unstructured data from diverse sources like text, images, and videos has significantly boosted the demand for Self-Supervised Learning (SSL). self-supervised learning models excel at analyzing such unstructured data without requiring extensive manual labeling, enabling businesses to extract actionable insights. Industries such as healthcare, finance, retail, and automotive are adopting self-supervised learning to improve processes like customer analytics, fraud detection, and personalized recommendations.

For instance, healthcare providers use SELF-SUPERVISED LEARNING for medical imaging and diagnostics, while financial institutions apply it to detect anomalies in vast transactional datasets.

This capability not only enhances decision-making but also reduces the time and cost associated with traditional data processing techniques. With businesses increasingly prioritizing data-driven strategies, the role of self-supervised learning in managing and leveraging unstructured data continues to expand, contributing significantly to market growth.

-

Cost-effective AI Training Solutions Using Unlabeled Data Propel Adoption of Self-Supervised Learning Technologies

Manual labelling of datasets is expensive and labor-intensive, particularly for organizations dealing with large-scale data. self-supervised learning eliminates this challenge by training models on unlabelled data, making AI implementation more cost-effective. This advantage is particularly relevant in sectors like automotive, where self-supervised learning models are used for training autonomous vehicles, and in retail, where customer behaviour is analysed using transactional and browsing data.

By reducing reliance on costly manual processes, self-supervised learning enables organizations to develop advanced AI solutions more efficiently. This affordability is encouraging small and medium-sized enterprises (SMEs) to invest in AI-driven tools, further expanding the market. Additionally, the scalability of self-supervised learning makes it suitable for cloud-based applications, allowing businesses to optimize operations and innovate without heavy upfront investments.

Restrain:

-

Limited Awareness and Technical Expertise in Self-Supervised Learning Hinders Market Expansion

Despite its transformative potential, the adoption of self-supervised learning faces challenges due to limited awareness and a lack of technical expertise among businesses. Many organizations, especially small and medium enterprises, are unfamiliar with the benefits of SSL, including its ability to process unstructured data efficiently and cost-effectively. Furthermore, implementing self-supervised learning solutions often requires specialized knowledge of AI and Machine Learning frameworks, which can be a barrier for companies lacking skilled personnel.

This knowledge gap is compounded by the complexity of integrating self-supervised learning models with existing systems, as organizations may face difficulties in transitioning from traditional supervised learning methods. Moreover, misconceptions about self-supervised learning’s capabilities and concerns over its computational requirements deter businesses from adopting these technologies. Addressing these issues through education, training programs, and user-friendly tools will be critical for unlocking the full potential of the self-supervised learning market.

Segments Analysis

By Technology

The Natural Language Processing (NLP) segment accounted for the largest revenue share of 43% in 2023, driven by the widespread adoption of AI-driven language models in various industries. NLP, a core AI technology, enables machines to understand and interpret human language, which is crucial for applications such as chatbots, sentiment analysis, translation, and voice assistants. In recent years, companies have made significant strides in NLP development. For example, OpenAI’s GPT-4 and Google’s PaLM have raised the bar in language model performance, driving further interest in self-supervised learning approaches.

The Speech Processing segment is projected to grow at the largest CAGR of 36.51% within the forecasted period, driven by increasing demand for speech recognition technologies across industries like healthcare, automotive, and customer service. Companies like Microsoft, Amazon, and Google are making major advancements in speech processing technology, with products like Amazon Alexa, Google Assistant, and Microsoft’s Speech SDK taking center stage. Amazon’s launch of the new Amazon Transcribe Medical service in 2023, which leverages self-supervised learning for accurate medical transcription from voice input, and Google’s advancements in multilingual voice assistants are perfect examples of the growing use of self-supervised learning in speech processing.

By End User

The BFSI segment held the largest revenue share of 19% in 2023, reflecting the critical role of AI and machine learning technologies in transforming financial services. Self-supervised learning is gaining traction within this segment, enabling banks and insurance companies to leverage vast amounts of unstructured data for fraud detection, risk assessment, customer behavior analysis, and automated decision-making.

Additionally, in the insurance sector, companies like Allianz have started using self-supervised learning for claims processing and underwriting, enhancing accuracy and efficiency. The BFSI industry benefits from self-supervised learning by improving model training, reducing the costs of data labeling, and providing scalable solutions to process complex datasets.

The Advertising & Media segment is expected to grow at the highest CAGR of 35.9% during the forecasted period, driven by the increasing reliance on AI-driven personalized content and targeted advertising. Self-supervised learning plays a significant role in the evolution of advertising technologies, particularly in content recommendation engines and audience segmentation.

In 2023, Meta launched new machine learning tools, including a self-supervised learning-powered content recommendation system that enhances ad targeting by analyzing user interactions across various platforms. Similarly, Google’s advancements in YouTube’s recommendation algorithm, which utilizes self-supervised learning techniques to predict user interests and improve video suggestions, are pushing the boundaries of personalized advertising.

Regional Analysis

In 2023, North America dominated the Self-Supervised Learning market, holding a significant market share, estimated at approximately 35%. This dominance is largely due to the region’s strong technology infrastructure, substantial investments in AI research, and the presence of major tech giants like Google, Microsoft, Amazon, and IBM. These companies are at the forefront of developing and deploying self-supervised learning models across industries, including finance, healthcare, automotive, and retail.

For instance, in 2023, IBM launched its Watsonx AI platform, incorporating SSL for enhanced natural language processing (NLP) capabilities, helping businesses in North America to process vast amounts of unstructured data efficiently.

Asia Pacific is the fastest-growing region in the Self-Supervised Learning market in 2023, with an estimated CAGR of 36.07% during the forecasted period. This rapid growth is driven by the increasing adoption of AI technologies across key markets like China, India, Japan, and South Korea. These countries are making significant strides in AI research, development, and deployment, particularly in sectors like e-commerce, finance, manufacturing, and telecommunications.

For example, Chinese tech giants such as Baidu and Alibaba are leveraging SSL techniques to enhance voice recognition and AI-powered search engines, while Indian companies are using SSL in fintech for fraud detection and risk assessment.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

Some of the major players in the Self-supervised Learning Market are:

-

Alphabet Inc. (Google LLC) (TensorFlow, Google Cloud AutoML)

-

Amazon Web Services, Inc. (Amazon SageMaker, AWS Deep Learning AMIs)

-

Apple Inc. (Core ML, Siri Personal Assistant)

-

Baidu, Inc. (PaddlePaddle, Baidu Apollo)

-

Dataiku (Dataiku DSS, AutoML in Dataiku)

-

Databricks (Databricks Lakehouse Platform, Databricks AutoML)

-

DataRobot, Inc. (DataRobot AI Cloud, Paxata)

-

IBM Corporation (IBM Watson Studio, IBM SPSS Modeler)

-

Meta (Facebook) (PyTorch, DINO)

-

Microsoft (Azure Machine Learning, Microsoft Project Bonsai)

-

SAS Institute Inc. (SAS Viya, SAS Visual Data Mining and Machine Learning)

-

Tesla (Full Self-Driving Software, Tesla Vision)

-

The MathWorks, Inc. (MATLAB, Simulink)

-

DataCamp, Inc. (DataCamp Workspace, DataCamp Projects)

-

Alison (Alison Machine Learning Courses, Alison AI Learning Paths)

-

Brain4ce Education Solutions Pvt. Ltd. (Edureka Machine Learning Certification Training, Edureka Deep Learning with TensorFlow)

-

edX LLC (edX MicroMasters in Artificial Intelligence, edX Deep Learning Professional Certificate)

Recent Development

-

In July 2024, Google LLC introduced India's Agricultural Landscape Understanding (ALU) tool. This AI-powered platform leverages high-resolution satellite imagery and machine learning to deliver detailed insights into drought preparedness, irrigation strategies, and crop management at the farm level. The tool is designed to address farmers' challenges by providing data-driven insights to enhance agricultural practices, boost crop yields, and improve market access.

-

In May 2024, researchers from Meta AI, Google, INRIA, and the University of Paris Saclay collaborated to develop an innovative dataset curation technique for Self-Supervised Learning (SSL). This approach utilizes embedding models and hierarchical k-means clustering to create balanced datasets, enhancing model performance while significantly reducing the time and cost of manual curation.

-

In January 2024, IBM Corporation partnered with Sevilla FC, a prominent Spanish football club, to launch Scout Advisor, a generative AI tool based on IBM’s Watson platform. This tool uses natural language processing to streamline player recruitment by analyzing scouting reports. By integrating self-supervised and supervised learning, Scout Advisor enables the scouting team to efficiently gather and assess subjective and objective player data, improving decision-making processes.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 12.23 Billion |

| Market Size by 2032 | US$ 171.0 Billion |

| CAGR | CAGR of 34.1 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By End User (Healthcare, BFSI, Automotive & Transportation, Software Development (IT), Advertising & Media, Others) • By Technology (Natural Language Processing (NLP), Computer Vision, Speech Processing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Alphabet Inc. (Google LLC), Amazon Web Services, Inc., Apple Inc., Baidu, Inc., Dataiku, Databricks, DataRobot, Inc., IBM Corporation, Meta, Microsoft, SAS Institute Inc., Tesla, The MathWorks, Inc., DataCamp, Inc., Alison, Brain4ce Education Solutions Pvt. Ltd., edX LLC. |

| Key Drivers | • Increasing Utilization of Unstructured Data for Enhanced Decision-Making Drives Growth in Self-Supervised Learning Market • Cost-effective AI Training Solutions Using Unlabeled Data Propel Adoption of Self-Supervised Learning Technologies |

| Restraints | • Limited Awareness and Technical Expertise in Self-Supervised Learning Hinders Market Expansion |