Get More information on Period Panties Market - Request Free Sample Report

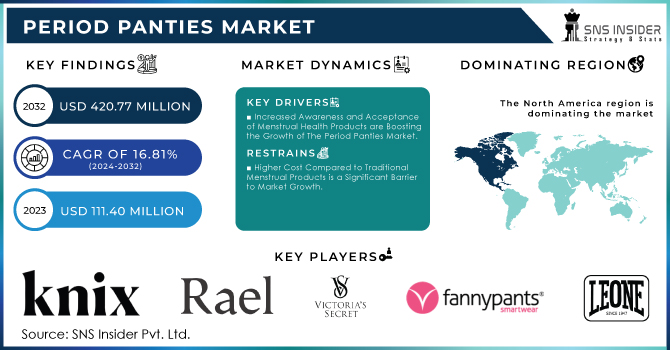

The Period Panties Market Size was valued at USD 133.24 Million in 2023 and is expected to reach USD 558.03 Million by 2032, growing at a CAGR of 17.25% over the forecast period of 2024-2032.

The Period Panties Market is redefining menstrual care with its cost-effectiveness and sustainability. Our report explores a detailed cost comparison with traditional products, proving long-term savings despite higher upfront costs. The rise of e-commerce sales is outpacing offline retail, making period panties more accessible. However, inflation and economic conditions are influencing material costs and pricing strategies. Celebrity endorsements are also shaping consumer choices, with influential figures driving awareness and demand. To assess product efficiency, our report includes a comparative analysis of absorbency levels, helping consumers make informed decisions. As pricing, sales channels, and performance metrics continue to evolve, understanding these dynamics is key to navigating this rapidly expanding market.

The US Period Panties Market Size was valued at USD 19.21 Million in 2023 and is expected to reach USD 97.83 Million by 2032, growing at a CAGR of 19.83% over the forecast period of 2024-2032.

The U.S. Period Panties Market is witnessing significant growth, driven by increasing consumer awareness of sustainable menstrual solutions and rising support from health organizations. Backed by initiatives from groups like the American Sustainable Business Network (ASBN) and The National Women's Health Network (NWHN), demand for eco-friendly alternatives is surging. U.S. based companies like Thinx, Knix, and Proof are expanding their product lines, leveraging e-commerce dominance and direct-to-consumer models. Additionally, the FDA’s regulation of menstrual products ensures safety, boosting consumer confidence. Growing social media advocacy and endorsements from influencers further accelerate adoption, making period panties a preferred choice in the evolving feminine hygiene market.

Drivers

Shifting Consumer Preferences Toward Cost-Effective and Long-Term Reusable Menstrual Products Instead of Disposable Hygiene Solutions

Consumers are increasingly shifting towards cost-effective and reusable menstrual products, driving the growth of the Period Panties Market. Traditional sanitary products such as pads and tampons require frequent repurchasing, leading to higher long-term expenses compared to reusable alternatives. With inflation affecting personal care product prices, consumers are seeking budget-friendly solutions that offer durability and reliability. Period panties, designed for multiple years of use, provide significant savings over time, making them an attractive choice. Many brands highlight cost-per-wear comparisons, showcasing how a single period panty can replace hundreds of disposable products over its lifespan. Additionally, financial incentives such as tax exemptions on menstrual products in various U.S. states and discounted subscription models by brands like Proof and Saalt further encourage adoption. Schools and workplaces are also contributing to the shift by incorporating sustainable menstrual products in hygiene initiatives, making period panties more accessible. The growing preference for minimal waste, convenience, and affordability is reshaping consumer buying habits, pushing brands to offer multipacks, bundle deals, and lifetime warranties to enhance product value. This trend is expected to continue as economic pressures and sustainability concerns drive further adoption of reusable menstrual products.

Restraints

Limited Public Awareness and Cultural Taboos Around Menstrual Hygiene Restrict the Market Growth in Certain Regions

Despite the increasing shift toward sustainable menstrual products, many regions still face deep-rooted cultural taboos and limited awareness about reusable options like period panties. In several societies, menstruation remains a stigmatized subject, leading to hesitation in trying new menstrual care alternatives. Many consumers rely on traditional practices or products passed down through generations, making it difficult for reusable solutions to gain traction. Additionally, some consumers harbor misconceptions about hygiene and maintenance, assuming that washing and reusing period panties is less sanitary than disposable alternatives. Insufficient marketing campaigns, lack of educational initiatives, and inadequate accessibility in rural areas further hinder adoption. Even in developed markets, many individuals remain unaware of the benefits of period panties, such as environmental sustainability, cost savings, and enhanced comfort. To counteract this, brands must invest in awareness campaigns, partner with healthcare professionals, and advocate for menstrual hygiene education in schools and workplaces. Without addressing these social and educational gaps, the Period Panties Market may struggle to reach its full potential, especially in culturally conservative regions.

Opportunities

Increasing Adoption of Sustainable Menstrual Solutions in Schools and Workplaces Drives Market Growth and Brand Visibility

The rising emphasis on sustainable menstrual hygiene solutions in schools and workplaces presents a significant opportunity for the Period Panties Market. As concerns over period poverty and environmental waste grow, many educational institutions and companies are integrating reusable menstrual products into their wellness and sustainability programs. In the United States, states like California and New York have implemented free menstrual product initiatives in public schools, increasing accessibility to sustainable options. Similarly, businesses are incorporating eco-friendly menstrual solutions into their corporate wellness programs to promote employee well-being and workplace inclusivity. The involvement of government-backed programs and non-profit organizations further strengthens the adoption rate, creating avenues for brands to expand their consumer base. Several universities have also started offering reusable menstrual products in campus hygiene dispensers, enhancing product visibility among young consumers. Additionally, companies are developing bulk-purchase partnerships with institutions, allowing them to distribute period panties at subsidized rates or through corporate health packages. By leveraging these institutional sales opportunities, manufacturers can significantly boost brand awareness and consumer trust, ultimately driving market growth.

Challenge

Competition from Alternative Sustainable Menstrual Products Such as Menstrual Cups and Reusable Pads Slowing Market Expansion

While the Period Panties Market is gaining traction, it faces stiff competition from other sustainable menstrual products, including menstrual cups and reusable cloth pads. Many consumers prefer menstrual cups due to their longer wear time, higher capacity, and lower maintenance compared to period panties, which require frequent washing. Additionally, menstrual cups and reusable pads tend to have a lower price point, making them more appealing to cost-sensitive consumers. Some individuals also find menstrual cups more convenient for travel, sports, and overnight protection, further reducing the appeal of period panties in certain segments. Moreover, traditional menstrual care brands have expanded their offerings, promoting eco-friendly pads and tampons with biodegradable materials, creating additional competition. To differentiate themselves, period panty manufacturers are focusing on innovative designs, hybrid products, and improved absorbency technology. Brands are also emphasizing comfort, discretion, and leak-proof guarantees to attract consumers who prioritize convenience and sustainability. Despite the competitive landscape, continuous product innovation and strategic marketing campaigns will be essential for sustained growth in the reusable menstrual care sector.

By Type

The Reusable segment dominated the Period Panties Market in 2023, holding a 70.5% market share, primarily due to the increasing focus on sustainability and long-term cost savings. Organizations like the Environmental Protection Agency (EPA) and the United Nations Environment Programme (UNEP) have raised awareness about the growing issue of menstrual waste, which has led consumers to shift from disposable pads and tampons to reusable alternatives. Additionally, reusable period panties provide better comfort, enhanced absorbency, and reduced irritation compared to traditional products. The rise of zero-waste movements and plastic-free menstrual product campaigns has further accelerated demand. The Menstrual Health Alliance and the World Health Organization (WHO) have also emphasized the importance of affordable and sustainable menstrual solutions, which has led governments in the U.S., Canada, and the U.K. to introduce tax exemptions on reusable menstrual products. Companies like Thinx, Knix, and Modibodi have launched advanced leak-proof technologies, making reusable period panties a preferred choice among environmentally conscious consumers.

By Style

The Brief style dominated the Period Panties Market in 2023, accounting for a 42.2% market share, owing to its high coverage, secure fit, and leak-proof protection. Brief-style period panties are particularly popular among working professionals, teenagers, and postpartum women, as they offer better support and comfort during heavy flow days. Organizations such as the American College of Obstetricians and Gynecologists (ACOG) have recommended full-coverage menstrual underwear for individuals experiencing heavy menstrual bleeding (HMB), which has contributed to the demand for brief-style period panties. Additionally, brands like Saalt, Bambody, and Ruby Love have introduced brief-style options with moisture-wicking layers and odor-resistant technology, making them a preferred choice among consumers. The Menstrual Hygiene Day initiative has also emphasized the importance of comfortable and effective period solutions, which has increased consumer preference for this style. Furthermore, with women engaging more in sports and outdoor activities, the brief style provides added security and confidence, further solidifying its dominance in the market.

By Material

The Cotton segment dominated the Period Panties Market in 2023 and held a 41.3% market share in 2023, driven by its breathability, softness, and skin-friendly properties. Consumers prefer cotton-based period panties due to their natural fiber composition, which reduces the risk of irritation, allergies, and infections. According to the National Institutes of Health (NIH), synthetic fabrics like polyester and nylon can trap heat and moisture, increasing the likelihood of bacterial growth and discomfort, making cotton the superior choice. Leading brands such as Thinx, Aisle, and Rael offer 100% organic cotton period panties, which appeal to health-conscious consumers. Additionally, the Organic Cotton Accelerator (OCA) and the Global Organic Textile Standard (GOTS) have promoted the use of chemical-free, organic cotton, increasing its adoption in menstrual hygiene products. Government policies in the U.S. and Europe that support organic and sustainable textiles have further fueled the demand for cotton-based period panties. The shift toward hypoallergenic and eco-friendly menstrual solutions continues to drive the dominance of cotton in the period panties market.

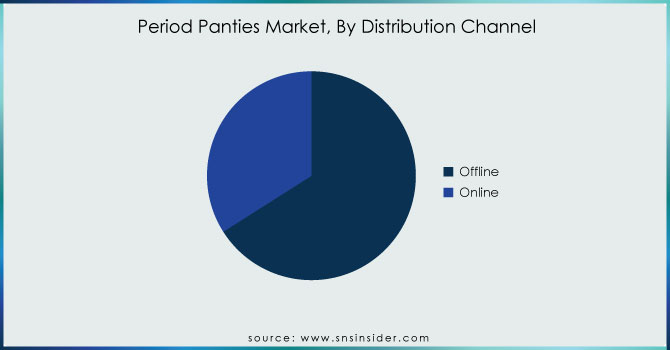

By Distribution Channel

Online Retailers dominated the Period Panties Market in 2023 and accounted for a 53.7% market share in the Period Panties Market in 2023, driven by the increasing popularity of e-commerce platforms and direct-to-consumer (DTC) brand strategies. Consumers prefer purchasing period panties online due to the wide range of options, detailed product descriptions, and easy comparison of features and prices. Companies like Amazon, Walmart, and Target, along with brand-specific websites such as Knix, Modibodi, and Saalt, have significantly expanded their online offerings, making period panties more accessible globally. The COVID-19 pandemic accelerated digital shopping trends, leading to a permanent shift in consumer behavior toward online retail platforms. According to the U.S. Census Bureau, e-commerce sales in the personal care and hygiene sector increased by 24% in 2023, indicating strong online demand. Additionally, the rise of subscription-based models and influencer marketing on platforms like Instagram and TikTok has fueled direct online sales. Discounts, free shipping, and flexible return policies offered by major online retailers further contribute to this distribution channel's dominance.

Get Customized Report as per your Business Requirement - Request For Customized Report

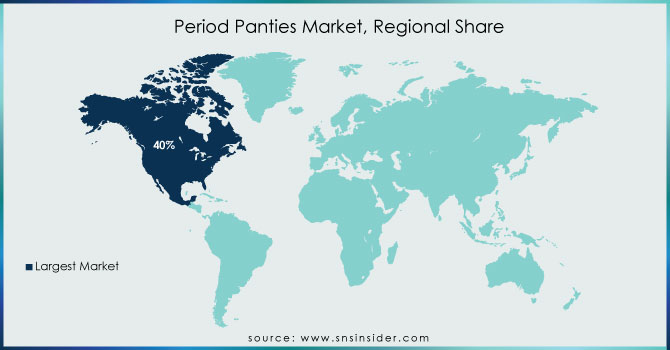

The Asia Pacific region dominated the Period Panties Market in 2023, capturing a 41.6% market share, driven by rising menstrual hygiene awareness, government initiatives, and an expanding middle-class population. Countries like China, India, and Japan have witnessed a surge in demand due to increasing disposable income and growing concerns over menstrual waste. The Indian government’s Menstrual Hygiene Scheme (MHS) and China’s initiatives to promote sustainable hygiene products have significantly contributed to this growth. The Asia-Pacific Menstrual Hygiene Coalition has actively promoted reusable menstrual products, leading to higher adoption rates. Additionally, companies like Unicharm, Wuka, and Modibodi have expanded their presence in Asia Pacific, increasing product accessibility. China, the largest contributor, benefits from strong e-commerce sales through Alibaba and JD.com, while India, the fastest-growing market, has seen a surge in demand due to brands like Sirona and Pee Safe offering affordable and eco-friendly period panties. Japan’s preference for high-tech fabric innovations in menstrual hygiene products further strengthens the region’s dominance.

Moreover, North America emerged as the fastest-growing region in the Period Panties Market, with a significant growth rate during the forecast period, driven by rising sustainability trends, increasing menstrual equity initiatives, and growing brand penetration. The United States leads the regional market, fueled by government policies promoting sustainable menstrual products, such as the Menstrual Equity for All Act. The U.S. Food and Drug Administration (FDA) has also emphasized the safety of reusable menstrual products, increasing consumer confidence. Additionally, organizations like Period.org and The Menstrual Equity Coalition actively promote awareness and accessibility of period panties. Leading brands such as Thinx, Knix, and Ruby Love have witnessed significant sales growth, with direct-to-consumer e-commerce platforms playing a vital role. Canada, the second-largest market, is expanding rapidly due to government-backed free menstrual product programs and increased consumer awareness. Meanwhile, Mexico’s growing middle-class population and increasing online retail penetration have fueled demand, making North America a highly lucrative market for period panties.

Aisle (formerly Lunapads) (Lunapads Reusable Period Pads, Luna Undies, Menstrual Cup)

Anigan Inc. (Anigan Period Panties, Anigan Absorbent Underwear, Anigan Menstrual Cup)

Clovia (Clovia Period Panties, Clovia Lingerie, Clovia Maternity Wear)

Dear Kate (Dear Kate Period Panties, Dear Kate Activewear, Dear Kate Sleepwear)

FANNYPANTS (FANNYPANTS Leakproof Period Underwear, FANNYPANTS Sleepwear, FANNYPANTS Maternity Wear)

FLUX Undies (FLUX Undies Period Panties, FLUX Undies Sleepwear, FLUX Undies Activewear)

Harebrained (Harebrained Period Panties, Harebrained Leakproof Activewear, Harebrained Sleepwear)

Knix Wear, Inc. (Knix Leakproof Period Underwear, Knix Comfort Bra, Knix Sleep Shorts)

Modibodi (Modibodi Period Underwear, Modibodi Maternity Underwear, Modibodi Swimwear)

Monthly Gift, Inc. (Dear Kate) (Dear Kate Period Panties, Dear Kate Activewear, Dear Kate Sleepwear)

Neione (Neione Period Panties, Neione Absorbent Underwear, Neione Maternity Wear)

Panty Prop Inc. (Ruby Love) (Ruby Love Period Panties, Ruby Love Activewear, Ruby Love Sleepwear)

Period Panteez (Period Panteez Leakproof Underwear, Period Panteez Sleepwear)

Proof (Proof Period Panties, Proof Sleepwear, Proof Activewear)

Rael (Rael Organic Period Panties, Rael Menstrual Pads, Rael Feminine Wipes)

Saalt, LLC (Saalt Period Panties, Saalt Menstrual Cup, Saalt Activewear)

The Period Company (The Period Company Period Underwear, The Period Company Sleepwear)

Thinx, Inc. (Thinx Period Panties, Thinx Thong, Thinx Activewear)

WUKA (WUKA Period Pants, WUKA Activewear, WUKA Swimwear)

December 2024: INTIMINA introduced Bloom Period Underwear, offering leak-proof, breathable, and eco-friendly menstrual protection. The product featured odor control, quick-dry fabric, and multiple absorbency levels, ensuring comfort beyond menstrual days. It was made available on INTIMINA’s website and select retailers.

September 2024: Pee Safe’s Disposable Period Panty campaign helped the brand achieve one million units sold. The high-absorbency, biodegradable design gained popularity among travelers and convenience seekers. The campaign used digital platforms and influencer marketing, strengthening Pee Safe’s market presence in India and beyond.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 133.24 Million |

| Market Size by 2032 | USD 558.03 Million |

| CAGR | CAGR of 17.25% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Reusable, Disposable) •By Style (Brief, Bikini, Boyshort, Hi-Waist, Others) •By Material (Cotton, Polyester, Nylon, Modal, Others) •By Distribution Channel (Direct Sales, Modern Trade, Convenience Stores, Specialty Stores, Mono Brand Stores, Online Retailers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Knix Wear, Inc., Ruby Love (PantyProp Inc.), Saalt, LLC, The Period Company, Proof, WUKA, Aisle (formerly Lunapads), FLUX Undies, Modibodi, Thinx, Inc. and other key players |

Ans: The Period Panties Market is projected to grow from USD 133.24 Million in 2023 to USD 558.03 Million by 2032 at a CAGR of 17.25%.

Ans: The Period Panties Market is growing due to their cost-effectiveness, sustainability, and increasing consumer awareness.

Ans: Online retail dominates the Period Panties Market, accounting for 53.7% of sales due to convenience and subscription-based models.

Ans: Cotton dominates the Period Panties Market with a 41.3% share due to its breathability, comfort, and hypoallergenic properties.

Ans: Increasing adoption of sustainable menstrual solutions in schools and workplaces presents growth opportunities for the Period Panties Market.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Cost Comparison with Conventional Menstrual Products

5.2 E-commerce Sales versus Offline Retail Performance

5.3 Effects of Inflation and Economic Conditions on Market Pricing

5.4 Impact of Celebrity Endorsements on Brand Sales

5.5 Comparative Analysis of Product Absorbency Levels

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Period Panties Market Segmentation, by Type

7.1 Chapter Overview

7.2 Reusable

7.2.1 Reusable Market Trends Analysis (2020-2032)

7.2.2 Reusable Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 Disposable

7.3.1 Disposable Market Trends Analysis (2020-2032)

7.3.2 Disposable Market Size Estimates and Forecasts to 2032 (USD Million)

8. Period Panties Market Segmentation, by Style

8.1 Chapter Overview

8.2 Brief

8.2.1 Brief Market Trends Analysis (2020-2032)

8.2.2 Brief Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Bikini

8.3.1 Bikini Market Trends Analysis (2020-2032)

8.3.2 Bikini Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Boyshort

8.4.1 Boyshort Market Trends Analysis (2020-2032)

8.4.2 Boyshort Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 Hi-Waist

8.5.1 Hi-Waist Market Trends Analysis (2020-2032)

8.5.2 Hi-Waist Market Size Estimates and Forecasts to 2032 (USD Million)

8.6 Others

8.6.1 Others Market Trends Analysis (2020-2032)

8.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

9. Period Panties Market Segmentation, by Material

9.1 Chapter Overview

9.2 Cotton

9.2.1 Cotton Market Trends Analysis (2020-2032)

9.2.2 Cotton Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Polyester

9.3.1 Polyester Market Trends Analysis (2020-2032)

9.3.2 Polyester Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Nylon

9.4.1 Nylon Market Trends Analysis (2020-2032)

9.4.2 Nylon Market Size Estimates and Forecasts to 2032 (USD Million)

9.5 Modal

9.5.1 Modal Market Trends Analysis (2020-2032)

9.5.2 Modal Market Size Estimates and Forecasts to 2032 (USD Million)

9.6 Others

9.6.1 Others Market Trends Analysis (2020-2032)

9.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

10. Period Panties Market Segmentation, by Distribution Channel

10.1 Chapter Overview

10.2 Direct Sales

10.2.1 Direct Sales Market Trends Analysis (2020-2032)

10.2.2 Direct Sales Market Size Estimates and Forecasts to 2032 (USD Million)

10.3 Modern Trade

10.3.1 Modern Trade Market Trends Analysis (2020-2032)

10.3.2 Modern Trade Market Size Estimates and Forecasts to 2032 (USD Million)

10.4 Convenience Stores

10.4.1 Convenience Stores Market Trends Analysis (2020-2032)

10.4.2 Convenience Stores Market Size Estimates and Forecasts to 2032 (USD Million)

10.5 Specialty Stores

10.5.1 Specialty Stores Market Trends Analysis (2020-2032)

10.5.2 Specialty Stores Market Size Estimates and Forecasts to 2032 (USD Million)

10.6 Mono Brand Stores

10.6.1 Mono Brand Stores Market Trends Analysis (2020-2032)

10.6.2 Mono Brand Stores Market Size Estimates and Forecasts to 2032 (USD Million)

10.7 Online Retailers

10.7.1 Online Retailers Market Trends Analysis (2020-2032)

10.7.2 Online Retailers Market Size Estimates and Forecasts to 2032 (USD Million)

10.8 Others

10.8.1 Others Market Trends Analysis (2020-2032)

10.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.2.3 North America Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.4 North America Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.2.5 North America Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.2.6 North America Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.2.7 USA

11.2.7.1 USA Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.7.2 USA Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.2.7.3 USA Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.2.7.4 USA Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.2.8 Canada

11.2.8.1 Canada Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.8.2 Canada Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.2.8.3 Canada Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.2.8.4 Canada Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.2.9 Mexico

11.2.9.1 Mexico Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.9.2 Mexico Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.2.9.3 Mexico Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.2.9.4 Mexico Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.1.3 Eastern Europe Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.4 Eastern Europe Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.5 Eastern Europe Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.6 Eastern Europe Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.1.7 Poland

11.3.1.7.1 Poland Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.7.2 Poland Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.7.3 Poland Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.7.4 Poland Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.1.8 Romania

11.3.1.8.1 Romania Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.8.2 Romania Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.8.3 Romania Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.8.4 Romania Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.9.2 Hungary Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.9.3 Hungary Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.9.4 Hungary Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.10.2 Turkey Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.10.3 Turkey Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.10.4 Turkey Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.11.2 Rest of Eastern Europe Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.1.11.3 Rest of Eastern Europe Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.1.11.4 Rest of Eastern Europe Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.2.3 Western Europe Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.4 Western Europe Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.5 Western Europe Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.6 Western Europe Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.7 Germany

11.3.2.7.1 Germany Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.7.2 Germany Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.7.3 Germany Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.7.4 Germany Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.8 France

11.3.2.8.1 France Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.8.2 France Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.8.3 France Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.8.4 France Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.9 UK

11.3.2.9.1 UK Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.9.2 UK Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.9.3 UK Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.9.4 UK Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.10 Italy

11.3.2.10.1 Italy Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.10.2 Italy Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.10.3 Italy Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.10.4 Italy Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.11 Spain

11.3.2.11.1 Spain Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.11.2 Spain Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.11.3 Spain Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.11.4 Spain Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.12.2 Netherlands Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.12.3 Netherlands Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.12.4 Netherlands Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.13.2 Switzerland Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.13.3 Switzerland Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.13.4 Switzerland Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.14 Austria

11.3.2.14.1 Austria Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.14.2 Austria Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.14.3 Austria Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.14.4 Austria Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.15.2 Rest of Western Europe Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.3.2.15.3 Rest of Western Europe Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.3.2.15.4 Rest of Western Europe Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.4.3 Asia Pacific Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.4 Asia Pacific Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.5 Asia Pacific Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.6 Asia Pacific Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.7 China

11.4.7.1 China Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.7.2 China Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.7.3 China Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.7.4 China Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.8 India

11.4.8.1 India Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.8.2 India Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.8.3 India Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.8.4 India Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.9 Japan

11.4.9.1 Japan Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.9.2 Japan Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.9.3 Japan Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.9.4 Japan Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.10 South Korea

11.4.10.1 South Korea Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.10.2 South Korea Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.10.3 South Korea Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.10.4 South Korea Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.11 Vietnam

11.4.11.1 Vietnam Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.11.2 Vietnam Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.11.3 Vietnam Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.11.4 Vietnam Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.12 Singapore

11.4.12.1 Singapore Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.12.2 Singapore Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.12.3 Singapore Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.12.4 Singapore Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.13 Australia

11.4.13.1 Australia Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.13.2 Australia Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.13.3 Australia Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.13.4 Australia Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.14.2 Rest of Asia Pacific Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.4.14.3 Rest of Asia Pacific Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.4.14.4 Rest of Asia Pacific Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.1.3 Middle East Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.4 Middle East Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.5 Middle East Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.6 Middle East Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.1.7 UAE

11.5.1.7.1 UAE Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.7.2 UAE Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.7.3 UAE Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.7.4 UAE Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.8.2 Egypt Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.8.3 Egypt Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.8.4 Egypt Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.9.2 Saudi Arabia Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.9.3 Saudi Arabia Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.9.4 Saudi Arabia Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.10.2 Qatar Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.10.3 Qatar Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.10.4 Qatar Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.11.2 Rest of Middle East Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.1.11.3 Rest of Middle East Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.1.11.4 Rest of Middle East Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.2.3 Africa Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.4 Africa Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.2.5 Africa Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.2.6 Africa Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.7.2 South Africa Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.2.7.3 South Africa Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.2.7.4 South Africa Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.8.2 Nigeria Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.2.8.3 Nigeria Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.2.8.4 Nigeria Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.9.2 Rest of Africa Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.5.2.9.3 Rest of Africa Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.5.2.9.4 Rest of Africa Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Period Panties Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.6.3 Latin America Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.4 Latin America Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.6.5 Latin America Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.6.6 Latin America Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.6.7 Brazil

11.6.7.1 Brazil Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.7.2 Brazil Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.6.7.3 Brazil Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.6.7.4 Brazil Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.6.8 Argentina

11.6.8.1 Argentina Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.8.2 Argentina Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.6.8.3 Argentina Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.6.8.4 Argentina Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.6.9 Colombia

11.6.9.1 Colombia Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.9.2 Colombia Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.6.9.3 Colombia Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.6.9.4 Colombia Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Period Panties Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.10.2 Rest of Latin America Period Panties Market Estimates and Forecasts, by Style (2020-2032) (USD Million)

11.6.10.3 Rest of Latin America Period Panties Market Estimates and Forecasts, by Material (2020-2032) (USD Million)

11.6.10.4 Rest of Latin America Period Panties Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Million)

12. Company Profiles

12.1 Knix Wear, Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Ruby Love (PantyProp Inc.)

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Saalt, LLC

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 The Period Company

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Proof

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 WUKA

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Aisle (formerly Lunapads)

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 FLUX Undies

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Modibodi

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Thinx, Inc.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Type

Reusable

Disposable

By Style

Brief

Bikini

Boyshort

Hi-Waist

Others

By Material

Cotton

Polyester

Nylon

Modal

Others

By Distribution Channel

Direct Sales

Modern Trade

Convenience Stores

Specialty Stores

Mono Brand Stores

Online Retailers

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Home Healthcare Devices Market size was valued at USD 61.62 billion in 2023 and is expected to reach USD 122.92 billion by 2032 and grow at a CAGR of 8.0% over the forecast period of 2024-2032.

The Hirsutism Market was valued at USD 3.21 billion in 2023 and is expected to reach USD 6.02 billion by 2032, growing at a CAGR of 7.25% over the forecast period of 2024-2032.

ELISA Analyzers Market was valued at USD 592.69 million in 2023 and is expected to reach USD 877.75 million by 2032, growing at a CAGR of 4.50% from 2024-2032.

The Biochips Market was valued at USD 10.35 billion in 2023 and is expected to reach USD 35.00 billion by 2032, growing at a CAGR of 14.52% from 2024 to 2032.

The Medical Electrodes Market was valued at USD 2.07 billion in 2023 and is expected to reach USD 3.17 billion by 2032, growing at a CAGR of 4.89% from 2024 to 2032.

Orthopedic Software Market Size was valued at USD 384.2 million in 2023 and is expected to reach USD 710.2 million by 2032, growing at a CAGR of 7.1% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd