Get PDF Sample Copy of Returnable Packaging Market - Request Sample Report

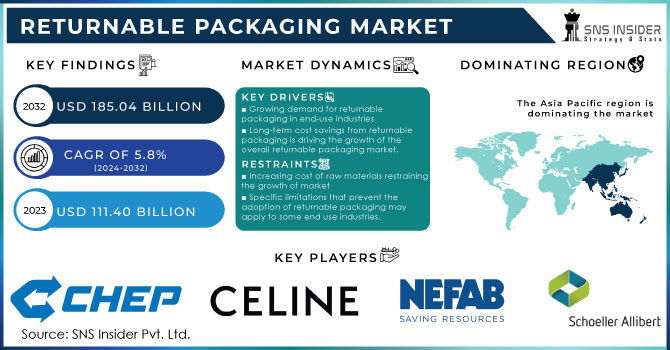

The Returnable Packaging Market size was valued at USD 111.40 billion in 2023 and is expected to Reach USD 185.04 billion by 2032 and grow at a CAGR of 5.8 % over the forecast period of 2024-2032.

The rising demand for robust and long-lasting material handling solutions is anticipated to drive growth in the global market for returnable packaging. Returnable packaging reduces the amount of packaging waste that ends up in landfills and is therefore very environmentally friendly. Market growth is anticipated to be fuelled by end-users growing adoption of green packaging solutions to enhance their brand reputation and by increasing regulatory pressure regarding the use of flexible plastic packaging. With a strong cold storage chain network all over the continent, North America has a thriving food and beverage industry.

Returnable plastic pallets are preferred over single-use wood pallets for the transportation of food and beverages products throughout the cold chain network because, when exposed to moisture, wood pallets are more likely to encourage bacterial and fungal growth. Therefore, increased food and beverage movement throughout the cold chain is anticipated to be advantageous for the local reusable packaging market. As more businesses come to understand the advantages of using sustainable packaging options, there is a rapid rise in the trend toward recyclable packaging in North America. Several factors, such as growing environmental awareness, increasing demand for eco-friendly packaging options, and government initiatives to support sustainable development, are behind this trend.

The use of robust materials, like plastic, metal, and wood, that can be reused numerous times before being recycled or disposed of, is one of the main trends in returnable packaging. In place of single-use packaging, which creates a lot of waste and is bad for the environment, these materials offer a more affordable and environmentally responsible option.

Additionally, returning pallets has a number of benefits, such as less waste, greater effectiveness, and cost savings. As a result, more businesses are incorporating these pallets into their supply chain management procedures. Using returnable pallets, companies can achieve sustainability goals and lessen their damaging environmental impact.

KEY DRIVERS:

Growing demand for returnable packaging in end-use industries

Different industries searching for affordable and sustainable solutions are the ones driving the demand for returnable packaging. Returnable packaging is being adopted by a variety of industries, including those in the automotive, retail, consumer goods, food and beverage, pharmaceutical, manufacturing, e-commerce, agriculture, electronics, and more, in order to improve product protection, reduce waste, and optimize logistics.

Long-term cost savings from returnable packaging is driving the growth of the overall returnable packaging market.

RESTRAIN:

Increasing cost of raw materials restraining the growth of market

During the forecast period the prices of raw materials and energy will increase. The increased raw materials prices will affect the growth of market and affect the value chain, resulting in rise of operation cost.

Specific limitations that prevent the adoption of returnable packaging may apply to some end use industries.

OPPORTUNITY:

The development of technology opens up possibilities for returnable packaging system optimization

Supply chain management software, Internet of Things (IoT) sensors, RFID tracking, data analytics, and other technologies can be integrated to provide real-time visibility, asset tracking, and improved decision-making capabilities, which can improve operational effectiveness and customer satisfaction.

Returnable packaging has lots of opportunities for innovation in terms of both functionality and design.

CHALLENGES:

Varying environmental laws and regulations across different regions

The environmental laws and policies governing packaging waste and sustainability can vary greatly from one nation to the next. Due to the need to navigate and adhere to various sets of regulations, businesses that operate across multiple regions or engage in international trade are made more difficult.

According to the European Federation of Wooden Pallet and Packaging Manufacturers, there will be pressure on the supply of wooden pallets and packaging as the conflict in Ukraine affects the supply of wood.

The organization, which represents manufacturers in the EU and the UK, expressed "deep sympathies and support for the people of Ukraine," saying the virtual shutdown of the Ukrainian economy would have "serious direct impacts on countries like Hungary, Italy, and Germany and an indirect impact across Europe by unbalancing the market, increasing competition for more limited wood supplies, and putting upward pressure

More than 215 million m3 of sawn softwood timber was exported from Ukraine last year, a large portion of which went toward the production of wooden pallets and packaging for use in countries like France, Germany, Italy, the Netherlands, and Poland. An estimated 16 million pallets were also produced and exported, mostly to Europe.

