Remote Weapon Stations Market Report Scope & Overview:

To get more information on Remote Weapon Stations Market - Request Free Sample Report

The Remote Weapon Stations Market Size was valued at US$ 6.70 billion in 2023 and is expected to grow to US$ 8.50 billion by 2031 at a CAGR of 3.02% over the forecast period 2024-2031.

A remote weapon station is a remotely controlled equipment used in open conflict conditions that allows soldiers to detect and engage targets with accuracy and safety by operating from a protected remote position using precise imaging systems, reducing collateral damage. It includes firing units, a remote control system, optical and imaging systems, acoustic devices, and other upgrades. Remote weapon stations can be installed in moving or stationary offensive units and are utilised in ground vehicles, ships, and aircraft.The rise in cross-border conflicts, peacekeeping, and humanitarian missions is driving the global remote weapon station industry. This poses a persistent threat to defence and civilian assets around the world. Furthermore, the increased use of UAVs for geolocation by adversaries compromises army locations, increasing the threat to army assets. Countries are establishing weapon stations in conflict-prone locations where soldiers represent a major hazard to their lives in order to avert such situations.

MARKET DYNAMICS

KEY DRIVERS

-

Various countries are increasing their demand for remote weapon stations for military applications.

-

There is an increasing demand for high-precision remote weapon stations.

RESTRAINTS

-

Increased development expenses and a larger capital need

OPPORTUNITIES

-

Military Modernization Programs in Various Countries Around the World

-

Rising Defense Expenditure by Emerging Markets

CHALLENGES

-

The Difficulty of Integrating Remote Weapon Stations With a Diverse Range of Platforms

-

Stabilized Remote Weapon Stations Have a High Development Cost

THE IMPACT OF COVID-19

The manufacturing sector of the remote weapon station industry was severely impacted by the pandemic. The output rate was drastically lowered, as with any other industry vertical. Because of the change in demand, the economic crisis and the growth of the homeland security segment were impacted. Previous investment plans from affluent countries predicted expansion in the remote weapon station business during the pandemic.

Based on platform, the land segment is likely to lead the remote weapon station market and will do so for the foreseeable future. Emerging countries, including China and India, are amassing massive numbers of Infantry Fighting Vehicles and armoured vehicles. These countries are increasing their investments in automated technology and focusing on the production of a diverse variety of offensive fighting vehicles.

The remote weapon station market has been examined and classified into three components human machine interface, sensors, and weapons and armaments. The guns and armaments category dominates the remote weapon station market. During the projection period, the sensors segment is expected to increase at the fastest CAGR. This expansion can be ascribed to the usage of sensor fusion technology and the sensor suite, which is constantly being upgraded to provide improved detection and decision-making. Combining data from important sensors gives the warrior the capacity to autonomously evaluate the whole tactical environment and respond quickly to identify dangers.

The remote weapon station market has been divided into close-in weapon system, remote controlled gun system, and others based on technology. The remote weapon station market's close-in weapon system category is expected to develop at the fastest CAGR during the forecast period. The expansion of the close-in weapon system segment may be ascribed to increased R&D activities worldwide for the development of sophisticated technologies, as well as improved weapon system reliability and unmanned operations.

Value Chain Analysis

Due to the increasing number of asymmetric warfare and modernization programme across the sector, the remote weapon stations market is generating a bigger market share in recent years. The emerging economies are significantly increasing military spending; on the other hand, the leading market players have been collaborating and implementing various tactics in recent years, which are regarded as the major drivers of market growth.

The majority of remote weapon stations are outfitted with a variety of sensors for improved performance, greater detection, and faster decision-making on the job. Thermal imagers, laser range finders, day imagers, and other modern sensors, for example, are playing an important role in the growth of the remote weapon station industry. Furthermore, better gun systems with faster responses are improving the performance of remote weapon stations, which is driving the overall expansion of the remote weapon stations market in recent years.

KEY MARKET SEGMENTATION

By Component

-

Sensors

-

HMI

-

Weapons & Armaments

By Weapon Type

-

Lethal

-

Non-lethal

By Mobility

-

Stationary

-

Moving

By Technology

-

Remote Controlled Gun Systems

-

Others

By Application

-

Military

By Platform

-

Land

-

Airborne

-

Naval

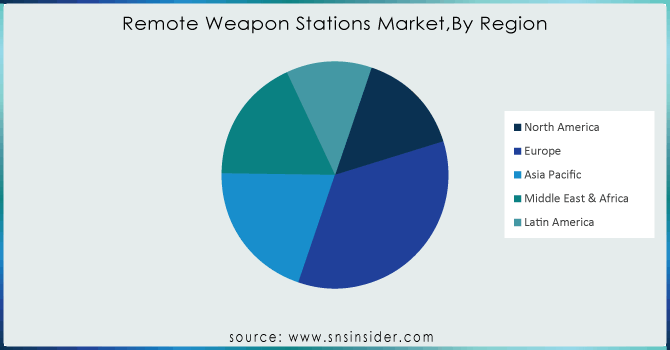

REGIONAL ANALYSIS

Europe is expected to lead the remote weapon station market, while the Asia Pacific region is expected to rise at a faster rate over the forecast period. In Europe, the primary markets for remote weapon stations include the United Kingdom, France, Russia, Italy, and Germany. The market's expansion in European countries is primarily attributed to technological advancements and rising incidences of armed conflicts or war against terrorism, as well as recent geopolitical events triggered by Russia, which have prompted many Eastern European countries to strengthen their defence capabilities.

Need any customization research on Remote Weapon Stations Market - Enquiry Now

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS

The Major Players are Saab AB, General Dynamics Ordnance, Tactical Systems, Moog Inc., Leonardo S.p.A., Kongsberg Defence Systems, Kollmorgen Elbit Systems Land and C4I Ltd., MERRILL, Singapore Technologies Engineering Ltd., Electro Optic Systems Pty Ltd & Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 6.70 Million |

| Market Size by 2031 | US$ 8.50 Million |

| CAGR | CAGR of 3.02% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Sensors, HMI, Weapons & Armaments) • By Weapon Type (Lethal, Non-lethal) • By Mobility(Stationary, Moving) • By Technology(Close-in Weapon Systems, Remote Controlled Gun Systems, Others) • By Application (Military, Homeland Security) • By Platform (Land, Airborne, Naval) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Saab AB, General Dynamics Ordnance and Tactical Systems, Moog Inc., Leonardo S.p.A., Kongsberg Defence Systems, Kollmorgen Elbit Systems Land and C4I Ltd., MERRILL, Singapore Technologies Engineering Ltd., Electro Optic Systems Pty Ltd. |

| KEY DRIVERS | • Various countries are increasing their demand for remote weapon stations for military applications. •There is an increasing demand for high-precision remote weapon stations. |

| Restraints | • Increased development expenses and a larger capital need |