Rubber Additives Market Report Scope & Overview:

Get More Information on Rubber Additives Market - Request Sample Report

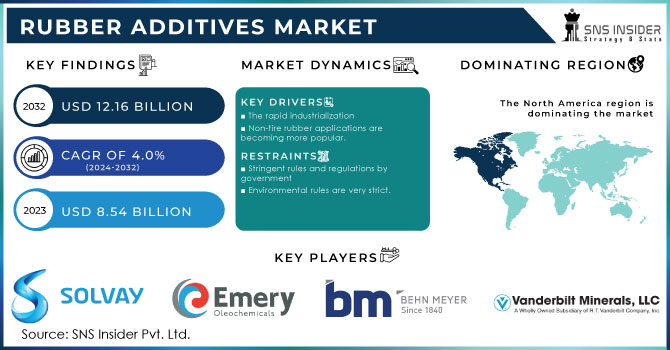

The Rubber Additives Market Size was valued at USD 8.5 billion in 2023 and is expected to reach USD 12.2 billion by 2032 and grow at a CAGR of 4.0% over the forecast period 2024-2032.

The Rubber Additives Market is experiencing significant transformation driven by various market dynamics, including the increasing demand for high-performance rubber in various end-user industries. These dynamics include advancements in manufacturing technologies, the growing focus on enhancing the performance and lifespan of rubber products, and environmental regulations pushing for more sustainable materials. In particular, the rise of electric vehicles (EVs) is creating a heightened need for specific rubber additives that can improve tire performance, reduce rolling resistance, and enhance fuel efficiency, as these factors are crucial for EV manufacturers aiming to meet regulatory standards and consumer expectations.

Recent collaborations in the industry illustrate these trends. For instance, a notable partnership formed between Suzano and Behn Meyer in June 2023 highlights efforts to innovate rubber production through the utilization of sustainable resources. This partnership aims to leverage Behn Meyer’s expertise in specialty chemicals to enhance the sustainability of rubber production processes, aligning with global trends emphasizing eco-friendliness. This collaboration not only supports the development of rubber products with lower environmental impact but also demonstrates a strategic move towards creating a more resilient supply chain in the rubber industry, where sustainability has become a competitive edge.

Additionally, companies are increasingly focusing on developing new formulations and applications for rubber additives to cater to emerging needs. For instance, in September 2023, Taizhou Huangyan Donghai Chemical Company reported on new trends that emphasize the importance of polymer processing aids and compatibilizers in rubber formulations. These advancements are essential for enhancing the compatibility of different materials used in rubber, which is particularly critical for products that require a blend of performance characteristics. The ongoing research and development in this area illustrate the market's proactive approach to meeting the demands of diverse applications, from automotive to construction.

Moreover, market players are also responding to the growing consumer awareness regarding the use of additives in rubber products. With the rise in demand for high-quality and environmentally sustainable products, companies are prioritizing transparency and quality assurance in their supply chains. The focus on green chemistry principles and the development of bio-based rubber additives reflect the industry's commitment to reducing its ecological footprint. This shift not only meets regulatory compliance but also resonates with consumers seeking products that align with their sustainability values. Overall, these developments signify a robust and evolving market landscape that is adapting to both technological advancements and changing consumer preferences.

Rubber Additives Market Dynamics:

Drivers:

-

Growing Demand for Eco-Friendly Products in Various Industries Boosts the Rubber Additives Market Growth

The increasing consumer awareness regarding sustainability is significantly driving the demand for eco-friendly products across various industries, including automotive, construction, and consumer goods. Manufacturers are now prioritizing the use of natural and biodegradable rubber additives, which not only meet regulatory standards but also align with consumers' environmental values. This shift towards sustainability is evident as companies invest in research and development to create innovative, environmentally friendly alternatives to traditional rubber additives, such as bio-based plasticizers and green fillers. For instance, industry leaders are focusing on reducing the carbon footprint associated with rubber production by sourcing raw materials from renewable resources and implementing sustainable manufacturing practices. This not only helps companies enhance their brand reputation but also attracts a broader customer base that prioritizes sustainable options. As regulations regarding waste and emissions become stricter, the rubber additives market is expected to continue evolving, with manufacturers increasingly adopting eco-friendly solutions to meet both regulatory requirements and consumer expectations.

-

Advancements in Manufacturing Technologies Enhance Efficiency in Rubber Additive Production

Technological advancements in manufacturing processes are revolutionizing the rubber additives market by increasing efficiency and reducing production costs. Innovations such as automated production lines, advanced mixing techniques, and real-time quality control systems allow manufacturers to optimize their operations and ensure consistent product quality. These advancements also facilitate the development of new formulations that meet the evolving needs of various end-user applications. For example, modern blending techniques enable better dispersion of additives within rubber compounds, resulting in improved performance characteristics such as enhanced strength, elasticity, and resistance to wear and tear. Furthermore, the integration of digital technologies and Industry 4.0 principles, such as IoT and data analytics, allows companies to monitor production processes more closely, identify inefficiencies, and make data-driven decisions to enhance productivity. As the demand for high-performance rubber products continues to rise, manufacturers who leverage these technological advancements will be better positioned to compete in the dynamic rubber additives market.

Restraint:

-

Fluctuating Raw Material Prices Pose a Restraint on Rubber Additives Market Growth

The rubber additives market faces challenges due to fluctuating raw material prices, which can significantly impact production costs and profitability. The prices of key raw materials, such as synthetic rubber, fillers, and additives, can vary widely based on global supply and demand dynamics, geopolitical issues, and natural disasters affecting production. For instance, disruptions in the supply chain caused by adverse weather conditions or political instability in major producing regions can lead to sudden spikes in raw material costs. These fluctuations can strain manufacturers, forcing them to either absorb the increased costs, which can erode profit margins, or pass them on to customers, which may affect sales. Additionally, the reliance on petrochemical-based materials poses a risk, as the transition towards more sustainable and renewable resources gains momentum in the industry. As a result, manufacturers must continuously strategize to mitigate these risks, either by diversifying their supply chains or investing in alternative raw materials, to maintain stability in their operations and ensure competitive pricing for their products.

Opportunity:

-

Increasing Opportunities for Innovation in Bio-Based Rubber Additives Present Growth Potential

The growing emphasis on sustainability and environmental stewardship presents significant opportunities for innovation in bio-based rubber additives. As consumers and industries alike seek more sustainable alternatives to traditional synthetic additives, there is a rising demand for bio-based options derived from renewable resources. This shift encourages manufacturers to invest in research and development to create new formulations that maintain or enhance performance while minimizing environmental impact. For instance, innovations in bioplastics and natural fillers sourced from agricultural byproducts or renewable biomass can provide viable alternatives to petroleum-based additives. Moreover, collaborations between chemical manufacturers and research institutions are fostering the development of new bio-based additives that meet specific performance criteria in applications such as tires, sealants, and coatings. The increasing availability of government incentives and support for green initiatives further enhances the market potential for bio-based rubber additives, positioning manufacturers who embrace these innovations to capitalize on emerging trends and gain a competitive advantage in the marketplace.

Challenge:

-

Stringent Regulatory Compliance Presents Challenges for Rubber Additives Manufacturers

Manufacturers in the rubber additives market face significant challenges related to stringent regulatory compliance and standards imposed by various governmental and environmental organizations. These regulations often require companies to adhere to strict guidelines regarding the use of certain chemicals and additives, particularly those that may be deemed harmful to health or the environment. For instance, the rising scrutiny over the use of hazardous substances in rubber production has led to increased testing and certification requirements, resulting in higher operational costs for manufacturers. Compliance with these regulations not only demands significant investments in technology and processes but also requires continuous monitoring and reporting to ensure adherence. Failure to comply with these regulations can result in severe penalties, product recalls, and reputational damage, creating substantial risks for companies operating in the rubber additives market. Additionally, the dynamic nature of regulatory frameworks, which can change frequently and vary across regions, adds complexity to the manufacturing process, compelling companies to remain vigilant and adaptable in their strategies to navigate these challenges effectively.

Rubber Additives Market Segments

By Type

In 2023, the Plasticizers segment dominated the Rubber Additives Market, accounting for a market share of 30%. Plasticizers play a crucial role in enhancing the flexibility, workability, and durability of rubber products. Their importance is particularly evident in applications such as tires and sealants, where the ability to maintain performance under various environmental conditions is critical. For example, leading manufacturers are increasingly using advanced plasticizers derived from renewable resources, which not only improve the properties of rubber but also align with the growing demand for eco-friendly materials. This trend is driven by the need for high-performance products that can withstand extreme temperatures and mechanical stresses while minimizing environmental impact.

By Application

The Tires segment dominated the application in the Rubber Additives Market in 2023, holding a market share of 40%. This dominance is primarily attributed to the increasing demand for high-performance tires, particularly in the automotive sector, where safety, durability, and fuel efficiency are paramount. Tire manufacturers are continually seeking ways to enhance the performance of their products, which requires the use of various rubber additives, including accelerators and anti-aging agents. For instance, advancements in tire technology, such as the incorporation of silica-based compounds and specialty additives, are contributing to improved grip, lower rolling resistance, and extended tread life, further fueling the growth of this segment.

By End Use Industry

In 2023, the Automotive sector dominated the Rubber Additives Market and accounted for a market share of 35%. The automotive industry is the largest consumer of rubber additives due to the widespread use of rubber in various components, including tires, seals, gaskets, and hoses. The shift towards electric vehicles (EVs) is further amplifying this demand, as manufacturers are focusing on developing specialized rubber formulations that enhance tire performance and vehicle safety. Additionally, the growing emphasis on lightweight materials and fuel efficiency is driving innovations in rubber additives, ensuring that automotive applications remain at the forefront of market development. For example, companies are investing in research to create rubber compounds that provide better thermal stability and chemical resistance, critical for modern automotive applications.

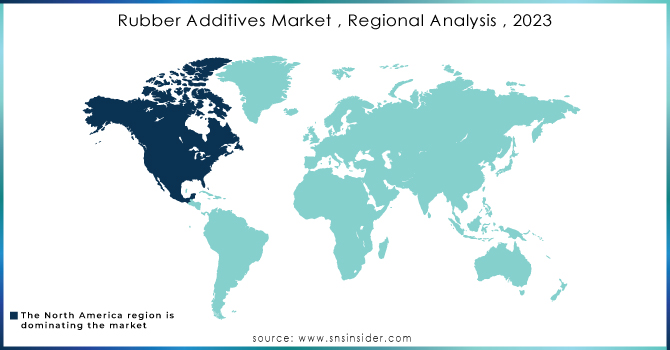

Rubber Additives Market Regional Analysis

In 2023, the Asia Pacific region dominated the Rubber Additives Market, with a market share of 45%. This dominance is primarily driven by the rapid industrialization and urbanization occurring in countries like China and India, which are among the largest consumers of rubber additives. The growing automotive and construction industries in this region are significant contributors to the demand for high-performance rubber products. For instance, China's aggressive push toward electric vehicle production is leading to increased use of advanced rubber formulations in tires and other components, requiring a wide array of additives. Furthermore, the presence of numerous manufacturing hubs and a favorable regulatory environment for chemical production bolster the region's market position, allowing companies to meet both domestic and export demands efficiently.

Moreover, the North American region emerged as the fastest-growing region in the Rubber Additives sector in 2023, with a CAGR of 6.5%. This growth is driven by the rising focus on technological innovations and sustainability in the rubber industry, particularly within the automotive sector. The increasing adoption of electric vehicles and stringent regulations regarding emissions are prompting manufacturers to develop more efficient and environmentally friendly rubber additives. For example, companies in the U.S. are investing heavily in research to create bio-based additives that can replace traditional petrochemical options, thus aligning with both regulatory demands and consumer preferences. Additionally, the strong presence of major automotive manufacturers and their continuous drive for improved performance in rubber components further contribute to the region's robust growth trajectory.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

-

Akzonobel N.V. (Durethan, Hybrane)

-

Arkema SA (Kraton, Eliokem)

-

BASF SE (Elastoflex, Irganox)

-

Behn Meyer Group (Vulcanizing Agents, Anti-oxidants)

-

China Petroleum and Chemical Corporation (Sinopec Rubber Processing Additives, Rubber Antioxidants)

-

Eastman Chemical Company (Eastman Tetrashield, Eastman Versaflex)

-

Emery Oleochemicals LLC (Emery Lox, Bio-Additives)

-

Lanxess AG (Vulcanization accelerators, Rhein Chemie Additives)

-

R.T. Vanderbilt Company Inc (Vanderbilt Carbon Black, Vanderbilt Anti-Oxidants)

-

Solvay SA (Solef, Hydralene)

-

Addivant USA LLC (Epolene, Addivant 1440)

-

Cabot Corporation (Cabot Carbon Blacks, Cabot Specialty Compounds)

-

DuPont de Nemours, Inc. (DuPont Keltan, DuPont Tychem)

-

Evonik Industries AG (Aerosil, VESTANAT)

-

Hexpol AB (Hexpol TPE, Hexpol Compounding)

-

Kumho Petrochemical Co., Ltd. (Kumho Styrene-Butadiene Rubber, Kumho EPDM)

-

Momentive Performance Materials Inc. (Momentive Silicones, Momentive MQ Silicones)

-

Michelin Group (Michelin Compounding Agents, Michelin Tread Compounds)

-

Rhein Chemie Rheinau GmbH (Rhenofit, Rhenogran)

-

The Dow Chemical Company (Dow Silicones, Dow Epoxy Resins)

Recent Developments

February 2023: Yokohama Rubber Co., Ltd. (YRC) unveiled its expansion plans for 2023, which follows the completion of its current medium-term business strategy, Yokohama Transformation 2023. This initiative involves increasing the production capacity of passenger car tires in India, aiming to boost the Group's output by 60%, resulting in a total annual production capacity of 4.5 million units.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 8.5 Billion |

| Market Size by 2032 | US$ 12.2 Billion |

| CAGR | CAGR of 4.0% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Accelerators, Activators, Peptizers, Plasticizers, Tackifiers, Others) • By Application (Tires, Conveyor Belts, Electric Cables, Specialty Tapes, Others) • By End Use Industry (Automotive, Electronics and Semiconductors, Construction, Industrial, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | R.T. Vanderbilt Company Inc, Emery Oleochemicals LLC, Solvay SA, Behn Meyer Group, Akzonobel N.V., BASF SE, Lanxess AG, China Petroleum and Chemical Corporation, Arkema SA, Eastman Chemical Company and other key players |

| Drivers | • Growing Demand for Eco-Friendly Products in Various Industries Boosts the Rubber Additives Market Growth • Advancements in Manufacturing Technologies Enhance Efficiency in Rubber Additive Production |

| Restraints | • Fluctuating Raw Material Prices Pose a Restraint on Rubber Additives Market Growth |