While Belarus exports about 3 mm3 and Russia exports about 4.3mm3 of softwood lumber to the EU, respectively, the trade sanctions that have been put in place against the two nations will have a significant effect on Europe. .

Up to 25% of the pallet and packaging wood used in some nations comes from these three nations. Alternative timber sources, such as those in Germany, the Baltic States, and Scandinavia, can only make up a small portion of the deficit.

The conflict has also significantly disrupted energy supplies, resulting in a more than 35% increase in the price of gasoline and a barrel of oil now costing more than US$100. According to FEFPEB, this would have a significant impact on production costs as a whole, resulting in inevitably higher prices.

Packaging needs will decline due to the recession, and the shutdown will cause paper waste to start going to landfills.

Gas prices have an impact on European paper mills. However, the lack of orders for finished goods is currently the main issue. This is a result of the economy's slowdown and expectations that a severe economic crisis will cause demand for packaging to fall precipitously. There were still warehouses that were overstocked due to the expectation of high demand.

Supply chain optimization efforts may prioritize the use of returnable packaging to enhance efficiency and minimize waste.

By Raw Material

Wood

Metal

Plastic

By Product Type

Crates

IBCs

Dunnage

Pallets

Barrels & Drums

Others

By Application

Food & Beverage

Healthcare

Automotive

Others

Due to the region's rapidly expanding manufacturing sector, particularly in nations like India, China, and Japan, Asia Pacific held a market share of over 35% in the regional segment in 2023. Furthermore, the region has a very high availability of raw materials like metal and plastic.

China produces 35% of the world's plastic, which is advantageous to manufacturers in terms of the cost and accessibility of raw materials. The largest importer and exporter of food, drink, and agri-food products, China is a significant economy in the Asia Pacific market for returnable packaging, with a share expected to reach over 45% in 2023.

Considering the size of the pharmaceutical, food and beverage, and automotive industries in the US, North America held the second-largest market share with over 28 % in 2023. The segment's largest share in 2022 is primarily attributable to the robustness, affordability, and lightweight of reusable packaging containers made of plastic. Further fuelling the market expansion is the regional trend toward recyclable packaging, which is accelerating as more businesses come to understand the advantages of using eco-friendly packaging options.

Get Customized Report as per Your Business Requiremrnt - Enquiry Now

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

South Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of the Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin American

Some major key players in the Returnable packaging market are Schoeller Allibert, CHEP, NEFAB GROUP, Celina, RPP Containers, Amatech Inc, UBEECO Packaging Solutions, PPS Midlands Limited, RPR Inc, Tri-pack Packaging Systems Ltd, and other players.

McDonald, Fast food giant McDonald's has partnered with logistics and supply chain firm Havi, and Burger King's rival is working with reusable packaging initiative Recup to create national deposit systems for reusable cups in Germany.

Nestle, Food giant Nestlé is experimenting with using reusable stainless steel containers for its Nesquik cocoa brand in Germany. These containers were rented from start-up Circolution.

| Report Attributes | Details |

| Market Size in 2023 | US$ 111.40 Bn |

| Market Size by 2032 | US$ 185.04 Bn |

| CAGR | CAGR of 5.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Raw Material (Wood, Metal, Plastic) • by Product Type (Crates, IBCs, Dunnage, Pallets, Barrels & Drums, Others) • by Application (Food & Beverage, Healthcare, Automotive, Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Schoeller Allibert, CHEP, NEFAB GROUP, Celina, RPP Containers, Amatech Inc, UBEECO Packaging Solutions, PPS Midlands Limited, RPR Inc, Tri-pack Packaging Systems Ltd |

| Key Drivers | • Growing demand for returnable packaging in end-use industries • Long-term cost savings from returnable packaging is driving the growth of the overall returnable packaging market. |

| Market Opportunities | • The development of technology opens up possibilities for returnable packaging system optimization • Returnable packaging has lots of opportunities for innovation in terms of both functionality and design. |

Ans: Returnable Packaging Market is expected to grow at a CAGR of 5.8% over the forecast period of 2024-2032.

Ans: The Returnable Packaging Market size was USD 111.40 Bn in 2023 and is expected to Reach USD 185.04 Bn by 2032.

Ans: Growing demand for returnable packaging in end-use industries.

Ans: Some major key players in the Returnable packaging market are Schoeller Allibert, CHEP, NEFAB GROUP, Celina, RPP Containers, Amatech Inc, UBEECO Packaging Solutions, PPS Midlands Limited, RPR Inc, Tri-pack Packaging Systems Ltd.

Ans: Asia Pacific held a market share of over 35% in the regional segment in 2023 and will continue to dominate the market.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Russia-Ukraine War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

4.3 Supply Demand Gap Analysis

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Returnable Packaging Market Segmentation, By Raw Material

8.1 Wood

8.2 Metal

8.3 Plastic

9. Returnable Packaging Market Segmentation, By Product Type

9.1 Crates

9.2 IBCs

9.3 Dunnage

9.4 Pallets

9.5 Barrels & Drums

9.6 Others

10. Returnable Packaging Market Segmentation, By Application

10.1 Food & Beverage

10.2 Healthcare

10.3 Automotive

10.4 Others

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Returnable Packaging Market by Country

11.2.2North America Returnable Packaging Market By Raw Material

11.2.3 North America Returnable Packaging Market By Product Type

11.2.4 North America Returnable Packaging Market By Application

11.2.6 USA

11.2.6.1 USA Returnable Packaging Market By Raw Material

11.2.6.2 USA Returnable Packaging Market By Product Type

11.2.6.3 USA Returnable Packaging Market by Application

11.2.7 Canada

11.2.7.1 Canada Returnable Packaging Market By Raw Material

11.2.7.2 Canada Returnable Packaging Market By Product Type

11.2.7.3 Canada Returnable Packaging Market By Application

11.2.8 Mexico

11.2.8.1 Mexico Returnable Packaging Market By Raw Material

11.2.8.2 Mexico Returnable Packaging Market By Product Type

11.2.8.3 Mexico Returnable Packaging Market By Application

11.3 Europe

11.3.1 Europe Returnable Packaging Market by Country

11.3.2 Europe Returnable Packaging Market By Raw Material

11.3.3 Europe Returnable Packaging Market By Product Type

11.3.4 Europe Returnable Packaging Market By Application

11.3.6 Germany

11.3.6.1 Germany Returnable Packaging Market By Raw Material

11.3.6.2 Germany Returnable Packaging Market By Product Type

11.3.6.3 Germany Returnable Packaging Market By Application

11.3.7 UK

11.3.7.1 UK Returnable Packaging Market By Raw Material

11.3.7.2 UK Returnable Packaging Market By Product Type

11.3.7.3 UK Returnable Packaging Market By Application

11.3.8 France

11.3.8.1 France Returnable Packaging Market By Raw Material

11.3.8.2 France Returnable Packaging Market By Product Type

11.3.8.3 France Returnable Packaging Market By Application

11.3.9 Italy

11.3.9.1 Italy Returnable Packaging Market By Raw Material

11.3.9.2 Italy Returnable Packaging Market By Product Type

11.3.9.3 Italy Returnable Packaging Market By Application

11.3.10 Spain

11.3.10.1 Spain Returnable Packaging Market By Raw Material

11.3.10.2 Spain Returnable Packaging Market By Product Type

11.3.10.3 Spain Returnable Packaging Market By Application

11.3.11 The Netherlands

11.3.11.1 Netherlands Returnable Packaging Market By Raw Material

11.3.11.2 Netherlands Returnable Packaging Market By Product Type

11.3.11.3 Netherlands Returnable Packaging Market By Application

11.3.11 Rest of Europe

11.3.11.1 Rest of Europe Returnable Packaging Market By Raw Material

11.3.11.2 Rest of Europe Returnable Packaging Market By Product Type

11.3.11.3 Rest of Europe Returnable Packaging Market By Application

11.4 Asia-Pacific

11.4.1 Asia Pacific Returnable Packaging Market by Country

11.4.2 Asia Pacific Returnable Packaging Market By Raw Material

11.4.3 Asia Pacific Returnable Packaging Market By Product Type

11.4.4Asia Pacific Returnable Packaging Market By Application

11.4.6 Japan

11.4.6.1 Japan Returnable Packaging Market By Raw Material

11.4.6.2 Japan Returnable Packaging Market By Product Type

11.4.6.3 Japan Returnable Packaging Market By Application

11.4.7 South Korea

11.4.7.1 South Korea Returnable Packaging Market By Raw Material

11.4.7.2 South Korea Returnable Packaging Market By Product Type

11.4.7.3 South Korea Returnable Packaging Market By Application

11.4.8 China

11.4.8.1 China Returnable Packaging Market By Raw Material

11.4.8.2 China Returnable Packaging Market By Product Type

11.4.8.3 China Returnable Packaging Market By Application

11.4.9 India

11.4.9.1 India Returnable Packaging Market By Raw Material

11.4.9.2 India Returnable Packaging Market By Product Type

11.4.9.3 India Returnable Packaging Market By Application

11.4.10 Australia

11.4.10.1 Australia Returnable Packaging Market By Raw Material

11.4.10.2 Australia Returnable Packaging Market By Product Type

11.4.10.3 Australia Returnable Packaging Market By Application

11.4.11 Rest of Asia-Pacific

11.4.11.1 APAC Returnable Packaging Market By Raw Material

11.4.11.2 APAC Returnable Packaging Market By Product Type

11.4.11.3 APAC Returnable Packaging Market By Application

11.5 The Middle East & Africa

11.5.1 The Middle East & Africa Returnable Packaging Market by Country

11.5.2 The Middle East & Africa Returnable Packaging Market By Raw Material

11.5.3 The Middle East & Africa Returnable Packaging Market By Product Type

11.5.4The Middle East & Africa Returnable Packaging Market By Application

11.5.6 Israel

11.5.6.1 Israel Returnable Packaging Market By Raw Material

11.5.6.2 Israel Returnable Packaging Market By Product Type

11.5.6.3 Israel Returnable Packaging Market By Application

11.5.7 UAE

11.5.7.1 UAE Returnable Packaging Market By Raw Material

11.5.7.2 UAE Returnable Packaging Market By Product Type

11.5.7.3 UAE Returnable Packaging Market By Application

11.5.8 South Africa

11.5.8.1 South Africa Returnable Packaging Market By Raw Material

11.5.8.2 South Africa Returnable Packaging Market By Product Type

11.5.8.3 South Africa Returnable Packaging Market By Application

11.5.9 Rest of Middle East & Africa

11.5.9.1 Rest of Middle East & Asia Returnable Packaging Market By Raw Material

11.5.9.2 Rest of Middle East & Asia Returnable Packaging Market By Product Type

11.5.9.3 Rest of Middle East & Asia Returnable Packaging Market By Application

11.6 Latin America

11.6.1 Latin America Returnable Packaging Market by Country

11.6.2 Latin America Returnable Packaging Market By Raw Material

11.6.3 Latin America Returnable Packaging Market By Product Type

11.6.4 Latin America Returnable Packaging Market By Application

11.6.6 Brazil

11.6.6.1 Brazil Returnable Packaging Market By Raw Material

11.6.6.2 Brazil Africa Returnable Packaging Market By Product Type

11.6.6.3 Brazil Returnable Packaging Market By Application

11.6.7 Argentina

11.6.7.1 Argentina Returnable Packaging Market By Raw Material

11.6.7.2 Argentina Returnable Packaging Market By Product Type

11.6.7.3 Argentina Returnable Packaging Market by By Application

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Returnable Packaging Market By Raw Material

11.6.8.2 Rest of Latin America Returnable Packaging Market By Product Type

11.6.8.3 Rest of Latin America Returnable Packaging Market By Application

12 Company Profile

12.1 Schoeller Allibert

12.1.1 Market Overview

12.1.2 Financials

12.1.3 Product/Services/Offerings

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 CHEP

12.2.1 Market Overview

12.2.2 Financials

12.2.3 Product/Services/Offerings

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 NEFAB GROUP

12.3.1 Market Overview

12.3.2 Financials

12.3.3 Product/Services/Offerings

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Celina

12.4.1 Market Overview

12.4.2 Financials

12.4.3 Product/Services/Offerings

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 RPP Containers

12.5.1 Market Overview

12.5.2 Financials

12.5.3 Product/Services/Offerings

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Amatech Inc

12.6.1 Market Overview

12.6.2 Financials

12.6.3 Product/Services/Offerings

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 UBEECO Packaging Solutions

12.7.1 Market Overview

12.7.2 Financials

12.7.3 Product/Services/Offerings

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 PPS Midlands Limited

12.8.1 Market Overview

12.8.2 Financials

12.8.3 Product/Services/Offerings

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 RPR Inc

12.9.1 Market Overview

12.9.2 Financials

12.9.3 Product/Services/Offerings

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Tri-pack Packaging Systems Ltd

12.10.1 Market Overview

12.10.2 Financials

12.10.3 Product/Services/Offerings

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

14. USE Cases and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Thermoform Packaging Market Size was valued at USD 52.5 billion in 2023 and is projected to reach USD 76.10 billion by 2031 and grow at a CAGR of 4.75% over the forecast periods 2024 -2031.

The Brick Carton Packaging Market size was USD 11.54 Billion in 2023 and will reach USD 17.60 Billion by 2032 and grow at a CAGR of 4.81% by 2024-2032.

The Spouted Pouch Market size was USD 25.45 billion in 2023 and is expected to Reach USD 41.80 billion by 2031 and grow at a CAGR of 6.4% over the forecast period of 2024-2031.

The Modified Atmosphere Packaging market size was USD 16.5 billion in 2023 and is expected to Reach USD 23.73 billion by 2031 and grow at a CAGR of 4.5% over the forecast period of 2024-2031.

The Industrial Drum Market size was USD 12.96 billion in 2023 and is expected to Reach USD 23.98 billion by 2031 and grow at a CAGR of 8% over the forecast period of 2024-2031.

The Retail Ready Packaging Market size was USD 74.7 billion in 2023 and is expected to Reach USD 107 billion by 2031 and grow at a CAGR of 4.6% over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd