Pediatric Cancer Biomarker Market Size Analysis

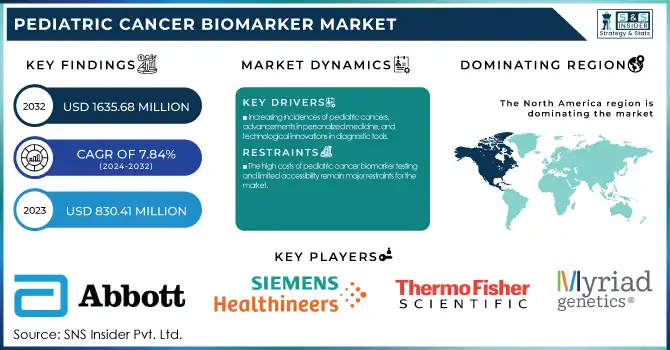

The Pediatric Cancer Biomarker Market was valued at USD 830.41 Million in 2023 and is projected to reach USD 1635.68 Million by 2032 with a growing CAGR of 7.84% over the forecast period of 2024-2032.

This report emphasizes the growing incidence and prevalence of pediatric cancer, driving demand for sophisticated diagnostic technologies, including biomarkers. The research identifies trends in the use of biomarkers across regions, highlighting early detection and personalization of treatment. It also analyzes R&D spending and funding trends, identifying contributions from government programs, private institutions, and commercial players toward developing biomarkers.

To Get more information on Pediatric Cancer Biomarker Market - Request Free Sample Report

The regulatory environment and approval procedures for pediatric cancer biomarkers are also evaluated, as they affect market growth and availability. In addition, the report explores the increasing importance of companion diagnostics and personalized medicine in pediatric oncology, highlighting how biomarker-guided strategies are revolutionizing treatment outcomes and precision care.

Pediatric Cancer Biomarker Market Dynamics

Drivers

-

Increasing incidences of pediatric cancers, advancements in personalized medicine, and technological innovations in diagnostic tools

Based on the American Cancer Society, almost 10,500 children below 15 years are diagnosed with cancer each year in the United States alone, of which leukemia and brain tumors are the most frequent. This increasing incidence of childhood cancer directly enhances the demand for early and precise diagnostic devices, specifically biomarkers that can offer details regarding the genetic makeup of the tumor, crucial for tailored treatment. In addition, the use of liquid biopsy technologies such as NGS (Next-Generation Sequencing) and proteomics is enhancing pediatric cancer diagnostic precision. Targeted therapy and immunotherapy research also propels market growth since the former depends on the identification of certain biomarkers to effectively use them. Investments by government and healthcare in pediatric oncology research, for example, National Cancer Institute (NCI) funding and those by the European Union, also drive the growth of the market. Rising awareness among parents and medical professionals about pediatric cancer also fuels early detection and a larger demand for solutions based on biomarkers.

Restraints

-

The high costs of pediatric cancer biomarker testing and limited accessibility remain major restraints for the market.

The expense of high-diagnostics tests like liquid biopsies and genetic sequencing is out of reach for most families and healthcare systems. For instance, NGS-based tests may vary from USD 1,000 to USD 10,000 based on the level of complexity of the testing involved, which may not be accessible to uninsured patients or in public healthcare systems in developing nations. This cost restricts the mass usage of these technologies, especially in poor areas. In addition, the absence of skilled staff and healthcare facilities to conduct these sophisticated tests in some areas of the globe worsens the situation. The unequal resource and expertise allocation between developed and developing countries contributes to huge imbalances in access to state-of-the-art diagnostics. Moreover, the new biomarker tests' regulatory approval process is lengthy and costly, further contributing to the difficulties in diagnostic companies providing wider access to these life-saving technologies worldwide. Unless there is a concerted effort to reduce the costs, make them more accessible, and eliminate the complexity in regulatory approvals, these will still be the main inhibitors of the market's potential.

Opportunities

-

The growing interest in liquid biopsy and targeted therapies presents substantial opportunities for the pediatric cancer biomarker market.

Liquid biopsy, which tests blood samples for tumor RNA or DNA, provides a non-invasive, inexpensive alternative to standard tissue biopsies and is especially valuable for pediatric patients who are likely to have complications with invasive testing. With the advancement of technology, liquid biopsy will change the face of early detection, monitoring, and treatment response assessment in pediatric cancer. Besides this, the rise in interest in precision medicine and the discovery of targeted therapies in response to selected genetic mutations or biomarkers of pediatric cancers has tremendous growth opportunities. For example, the ALK inhibitors applied to neuroblastoma and the CD19-directed CAR-T cells used in leukemia have yielded impressive outcomes. An illustration of such an outcome following precision medicine depending on biomarkers is the FDA-approved Kymriah in pediatric leukemia. Pediatric oncology biomarker research and development are being strongly supported by pharma firms and biotech companies, which are breaking new grounds for novel therapies. In addition, the cooperation among academic institutions, biotech companies, and pharma companies is resulting in the identification of new biomarkers, thereby paving the way for new diagnostic technologies and therapies for pediatric cancers. Such cooperation among different stakeholders is important for driving future growth.

Challenges

-

The regulatory hurdles associated with the approval and commercialization of new diagnostic tests and treatments.

The FDA's process of approval for new biomarkers usually consists of large-scale clinical trials and data gathering that takes years and costs a great deal. The pediatric population has its special regulatory challenges in that treatment and diagnostic agents need to be particularly tested and reformulated for children, which is distinct from research on adult oncology. The protracted approval times and complexity of regulation requirements across regions have the potential to slow the deployment of life-saving technologies. Another hurdle is the data integration problem, as more genetic and molecular information becomes available using newer diagnostic tools such as NGS and multi-omics, physicians find it challenging to process this information quickly, interpret it, and integrate it into clinical decision-making. The absence of standardized methods for interpreting biomarker data can result in inconsistent results, diluting the utility of tailored treatment strategies. Additionally, concerns about patient privacy and data security in managing patient data complicate the use of digital technology in pediatric cancer biomarker screening. These constraints call for improved regulatory environments, more transparent data-sharing mechanisms, and cooperation among stakeholders to overcome challenges and unlock the full potential of pediatric cancer biomarkers.

Pediatric Cancer Biomarker Market Segmentation Insights

By Indication

In 2023, the leukemia segment held the largest share in the pediatric cancer biomarker market at 41.2% of the overall market share. Leukemia, especially acute lymphoblastic leukemia (ALL), is the leading childhood cancer, and this fuels a high need for biomarker-based diagnostics. CD19, CD22, and minimal residual disease (MRD) markers are some of the biomarkers that have become essential in monitoring the disease, risk stratification, and treatment planning. The growing acceptance of CAR-T cell therapy and targeted therapies that need biomarker-based companion diagnostics has further bolstered leukemia's leadership in the market. In addition, development in flow cytometry, next-generation sequencing (NGS), and polymerase chain reaction (PCR) methodologies has enhanced the early detection and tailored treatment methods. Increased consciousness of precision medicine and an increase in pediatric cancer screening programs among hospitals and research centers have also been key drivers for the robust market presence of this segment.

The CNS tumors segment is growing at the highest rate owing to increasing incidences of pediatric brain and central nervous system tumors and rising investments in biomarker-based diagnostics. The advent of molecular biomarkers such as DNA methylation profiling, cerebrospinal fluid-based liquid biopsies, and NGS-based tests has improved early diagnosis and treatment planning. Moreover, clinical trials of targeted therapies for specific genetic alterations in CNS tumors are driving market growth.

By Biomarker

The CD19, CD20, and CD22 biomarker segments dominated the market in 2023, capturing 30.1% of the overall share, owing mainly to its application in diagnosing and treating pediatric lymphoma and leukemia. The biomarkers are extensively used in immunophenotyping, risk stratification, and minimal residual disease (MRD) monitoring in children. The rising use of CD-targeted immunotherapies, especially CAR-T cell therapies like Kymriah and Tecartus, has also increased their clinical demand further. Additionally, diagnostic laboratories and hospitals are incorporating new technologies like flow cytometry, fluorescence in situ hybridization (FISH), and enzyme-linked immunosorbent assays (ELISA) to enhance the efficiency of biomarker-based testing. The increasing application of targeted therapies and monoclonal antibodies has further cemented the supremacy of biomarkers in pediatric cancer diagnosis.

The ALK (anaplastic lymphoma receptor tyrosine kinase gene) segment is experiencing the highest growth with its increasingly recognized role in pediatric lymphomas and neuroblastoma. Oncogenic drivers in the form of ALK mutations and rearrangements have been recognized, and therefore, are crucial for precision medicine interventions. The increasing use of ALK inhibitors like Crizotinib and Lorlatinib, together with more clinical trials for targeted therapy, have driven market growth. The improvements in liquid biopsy and genomic profiling have also increased the adoption of ALK biomarker testing.

By End Use

The hospital segment contributed the highest share of 41.2% in 2023, as hospitals are still the main centers for pediatric cancer diagnosis, treatment, and biomarker testing. Hospitals contain sophisticated diagnostic equipment, allowing the application of molecular diagnostics, flow cytometry, and genetic sequencing to identify cancer biomarkers effectively. With the growing focus on precision medicine, hospitals are incorporating biomarker-guided strategies into treatment protocols for better patient outcomes. Moreover, government programs and reimbursement policies have facilitated the extensive application of biomarker-based diagnostics in hospitals. The availability of multidisciplinary oncology teams, pediatric specialists, and the capability to perform biopsy-based and liquid biopsy testing have also strengthened the leadership of hospitals in the pediatric cancer biomarker market.

The research institutions segment is the most rapidly growing segment owing to increased investments in biomarker discovery, precision oncology, and pediatric cancer research. Research centers are at the forefront of creating new biomarkers, resulting in new diagnostic devices, targeted therapies, and AI-based biomarker analysis. Growing funding from government grants, private investors, and pharma companies is driving research into multi-omics strategies like genomics, proteomics, and metabolomics. Further, CRISPR gene-editing advances, machine learning for biomarker discovery, and real-time monitoring technologies are widening the scope of biomarkers in pediatric cancer diagnosis.

Pediatric Cancer Biomarker Market Regional Insights

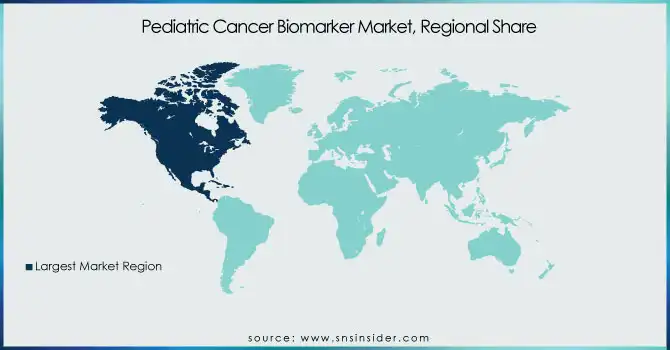

North America dominated the pediatric cancer biomarker market in 2023 with the highest share, driven by its well-developed healthcare infrastructure, extensive use of innovative biomarker diagnostics, and heavy investments in pediatric oncology research. The United States is a key contributor, with leading healthcare providers and research centers heavily investing in the development of pediatric cancer biomarkers. Its dominance of the regional market is supplemented by having dominant pharmaceutical and diagnostic companies present within, boosting its ranking as the global leader in the same area.

At the same time, Europe's market is experiencing steady development, fueled by strong healthcare infrastructure, government support, and a developing focus on personalized medicine. The UK, Germany, and France are the leaders in applying biomarker-driven diagnostics to pediatric cancer, and research institutions have been instrumental in pushing biomarker discovery and clinical utility forward.

The Asia-Pacific market is set to witness high growth in the market, driven by enhanced access to healthcare, growing awareness of pediatric cancer, and rising government expenditure on medical research. Major nations such as China, India, and Japan are becoming major contributors, with growing healthcare investments and advancements in molecular diagnostics. This is likely to further drive the market growth in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players and Their Pediatric Cancer Biomarker Offerings

-

F. Hoffmann-La Roche Ltd – Cobas EGFR Mutation Test, FoundationOne Liquid

-

Abbott Laboratories – Vysis ALK Break Apart FISH Probe Kit, RealTime IDH1 Assay

-

Siemens Healthineers – ADVIA Centaur AFP Assay, IMMULITE Tumor Marker Assays

-

Thermo Fisher Scientific Inc. – Oncomine Childhood Cancer Research Assay, Ion AmpliSeq Panels

-

QIAGEN N.V. – QIAseq Targeted DNA Panels, ipsogen JAK2 RGQ PCR Kit

-

Myriad Genetics, Inc. – MyRisk Hereditary Cancer Test

-

Beckman Coulter, Inc. – Access AFP Assay, Flow Cytometry Panels

-

Bio-Rad Laboratories, Inc. – Bio-Plex Pro Cancer Biomarker Panels

-

Agilent Technologies, Inc. – SureSelect Cancer All-In-One Panels, ALK FISH Probe

-

BIOMÉRIEUX SA. – VIDAS Tumor Markers, NephroCheck Biomarker Test

-

RayBiotech, Inc. – Human Cancer Biomarker Array, ELISA Kits for Oncology

-

Randox Laboratories Ltd. – Evidence Investigator Tumor Marker Array, Biochip Technology

-

Illumina, Inc. – TruSight Oncology 500, NGS Panels for Pediatric Cancer

-

AstraZeneca PLC – Companion Diagnostics for Targeted Therapies

-

Guardant Health, Inc. – Guardant360 CDx Liquid Biopsy

-

ICON Public Limited Company – Biomarker Discovery & Validation Services

-

Merck Sharp & Dohme Corp. – Oncology Biomarker Partnerships

Recent Developments in the Pediatric Cancer Biomarker Market

-

In Feb 2025, Damon Runyon Cancer Research Foundation and St. Jude Children’s Research Hospital committed USD 1.8 million to advance childhood cancer research, supporting innovative studies focused on improving diagnostics and treatments.

-

In Jan 2025, UK HealthCare earned Pediatric Specialty Accreditation from the American College of Surgeons (ACS) Commission on Cancer (CoC), recognizing its high standards in pediatric cancer care. This accreditation highlights its excellence in treating children and adolescents with cancer.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 830.41 Million |

|

Market Size by 2032 |

USD 1635.68 Million |

|

CAGR |

CAGR of 7.84% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Indication [Leukemia, Neuroblastoma, CNS Tumors, Lymphoma, Others] |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

F. Hoffmann-La Roche Ltd, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific Inc., QIAGEN N.V., Myriad Genetics, Inc., Beckman Coulter, Inc., Bio-Rad Laboratories, Inc., Agilent Technologies, Inc., BIOMÉRIEUX SA, RayBiotech, Inc., Randox Laboratories Ltd., Illumina, Inc., AstraZeneca PLC, Guardant Health, Inc., ICON Public Limited Company, Merck Sharp & Dohme Corp. |