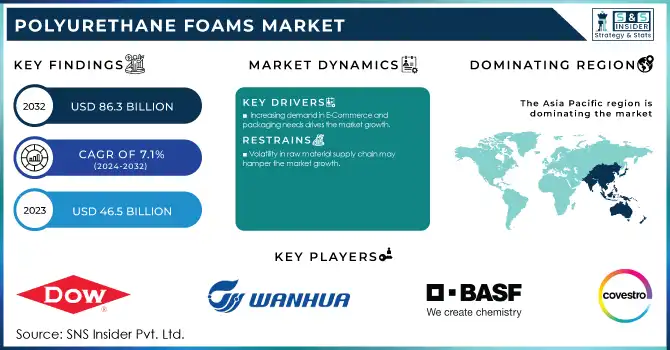

The Polyurethane Foams Market size was USD 46.5 billion in 2023 and is expected to reach USD 86.3 Billion by 2032 and grow at a CAGR of 7.1% over the forecast period of 2024-2032.

Get More Information on Polyurethane Foams Market - Request Sample Report

The key factor driving the growth of the polyurethane foams market is the increasing demand for insulation materials. With the growth of worldwide energy consumption, energy efficiency has become a point of attention within homes and businesses. As governments across the globe are enforcing stricter energy-saving standards, industries need advanced insulation solutions to reduce heat loss thus minimizing energy costs. Polyurethane foam is a highly effective thermal insulator and is most commonly used in construction as insulation in walls, roofs, and floors. It is the best energy-efficient construction material as it serves as an effective insulator with a very low thickness. Furthermore, increasing concerns regarding environmental sustainability are increasing the requirement of materials to reduce carbon footprints, and also polyurethane foam is the most effective form of insulation for energy conservation making it the preferred material for insulation among green building projects. While well entrenched in developed economies such as North America and Europe, where energy-efficient building codes are more rigorously enforced, this trend is also growing rapidly in the developing world, where urbanization and industrial development are advancing quickly.

According to the U.S. Department of Energy, residential and commercial buildings account for nearly 40% of total U.S. energy consumption, with a significant portion of this energy used for heating and cooling. The U.S. government has set ambitious targets to improve energy efficiency, including the Better Buildings Initiative, which aims to make commercial buildings 20% more energy-efficient by 2025. This initiative promotes the use of advanced insulation materials such as polyurethane foams to reduce energy consumption in buildings.

The increase in purchasing power of consumers, they are spending more on better quality durable, and comfortable garments. Polyurethane foam is used in these industries for its versatility, durability, and ease of adaptation to varied firmness and density to make mattresses, cushions, and upholstered furniture more comfortable. Notably in fast-growing-limited economies, urbanization and a rising middle class further spur consumer demand for home products and furniture. Not only does it introduce comfort, but its durability and resilience extend the lifetime of products as well, thus appealing to consumers looking for attractive, value-driven products. This demand for furniture and bedding made with polyurethane foam is being driven by a greater focus on quality of life and home aesthetics in emerging markets as well as improved access to modern home use standards. Additionally, advancements in foam technology, like memory and sustainable foams, are broadening its scope, which greatly supports the growth in these industries.

According to the U.S. Bureau of Economic Analysis, real disposable personal income in the U.S. increased by 3.6% in 2023, supporting higher consumer spending on goods like furniture and bedding. This trend aligns with the growing consumer demand for higher-quality products, including those made with polyurethane foams.

Market Dynamic:

Drivers

Increasing demand in E-Commerce and packaging needs drives the market growth.

A major reason for the growth in the polyurethane foams market is their increasing demand from e-commerce and packaging applications. The e-commerce industry is growing rapidly as it has changed the process of buying and shipping products worldwide. As online shopping is on the rise, demand for safe, reliable and lightweight packaging has become even more significant for protecting products from machine, junction and-handling shocks . Some of the most common uses of polyurethanes are in packaging for cushioning purposes, as they are very lightweight and used for shock absorbing to protect delicate goods in transit. In addition, as e-commerce companies are trying to create higher customer satisfaction, they are looking up to innovative packaging solutions that serve dual functionality, providing protection along with sustainability. In response to increasing consumer and regulatory pressure to switch to sustainable packaging solutions, polymeric foams such as polyurethane foam, particularly bio-based versions, are gradually being used. The trend is visible across product categories ranging from electronics and appliances to cosmetics and personal care products. The increase in global e-commerce coupled with the growing trend of sustainable packaging, is creating ample opportunity for polyurethane foams thereby boosting the market.

The European Commission has implemented several policies aimed at improving the sustainability of packaging, including the Packaging and Packaging Waste Directive. This has led to increased interest in eco-friendly packaging materials. The EU is pushing for a 10% reduction in packaging waste by 2025, encouraging the adoption of sustainable and protective materials like bio-based polyurethane foams in the packaging industry.

Restraint

Volatility in raw material supply chain may hamper the market growth.

Polyols and isocyanates, which are the key raw materials for polyurethane foam production, are made based on petrochemical products and are directly affected by the crude oil price fluctuations. Since pure unwieldy oil price changes can also instigate unanticipated cost modifications for manufacturers, that can have an effect on their profitability in addition to the overall poker size of polyurethane foams amongst the advertisement lifecycle, any ailment in crude oil supply can motive widespread domino impact. In addition, factors like geopolitics, natural calamities, and trade policy changes can contribute to other aspects of disruption in the upstream supply chain, causing the unavailability of materials and stopping production.

By Product

Flexible foam held the largest market share around 59% in 2023. It is due to its versatility, comfort, and its high scope of applications in various industries. Flexible polyurethane foam is recognized for its cushioning and support and is commonly used in mattresses, upholstered furniture, automotive seating, and bedding. It can be produced to suit various specifications of the merchandise, is redoubtable, light-weight, exploitable, and comes up with different firmness levels for varied consumer preferences, providing the user with total flexibility. Given the importance of comfort and durability in the furniture and bedding industries, flexible foam has become a necessary product.

By Application

The bedding & furniture segment held the largest market share around 35% in 2023. It is owing to the importance of the role of polyurethane foam in improving comfort, durability, and functionality in many such products. And, the superior comfort and support offered by polyurethane foams (especially flexible foams) the most common application of these foams is in the making of mattresses, cushions, sofas and other upholstered furniture. Higher disposable incomes and shifting consumer lifestyles have played a critical role in supporting the demand for high quality, sturdy, and long-lasting furniture and bedding products, and the segment benefits from an ability to appeal to consumers across price point tiers. Furthermore, growing knowledge regarding the advantages of good sleep quality has led consumers to seek high-performing mattresses that incorporate advanced polyurethane foams, particularly in memory foam so that they contour to the body for enhanced relaxation.

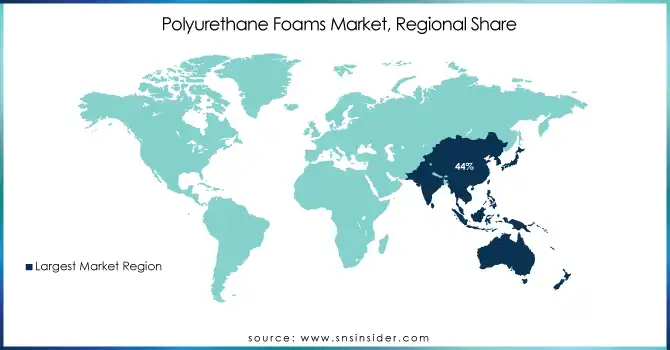

Asia Pacific held the largest market share around 44% in 2023. This is due the system of high velocity of urgent industrialization, urbanization, and then an incremental consumer demand from several sectors. China, India, and Japan among the fastest-growing economies in the world, which have increased production and consumption of polyurethane foams considerably, are located in this region itself. The construction and automotive sectors, the largest users of polyurethane foams, are buoyant in Asia Pacific due to infrastructure development, urbanization, and growing demand for energy efficient materials in construction sector. Polyurethane foam is rapidly gaining demand as a lightweight and durable materials in the automotive space, especially in countries, such as China, in which vehicle production and sales are soaring. Additionally, the growing population, rising disposable income levels, and changing consumer behaviors towards mattresses, furniture, and electronics are contributing to the high consumption of polyurethane foams in the region. Moreover, Asia pacific is trending towards eco-friendly and sustainable materials, due to this trend, manufacturers are emphasizing on manufacturing bio-based polyurethane foams to match your market demand. Asia Pacific will continue to be the largest market for polyurethane foams worldwide, attributed to the presence of large manufacturers of polyurethane foam, low production cost and rise in the shift towards advanced technologies in the region.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

Covestro AG (Desmodur, Bayblend)

BASF SE (Sodium Nitrite, Master Builders Solutions)

Wanhua Chemical Group Co., Ltd. (Methylene Diphenyl Diisocyanate (MDI), Polyurethane System)

Dow Inc. (DOWLEX, AFFINITY)

Huntsman Corporation (VITON, TIOXIDE)

Sekisui Chemical Co., Ltd. (S-LINE, Thermoplastic Elastomers)

Saint-Gobain (Abrasives, Gypsum)

Deepak Nitrite Ltd. (Nitrobenzene, Aniline)

Shijiazhuang Fengshan Chemical Co. Ltd. (Sodium Nitrite, Sodium Nitrate)

Ural Chem JSC (Sodium Nitrite, Sodium Nitrate)

Linyi Luguang Chemical Co. Ltd. (Sodium Nitrite, Sodium Nitrate)

Radiant Indus Chem Pvt. Ltd. (Sodium Nitrite, Potassium Nitrite)

Yingfengyuan Industrial Group Limited (Sodium Nitrite, Sodium Nitrate)

SABIC (SABIC Polycarbonate, SABIC PP)

Merck KGaA (Sigma-Aldrich, Millipore)

Solvay (Sodium Carbonate, Soda Ash)

LANXESS (Bayferrox, Levasil)

Albemarle Corporation (Bromine, Refining Solutions)

Mitsubishi Chemical Corporation (Polypropylene, Methacrylate)

DSM (Dyneema, Akulon)

In May 2024: Media Fusion and Crain Communications announced the first sustainable Polyurethane and Foam Expo Show in India at the NESCO, Bombay Exhibition Center. With an emphasis on environmentally friendly business practices, this event sought to unite manufacturers and producers of PU materials, products, and technologies.

In March 2024, Milliken & Company to improve polyurethane formulations displayed a wide range of colorants and additives. By providing increased recovery yields and boosting post-industrial and post-consumer usage without affecting the color of the recycled polyol, these developments support environmentally friendly foam production methods.

| Report Attributes | Details |

| Market Size in 2023 | USD 46.5 Billion |

| Market Size by 2032 | USD 86.3 Billion |

| CAGR | CAGR of 7.1% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Flexible Foams, Rigid Foams ) • By Application(Bedding & Furniture, Transportation, Packaging, Construction, Electronics, Footwear, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Covestro AG, BASF SE, Wanhua Chemical Group Co., Ltd., Dow Inc., Huntsman Corporation, Sekisui Chemical Co., Ltd., Saint-Gobain, and others. |

| Key Drivers | • Increasing demand in E-Commerce and packaging needs drives the market growth. |

| RESTRAINTS | • Volatility in raw material supply chain may hamper the market growth. |

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Ans: Key Stakeholders Considered in the study:

Raw material vendors

Distributors/traders/wholesalers/suppliers

Regulatory authorities, including government agencies and NGO

Commercial research & development (R&D) institutions

Importers and exporters

Government organizations, research organizations, and consulting firms

Trade/Industrial associations

End-use industries are the stake holder in this report

Ans: The worldwide execution of COVID-19 lockdowns brought about an impressive drop in MDI interest from March to June 2020. The vital clients in Asia Pacific either dropped or deferred their development orders. The decrease sought after for MDI in Europe was to a great extent because of a drop popular for polyurethane froths from the vehicle area. The episode and spread of COVID-19 has brought about a TDI shortage in significant spots all over the planet.

Ans: The high costs of essential feedstock materials are the challenges faced by the Polyurethane Foam Market.

Ans: The Polyurethane Foams Market size was USD 46.5 billion in 2023 and is expected to reach USD 86.3 Million by 2032 and grow at a CAGR of 7.1% over the forecast period of 2024-2032.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

3.1 Market Driving Factors Analysis

3.1.2 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 PESTLE Analysis

3.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 By Production Capacity and Utilization, by Country, By Type, 2023

5.2 Feedstock Prices, by Country, By Type, 2023

5.3 Regulatory Impact, by l Country, By Type, 2023.

5.4 Environmental Metrics: Emissions Data, Waste Management Practices, and Sustainability Initiatives, by Region

5.5 Innovation and R&D, Type, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 By Product Benchmarking

6.3.1 By Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion Plans and New Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Polyurethane Foams Market Segmentation, By Product

7.1 Chapter Overview

7.2 Rigid Foam

7.2.1 Rigid Foam Trends Analysis (2020-2032)

7.2.2 Rigid Foam Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Flexible Foam

7.3.1 Flexible Foam Market Trends Analysis (2020-2032)

7.3.2 Flexible Foam Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Polyurethane Foams Market Segmentation, by Application

8.1 Chapter Overview

8.2 Bedding & Furniture

8.2.1 Bedding & Furniture Market Trends Analysis (2020-2032)

8.2.2 Bedding & Furniture Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Transportation

8.3.1 Transportation Market Trends Analysis (2020-2032)

8.3.2 Transportation Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Packaging

8.4.1 Packaging Market Trends Analysis (2020-2032)

8.4.2 Packaging Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Construction

8.5.1 Construction Market Trends Analysis (2020-2032)

8.5.2 Construction Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Electronics

8.6.1 Electronics Market Trends Analysis (2020-2032)

8.6.2 Electronics Market Size Estimates and Forecasts to 2032 (USD Billion)

8.7 Footwear

8.7.1 Footwear Market Trends Analysis (2020-2032)

8.7.2 Footwear Market Size Estimates and Forecasts to 2032 (USD Billion)

8.8 Others

8.8.1 Others Market Trends Analysis (2020-2032)

8.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.4 North America Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.5.2 USA Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.6.2 Canada Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.7.2 Mexico Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.5.2 Poland Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.6.2 Romania Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.4 Western Europe Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.5.2 Germany Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.6.2 France Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.7.2 UK Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.8.2 Italy Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.9.2 Spain Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.12.2 Austria Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.4 Asia Pacific Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 China Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 India Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 Japan Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.6.2 South Korea Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.7.2 Vietnam Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.8.2 Singapore Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.9.2 Australia Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.4 Middle East Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.5.2 UAE Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.4 Africa Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Polyurethane Foams Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.4 Latin America Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.5.2 Brazil Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.6.2 Argentina Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.7.2 Colombia Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Polyurethane Foams Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Polyurethane Foams Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10. Company Profiles

10.1 Covestro AG

10.1.1 Company Overview

10.1.2 Financial

10.1.3 By Product / Services Offered

10.1.4 SWOT Analysis

10.2 BASF SE

10.2.1 Company Overview

10.2.2 Financial

10.2.3 By Product / Services Offered

10.2.4 SWOT Analysis

10.3 Wanhua Chemical Group Co., Ltd.

10.3.1 Company Overview

10.3.2 Financial

10.3.3 By Product / Services Offered

10.3.4 SWOT Analysis

10.4 Dow Inc.

10.4.1 Company Overview

10.4.2 Financial

10.4.3 By Product / Services Offered

10.4.4 SWOT Analysis

10.5 Huntsman Corporation

10.5.1 Company Overview

10.5.2 Financial

10.5.3 By Product / Services Offered

10.5.4 SWOT Analysis

10.6 Sekisui Chemical Co., Ltd.

10.6.1 Company Overview

10.6.2 Financial

10.6.3 By Product / Services Offered

10.6.4 SWOT Analysis

10.7 Saint-Gobain

10.7.1 Company Overview

10.7.2 Financial

10.7.3 By Product / Services Offered

10.7.4 SWOT Analysis

10.8 Deepak Nitrite Ltd.

10.8.1 Company Overview

10.8.2 Financial

10.8.3 By Product / Services Offered

10.8.4 SWOT Analysis

10.9 Shijiazhuang Fengshan Chemical Co. Ltd.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 By Product / Services Offered

10.9.4 SWOT Analysis

10.10 Ural Chem JSC

10.10.1 Company Overview

10.10.2 Financial

10.10.3 By Product / Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Product

By Application

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

Europe

Asia Pacific

Middle East & Africa

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

The Hydrogen Fluoride Gas Detection Market Size was USD 605.63 Million in 2023 and will reach $976.29 Mn by 2032, growing at a CAGR of 5.47% by 2024-2032.

The Industrial Filtration Market size was USD 35.37 billion in 2023 and is expected to Reach USD 54.35 billion by 2032 and grow at a CAGR of 5.61% over the forecast period of 2024-2032.

The Cyclohexanone Market size was valued at USD 8.8 Billion in 2023. It is expected to grow to USD 12.6 Billion by 2032 and grow at a CAGR of 4.1% over the forecast period of 2024-2032.

The Benzoates Market Size was valued at USD 3.42 Billion in 2023 and is expected to reach USD 5.73 Billion by 2032, growing at a CAGR of 5.89% over the forecast period of 2024-2032.

The Tight Gas Market Size was valued at USD 12.76 trillion cubic feet in 2023 and is expected to reach USD 19.97 trillion cubic feet by 2032 and grow at a CAGR of 5.85% over the forecast period 2024-2032.

The Digital Textile Printing Inks Market size was USD 1.7 billion in 2023 and is expected to reach USD 4.1 billion by 2032 and grow at a CAGR of 9.6% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd