Power Semiconductor Market Size & Growth Trends:

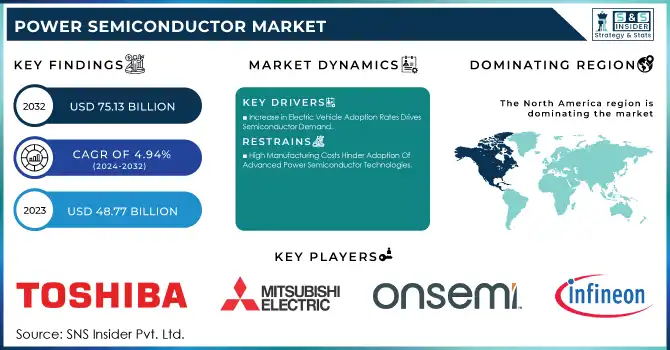

The Power Semiconductor Market Size was valued at USD 48.77 Billion in 2023 and is expected to reach USD 75.13 Billion by 2032 and grow at a CAGR of 4.94% over the forecast period 2024-2032. Significant momentum has been experienced in the Power Semiconductors Market during 2023 and 2024 as more global pressure is created in energy efficiency, adoption of renewable energy, and industrial electrification. Japan, China, the USA, France, Germany, and India have spearheaded such growth with the adoption of high-end technologies and pro-government policies. For example, China, which has placed strategic emphases on clean energy, focusing on subsidies for electric vehicle (EV) manufacturers and renewable energy schemes, has emerged as a world leader. In the USA, the Inflation Reduction Act (IRA) presents further incentives for investment in such clean energy technologies. Japan takes the lead through its green growth strategy by emphasizing investments in energy-efficient power semiconductors for industrial as well as automotive applications.

Get more information on Power Semiconductor Market - Request Sample Report

Technological advancements are taking their forefront, and at the helm of this development stands the commercialization of silicon carbide (SiC) and gallium nitride (GaN) semiconductors. Israeli semiconductor manufacturer VisIC Technologies and AVL are also cooperating in the field of gallium nitride inverters for electric cars. There, they are developing new inverters that are going to outperform silicon-carbide-based inverters both in terms of performance as well as cost. Such semiconductor developments offer better energy efficiency, higher power density, and reduced energy losses. All of these features are of interest for applications in electric vehicles, renewable energy systems, and 5G telecommunications. Some of the notable launches during 2023 and 2024 include next-generation SiC MOSFETs and GaN-based power devices designed for high-demand applications like EV fast chargers and industrial automation.

Increasing penetration of EVs remains a key driver of the market growth. Global EV sales increased by more than 33% in 2023, according to reports from the International Energy Agency (IEA). Countries such as Germany and India are expanding their EV infrastructure at a lightning pace, driving demand for power semiconductors. In this space, renewable energy has also grown incredibly well, with solar capacity increasing 27% across the world in 2023. Advanced power semiconductors are thus the need of the hour to improve the efficiency of solar inverters, wind turbines, and battery storage systems.

Power Semiconductor Market Dynamics

KEY DRIVERS:

-

Increase in Electric Vehicle Adoption Rates Drives Semiconductor Demand.

The growing penetration of electric vehicles (EVs) around the world has resulted in a strong demand for power semiconductors. These devices are critical to the efficient operation of EV powertrains, battery management systems, and charging infrastructure. According to the International Energy Agency (IEA), global EV cars rose by more than 55% in 2023, with countries like China and the USA leading the charge.

Power semiconductors, especially SiC and GaN devices, make it possible to charge more efficiently and save energy. Governments can also encourage the use of electric vehicles by offering incentives like the Indian FAME scheme or the German tax breaks for buying EVs. In short, the automotive industry is likely to focus on becoming an all-electric power vehicle segment for years to come, ensuring a continued market for these power semiconductors.

-

Growth In Renewable Energy Installations Accelerates Semiconductor Adoption.

Renewable energy expansion, driven by global decarbonization efforts, is the primary factor fueling the power semiconductors market. Advanced semiconductors are the backbone of optimal performance for solar inverters, wind turbines, and energy storage systems. According to the International Renewable Energy Agency, global solar capacity increased by 27% in 2023, with China, India, and the USA among the major contributors.

SiC-based semiconductors are significantly important in solar and wind power systems where efficiency is high, and the energy loss is less. The governments has also promoted renewable projects; for example, Germany wants to ensure 80% of the energy will be produced through renewable sources by 2030. Due to such commitment towards clean energy, power semiconductors have been integrated with an objective of long-term market growth and innovation.

RESTRAIN:

-

High Manufacturing Costs Hinder Adoption Of Advanced Power Semiconductor Technologies.

The high cost of manufacturing advanced power semiconductors, such as SiC and GaN devices, is a major barrier to widespread adoption. These materials are more expensive to produce than traditional silicon-based components, primarily because of complex fabrication processes and limited supply chains. For example, SiC wafers are about 40% more expensive than the conventional silicon wafers, according to industry sources in 2023. Furthermore, the global manufacturing capacity for these advanced materials is still inadequate.

Most manufacturers are struggling to scale up their production because of the high capital investment needed for state-of-the-art facilities. This cost constraint affects pricing, as the penetration of advanced devices is not possible in cost-sensitive markets such as India and Southeast Asia. Although government subsidies and R&D initiatives are aimed at solving these issues, the high initial costs remain a significant hindrance to rapid adoption. Thus, solving these barriers would be a key enabler of unlocking the full potential of the power semiconductors market.

Power Semiconductor Market Key Segments

by Module

The Discrete segment dominated in 2023 with 53% of market share due to its widespread use in automotive and consumer electronics. Such components are crucial in applications that demand high efficiency and reliability, such as inverters and motor drives.

On the other hand, the Module segment is expected to expand with the highest CAGR of 5.50% over the forecast period 2024-2032 due to their increasing applications in renewable energy systems and industrial automation.

Power ICs, which integrate various functions within compact designs, are in high demand in portable consumer products and IoT applications. Technological advancements in SiC and GaN materials are enhancing the efficiency of these components, thus making them indispensable for energy-intensive applications. This segment explains the diverse and constantly changing power semiconductors market.

by Application

The IT & Telecommunication segment dominated in 2023 with 29.67% of market share, driven by the rapid growth of 5G infrastructure and data centers across the globe. These applications demand high-performance power semiconductors to effectively manage energy efficiency and heat dissipation.

The Automotive segment is expected to grow with the fastest CAGR of 5.59% during the forecast period 2024-2032, driven by the accelerated adoption of electric vehicles and autonomous driving technologies. Industrial applications are also substantial, where advanced power semiconductors are used for automation and smart manufacturing processes.

The growing incorporation of these components in various sectors underlines their critical role in attaining operational efficiency and sustainability, further propelling the growth of the market.

Power Semiconductor Market Regional Overview

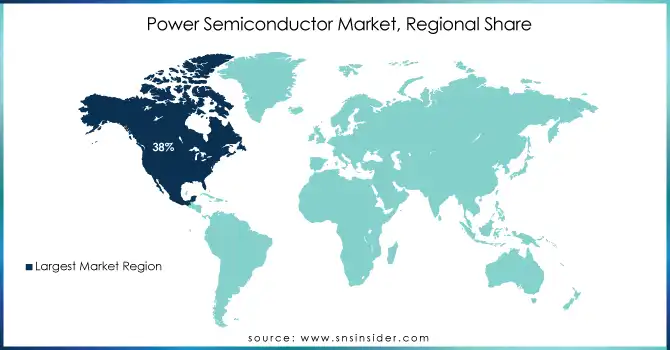

North America dominated in 2023 with 38% market share, driven by strong investments in renewable energy projects and electric vehicle infrastructure, particularly in the USA. Government incentives, such as tax credits for clean energy technologies, have further boosted market demand.

Asia Pacific is expected to grow the fastest with a CAGR of 6.07% during the forecast period 2024-2032, driven by rapid industrialization and urbanization in countries like China and India. Significant government initiatives, such as China's 2060 carbon neutrality goal and India's solar energy expansion, are catalyzing the adoption of advanced power semiconductor technologies.

Get Customized Report as per your Business Requirement - Ask For Customized Report

Key Players

Some of the major players in the Power Semiconductors Market are

-

Infineon Technologies (IGBT Modules, MOSFETs)

-

ON Semiconductor (Power MOSFETs, Gate Drivers)

-

Mitsubishi Electric (Power Modules, SiC Devices)

-

Toshiba Corporation (Power Transistors, Diodes)

-

STMicroelectronics (SiC MOSFETs, Power ICs)

-

Texas Instruments (Power Amplifiers, Voltage Regulators)

-

Vishay Intertechnology (Rectifiers, Optoelectronics)

-

Fuji Electric (IGBT Modules, Inverters)

-

NXP Semiconductors (Power Management ICs, RF Power Devices)

-

Renesas Electronics (Power MOSFETs, Gate Drivers)

-

ABB Ltd (Power Converters, HVDC Systems)

-

Broadcom Inc. (Optoelectronic Devices, Power Amplifiers)

-

Wolfspeed (SiC Substrates, GaN Devices)

-

Rohm Semiconductor (SiC Power Devices, ICs)

-

Hitachi Energy (IGBT Modules, SiC Diodes)

-

Semikron (IGBT Modules, Power Assemblies)

-

Littelfuse (Protection Relays, Fuses)

-

Microchip Technology (Gate Drivers, Power Modules)

-

Analog Devices (Power Management ICs, Signal Chains)

-

Delta Electronics (Power Converters, UPS Systems)

Major Suppliers (Components, Technologies)

-

Sumitomo Electric Industries (SiC Wafers, GaN Materials)

-

Dow Chemical (Silicon Materials, Epoxy Resins)

-

Cree Inc. (SiC Substrates, GaN Materials)

-

Shin-Etsu Chemical (Silicon Wafers, Polycrystalline Silicon)

-

Heraeus Electronics (Bonding Wires, Solder Pastes)

-

II-VI Incorporated (SiC Substrates, Epitaxial Wafers)

-

Applied Materials (Semiconductor Equipment, Deposition Systems)

-

Linde Group (Electronic Specialty Gases, Chemicals)

-

BASF SE (Electronic Chemicals, Advanced Polymers)

-

Sumco Corporation (Silicon Wafers, Epitaxial Substrates)

Major Clients

-

Tesla

-

General Electric

-

Siemens

-

Samsung Electronics

-

Huawei Technologies

-

Apple Inc.

-

LG Electronics

-

Boeing

-

Toyota Motor Corporation

-

Schneider Electric

Recent Trends

-

December 2024: ON Semi has announced the acquisition plans for Qorvo's Silicon Carbide (SiC) JFET business, enhancing its power semiconductor portfolio in the high and mid-voltage space. The deal is valued at USD 115 million and encompasses Qorvo's subsidiary United Silicon Carbide and is to be completed by Q1 2025.

-

December 2024: ROHM and TSMC will join forces in a strategic collaboration to develop and manufacture volume for gallium nitride power devices for electric vehicle applications. It will combine ROHM's device development technology with TSMC's GaN-on-silicon industry-leading process technology to keep up with the increasing demand of power devices that have more excellent high-voltage and high-frequency properties than those provided by silicon.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 48.77 Billion |

| Market Size by 2032 | USD 75.13 Billion |

| CAGR | CAGR of 4.94 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Discrete, Module, Power Integrated Circuits), • By Application (Automotive, Consumer Electronics, IT & Telecommunications, Military & Aerospace, Power, Industrial, and Other), • By Material (SILICON CARBIDE, Gan SILICON, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Infineon Technologies, ON Semiconductor, Mitsubishi Electric, Toshiba Corporation, STMicroelectronics, Texas Instruments, Vishay Intertechnology, Fuji Electric, NXP Semiconductors, Renesas Electronics, ABB Ltd, Broadcom Inc., Wolfspeed, Rohm Semiconductor, Hitachi Energy, Semikron, Littelfuse, Microchip Technology, Analog Devices, Delta Electronics. |

| Key Drivers | • Increase in Electric Vehicle Adoption Rates Drives Semiconductor Demand. • Growth In Renewable Energy Installations Accelerates Semiconductor Adoption. |

| Restraints | • High Manufacturing Costs Hinder Adoption Of Advanced Power Semiconductor Technologies. |