Get More Information on PV Inverters Market - Request Sample Report

The PV Inverters Market size was estimated at USD 12.9 billion in 2023 and is predicted to reach over USD 47.44 billion by 2032 with an emerging CAGR growth of 18.5% Over the Forecast Period of 2024-2032.

Demand for electricity continues to grow year by year, further enhancing the demand for various renewable resources such as solar power and machinery. Since the fall in gas prices in 2014, different energy sources, especially wind and solar, have been placed on the back burner and this trend has changed in many industries.

By Product-In terms of revenue, the central inverter had a larger revenue share of more than 49.0% by 2023. These converters are very reliable with timely repairs and are stored in a secure place for installation. Inverters combined with large arrays installed in stadium installations, industrial facilities, and buildings, take DC power across all PV panels and convert it into AC power into a single power distribution point.

Part of the string inverter took its second-largest market share in 2023. The string inverter is widely used in the commercial and residential sectors. Low initial cost and easy installation are among the key factors responsible for partial growth. These inverters are robust, allow for high design flexibility, deliver high efficiency, offer three-phase variability, are well supported (with reliable products), and have the ability to monitor remote systems.

Part of the micro PV inverters is expected to witness a significant growth rate during the forecast period. Micro PV inverters are module-level electronics and have become popular in the commercial and industrial sectors. These inverters have the advantage of high reliability, increased efficiency and performance with Maximum Power Point Tracker (MPPT), easy installation, no space constraints, and cost savings.

By Applications-In position of revenue generated, the utility segment led the PV inverter market by 2022, accounting for a budget of about 44.0%. The most widely used PV Inverter in the service sector is the central & string inverter. Increased demand for renewable energy, lowering the cost of solar energy and equipment, and government subsidies are the main reasons for the growth of the resource sector. The presence of key players, providing consumers with industry-leading service rating solutions to achieve high efficiency and reducing system balance costs through their pre-assembled power stations drives partial growth.

Based on end-use, the market is divided into commercial, residential and industrial, and services. The residential sector has seen growth due to the growing demand for renewable solar energy among consumers for electrical purposes. Governments in various countries have taken practical steps through policies and financing to promote the grip of power-gripped power generation with renewable resources such as residential power. Commercial buildings include supermarkets, shops, offices, hospitals, and schools that install solar panels for use in captivity. These sectors require continuous power supply in order to operate without interruption.

The outbreak of COVID-19 has severely hampered the growth of the PV inverter market. The virus has affected large countries, thus curbing the growth of businesses. However, it is expected that the industry will renew its capacity to measure these impacts in the coming years.

COMPETITIVE LANDSCAPE

The market is very competitive and compact due to the presence of a large number of market players. A key practice in the operation of these solar companies involves direct integration that protects market power and reduces competition. Acquisition of technology, skilled workers, and strong R&D are among the key factors that control the competitiveness of the PV inverters industry. In March 2020, the Fimer team acquired the ABB solar switching business, making the company the 4th largest manufacturer of solar inverter worldwide. This acquisition strategy will help the company grow its global presence..

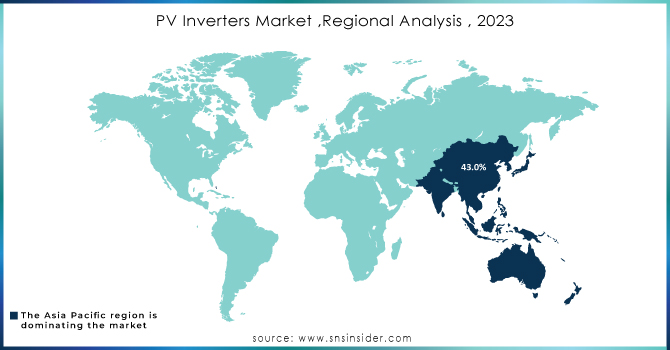

The Asia Pacific is expected to have a higher revenue share of more than 43.0% over the forecast period. China plays a major role in the rapid growth of the region's solar market and is a major global competitor. The growing number of solar installations in developing countries has also contributed significantly to regional market growth.

North America captured the largest share of revenue in 2023, and the US played a major role in market growth. The U.S. is a leading market for different types of PV inverter. Some of the latest inverter systems in the world include 60 kW plus power for three phase unit inverters and 1.5 MW and medium capacity inverters. Although North America has seen strong growth of cable inverters, central PV inverters are expected to maintain the largest market share in the forecast period.

Europe is expected to see an important CAGR in the forecast period due to the existence of favorable government policies and the provision of subsidies such as residential taxes that encourage consumers to invest in renewable energy. Germany holds a leading position in the production of solar inverters in line with the hi-tech nature of inverters. So German solar companies make more competitive profit than other players.

Need any Customization as Per Your Business Requirement on PV Inverters Market - Enquiry Now

The Major Players are Delta Electronics Inc, Eaton, Emerson Electric Co, Omron Corporation, Hitachi Hi-Rel Power Electronics Pvt Ltd, Power Electronics, Siemens AG, SMA Solar Technolgy AG and SunPower Corporation., Siemens Energy, Fimer Group, SMA Solar, Technology AG, Delta Electronics, Inc, SunPower Corporation, Eaton and Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 12.9 Billion |

| Market Size by 2032 | US$ 47.44 Billion |

| CAGR | CAGR of 18.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by type(Central, String, Micro, Others) • by Product (Central PV inverter, String PV inverter, Micro PV inverter, Others) • by Application (Residential, Commercial & industrial, Utilities) • by Connectivity (Standalone, On-grid) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Delta Electronics Inc, Eaton, Emerson Electric Co, Omron Corporation, Hitachi Hi-Rel Power Electronics Pvt Ltd, Power Electronics, Siemens AG, SMA Solar Technolgy AG |

PV Inverters market size was valued at 12.9 billion in 2023 at a CAGR of 18.5%.

North America has the PV Inverters greatest market share in terms of revenue and region market.

The residential sector of the PV inverter market is the fastest-growing market.

Yes, and they are Raw material vendors, Distributors/traders/wholesalers/suppliers, Regulatory authorities, including government agencies and NGOs, Commercial research & development (R&D) institutions, Importers and exporters, Government organizations, research organizations, and consulting firms, Trade/Industrial associations, End-use industries.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 COVID-19 Impact Analysis

4.2 Impact of Ukraine- Russia War

4.3 Impact of ongoing Recession

4.3.1 Introduction

4.3.2 Impact on major economies

4.3.2.1 US

4.3.2.2 Canada

4.3.2.3 Germany

4.3.2.4 France

4.3.2.5 United Kingdom

4.3.2.6 China

4.3.2.7 Japan

4.3.2.8 South Korea

4.3.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. The SNS Graph

9. Global PV Inverters Market Segmentation, By type

9.1 Introduction

9.2 Central

9.3 String

9.4 Micro

9.5 Others

10. Global PV Inverters Market Segmentation, By Product

10.1Introduction

10.2Central PV inverter

10.3 String PV inverter

10.4 Micro PV inverter

10.5 Other PV inverters

11. Global PV Inverters Market Segmentation, By Application

11.1 Introduction

11.2 Residential

11.3 Commercial & industrial

11.4 Utilities

12. Global PV Inverters Market Segmentation, By connectivity

12.1 Introduction

12.2 Standalone

12.3 On-grid

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 USA

13.2.2 Canada

13.2.3 Mexico

13.3 Europe

13.3.1 Germany

13.3.2 UK

13.3.3 France

13.3.4 Italy

13.3.5 Spain

13.3.6 The Netherlands

13.3.7 Rest of Europe

13.4 Asia-Pacific

13.4.1 Japan

13.4.2 South Korea

13.4.3 China

13.4.4 India

13.4.5 Australia

13.4.6 Rest of Asia-Pacific

13.5 The Middle East & Africa

13.5.1 Israel

13.5.2 UAE

13.5.3 South Africa

13.5.4 Rest

13.6 Latin America

13.6.1 Brazil

13.6.2 Argentina

13.6.3 Rest of Latin America

14. Company Profiles

14.1 Delta Electronics Inc.

14.1.1 Financial

14.1.2 Products/ Services Offered

14.1.3 SWOT Analysis

14.1.4 The SNS view

14.2 Eaton

14.3 Emerson Electric Co

14.4 Hitachi Hi-Rel Power Electronics Pvt Ltd

14.5 Omron Corporation

14.6 Power Electronics

14.7 Siemens AG

14.8 SMA Solar Technolgy AG and SunPower Corporation.

14.9 Siemens Energy

14.10 Fimer Group

14.11 SMA Solar Technology AG

14.12 Delta Electronics, Inc

14.13 SunPower Corporation

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Type

Central

String

Micro

Others

By Product

Central PV inverter

String PV inverter

Micro PV inverter

Other PV inverters

By Application

Residential

Commercial & Industrial

Utilities

By Connevtivity

Standalone

On-grid

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The LPG vaporizer Market Size was valued at USD 1.27 Billion in 2023 and is expected to reach USD 1.57 Billion by 2031 and grow at a CAGR of 2.7% over the forecast period 2024-2031.

The High-Speed Engine Market size was valued at USD 24.58 billion in 2022 and is expected to grow to USD 33.38 billion by 2030 and grow at a CAGR of 3.9% over the forecast period of 2023-2030.

The Gas Turbine MRO Market size was valued at USD 14.8 billion in 2023 and is expected to grow to USD 19.33 billion by 2032 with an emerging CAGR of 3.4% over the forecast period of 2024-2032.

The Hydrogen Energy Storage Market Size was valued at USD 11.11 billion in 2023 and is expected to reach USD 1933.28 billion by 2032 and grow at a CAGR of 77.4 % over the forecast period 2024-2032.

The Offshore Pipeline Market size was valued at USD 14.82 Billion in 2023 and is projected to reach USD 21.11 Billion by 2032, with a growing at a compound annual growth rate (CAGR) of 4.01% over the forecast period of 2024 to 2032.

The Oilfield Services Market size was valued at USD 139.69 billion in 2023 and is expected to grow to USD 200.03 billion by 2032 and grow at a CAGR of 4.07% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd