The Ransomware Protection Market was valued at USD 25.59 billion in 2023 and is expected to reach USD 91.80 billion by 2032, growing at a CAGR of 15.29% over the forecast period 2024-2032.

To get more information on Ransomware Protection Market - Request Free Sample Report

The Global Ransomware Protection Market is growing due to the rise in ransomware attacks worldwide. There are increasing cyber threats to critical data for organizations, and financial losses due to operational disruptions. Ransomware evolution sandbox and its ways to target vulnerabilities in systems it is notorious for big exploits in industries from healthcare BFSI, and manufacturing dealing with sensitive data. As this threat landscape continues to grow, more and more businesses are looking for strong cybersecurity solutions which, in turn, is developing the market for ransomware protection solutions and services. Moreover, increasing regulatory compliance mandates around data security, and data privacy are making organizations spend on advanced security posture. Over 59% of organizations are targeted for Ransomware attacks and the average ransom demand in 2024 is USD 5.2 million. After the attacks, companies endured an average of 24 days of downtime. Ransomware protection was up 32% in spending, and 16 U.S. states enacted or updated data privacy and cybersecurity laws, covering more than 70% of businesses. More than 150 hospitals around the world were affected as healthcare organizations witnessed a 35% rise in ransomware attacks.

One more important contributing element boosting the market development is to increase the extent of digitalization and cloud-based areas. These technologies can make an organization more efficient in terms of operation but can also expand the attack surface, making it more vulnerable to cyber-attacks. Endpoint protection, network security, and managed security services are becoming the standard for businesses to protect their critical digital assets. In addition, increasing recognition of the economic and image costs of ransomware attacks is forcing enterprises and SMEs to raise their efforts in advance of security. According to an analysis, this ransomware protection market is expected to grow in upcoming years, due to the rising ransomware attacks and the need for real-time monitoring along with the protection of businesses coupled with technological advancements in AI-based threat detection. By 2024, more than 94% of enterprises will use cloud services, and 62% have experienced a cyberattack targeting cloud infrastructure. Also, 70% of organizations have a fast-paced digital transformation that has led to increased cyber risk exposure and 73% of enterprises have integrated endpoint security into core security strategies.

Key Drivers:

Rising IoT Adoption and Vulnerabilities Fueling Increased Ransomware Attacks Driving Demand for Advanced Protection

The rise in adoption of the Internet of Things (IoT) and connected devices is leading to an increase in the ransomware protection market. IoT devices can improve operational efficiency and allow for data-based decisions, but most of them have poor security processes that make them vulnerable to ransomware attacks. But when industries, including manufacturing and smart cities, and of course healthcare, embed IoT solutions into their ecosystems, the threat posed by ransomware multiplies exponentially. This increased focus on the need for securing IoT networks and endpoints has compelled organizations to start adopting advanced ransomware protection solutions like network segmentation, endpoint security, and Intrusion Detection Systems. This is leading to market growth as companies struggle to secure their ecosystems from bad actors targeting IoT weaknesses. In 2024, 53% of IoT devices held critical vulnerabilities with the number of cyberattacks against IoT devices increasing by 107% year on year to 4.3 billion attacks globally. Ransomware attacks on IoT devices comprised 40% of all attacks in healthcare, while 29% of smart cities saw ransomware attacks on their IoT infrastructure.

Remote Work and Hybrid Environments Drive Increased Ransomware Risks Boosting Demand for Advanced Security Solutions

The other big factor is the enforcement of remote work and hybrid work environments, which has significantly increased the attack surface targeted by ransomware actors. The number of entries for ransomware attacks has expanded due to workers logging into corporate networks from multiple places and devices. Together with the above process, demand for endpoint security, secure web gateways, and cloud-based ransomware protection tools has gone up. Other organizations are also focusing on employee training and phishing simulation tools to minimize human errors which are still among the highest contributing factors to ransomware incidents. Also, businesses are using zero-trust architectures and multifactor authentication to guard against ransomware in greater numbers. With remote and hybrid work culture here to stay, the need for such solutions will only continue to grow, thereby pushing the market ahead. Remote or hybrid work will be offered by 65% of organizations in 2024, bringing increased attack surface. Phishing attacks caused 80% of all security breaches, and 61% of companies embraced Zero Trust security models, compared to 24% in 2021. Upon closer examination, 34% of medium businesses and 27% of small businesses used MFA, endpoint security solutions grew by 25% in demand, and 42% of companies used a secure web gateway.

Restrains:

Challenges in Deploying Next Generation Ransomware Protection Solutions Amid Evolving Threats and Skill Shortages

One of the major drawbacks of the ransomware protection market is the difficulty in deploying next-generation security solutions into existing IT infrastructure. A lot of organizations especially small and medium-sized enterprises (SMEs) still run legacy systems incapable of playing ball with contemporary ransomware defenses. Simplicity of Deployment It is easier to initiate security problems with a solution-to-solution network-to-cloud solution (isolation) which does not have a (common) standard. The biggest issue would be ransomware playing catch-up. As cybercriminals become more sophisticated, they continue to create new means to bypass traditional security, such as leveraging zero-day vulnerabilities and multi-layer attack methods. Organizations struggle to constantly update ransomware protection to appease this continually evolving threat landscape. Not to mention that there is a shortage of skilled cybersecurity professionals, which complicates things even more, making it difficult for a lot of companies to implement the necessary protection strategies, let alone sustain them. The difficulties pointed out here highlight the importance of continued training, collaboration, and investment in cybersecurity solutions.

By Solution

Standalone Anti-Ransomware Software was the leading segment in 2023 with a 34.7% market share as the segment is specifically aimed at countering ransomware threats. These solutions are built for ransomware detection, protection, and remediation, so they enable organizations to directly attack one of the top security pain points. Due to their high degree of effectiveness in recognizing patterns of ransomware and blocking it before it can carry out encryption, they have been fast becoming a go-to option for companies, especially in high data sensitivity sectors like BFSI, healthcare, and retail. In addition, their simplicity of deployment and integration with existing security frameworks have made them popular.

End-Point Security is expected to grow at the highest CAGR between 2024 and 2032 due to the surge in remote & hybrid work environments. Ransomware attackers have now honed in on endpoints as one of the two main targets with employees working remotely from various places and devices accessing corporate networks. Today, the best endpoint security solutions come equipped with advanced technology such as real-time threat detection, behavioral analytics, and response capabilities, making them indispensable to organizations looking for comprehensive protection. The growth of Bring Your Own Device (BYOD) policies and the number of IoT devices connected to corporate networks also drive the need for strong endpoint security, further propelling its expansion.

By Service

In 2023, the ransomware protection market share for managed services was leading with 45.9% and is projected to witness the fastest growth throughout the forecast period, 2024-2032. The growing share of managed services can be attributed to their low-cost provision, providing organizations with rich end-to-end security to monitor, detect, and respond to threats without the demand for heavy in-house expertise. As the nature of ransomware attacks continues to shift, organizations are turning to managed service providers (MSPs) to address complex cybersecurity problems. This is especially beneficial for SMEs, whose resources typically prevent them from maintaining dedicated cybersecurity teams. The expected rapid growth of managed services is due to the increasing take-up of cloud solutions, hybrid work, and the need for around-the-clock security monitoring. With the help of managed services, businesses can leave their networks and endpoints as well as perimeters protected from ransomware attacks while focusing on operations.

By Industry Vertical

In 2023, BFSI (Banking, Financial Services, and Insurance) held the largest ransomware protection market share of 28.5% as the sector is more susceptible to cyberattacks. The nature of this industry deals with massive amounts of sensitive financial and personal data, which leads it to be a top target for ransomware campaigns. Investments in ransomware protection are also being fuelled by regulatory requirements PCI DSS, GDPR, etc. that are causing BFSI organizations to adopt superlative security measures to protect customer trust as well as compliance. Furthermore, digital transformation to online banking and mobile banking has also resulted in the rising attack surface, which makes the requirement for even more backup ransomware in the field of banking.

IT & Telecom is projected to attain the highest CAGR from 2024 to 2032 as it serves as the backbone for digital infrastructure across sectors. As the scale of 5G networks, cloud computing, and IoT grows, the IT & Telecom industry has broadened assault surfaces in terms of high-impact ransomware attacks that tend to target critical infrastructure and customer data. As a result, companies in this sector are focusing on endpoint security, network security, and real-time threat detection to protect their business. The need for advanced ransomware protection is driven even more by the sector's increasingly essential role in hybrid work and continued connectivity, earmarking it for outsized growth in the years to come.

By Deployment Mode

In 2023, cloud solutions captured a majority of the ransomware protection market, with a 58.6% share, and are anticipated to grow at the highest CAGR during the forecast period (2024 − 2032). This overwhelming prevalence is primarily due to the steady and growing interest of all industries to adopt cloud computing, having their operations, data, and apps in cloud environments. The scalability, flexibility, and ease of deployment offered by cloud-based ransomware protection solutions are driving higher adoption across organizations of all sizes. Additionally, they offer high-end capabilities, such as real-time threat detection, automatic updates, and centralized management, making them ideal solutions for distributed networks and remote workforces. Cloud-native security solutions are best at tracking multiple endpoints, networks, and applications in combating the new age of sophisticated ransomware threats in diverse and dispersed IT environments. Additionally, the shift towards multi-cloud and hybrid cloud is creating a growing need for integrated ransomware protection tools capable of catering to those ecosystems. Meanwhile, ongoing developments in artificial intelligence and machine learning regarding threat detection and prediction within cloud security systems will lead to further growth of cloud-oriented solutions over the next few years.

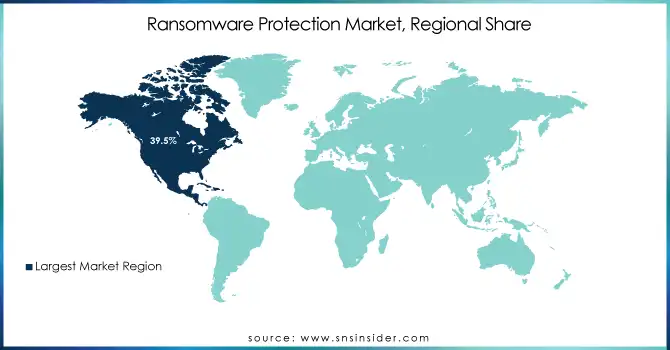

North America led the market, accounting for 39.5% market share in 2023 due to technological advancements, the high spending capability of the population, and strong infrastructure in countries like the U. S., Canada, and Mexico. Leading cognitive assessment and training companies such as Pearson, Cogstate, Lumosity, etc. provide cognitive testing and brain-training solutions in these regions that are utilized in several industries including healthcare, education, business, etc. Cognitive testing is critical in the diagnosis of Alzheimer’s, dementia, and other neurodegenerative diseases a healthcare application. It provides tools that allow healthcare providers to monitor mental health and cognitive decline. In addition, tools measuring cognitive ability are employed in workplaces and schools for hiring, employee training, and productivity efficiency. North America holds a significant market share owing to the high adoption of digital tools and e-learning solutions at various educational institutions and corporations.

Asia Pacific is anticipated to register the fastest compound annual growth rate (CAGR) between 2024 to 2032, owing to the rising economies and adoption of cognitive assessment and training solutions, advancement of technology, and growing demand for improving mental health and skills development. Various regions such as China, India, Japan, and South Korea are investing heavily in artificial intelligence, huge data, and digital learning, and are expected to drive the market growth during the forecast period. In fact, Japan is implementing cognitive training solutions in the education sector to improve learning and in workplaces to enhance workforce development. Meanwhile, e-learning platforms have boomed in China together with the development of AI-enabled cognitive assessment tools and shifting people toward new ways of learning and recruiting landscape. Additionally, mental wellness and cognitive health have become a key focus, with increased demand for effective cognitive assessment solutions across industries, including education, healthcare, and corporate. Consequently, Asia Pacific is emerging as a pivotal market for the cognitive training and assessment industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the major players in the Ransomware Protection Market are:

Microsoft (Microsoft Defender, Azure Sentinel)

Cisco Systems (Cisco Umbrella, Cisco Secure Endpoint)

CrowdStrike (Falcon Prevent, Falcon Insight)

Palo Alto Networks (Cortex XDR, Prisma Cloud)

Sophos (Intercept X, XG Firewall)

Trend Micro (Worry-Free Business Security, Deep Discovery)

Check Point Software (ThreatCloud, SandBlast)

Fortinet (FortiGate, FortiEDR)

McAfee (McAfee Total Protection, MVISION Endpoint Security)

FireEye (Helix, Endpoint Security)

Kaspersky Lab (Kaspersky Anti-Virus, Kaspersky Endpoint Security)

ESET (ESET NOD32 Antivirus, ESET Endpoint Security)

Carbon Black (VMware Carbon Black Cloud, Carbon Black Response)

Bitdefender (Bitdefender GravityZone, Bitdefender Antivirus)

Acronis (Acronis Cyber Protect, Acronis True Image)

Barracuda Networks (Barracuda Web Security Gateway, Barracuda Backup)

Veeam (Veeam Backup & Replication, Veeam Availability Suite)

Symantec (Symantec Endpoint Protection, Symantec Advanced Threat Protection)

Mimecast (Mimecast Email Security, Mimecast Targeted Threat Protection)

Zscaler (Zscaler Internet Access, Zscaler Private Access)

Some of the Raw Material Suppliers for Ransomware Protection Companies:

Intel

NVIDIA

Micron Technology

Broadcom

Seagate Technology

Western Digital

Cisco Systems

Samsung Electronics

Qualcomm

AMD

In November 2024, Palo Alto Networks confirmed the exploitation of a critical zero-day vulnerability in its PAN-OS firewall, allowing remote command execution. The company has released patches and urges users to secure their management interfaces.

In February 2024, Sophos MDR and XDR services now integrate with Veeam Backup & Replication, enhancing ransomware protection and backup data security. This integration allows better detection and response to threats targeting backup systems.

In March 2024, Broadcom merged its Symantec and Carbon Black divisions into a new Enterprise Security Group to enhance endpoint and network protection. The move aims to provide integrated, comprehensive security solutions for enterprises.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 25.59 Billion |

| Market Size by 2032 | USD 91.80 Billion |

| CAGR | CAGR of 15.29% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Standalone Anti-Ransomware Software, End-Point Security, Network Security, Secure Web Gateways) • By Service (Managed, Consulting, Support & Management) • By Industry Vertical (BFSI, IT & Telecom, Healthcare, Education, Manufacturing, Retail) • By Deployment Mode (Cloud, On-Premise) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM, Samsung, Adobe, Anthology, SMART Technologies, Oracle, SAP, Microsoft, Cornerstone OnDemand, Pearson, BenQ, Google, McGraw Hill, Cisco, Huawei, D2L, Ellucian, Alphabet Inc., Upside LMS, Edsys |

| Key Drivers | • Rising IoT Adoption and Vulnerabilities Fueling Increased Ransomware Attacks Driving Demand for Advanced Protection • Remote Work and Hybrid Environments Drive Increased Ransomware Risks Boosting Demand for Advanced Security Solutions |

| RESTRAINTS | • Challenges in Deploying Next Generation Ransomware Protection Solutions Amid Evolving Threats and Skill Shortages |

Ans: The Ransomware Protection Market is expected to grow at a CAGR of 15.29% during 2024-2032.

Ans: Ransomware Protection Market size was USD 25.59 billion in 2023 and is expected to Reach USD 91.80 billion by 2032.

Ans: The major growth factor of the ransomware protection market is the increasing frequency and sophistication of ransomware attacks targeting businesses across various industries.

Ans: The Managed segment dominated the Ransomware Protection Market in 2023.

Ans: North America dominated the Ransomware Protection Market in 2023.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Ransomware Protection Solution Effectiveness (2023)

5.2 Ransomware Protection Customer Satisfaction and Retention (2023)

5.3 Ransomware Protection Incident Response Times

5.4 Ransomware Protection Cybersecurity Budget Allocation

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Ransomware Protection Market Segmentation, By Solution

7.1 Chapter Overview

7.2 Standalone Anti-Ransomware Software

7.2.1 Standalone Anti-Ransomware Software Market Trends Analysis (2020-2032)

7.2.2 Standalone Anti-Ransomware Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 End-Point Security

7.3.1 End-Point Security Market Trends Analysis (2020-2032)

7.3.2 End-Point Security Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Network Security

7.4.1 Network Security Market Trends Analysis (2020-232)

7.4.2 Network Security Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Secure Web Gateways

7.5.1 Secure Web Gateways Market Trends Analysis (2020-2032)

7.5.2 Secure Web Gateways Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Ransomware Protection Market Segmentation, By Service

8.1 Chapter Overview

8.2 Managed

8.2.1 Managed Market Trends Analysis (2020-2032)

8.2.2 Managed Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Consulting

8.3.1 Consulting Market Trends Analysis (2020-2032)

8.3.2 Consulting Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Support & Management

8.4.1 Support & Management Market Trends Analysis (2020-2032)

8.4.2 Support & Management Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Ransomware Protection Market Segmentation, By Industry Vertical

9.1 Chapter Overview

9.2 BFSI

9.2.1 BFSI Market Trends Analysis (2020-2032)

9.2.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 IT & Telecom

9.3.1 IT & Telecom Market Trends Analysis (2020-2032)

9.3.2 IT & Telecom Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Healthcare

9.4.1 Healthcare Market Trends Analysis (2020-2032)

9.4.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Education

9.5.1 Education Market Trends Analysis (2020-2032)

9.5.2 Education Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Manufacturing

9.6.1 Manufacturing Market Trends Analysis (2020-2032)

9.6.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

9.7 Retail

9.7.1 Retail Market Trends Analysis (2020-2032)

9.7.2 Retail Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Ransomware Protection Market Segmentation, By Deployment Mode

10.1 Chapter Overview

10.2 Cloud

10.2.1 Cloud Market Trends Analysis (2020-2032)

10.2.2 Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 On-Premise

10.3.1 On-Premise Market Trends Analysis (2020-2032)

10.3.2 On-Premise Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.2.4 North America Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.2.5 North America Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.6 North America Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.2.7.2 USA Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.2.7.3 USA Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.7.4 USA Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.2.8.2 Canada Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.2.8.3 Canada Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.8.4 Canada Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.2.9.2 Mexico Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.2.9.3 Mexico Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.9.4 Mexico Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.7.2 Poland Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.7.3 Poland Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.7.4 Poland Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.8.2 Romania Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.8.3 Romania Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.8.4 Romania Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.1.10 turkey

11.3.1.10.1 Turkey Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.4 Western Europe Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.5 Western Europe Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.6 Western Europe Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.7.2 Germany Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.7.3 Germany Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.7.4 Germany Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.8.2 France Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.8.3 France Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.8.4 France Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.9.2 UK Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.9.3 UK Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.9.4 UK Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.10.2 Italy Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.10.3 Italy Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.10.4 Italy Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.11.2 Spain Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.11.3 Spain Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.11.4 Spain Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.14.2 Austria Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.14.3 Austria Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.14.4 Austria Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.4 Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.5 Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.6 Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.7.2 China Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.7.3 China Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.7.4 China Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.8.2 India Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.8.3 India Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.8.4 India Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.9.2 Japan Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.9.3 Japan Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.9.4 Japan Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.10.2 South Korea Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.10.3 South Korea Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.10.4 South Korea Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.11.2 Vietnam Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.11.3 Vietnam Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.11.4 Vietnam Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.12.2 Singapore Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.12.3 Singapore Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.12.4 Singapore Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.13.2 Australia Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.13.3 Australia Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.13.4 Australia Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.4 Middle East Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.5 Middle East Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.6 Middle East Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.7.2 UAE Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.7.3 UAE Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.7.4 UAE Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.2.4 Africa Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.2.5 Africa Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.6 Africa Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Ransomware Protection Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.6.4 Latin America Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.6.5 Latin America Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.6 Latin America Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.6.7.2 Brazil Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.6.7.3 Brazil Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.7.4 Brazil Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.6.8.2 Argentina Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.6.8.3 Argentina Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.8.4 Argentina Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.6.9.2 Colombia Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.6.9.3 Colombia Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.9.4 Colombia Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Ransomware Protection Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Ransomware Protection Market Estimates and Forecasts, By Service (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Ransomware Protection Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Ransomware Protection Market Estimates and Forecasts, By Deployment Mode (2020-2032) (USD Billion)

12. Company Profiles

12.1 Microsoft

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Cisco Systems

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 CrowdStrike

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Palo Alto Networks

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Sophos

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Trend Micro

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Check Point Software

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Fortinet

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 McAfee

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 FireEye

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Solution

Standalone Anti-Ransomware Software

End-Point Security

Network Security

Secure Web Gateways

By Service

Managed

Consulting

Support & Management

By Industry Vertical

BFSI

IT & Telecom

Healthcare

Education

Manufacturing

Retail

By Deployment Mode

Cloud

On-Premise

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Online Video Platform Market was valued at USD 10.11 billion in 2023 and is expected to reach USD 49.12 billion by 2032, growing at a CAGR of 19.26% from 2024-2032.

The Golf Simulators Market was valued at USD 1.71 billion in 2023 and is projected to reach USD 3.69 billion by 2032, growing at a CAGR of 9.08% during the forecast period of 2024–2032.

The Data Center Virtualization Market was valued at USD 8.0 Billion in 2023 and will reach USD 28.9 Billion by 2032, growing at a CAGR of 15.42% by 2032.

The Virtual Reality Headset Market Size was valued at USD 10.99 Billion in 2023 and will reach USD 75.04 Billion by 2032 and grow at a CAGR of 23.96% by 2032.

The Bare Metal Cloud Market was valued at USD 8.47 billion in 2023 and is expected to reach USD 46.14 billion by 2032, growing at a CAGR of 20.77% over the forecast period 2024-2032.

The Graph Database Market size was valued at US$ 2.8 billion in 2023 and is expected to reach US$ 15.94 billion in 2032 with a growing CAGR of 21.32 % over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd