To get more information on Robotic Lawn Mower Market - Request Free Sample Report

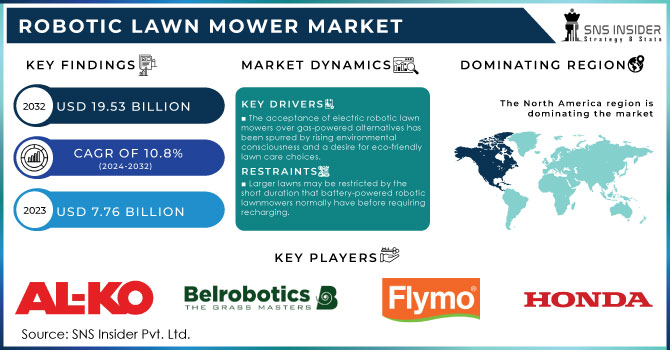

The Robotic Lawn Mower Market size was estimated at USD 7.76 billion in 2023 and is expected to reach USD 19.53 billion by 2032 at a CAGR of 10.8% during the forecast period of 2024-2032.

The industry was anticipated to expand at a significant rate due to the increasing preference of lawn care and gardening in high-income residents. This is due to increasing end-user income levels and rising demand for robotic lawn mowers. It was found that a mower enhances appearance and user experiences. In addition, this invention has a specific. The emergence of high-end products and technology is expected to be the primary driver of expansion for this market. The wooden mowers utilize this wire to determine the part of the plot that needs to be chopped and sometimes to locate a recharging station. Most of these robotic devices can maintain about 320,000 sq.ft of grass. Robotic mowers that are under 60 decibels may sometimes mow in situations where other ordinary lawn mower are not allowed to operate. The robotic mower sleeps in the day and works in any lawn, whether making a manicure in the middle of the night. The robot grass cutter can work with any slope of your garden or plot, returning to the charging point whenever it stops. The range of noise among the least quiet robot lawn mower to the loudest is from 58 to 74 dB.

Increased expenditure on backyard beautification, landscaping, garden parties, and backyard cookouts, among others, and consumer need to save on time spent on lawn maintenance activities are the key factors expected to drive the global demand for gardening tools. The growth of the market is also attributable to the increasing construction and tourism industries and the rising disposable income of people across the global scales. Furthermore, the anticipated financial hitches in the global demand for robotic lawn mowers are expected to generate positive shifts in the global demand. A number of consumers in the US, Germany, and the UK, among other regions in the global scale, are currently dedicating considerable amounts of time and financial resources into bettering their gardens, yards, and lawns. The consumer approach is expected to increase the global demand for smart lawn care products that save time, money, and energy. Consequently, the high spending by consumers in the beautification of their backyard area is expected to drive the growth of the market.

DRIVERS

The acceptance of electric robotic lawn mowers over gas-powered alternatives has been spurred by rising environmental consciousness and a desire for eco-friendly lawn care choices.

The increasing popularity of electric robotic lawn mowers over polluting gas-powered models is mainly due to a number of factors. Due to the growing attention of buyers to environmental issues, solutions contributing to their resolution appear to be of the greatest interest. Such an approach allows people to notice that traditional gas-powered lawn mowers are not quite eco-friendly. Firstly, they had a non-renewable gas that produced gases hazardous to the environment. Gas also contributes to the impoverishment of the atmosphere and entices into it noise that exceeds environmental standards. Mowers are also relatively safe for buyers, especially for children and animals. The electric lawn mower in this case is much cleaner. They only work on the battery built into them which, of course, allows these lawn mowers to maintain the environment. This type of mower is less expensive to use. Refuelling is not required, and the periodic replacement of several special parts does not create a burden on the budget. Other advantages of electric robotic mowers are that they are a reliable and durable supply of batteries. This generation of batteries, which is currently being produced, allows these lawn mowers to be used by both ordinary buyers and professional builders of the lawn. One big advantage is the ability of people to provide them with work according to the schedule selected by homeowners. Most of these devices have a built-in controller that allows the lawn to maintain the same size, and even without human intervention. The new electric mowers also create a sense of security for adults, and headphones are worth the kids and the animals. The number of new models per year is growing and is only on the rise. The electric lawn mower has also lessened in price, so it is no longer labelled as an exclusive unit, so more and more people are opting for it.

Robotic lawnmowers are finding an increasing market in areas with older populations because they appeal to people who would find it difficult to maintain a regular lawn.

Robotic lawnmowers are becoming more and more popular in regions with older populations for numerous reasons. On the one hand, with age come physical limitations, and older individuals often may find it much more difficult than they did previously to actually perform all labour-intensive work in the garden, including mowing, edging or raking. Those who need some help also need the labour-intensive work that is a part of traditional lawn maintenance done for them. This is where the robotic lawnmower comes in play. This device provides for a labour-free, hands-free solution to lawn maintenance. Additionally, the robotic lawnmower operates in full-automatic mode since the device operates by advanced sensory and navigation systems, ensuring the device actually avoids any type of obstacles, maintains its designated cutting pattern and docks itself to the charger when the battery gets empty. This device can provide a timely solution to the lawn-maintenance needs of senior citizens and older individuals who cannot actually perform the tasks themselves.

The robotic lawnmowers contribute to a great level of safety, which is important for older individuals who risk getting in a considerably hazardous situation of getting injured by traditional lawnmowers, and risking getting cut by their rotating blades. In addition to this, robotic lawnmowers turn off automatically when left, tilted or picked up and are thus overall, completely safe for use. Finally, since one of the most major issues raised by the usage of traditional lawnmowers is the noise and pollution they create, and therefore exposing the user and other individuals who spend time in the yard to the detrimental consequences that come by noise, robotic lawnmowers are a quiet, pollution-free machine suitable for this purpose.

The current trend increases that in the aging communities there is a growing use of robotic lawnmowers, which is a part of the wider process of the utilization of smart home technology. There are many smart devices that are utilized by older adults and that simplify human lives. Robotic mowers are no more an exception here as by owning and utilizing such devices, the older adults keep their lawns beautiful without the need to use additional physical efforts and move the mower around. Therefore, due to the ongoing process of the older generation’s increase, the demand for robotic lawnmowers will only grow as people will need accessible and simple-to-use devices to maintain their households.

RESTRAIN

Larger lawns may be restricted by the short duration that battery-powered robotic lawnmowers normally have before requiring recharging.

The battery-powered robotic lawnmowers face when dealing with larger lawns is that of battery life. Most mowers are designed to be used primarily on smaller lawns, running for 60 to 90 minutes between each charge. Not only is this a significant oversight for a larger lawn, where the mower would be expected to run for several hours, but the need for multiple recharging cycles appears to be fundamentally opposed to the idea of the robotic mower as a time-saving device. Moreover, having to recharge the mower every hour or so during a typically two or three hour-long mowing session will likely lead to the user losing interest and allowing the lawn to grow. It seems unlikely that a robotic mower would be the best option for the owner of the linked property, at least without doing further research into more powerful models. An alternative option worth exploring is, of course, that of a traditional gas-powered mower while non-automatic and potentially damaging to the environment, gasoline mowers can easily be used to mow very large properties, as they do not have the same constraints on battery life.

By Battery Capacity

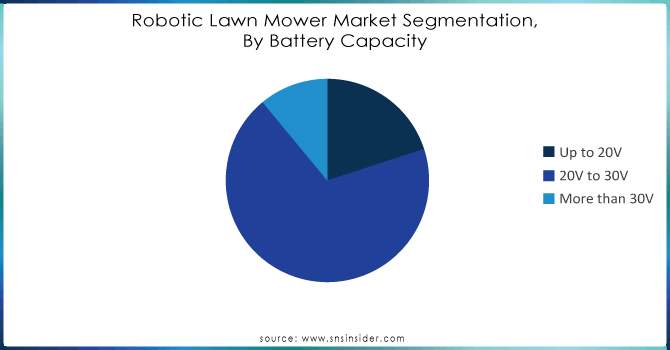

The 20V to 30V battery segment held a market share of over 69.02% in 2023, based on battery capacity. These batteries are mostly used in robotic lawn mowers for commercial applications. Those types of devices are costlier and are used to mow lawns of 1.0 to 2.5 acres and are seen in commercial spaces such as sports/golf field and hospitality industries. The segment delivers adequate power to handle intensive load-carrying capacities, traverse a way and climb up slopes or ramps. Besides, the batteries have a longer life cycle that enables the operations to be performed smoothly without issues.

Need any customization research on Robotic Lawn Mower Market - Enquiry Now

By Application

The residential sector is the segment representing the largest market share of over 57.03% in 2023. The growth in the demand for ease and time-saving solutions has prompted homeowners to switch to automatic applications that can get the job done without any voluntary input of the people residing in this area. This application allows these individuals to spend more time running errands and doing other things.

By Sales Channel

The retail stores/offline segment had the largest share of revenue of over 58.04% in 2023. The escalating demand for time-saving and convenient solutions has compelled traditional retail stores to capitalize on the use of robotic lawn mowers, which are an ease to homeowners who have very minimal time to spend mowing their lawns. Robotic lawn mowers target a wide range of end users from the busy professionals who do not have time and want to come home to groomed lawns, to the elderly who may not have the physical strength to mow the lawns as well.

REGIONAL ANALYSES

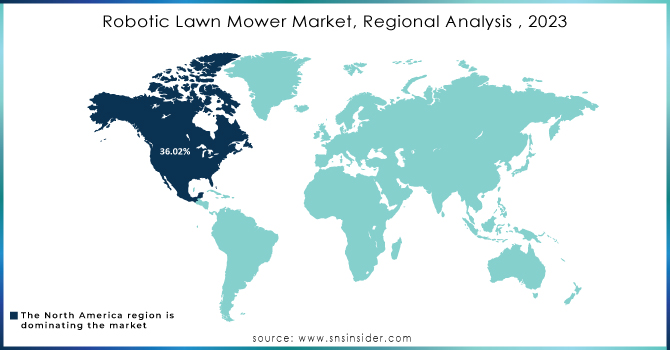

North America dominated the market with a revenue share of over 36.02% in 2023. Busy lifestyle patterns resulted in end users’ approach towards automatizing the conventional lawn maintenance activities. The robotic lawn mowers are equipped with sensors, GPS navigation systems and artificial intelligence and for every lawn size and complexity, it navigates and maintains it efficiently. Work is performed end-to end without any input from users, which allow end users to spend their time with families and maintain their focus on more important activities. Also, use of new technologies for automating lawn care routines is another factor influencing the market growth.

Asia Pacific region is expected to register the highest CAGR over the forecast period. The rapid urbanization and increasing affluence across the region have resulted in demand for smart solutions for a more convenient life. Robotic lawn mowers fit this trend by providing automatic and simple lawn care systems. Helper robots, such as robotic lawn mowers operate in gardens and yards, managing everything from cleaning pools and leaf blowing to raking leaves. The presence of countries like China, Japan and South Korea as the forerunners in adopting automation and robotics has made the market more favorable for technologies such as robotic lawn mowers.

The major key players are AL-KO, Belrobotics, Deere & Company, Flymo, HONDA MOTOR CO., LTD, Husqvarna Group,Robert Bosch GmbH, Robomow Friendly House, The Toro Co, STIGA S.p.A., WIPER S.R.L., Worx and others.

RECENT DEVELOPMENT

In January 2024: The company HOOKII Neomow launched new advancements in robotic lawn mowers such as LiDAR (Light Detection and Ranging) and SLAM (Simultaneous Localization and Mapping). LiDAR technology allowed mowers to create a more accurate map of their surroundings, enabling them to navigate more efficiently and avoid obstacles more effectively. SLAM This technology allowed mowers to build a map of their surroundings as they move, eliminating the need for perimeter wires.

In May 2022: Toro for the domestic lawn care sector, Toro revealed a robotic lawn mower with cutting-edge, user-friendly technology and previously unheard-of features. The latest in smart, connected technology for homeowners and their yards is Toro's new robotic, battery-powered mower, which the company has been producing for more than a century.

| Report Attributes | Details |

| Market Size in 2023 | US$ 7.76 Bn |

| Market Size by 2032 | US$ 19.53 Bn |

| CAGR | CAGR of 10.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Battery Capacity(Up to 20V, 20V to 30V, More than 30V) • By Application (Residential, Commercial) • By Sales Channel(Retail Store/Offline, Online Websites) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AL-KO, Belrobotics, Deere & Company, Flymo, HONDA MOTOR CO., LTD, Husqvarna Group, Robert Bosch GmbH, Robomow Friendly House, The Toro Co, STIGA S.p.A., WIPER S.R.L., Worx |

| Key Drivers | • The acceptance of electric robotic lawn mowers over gas-powered alternatives has been spurred by rising environmental consciousness and a desire for eco-friendly lawn care choices. • Robotic lawnmowers are finding an increasing market in areas with older populations because they appeal to people who would find it difficult to maintain a regular lawn. |

| Market Challenges | • Larger lawns may be restricted by the short duration that battery-powered robotic lawnmowers normally have before requiring recharging. |

Ans: The Robotic Lawn Mower Market is expected to grow at a CAGR of 10.8%.

Ans: Robotic Lawn Mower Market size was USD 7.76 billion in 2023 and is expected to Reach USD 19.53 billion by 2032.

Ans: 20V to 30V is the dominating segment by battery capacity in the Robotic Lawn Mower Market.

Ans: The acceptance of electric robotic lawn mowers over gas-powered alternatives has been spurred by rising environmental consciousness and a desire for eco-friendly lawn care choices.

Ans: North America is the dominating region in the Robotic Lawn Mower Market.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Robotic Lawn Mower Market Segmentation, By Battery Capacity

7.1 Introduction

7.2 Up to 20V

7.3 20V to 30V

7.4 More than 30V

8. Robotic Lawn Mower Market Segmentation, By Application

8.1 Introduction

8.2 Residential

8.3 Commercial

9. Robotic Lawn Mower Market Segmentation, By Sales Channel

9.1 Introduction

9.2 Retail Store/Offline

9.3 Online Websites

10. Regional Analysis

10.1 Introduction

10.2 North America

10.2.1 Trend Analysis

10.2.2 North America Robotic Lawn Mower Market, By Country

10.2.3 North America Robotic Lawn Mower Market, By Battery Capacity

10.2.4 North America Robotic Lawn Mower Market, By Application

10.2.5 North America Robotic Lawn Mower Market, By Sales Channel

10.2.6 USA

10.2.6.1 USA Robotic Lawn Mower Market, By Battery Capacity

10.2.6.2 USA Robotic Lawn Mower Market, By Application

10.2.6.3 USA Robotic Lawn Mower Market, By Sales Channel

10.2.7 Canada

10.2.7.1 Canada Robotic Lawn Mower Market, By Battery Capacity

10.2.7.2 Canada Robotic Lawn Mower Market, By Application

10.2.7.3 Canada Robotic Lawn Mower Market, By Sales Channel

10.2.8 Mexico

10.2.8.1 Mexico Robotic Lawn Mower Market, By Battery Capacity

10.2.8.2 Mexico Robotic Lawn Mower Market, By Application

10.2.8.3 Mexico Robotic Lawn Mower Market, By Sales Channel

10.3 Europe

10.3.1 Trend Analysis

10.3.2 Eastern Europe

10.3.2.1 Eastern Europe Robotic Lawn Mower Market, By Country

10.3.2.2 Eastern Europe Robotic Lawn Mower Market, By Battery Capacity

10.3.2.3 Eastern Europe Robotic Lawn Mower Market, By Application

10.3.2.4 Eastern Europe Robotic Lawn Mower Market, By Sales Channel

10.3.2.5 Poland

10.3.2.5.1 Poland Robotic Lawn Mower Market, By Battery Capacity

10.3.2.5.2 Poland Robotic Lawn Mower Market, By Application

10.3.2.5.3 Poland Robotic Lawn Mower Market, By Sales Channel

10.3.2.6 Romania

10.3.2.6.1 Romania Robotic Lawn Mower Market, By Battery Capacity

10.3.2.6.2 Romania Robotic Lawn Mower Market, By Application

10.3.2.6.4 Romania Robotic Lawn Mower Market, By Sales Channel

10.3.2.7 Hungary

10.3.2.7.1 Hungary Robotic Lawn Mower Market, By Battery Capacity

10.3.2.7.2 Hungary Robotic Lawn Mower Market, By Application

10.3.2.7.3 Hungary Robotic Lawn Mower Market, By Sales Channel

10.3.2.8 Turkey

10.3.2.8.1 Turkey Robotic Lawn Mower Market, By Battery Capacity

10.3.2.8.2 Turkey Robotic Lawn Mower Market, By Application

10.3.2.8.3 Turkey Robotic Lawn Mower Market, By Sales Channel

10.3.2.9 Rest of Eastern Europe

10.3.2.9.1 Rest of Eastern Europe Robotic Lawn Mower Market, By Battery Capacity

10.3.2.9.2 Rest of Eastern Europe Robotic Lawn Mower Market, By Application

10.3.2.9.3 Rest of Eastern Europe Robotic Lawn Mower Market, By Sales Channel

10.3.3 Western Europe

10.3.3.1 Western Europe Robotic Lawn Mower Market, By Country

10.3.3.2 Western Europe Robotic Lawn Mower Market, By Battery Capacity

10.3.3.3 Western Europe Robotic Lawn Mower Market, By Application

10.3.3.4 Western Europe Robotic Lawn Mower Market, By Sales Channel

10.3.3.5 Germany

10.3.3.5.1 Germany Robotic Lawn Mower Market, By Battery Capacity

10.3.3.5.2 Germany Robotic Lawn Mower Market, By Application

10.3.3.5.3 Germany Robotic Lawn Mower Market, By Sales Channel

10.3.3.6 France

10.3.3.6.1 France Robotic Lawn Mower Market, By Battery Capacity

10.3.3.6.2 France Robotic Lawn Mower Market, By Application

10.3.3.6.3 France Robotic Lawn Mower Market, By Sales Channel

10.3.3.7 UK

10.3.3.7.1 UK Robotic Lawn Mower Market, By Battery Capacity

10.3.3.7.2 UK Robotic Lawn Mower Market, By Application

10.3.3.7.3 UK Robotic Lawn Mower Market, By Sales Channel

10.3.3.8 Italy

10.3.3.8.1 Italy Robotic Lawn Mower Market, By Battery Capacity

10.3.3.8.2 Italy Robotic Lawn Mower Market, By Application

10.3.3.8.3 Italy Robotic Lawn Mower Market, By Sales Channel

10.3.3.9 Spain

10.3.3.9.1 Spain Robotic Lawn Mower Market, By Battery Capacity

10.3.3.9.2 Spain Robotic Lawn Mower Market, By Application

10.3.3.9.3 Spain Robotic Lawn Mower Market, By Sales Channel

10.3.3.10 Netherlands

10.3.3.10.1 Netherlands Robotic Lawn Mower Market, By Battery Capacity

10.3.3.10.2 Netherlands Robotic Lawn Mower Market, By Application

10.3.3.10.3 Netherlands Robotic Lawn Mower Market, By Sales Channel

10.3.3.11 Switzerland

10.3.3.11.1 Switzerland Robotic Lawn Mower Market, By Battery Capacity

10.3.3.11.2 Switzerland Robotic Lawn Mower Market, By Application

10.3.3.11.3 Switzerland Robotic Lawn Mower Market, By Sales Channel

10.3.3.12 Austria

10.3.3.12.1 Austria Robotic Lawn Mower Market, By Battery Capacity

10.3.3.12.2 Austria Robotic Lawn Mower Market, By Application

10.3.3.12.3 Austria Robotic Lawn Mower Market, By Sales Channel

10.3.3.13 Rest of Western Europe

10.3.3.13.1 Rest of Western Europe Robotic Lawn Mower Market, By Battery Capacity

10.3.3.13.2 Rest of Western Europe Robotic Lawn Mower Market, By Application

10.3.3.13.3 Rest of Western Europe Robotic Lawn Mower Market, By Sales Channel

10.4 Asia-Pacific

10.4.1 Trend Analysis

10.4.2 Asia-Pacific Robotic Lawn Mower Market, By Country

10.4.3 Asia-Pacific Robotic Lawn Mower Market, By Battery Capacity

10.4.4 Asia-Pacific Robotic Lawn Mower Market, By Application

10.4.5 Asia-Pacific Robotic Lawn Mower Market, By Sales Channel

10.4.6 China

10.4.6.1 China Robotic Lawn Mower Market, By Battery Capacity

10.4.6.2 China Robotic Lawn Mower Market, By Application

10.4.6.3 China Robotic Lawn Mower Market, By Sales Channel

10.4.7 India

10.4.7.1 India Robotic Lawn Mower Market, By Battery Capacity

10.4.7.2 India Robotic Lawn Mower Market, By Application

10.4.7.3 India Robotic Lawn Mower Market, By Sales Channel

10.4.8 Japan

10.4.8.1 Japan Robotic Lawn Mower Market, By Battery Capacity

10.4.8.2 Japan Robotic Lawn Mower Market, By Application

10.4.8.3 Japan Robotic Lawn Mower Market, By Sales Channel

10.4.9 South Korea

10.4.9.1 South Korea Robotic Lawn Mower Market, By Battery Capacity

10.4.9.2 South Korea Robotic Lawn Mower Market, By Application

10.4.9.3 South Korea Robotic Lawn Mower Market, By Sales Channel

10.4.10 Vietnam

10.4.10.1 Vietnam Robotic Lawn Mower Market, By Battery Capacity

10.4.10.2 Vietnam Robotic Lawn Mower Market, By Application

10.4.10.3 Vietnam Robotic Lawn Mower Market, By Sales Channel

10.4.11 Singapore

10.4.11.1 Singapore Robotic Lawn Mower Market, By Battery Capacity

10.4.11.2 Singapore Robotic Lawn Mower Market, By Application

10.4.11.3 Singapore Robotic Lawn Mower Market, By Sales Channel

10.4.12 Australia

10.4.12.1 Australia Robotic Lawn Mower Market, By Battery Capacity

10.4.12.2 Australia Robotic Lawn Mower Market, By Application

10.4.12.3 Australia Robotic Lawn Mower Market, By Sales Channel

10.4.13 Rest of Asia-Pacific

10.4.13.1 Rest of Asia-Pacific Robotic Lawn Mower Market, By Battery Capacity

10.4.13.2 Rest of Asia-Pacific Robotic Lawn Mower Market, By Application

10.4.13.3 Rest of Asia-Pacific Robotic Lawn Mower Market, By Sales Channel

10.5 Middle East & Africa

10.5.1 Trend Analysis

10.5.2 Middle East

10.5.2.1 Middle East Robotic Lawn Mower Market, By Country

10.5.2.2 Middle East Robotic Lawn Mower Market, By Battery Capacity

10.5.2.3 Middle East Robotic Lawn Mower Market, By Application

10.5.2.4 Middle East Robotic Lawn Mower Market, By Sales Channel

10.5.2.5 UAE

10.5.2.5.1 UAE Robotic Lawn Mower Market, By Battery Capacity

10.5.2.5.2 UAE Robotic Lawn Mower Market, By Application

10.5.2.5.3 UAE Robotic Lawn Mower Market, By Sales Channel

10.5.2.6 Egypt

10.5.2.6.1 Egypt Robotic Lawn Mower Market, By Battery Capacity

10.5.2.6.2 Egypt Robotic Lawn Mower Market, By Application

10.5.2.6.3 Egypt Robotic Lawn Mower Market, By Sales Channel

10.5.2.7 Saudi Arabia

10.5.2.7.1 Saudi Arabia Robotic Lawn Mower Market, By Battery Capacity

10.5.2.7.2 Saudi Arabia Robotic Lawn Mower Market, By Application

10.5.2.7.3 Saudi Arabia Robotic Lawn Mower Market, By Sales Channel

10.5.2.8 Qatar

10.5.2.8.1 Qatar Robotic Lawn Mower Market, By Battery Capacity

10.5.2.8.2 Qatar Robotic Lawn Mower Market, By Application

10.5.2.8.3 Qatar Robotic Lawn Mower Market, By Sales Channel

10.5.2.9 Rest of Middle East

10.5.2.9.1 Rest of Middle East Robotic Lawn Mower Market, By Battery Capacity

10.5.2.9.2 Rest of Middle East Robotic Lawn Mower Market, By Application

10.5.2.9.3 Rest of Middle East Robotic Lawn Mower Market, By Sales Channel

10.5.3 Africa

10.5.3.1 Africa Robotic Lawn Mower Market, By Country

10.5.3.2 Africa Robotic Lawn Mower Market, By Battery Capacity

10.5.3.3 Africa Robotic Lawn Mower Market, By Application

10.5.3.4 Africa Robotic Lawn Mower Market, By Sales Channel

10.5.3.5 Nigeria

10.5.3.5.1 Nigeria Robotic Lawn Mower Market, By Battery Capacity

10.5.3.5.2 Nigeria Robotic Lawn Mower Market, By Application

10.5.3.5.3 Nigeria Robotic Lawn Mower Market, By Sales Channel

10.5.3.6 South Africa

10.5.3.6.1 South Africa Robotic Lawn Mower Market, By Battery Capacity

10.5.3.6.2 South Africa Robotic Lawn Mower Market, By Application

10.5.3.6.3 South Africa Robotic Lawn Mower Market, By Sales Channel

10.5.3.7 Rest of Africa

10.5.3.7.1 Rest of Africa Robotic Lawn Mower Market, By Battery Capacity

10.5.3.7.2 Rest of Africa Robotic Lawn Mower Market, By Application

10.5.3.7.3 Rest of Africa Robotic Lawn Mower Market, By Sales Channel

10.6 Latin America

10.6.1 Trend Analysis

10.6.2 Latin America Robotic Lawn Mower Market, By Country

10.6.3 Latin America Robotic Lawn Mower Market, By Battery Capacity

10.6.4 Latin America Robotic Lawn Mower Market, By Application

10.6.5 Latin America Robotic Lawn Mower Market, By Sales Channel

10.6.6 Brazil

10.6.6.1 Brazil Robotic Lawn Mower Market, By Battery Capacity

10.6.6.2 Brazil Robotic Lawn Mower Market, By Application

10.6.6.3 Brazil Robotic Lawn Mower Market, By Sales Channel

10.6.7 Argentina

10.6.7.1 Argentina Robotic Lawn Mower Market, By Battery Capacity

10.6.7.2 Argentina Robotic Lawn Mower Market, By Application

10.6.7.3 Argentina Robotic Lawn Mower Market, By Sales Channel

10.6.8 Colombia

10.6.8.1 Colombia Robotic Lawn Mower Market, By Battery Capacity

10.6.8.2 Colombia Robotic Lawn Mower Market, By Application

10.6.8.3 Colombia Robotic Lawn Mower Market, By Sales Channel

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Robotic Lawn Mower Market, By Battery Capacity

10.6.9.2 Rest of Latin America Robotic Lawn Mower Market, By Application

10.6.9.3 Rest of Latin America Robotic Lawn Mower Market, By Sales Channel

11. Company Profiles

11.1 AL-KO

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 The SNS View

11.2 Deere & Company

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 The SNS View

11.3 Flymo

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 The SNS View

11.4 HONDA MOTOR CO., LTD.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 The SNS View

11.5 Husqvarna Group

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 The SNS View

11.6 Robert Bosch GmbH

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 The SNS View

11.7 Robomow Friendly House

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 The SNS View

11.8 STIGA S.p.A.

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 The SNS View

11.9 WIPER S.R.L.

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 The SNS View

11.10 Belrobotics

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 The SNS View

12. Competitive Landscape

12.1 Competitive Benchmarking

12.2 Market Share Analysis

12.3 Recent Developments

12.3.1 Industry News

12.3.2 Company News

12.3.3 Mergers & Acquisitions

13. Use Case and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments

By Battery Capacity

Up to 20V

20V to 30V

More than 30V

By Application

Residential

Commercial

By Sales Channel

Retail Store/Offline

Online Websites

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Chemical Processing Equipment Market was valued at $ 63.60 billion in 2023 and is expected to reach $ 103.82 billion by 2032, at a CAGR of 5.60% from 2024-2032.

The Renting & Leasing Test and Measurement Equipment Market Size was esteemed at USD 6.35 billion in 2023 and is supposed to arrive at USD 9.61 billion by 2032 with a growing CAGR of 4.71% over the forecast period 2024-2032.

The Automatic Labeling Machine Market size was estimated at USD 3.04 billion in 2023 and is expected to reach USD 4.25 billion by 2032 with a growing CAGR of 3.82% during the forecast period of 2024-2032.

The Diaphragm Pump Market Size was estimated at USD 7.26 billion in 2023 and is expected to arrive at USD 11.25 billion by 2032 with a growing CAGR of 4.99% over the forecast period 2024-2032.

The Industrial Boilers Market Size was valued at USD 13.80 Billion in 2023 and is expected to reach USD 20.49 Billion by 2032 and grow at a CAGR of 4.52% over the forecast period 2024-2032.

The Concrete Equipment Market size was valued at USD 18.66 billion in 2023. It is expected to grow to USD 24.97 billion by 2032 and grow at a CAGR of 3.29% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd