The Plastic Films & Sheets market size was valued at USD 135 billion in 2023 and is expected to reach USD 212.3 billion by 2032 and grow at a CAGR of 5.20% over the forecast period 2024-2032. The plastic films & sheets market report provides a comprehensive analysis of production capacity and utilization rates by country and type, highlighting key manufacturing hubs. It examines raw material price trends, including fluctuations in polyethylene, polypropylene, and PVC costs across major regions. The report also explores the regulatory impact, covering evolving policies such as plastic bags and recycling mandates worldwide. Additionally, it assesses environmental metrics, including recycling rates and sustainability initiatives, alongside R&D and innovation trends in high-barrier and biodegradable films. Lastly, the report provides insights into end-user demand shifts, analyzing growth trends in packaging, agriculture, healthcare, and industrial applications.

Get More Information on Plastic Films & Sheets Market - Request Sample Report

Drivers

Growing demand for bi-axially oriented films drives market growth.

Increasing demand for bi-axially oriented films (BO films) owing to their better mechanical and glossy property along with enhanced barrier performance are factors involved in the growth of the market. This grade of films such as BOPP (bi-axially oriented polypropylene), BOPET (bi-axially oriented polyester), and BOPA (bi-axially oriented polyamide) find applications in food packaging, pharmaceuticals, and industrial applications owing to their improved mechanical strength, moisture barrier, and printability. Moreover, the growing inclination towards sustainable and lightweight packaging solutions coupled with rising flexible packaging adoption in e-commerce and FMCG sectors provide an impetus for market growth. The growth of the industry is further boosted by the advent of film processing technologies and recyclable BO films that meet the growing regulatory and environmental requirements.

Restraint

Fluctuating raw material prices which may hamper the market growth.

The variations in prices of the raw materials are one of the key restraining factors to the growth of this market. The key raw materials for plastic films & sheets such as polypropylene (PP), polyethylene (PE), polyvinyl chloride (PVC), and polyethylene terephthalate (PET) are derived from crude oil and natural gas. With rising geopolitical tensions, supply-chain disruptions, and energy prices fluctuating from parity, price variability in petrochemical feedstocks affects the production costs of plastic films and sheets. This inconsistency puts financial stress on the manufacturers impacting profit margins and pricing. Moreover, a sudden spike in the cost can cause supply shortages, and delays in the production cycle, and the end-users in the packaging, agriculture, and construction sectors could lower the purchasing capacity. To address these concerns, manufacturers are looking into expanding their reach into recycled and bio-based counterparts to reduce reliance on fossil-fuel-based raw materials and better balance pricing.

Opportunities

Growing use of high-barrier films in food packaging creating an opportunity for the market.

The key factor driving the demand for plastic films, particularly high-barrier films is the significant growth of the market for extended shelf-life and food safety which is expected to create remarkable opportunities in the plastic films & sheets Market. Films with higher barriers, like EVOH (ethylene vinyl alcohol), PVDC-coated, metalized films, and multi-layer laminates provide the best moisture, oxygen, and UV resistance to protect the contents from spoilage and preserve freshness. The rise in demand for such fresh and ready-to-eat meals along with frozen and perishable items from the e-commerce and retail sectors are further driving the advanced packaging products demand. Moreover, the increasing government mandates regarding food safety and waste reduction are encouraging manufacturers to develop cost-competitive high-performance recyclable barrier films, which is anticipated to offer the market manufacturers attractive innovation and expansion opportunities.

Challenges

Limited raw material availability major challenge for Plastic Films & Sheets market.

One of the key factors hampering the Plastic Films & Sheets (HPFs) market is the raw material availability as HPF production is based on a limited range of fluorspar, one of the critical minerals needed for its production. Supply chain disruptions and the consequent price volatility have been major issues plaguing the chemical sector which, in tandem with ongoing geopolitical tensions, export restrictions, and mining swings, have reduced the overall production capacity of fluoropolymers. Strong fluorspar reserves are often accompanied by export control practices from countries that do hold the reserves, in prioritizing domestic industry over external supply during constrained market conditions. The associated extraction and refining costs further complicate matters and make pricing stability difficult to sustain among manufacturers. The growing demand for high-performance fibers in the automotive, aerospace, semiconductors, and renewable energy sectors is a primary driver for these HPF suppliers to address high raw material supply risks at competitive prices for players in the market. In response, companies are investigating different sourcing solutions, recycling technologies, and sustainable production methods for fluoropolymers.

By Material Type

LDPE/LLDPE held the largest market share around 38% in 2023. This is due to their overall performance such as versatility and cost, transparency, and mechanical properties (High tensile strength). With high flexibility and impact resistance, moisture barrier, and transparency, they are popular in the food packaging industry, agriculture films, industrial liners, and some medical applications. Also, their increased supremacy in the Flexible packaging solutions which are increasing with consumer demand as well as food & beverage and e-commerce sectors reinforces demand and therefore reflects their ascendant status. Moreover, LDPE/LLDPE films are also extremely recyclable and processable, making them an integral part of the global sustainability movement. They can be combined with additives to increase UV resistance, antistatic properties, and durability which makes them the preferred option for several end-user industries, further strengthening its market position.

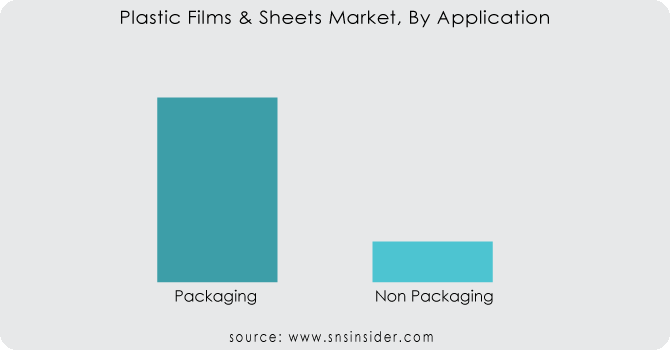

By Application

The packaging held the largest market share around 68% in 2023. The rising demand for lightweight, flexible, and durable packaging solutions in various sectors including food & beverage, pharmaceuticals, personal care, and e-commerce. Plastic films offer excellent moisture, oxygen and contaminants barrier properties and ensure product safety and shelf life. Furthermore, the fast-paced growth of the e-commerce and retail industries and the changing consumer trend for convenience and single-use packaging have strongly embedded the position of plastic films in several packaging applications. Enhancements in their attractiveness for cost competitiveness, functionality, and recyclability have continued to cement their place at the head of the market.

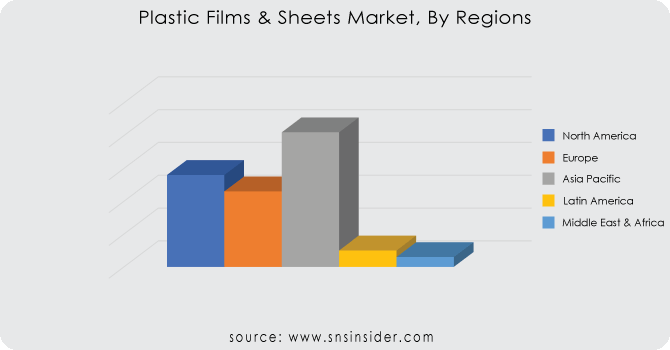

Asia Pacific held the largest market share around 42% in 2023. It is owing to its well-established manufacturing industry, high demand for packaged goods and rapid rate of industrialization in emerging economies. It is the major plastic producers and converters in that region gain from low production cost, high availability of raw materials, and availability of processing technologies. Market growth is mainly driven by rapid demand for flexible packaging in the food & beverage, pharmaceutical, and e-commerce industry, particularly for countries such as China, India, and Japan. In Asia Pacific, the high-growth agriculture sector also supports the growth of mulch films, greenhouse films, and silage wraps. The market expansion is further strengthened due to government initiatives for bioplastics and recyclable plastics which help the region stay dominant over the market.

North America held the significant market share. It is driven by the regions established packaging industry besides also high demand for high-performance films and advanced recycling infrastructure. Strong end-user consumption of flexible packaging in food & beverage, pharmaceutical, and personal care industries in the form of packaging for extension of shelf-life and convenience are driving demand in this region. Moreover, the market is further boosted by the ongoing developments in barrier films, biodegradable plastics, and multi-layered structures. Market growth is further accelerated by a favorable e-commerce scenario and strict government regulations to promote sustainable packaging solutions among key market players. In addition to this, North America holds a significant market position due to the increasing industrial and agricultural applications as well as tremendous investments in recyclable and bio-based plastic films.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Novolex (Eco-Products, Shields Poly Films)

Saudi Basic Industries Corporation (SABIC) (LLDPE Films, BOPP Films)

Toyobo Co. Ltd (HINOMARU Film, COSMOSHINE SRF)

British Polythene Industries Plc (Silage Films, Pallet Wrap)

The Dow Company (ELITE Polyethylene, INNATE Precision Packaging Resins)

DuPont (Mylar Polyester Films, Tedlar PVF Films)

Toray Industries, Inc. (LUMIRROR Polyester Film, TORAYFAN™ PP Films)

Berry Global, Inc. (FormiFor Films, AgriSeal Films)

Plastic Film Corporation of America (PVC Films, PETG Films)

Bemis Company, Inc. (PerfecTear Films, SmartTack Films)

Sealed Air Corporation (Cryovac Barrier Films, Opti Shrink Films)

Uflex Ltd (FLEXPET Polyester Films, FLEXMETPROTECT Metallized Films)

Amcor Plc (Propafilm OPP Films, EcoLam Recyclable Films)

Avery Dennison Corporation (FASSON Overlaminate Films, Nexgen Films)

Jindal Poly Films Limited (BICOR BOPP Films, MICRORITE Anti-fog Films)

Mitsubishi Chemical Corporation (Hostaphan Polyester Films, Diafoil PET Films)

Inteplast Group (AmTopp BOPP Films, VISTOPP Stretch Films)

Polyplex Corporation Ltd. (Sarafil Polyester Films, BOPET Heat-sealable Films)

Cosmo Films Ltd. (BOPP Thermal Lamination Films, Synthetic Paper)

Klöckner Pentaplast (Pentapharm Medical Films, Pentaclear Packaging Films)

In May 2023, three industry leaders - Berry Global Group, Peel Plastic Products Ltd., and ExxonMobil - joined forces to create a more sustainable future for pet food packaging. Their collaboration focuses on incorporating certified recycled plastics into packaging for household pet food brands. This initiative leverages ExxonMobil's innovative Exxtend™ technology, which uses advanced recycling to transform plastic waste into high-quality, food-safe packaging materials. This approach, known as mass balance, ensures the responsible use of recycled content.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 135 Billion |

| Market Size by 2032 | US$ 212.3 Billion |

| CAGR | CAGR of 5.20% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (LLDPE, LDPE, HDPE, BOP, CPP, PVC, PES, PA, Others) • By Application (Packaging, Non-Packaging) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Novolex, Saudi Basic Industries Corporation (SABIC), Toyobo Co. Ltd, British Polythene Industries Plc, The Dow Company, DuPont, Toray Industries, Inc., Berry Global, Inc., Plastic Film Corporation of America, Bemis Company, Inc., Sealed Air Corporation, Uflex Ltd, Amcor Plc, Avery Dennison Corporation, Jindal Poly Films Limited, Mitsubishi Chemical Corporation, Inteplast Group, Polyplex Corporation Ltd., Cosmo Films Ltd., Klöckner Pentaplast |

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Ans: Primary or secondary type of research done by this reports.

Ans:Asia Pacific held the largest market share in Plastic Films & Sheets Market.

Ans: Fluctuating raw material prices which may hamper the market growth.

Ans: The Plastic Films & Sheets market size was valued at USD 135 billion in 2023 and is expected to reach USD 212.3 billion by 2032 and grow at a CAGR of 5.20% over the forecast period 2024-2032.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Production Capacity and Utilization, by Country, By Type, 2023

5.2 Feedstock Prices, by Country, By Type, 2023

5.3 Regulatory Impact, by Country, By Type 2023.

5.4 Environmental Metrics: Emissions Data, Waste Management Practices, and Sustainability Initiatives, by Region

5.5 Innovation and R&D, Type, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion Plans and New Product Launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Plastic Films & Sheets Market Segmentation, By Material Type

7.1 Chapter Overview

7.2 LDPE/LLDPE

7.2.1 LDPE/LLDPE Trends Analysis (2020-2032)

7.2.2 LDPE/LLDPE Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 PVC

7.3.1 PVC Market Trends Analysis (2020-2032)

7.3.2 PVC Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 PA

7.4.1 PA Trends Analysis (2020-2032)

7.4.2 PA Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 BOPP

7.5.1 BOPP Market Trends Analysis (2020-2032)

7.5.2 BOPP Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 HDPE

7.6.1 HDPE Trends Analysis (2020-2032)

7.6.2 HDPE Market Size Estimates and Forecasts to 2032 (USD Billion)

7.7 CPP

7.7.1 CPP Trends Analysis (2020-2032)

7.7.2 CPP Market Size Estimates and Forecasts to 2032 (USD Billion)

7.8 Others

7.8.1 Others Trends Analysis (2020-2032)

7.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Plastic Films & Sheets Market Segmentation, by End-Use Industry

8.1 Chapter Overview

8.2 Packaging

8.2.1 Packaging Market Trends Analysis (2020-2032)

8.2.2 Packaging Market Size Estimates and Forecasts to 2032 (USD Billion)

8.2.3 Food

8.2.3.1 Food Market Trends Analysis (2020-2032)

8.2.3.2 Food Market Size Estimates and Forecasts to 2032 (USD Billion)

8.2.4 Consumer Goods

8.2.4.1 Consumer Goods Market Trends Analysis (2020-2032)

8.2.4.2 Consumer Goods Market Size Estimates and Forecasts to 2032 (USD Billion)

8.2.5 Medical

8.2.5.1 Medical Market Trends Analysis (2020-2032)

8.2.5.2 Medical Market Size Estimates and Forecasts to 2032 (USD Billion)

8.2.6 Others

8.2.6.1 Others Market Trends Analysis (2020-2032)

8.2.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Non-packaging

8.3.1 Non-packaging Market Trends Analysis (2020-2032)

8.3.2 Non-packaging Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3.3 Construction

8.3.3.1 Construction Market Trends Analysis (2020-2032)

8.3.3.2 Construction Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3.4 Healthcare

8.3.4.1 Healthcare Market Trends Analysis (2020-2032)

8.3.4.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3.5 Agriculture

8.3.5.1 Agriculture Market Trends Analysis (2020-2032)

8.3.5.2 Agriculture Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3.6 Others

8.3.6.1 Others Market Trends Analysis (2020-2032)

8.3.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.2.4 North America Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.2.5.2 USA Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.2.6.2 Canada Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.2.7.2 Mexico Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.5.2 Poland Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.6.2 Romania Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.4 Western Europe Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.5.2 Germany Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.6.2 France Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.7.2 UK Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.8.2 Italy Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.9.2 Spain Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.12.2 Austria Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.4 Asia Pacific Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.5.2 China Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.5.2 India Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.5.2 Japan Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.6.2 South Korea Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.2.7.2 Vietnam Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.8.2 Singapore Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.9.2 Australia Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.4 Middle East Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.5.2 UAE Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.2.4 Africa Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Plastic Films & Sheets Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.6.4 Latin America Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.6.5.2 Brazil Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.6.6.2 Argentina Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.6.7.2 Colombia Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Plastic Films & Sheets Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Plastic Films & Sheets Market Estimates and Forecasts, by End-Use Industry (2020-2032) (USD Billion)

10. Company Profiles

10.1 Novolex

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Product / Services Offered

10.1.4 SWOT Analysis

10.2 Saudi Basic Industries Corporation

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Product/ Services Offered

10.2.4 SWOT Analysis

10.3 Toyobo Co. Ltd

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Product/ Services Offered

10.3.4 SWOT Analysis

10.4 British Polythene Industries Plc

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Product/ Services Offered

10.4.4 SWOT Analysis

10.5 The Dow Company

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Product/ Services Offered

10.5.4 SWOT Analysis

10.6 DuPont

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Product/ Services Offered

10.6.4 SWOT Analysis

10.7 Toray Industries, Inc

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Product/ Services Offered

10.7.4 SWOT Analysis

10.8 Berry Global, Inc

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Product/ Services Offered

10.8.4 SWOT Analysis

10.9 Plastic Film Corporation of America

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Product/ Services Offered

10.9.4 SWOT Analysis

10.10 Bemis Company, Inc

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Product/ Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Material Type

LDPE/LLDPE

PVC

PA

BOPP

HDPE

CPP

Others

By Application

Packaging

Food

Consumer Goods

Medical

Others

Non-packaging

Construction

Healthcare

Agriculture

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Polymer Bearing Market Size was valued at USD 10.81 billion in 2023 and is expected to reach USD 16.07 billion by 2032 and grow at a CAGR of 4.50% over the forecast period 2024-2032.

The Intumescent Coatings Market Size was valued at USD 1.18 Billion in 2023 and is expected to reach USD 1.97 Billion by 2032, growing at a CAGR of 5.88% over the forecast period of 2024-2032.

Thermoplastic Polyurethane Adhesive Market Size is expected to reach USD 2.43 Billion by 2032, growing at a CAGR of 7.07% from 2024 to 2032.

The industrial coatings market size was valued at USD 116.38 billion in 2023 and is expected to reach USD 161.06 billion by 2032 and grow at a CAGR of 3.68% over the forecast period 2024-2032.

Graphene Market Size was valued at USD 366.5 Million in 2023 and is expected to grow to USD 4997.1 Million by 2032, exhibiting a CAGR of 33.2% from 2024-2032.

The Epoxy Adhesives Market Size was valued at USD 9.6 billion in 2023 and is expected to reach USD 14.8 billion by 2032 and grow at a CAGR of 4.9% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd