Get More Information on Premade Pouch Packaging Market - Request Free Sample Report

The Premade Pouch Packaging Market Size was USD 10.8 billion in 2023 & is projected to reach USD 16.47 billion by 2032 growing at a CAGR of 4.8% by 2024 to 2032

Premade pouches are conquering the market with their consumer-centric approach. Effortless opening mechanisms like tear notches and zippers make them a breeze to use, while their lightweight design translates to reduced costs for transportation and storage. Sustainability is another feather in their cap, as the industry increasingly embraces eco-friendly materials in pouch production. This aligns perfectly with the growing environmental consciousness of both consumers and businesses. Premade pouches can adapt to a wide range of products, from food and beverages to cosmetics and pharmaceuticals, offering manufacturers a packaging solution that maximizes shelf space and caters to diverse needs. However, one potential hurdle remains, achieving optimal protection for certain products.

The premade pouch industry is experiencing a revolution. Intelligent packaging is taking center stage, with QR codes and RFID technology being incorporated to boost traceability, empower consumers with interactive experiences, and deliver rich product information at their fingertips. Sustainability is a cornerstone trend, with the development and adoption of eco-friendly materials for premade pouches flourishing. Japan's pharmaceutical market is ripe for growth. Generic drugs dominate at nearly 81% of prescriptions, and the country imports a significant amount of pharmaceuticals. With a rapidly aging population requiring new treatments, this demand is expected to climb even higher, fueling positive growth in the market.

KEY DRIVERS:

The growing demand for convenience in everyday life is a key driver shaping consumer preferences across various industries

The packaging industry is getting a makeover, with a focus on creating a positive brand experience and prioritizing consumer comfort. This translates to a surge in flexible packaging, especially pouches. These user-friendly pouches are a win-win for both brands and consumers. Brands benefit from the potential for stronger brand loyalty thanks to the premium feel of flexible packaging.

Pre-made pouches' wide product compatibility across industries makes them a versatile packaging choice

RESTRAINE:

One potential drawback of pre-made pouches is their limited barrier properties compared to some rigid packaging options

Concerns about the environmental impact of production processes and potential limitations in the recyclability of certain pouch materials

OPPORTUNITY:

The production of PET jars and bottles is a highly profitable venture within the plastics and polymer industry

Stand-out packaging is key in today's crowded shelves. It needs to be both eye-catching and appealing to consumers

Customers are drawn to brands that offer unique and creative packaging, like Roots and Agrostreet. This packaging goes beyond aesthetics it's durable, convenient, and even customizable for different occasions. With the e-commerce boom fueled by COVID-19, eye-catching packaging is a strategic weapon for brands to grab attention and retain customers in the competitive online marketplace.

CHALLENGES:

Pouch adoption faces a hurdle as competition from cheap, familiar rigid containers

New equipment and production lines for pouches can be a budget barrier for some companies considering the switch

The Russia-Ukraine war has created a ripple effect through the premade pouch packaging market. Disruptions in the supply chain, production halts, and rising material costs pose significant challenges for pouch manufacturers. This could lead to higher prices, product shortages, and even a shift towards alternative packaging solutions in the short term. Over 300 major western packaging companies have exited Ukraine and Russia. Karpatneftekhim, Ukraine's largest PET plant, has shut down operations. The price of aluminum, a key material in premade pouches, has surged due to the war. The price of kraft pulp, another material used in premade pouches, has also increased significantly.

The severity and duration of the economic slowdown will play a significant role in its impact on the market. The relative price competitiveness of premade pouches compared to alternative packaging options will be crucial. The ability of the premade pouch industry to innovate and develop cost-effective solutions will influence its success during an economic downturn. The growth of e-commerce often continues even during economic slowdowns. Premade pouches can be a good fit for e-commerce due to their lightweight nature and efficient use of space, potentially leading to increased demand.

By Material

Plastic

Paper

Foil

Multi-layer

Plastic pouches reign supreme in the premade pouch market. This dominance stems from their triple threat of affordability, versatility, and lightweight design. They cater to various industries with their customizable shapes, sizes, and attractive printability. Plus, compared to other materials, plastic keeps production and transportation costs down.

By Closure Type

Tear Notch

Zipper

Spout

Flip Lid

Tear notches reign supreme in the world of pouch closures, claiming the dominant market share and expected to maintain their lead. This dominance is fueled by a powerful trio of advantages such as simplicity, convenience, and affordability. The ingenious tear notch design eliminates the need for fumbling with extra tools or utensils consumers simply tear along a designated perforation to access the contents. This user-centric approach perfectly aligns with the growing trend of consumers prioritizing convenience in their packaging choices.

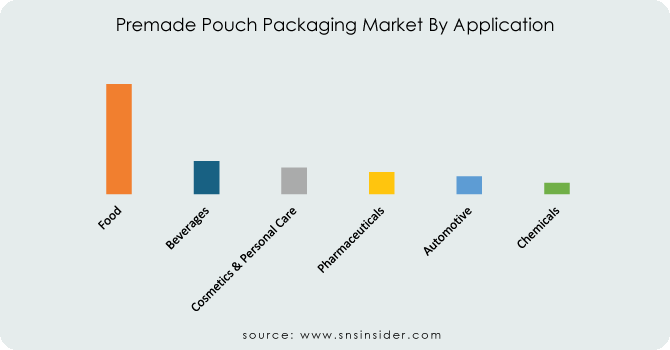

By Application

Food

Beverages

Cosmetics & Personal Care

Pharmaceuticals

Automotive

Chemicals

The food industry reigns supreme in the premade pouch market, holding a dominant 52% share and projected for continued growth. This dominance is fueled by the convenience and versatility pouches offer. From keeping fresh-cut vegetables crisp to showcasing snacks enticingly, pouches cater to a variety of food applications. They promote portion control for single-serve meals, reduce packaging waste, and enhance portability all while maximizing consumer convenience. Pouches can handle diverse textures, from liquids like yogurt to solid snacks like nuts, and their resealable closures add another layer of user-friendliness. Compared to rigid containers, pouches are lighter, easier to store and transport, ultimately creating a superior experience for food consumers.

Get Customized Report as per your Business Requirement - Request For Customized Report

North America reigns supreme in the premade pouch market, boasting a dominant share of 45% and projected for further growth. This dominance is fueled by a powerful combination of strong economies with high consumer buying power, a growing preference for convenient and portable packaging, and the e-commerce boom. Additionally, North American consumers' increasing focus on sustainability is driving demand for eco-friendly pouch materials, making this region a leader in adopting innovative and responsible packaging solutions.

Germany leads the European pre-made pouch market, while Russia and Spain are poised for the fastest growth. This surge is fueled by Europe's rising demand for packaged food and innovative pouch features like easy-open, resealable closures, making them a convenient and user-friendly choice for consumers. China's booming population, fondness for packaged food, and rising disposable income make it a prime market for pre-made pouches in Asia. Early adoption of recyclables and a robust healthcare system further solidify China's position as a major player.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Argentina

Colombia

Rest of Latin America

Some of the major players in the Premade Pouch Packaging Market are Berry Global, Amcor, Mondi Group, Sealed Air (Cryovac), Constantia Flexibles, Sonoco Products, Huhtamaki, C-P Flexible Packaging, Tyler Packaging, Viking Masek, Accredo Packaging, Karlville, General Packer And Others Players.

German company Sihl, known for their facestock expertise, launched Artysio in June 2022. This innovative film is designed for pre-made stand-up pouches that can be individually printed, making it suitable for both "print and pack" and "pack and print" production processes.

Mondi, a major player, announced an investment in July 2022 to expand its offerings in sustainable pet food packaging solutions. This commitment goes a step further with a planned EUR 65 million investment across three European consumer flexible packaging plants. This expansion aims to boost production capacity and cater to the growing demand for eco-friendly pet food packaging solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 10.8 Bn |

| Market Size by 2032 | US$ 16.47 Bn |

| CAGR | CAGR of 4.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Plastic, Paper, Foil, Multi-Layer) • By Closure Type (Tear Notch, Zipper, Spout, Flip Lid) • By Application (Food, Beverages, Cosmetics & Personal Care, Pharmaceuticals, Automotive, Chemicals) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Berry Global, Amcor, Mondi Group, Sealed Air (Cryovac), Constantia Flexibles, Sonoco Products, Huhtamaki, C-P Flexible Packaging, Tyler Packaging, Viking Masek, Accredo Packaging, Karlville, General Packer |

| Key Drivers | • The growing demand for convenience in everyday life is a key driver shaping consumer preferences across various industries • Pre-made pouches' wide product compatibility across industries makes them a versatile packaging choice |

| Key Restraints | • One potential drawback of pre-made pouches is their limited barrier properties compared to some rigid packaging options • Concerns about the environmental impact of production processes and potential limitations in the recyclability of certain pouch materials |

Ans: The Premade Pouch Packaging Market is expected to grow at a CAGR of 4.8%.

Ans: Premade Pouch Packaging Market size was USD 10.8 billion in 2023 and is expected to Reach USD 16.47 billion by 2032.

Ans: The growing demand for convenience in everyday life is a key driver shaping consumer preferences across various industries.

Ans: One potential drawback of premade pouches is their limited barrier properties compared to some rigid packaging options.

Ans: North America holds the dominant position with the market share of 45%.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Premade Pouch Packaging Market Segmentation, By Material

9.1 Introduction

9.2 Trend Analysis

9.3 Plastic

9.4 Paper

9.5 Foil

9.6 Multi-layer

10. Premade Pouch Packaging Market Segmentation, By Closure Type

10.1 Introduction

10.2 Trend Analysis

10.3 Tear Notch

10.4 Zipper

10.5 Spout

10.6 Flip Lid

11. Premade Pouch Packaging Market Segmentation, By Application

11.1 Introduction

11.2 Trend Analysis

11.3 Food

11.4 Beverages

11.5 Cosmetics & Personal Care

11.6 Pharmaceuticals

11.7 Automotive

11.8 Chemicals

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America Premade Pouch Packaging Market by Country

12.2.3 North America Premade Pouch Packaging Market By Material

12.2.4 North America Premade Pouch Packaging Market By Closure Type

12.2.5 North America Premade Pouch Packaging Market By Application

12.2.6 USA

12.2.6.1 USA Premade Pouch Packaging Market By Material

12.2.6.2 USA Premade Pouch Packaging Market By Closure Type

12.2.6.3 USA Premade Pouch Packaging Market By Application

12.2.7 Canada

12.2.7.1 Canada Premade Pouch Packaging Market By Material

12.2.7.2 Canada Premade Pouch Packaging Market By Closure Type

12.2.7.3 Canada Premade Pouch Packaging Market By Application

12.2.8 Mexico

12.2.8.1 Mexico Premade Pouch Packaging Market By Material

12.2.8.2 Mexico Premade Pouch Packaging Market By Closure Type

12.2.8.3 Mexico Premade Pouch Packaging Market By Application

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe Premade Pouch Packaging Market by Country

12.3.2.2 Eastern Europe Premade Pouch Packaging Market By Material

12.3.2.3 Eastern Europe Premade Pouch Packaging Market By Closure Type

12.3.2.4 Eastern Europe Premade Pouch Packaging Market By Application

12.3.2.5 Poland

12.3.2.5.1 Poland Premade Pouch Packaging Market By Material

12.3.2.5.2 Poland Premade Pouch Packaging Market By Closure Type

12.3.2.5.3 Poland Premade Pouch Packaging Market By Application

12.3.2.6 Romania

12.3.2.6.1 Romania Premade Pouch Packaging Market By Material

12.3.2.6.2 Romania Premade Pouch Packaging Market By Closure Type

12.3.2.6.4 Romania Premade Pouch Packaging Market By Application

12.3.2.7 Hungary

12.3.2.7.1 Hungary Premade Pouch Packaging Market By Material

12.3.2.7.2 Hungary Premade Pouch Packaging Market By Closure Type

12.3.2.7.3 Hungary Premade Pouch Packaging Market By Application

12.3.2.8 Turkey

12.3.2.8.1 Turkey Premade Pouch Packaging Market By Material

12.3.2.8.2 Turkey Premade Pouch Packaging Market By Closure Type

12.3.2.8.3 Turkey Premade Pouch Packaging Market By Application

12.3.2.9 Rest of Eastern Europe

12.3.2.9.1 Rest of Eastern Europe Premade Pouch Packaging Market By Material

12.3.2.9.2 Rest of Eastern Europe Premade Pouch Packaging Market By Closure Type

12.3.2.9.3 Rest of Eastern Europe Premade Pouch Packaging Market By Application

12.3.3 Western Europe

12.3.3.1 Western Europe Premade Pouch Packaging Market by Country

12.3.3.2 Western Europe Premade Pouch Packaging Market By Material

12.3.3.3 Western Europe Premade Pouch Packaging Market By Closure Type

12.3.3.4 Western Europe Premade Pouch Packaging Market By Application

12.3.3.5 Germany

12.3.3.5.1 Germany Premade Pouch Packaging Market By Material

12.3.3.5.2 Germany Premade Pouch Packaging Market By Closure Type

12.3.3.5.3 Germany Premade Pouch Packaging Market By Application

12.3.3.6 France

12.3.3.6.1 France Premade Pouch Packaging Market By Material

12.3.3.6.2 France Premade Pouch Packaging Market By Closure Type

12.3.3.6.3 France Premade Pouch Packaging Market By Application

12.3.3.7 UK

12.3.3.7.1 UK Premade Pouch Packaging Market By Material

12.3.3.7.2 UK Premade Pouch Packaging Market By Closure Type

12.3.3.7.3 UK Premade Pouch Packaging Market By Application

12.3.3.8 Italy

12.3.3.8.1 Italy Premade Pouch Packaging Market By Material

12.3.3.8.2 Italy Premade Pouch Packaging Market By Closure Type

12.3.3.8.3 Italy Premade Pouch Packaging Market By Application

12.3.3.9 Spain

12.3.3.9.1 Spain Premade Pouch Packaging Market By Material

12.3.3.9.2 Spain Premade Pouch Packaging Market By Closure Type

12.3.3.9.3 Spain Premade Pouch Packaging Market By Application

12.3.3.10 Netherlands

12.3.3.10.1 Netherlands Premade Pouch Packaging Market By Material

12.3.3.10.2 Netherlands Premade Pouch Packaging Market By Closure Type

12.3.3.10.3 Netherlands Premade Pouch Packaging Market By Application

12.3.3.11 Switzerland

12.3.3.11.1 Switzerland Premade Pouch Packaging Market By Material

12.3.3.11.2 Switzerland Premade Pouch Packaging Market By Closure Type

12.3.3.11.3 Switzerland Premade Pouch Packaging Market By Application

12.3.3.1.12 Austria

12.3.3.12.1 Austria Premade Pouch Packaging Market By Material

12.3.3.12.2 Austria Premade Pouch Packaging Market By Closure Type

12.3.3.12.3 Austria Premade Pouch Packaging Market By Application

12.3.3.13 Rest of Western Europe

12.3.3.13.1 Rest of Western Europe Premade Pouch Packaging Market By Material

12.3.3.13.2 Rest of Western Europe Premade Pouch Packaging Market By Closure Type

12.3.3.13.3 Rest of Western Europe Premade Pouch Packaging Market By Application

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific Premade Pouch Packaging Market by Country

12.4.3 Asia-Pacific Premade Pouch Packaging Market By Material

12.4.4 Asia-Pacific Premade Pouch Packaging Market By Closure Type

12.4.5 Asia-Pacific Premade Pouch Packaging Market By Application

12.4.6 China

12.4.6.1 China Premade Pouch Packaging Market By Material

12.4.6.2 China Premade Pouch Packaging Market By Closure Type

12.4.6.3 China Premade Pouch Packaging Market By Application

12.4.7 India

12.4.7.1 India Premade Pouch Packaging Market By Material

12.4.7.2 India Premade Pouch Packaging Market By Closure Type

12.4.7.3 India Premade Pouch Packaging Market By Application

12.4.8 Japan

12.4.8.1 Japan Premade Pouch Packaging Market By Material

12.4.8.2 Japan Premade Pouch Packaging Market By Closure Type

12.4.8.3 Japan Premade Pouch Packaging Market By Application

12.4.9 South Korea

12.4.9.1 South Korea Premade Pouch Packaging Market By Material

12.4.9.2 South Korea Premade Pouch Packaging Market By Closure Type

12.4.9.3 South Korea Premade Pouch Packaging Market By Application

12.4.10 Vietnam

12.4.10.1 Vietnam Premade Pouch Packaging Market By Material

12.4.10.2 Vietnam Premade Pouch Packaging Market By Closure Type

12.4.10.3 Vietnam Premade Pouch Packaging Market By Application

12.4.11 Singapore

12.4.11.1 Singapore Premade Pouch Packaging Market By Material

12.4.11.2 Singapore Premade Pouch Packaging Market By Closure Type

12.4.11.3 Singapore Premade Pouch Packaging Market By Application

12.4.12 Australia

12.4.12.1 Australia Premade Pouch Packaging Market By Material

12.4.12.2 Australia Premade Pouch Packaging Market By Closure Type

12.4.12.3 Australia Premade Pouch Packaging Market By Application

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Premade Pouch Packaging Market By Material

12.4.13.2 Rest of Asia-Pacific Premade Pouch Packaging Market By Closure Type

12.4.13.3 Rest of Asia-Pacific Premade Pouch Packaging Market By Application

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East Premade Pouch Packaging Market by Country

12.5.2.2 Middle East Premade Pouch Packaging Market By Material

12.5.2.3 Middle East Premade Pouch Packaging Market By Closure Type

12.5.2.4 Middle East Premade Pouch Packaging Market By Application

12.5.2.5 UAE

12.5.2.5.1 UAE Premade Pouch Packaging Market By Material

12.5.2.5.2 UAE Premade Pouch Packaging Market By Closure Type

12.5.2.5.3 UAE Premade Pouch Packaging Market By Application

12.5.2.6 Egypt

12.5.2.6.1 Egypt Premade Pouch Packaging Market By Material

12.5.2.6.2 Egypt Premade Pouch Packaging Market By Closure Type

12.5.2.6.3 Egypt Premade Pouch Packaging Market By Application

12.5.2.7 Saudi Arabia

12.5.2.7.1 Saudi Arabia Premade Pouch Packaging Market By Material

12.5.2.7.2 Saudi Arabia Premade Pouch Packaging Market By Closure Type

12.5.2.7.3 Saudi Arabia Premade Pouch Packaging Market By Application

12.5.2.8 Qatar

12.5.2.8.1 Qatar Premade Pouch Packaging Market By Material

12.5.2.8.2 Qatar Premade Pouch Packaging Market By Closure Type

12.5.2.8.3 Qatar Premade Pouch Packaging Market By Application

12.5.2.9 Rest of Middle East

12.5.2.9.1 Rest of Middle East Premade Pouch Packaging Market By Material

12.5.2.9.2 Rest of Middle East Premade Pouch Packaging Market By Closure Type

12.5.2.9.3 Rest of Middle East Premade Pouch Packaging Market By Application

12.5.3 Africa

12.5.3.1 Africa Premade Pouch Packaging Market by Country

12.5.3.2 Africa Premade Pouch Packaging Market By Material

12.5.3.3 Africa Premade Pouch Packaging Market By Closure Type

12.5.3.4 Africa Premade Pouch Packaging Market By Application

12.5.3.5 Nigeria

12.5.3.5.1 Nigeria Premade Pouch Packaging Market By Material

12.5.3.5.2 Nigeria Premade Pouch Packaging Market By Closure Type

12.5.3.5.3 Nigeria Premade Pouch Packaging Market By Application

12.5.3.6 South Africa

12.5.3.6.1 South Africa Premade Pouch Packaging Market By Material

12.5.3.6.2 South Africa Premade Pouch Packaging Market By Closure Type

12.5.3.6.3 South Africa Premade Pouch Packaging Market By Application

12.5.3.7 Rest of Africa

12.5.3.7.1 Rest of Africa Premade Pouch Packaging Market By Material

12.5.3.7.2 Rest of Africa Premade Pouch Packaging Market By Closure Type

12.5.3.7.3 Rest of Africa Premade Pouch Packaging Market By Application

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America Premade Pouch Packaging Market by country

12.6.3 Latin America Premade Pouch Packaging Market By Material

12.6.4 Latin America Premade Pouch Packaging Market By Closure Type

12.6.5 Latin America Premade Pouch Packaging Market By Application

12.6.6 Brazil

12.6.6.1 Brazil Premade Pouch Packaging Market By Material

12.6.6.2 Brazil Premade Pouch Packaging Market By Closure Type

12.6.6.3 Brazil Premade Pouch Packaging Market By Application

12.6.7 Argentina

12.6.7.1 Argentina Premade Pouch Packaging Market By Material

12.6.7.2 Argentina Premade Pouch Packaging Market By Closure Type

12.6.7.3 Argentina Premade Pouch Packaging Market By Application

12.6.8 Colombia

12.6.8.1 Colombia Premade Pouch Packaging Market By Material

12.6.8.2 Colombia Premade Pouch Packaging Market By Closure Type

12.6.8.3 Colombia Premade Pouch Packaging Market By Application

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Premade Pouch Packaging Market By Material

12.6.9.2 Rest of Latin America Premade Pouch Packaging Market By Closure Type

12.6.9.3 Rest of Latin America Premade Pouch Packaging Market By Application

13. Company Profiles

13.1 Berry Global

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Products/ Services Offered

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 Amcor

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Products/ Services Offered

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 Mondi Group

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Products/ Services Offered

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Sealed Air (Cryovac)

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Products/ Services Offered

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 Constantia Flexibles

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Products/ Services Offered

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 Sonoco Products

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Products/ Services Offered

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Huhtamaki

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Products/ Services Offered

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 C-P Flexible Packaging

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Products/ Services Offered

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Tyler Packaging

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Products/ Services Offered

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 Viking Masek

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Products/ Services Offered

13.10.4 SWOT Analysis

13.10.5 The SNS View

13.11 Accredo Packaging

13.11.1 Company Overview

13.11.2 Financial

13.11.3 Products/ Services Offered

13.11.4 SWOT Analysis

13.11.5 The SNS View

13.12 Karlville

13.12.1 Company Overview

13.12.2 Financial

13.12.3 Products/ Services Offered

13.12.4 SWOT Analysis

13.12.5 The SNS View

13.13 General Packer

13.13.1 Company Overview

13.13.2 Financial

13.13.3 Products/ Services Offered

13.13.4 SWOT Analysis

13.13.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Green Packaging Market size was USD 325.74 billion in 2023 and is expected to Reach USD 527.08 billion by 2031 and grow at a CAGR of 6.2 % over the forecast period of 2024-2031.

The Premade Pouch Packaging Market Size was USD 10.8 billion in 2023 & is projected to reach USD 16.47 billion by 2032 growing at a CAGR of 4.8% by 2024 to 2032

The Caps & Closures Market size was valued at USD 74 billion in 2023 and is expected to reach USD 114.79 billion by 2032 with a growing CAGR of 5% over the forecast period of 2024-2032.

The Food Service Disposables Market size was USD 62.11 billion in 2023 and is expected to Reach USD 93.87 billion by 2031 and grow at a CAGR of 5.3% over the forecast period of 2024-2031.

The Single-Use Packaging Market size was USD 26.12 billion in 2023 and is expected to Reach USD 42.27 billion by 2031 and grow at a CAGR of 6.2% over the forecast period of 2024-2031.

The Produce Packaging Market size was USD 34.45 billion in 2023 and is expected to Reach USD 50.52 billion by 2031 and grow at a CAGR of 4.9% over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd