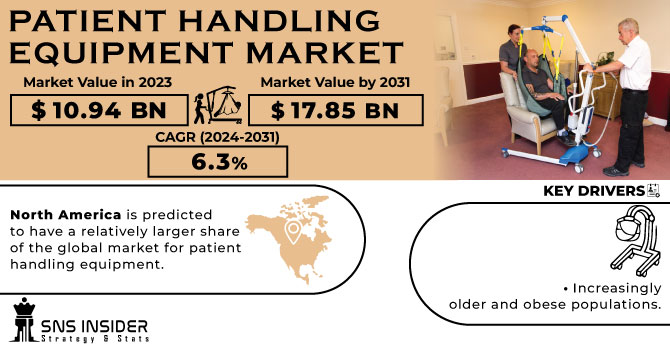

The Patient Handling Equipment Market size was estimated at USD 10.94 billion in 2023 and is expected to reach USD 17.85 billion By 2031 at a CAGR of 6.3% during the forecast period of 2024-2031.

In addition, the implementation of government laws to guarantee carers' safety during manual lifting procedures and the sharp increase in hospital admissions are anticipated to fuel the sector's growth over the projection period. For instance, the National Institute of Occupational Safety and Health has established Recommended Weight Limit recommendations for the effective treatment of patients in a medical facility and to lower the risk of practitioner injury.

Get More Information on Patient Handling Equipment Market - Request Sample Report

The demand for these medical systems is also being fueled by the regulations established by regulatory organisations like the CDC, EU-OSHA, and WSHC. Additionally, there is a growing market for gadgets for the efficient care of musculoskeletal problems, which impact more than 1.5 billion people globally. Additionally, there will be tremendous development potential due to the growing demand for and use of these systems in emerging nations. There is still a sizable untapped market in various nations, even though the forecast for the global patient handling equipment market is expanding significantly in emerging economies. The major firms are expanding into unexplored markets in the APAC area as a result of the rapid economic expansion and rising number of government initiatives.

The markets in nations like China and India have enormous growth potential because of the rapid expansion of their healthcare sectors. Additionally, the substantial populations and developing healthcare systems are luring medical device producers to locate their manufacturing facilities in these nations. Additionally, producing medical device products in poor nations tends to lower the overall cost of production, bringing down the price of the goods without sacrificing quality.

DRIVERS

Increasingly older and obese populations

Over time, there has been a steady increase in the population of those 60 and older. The elderly are more vulnerable to injuries from falls, which can result in various functional limitations and a dependency on mobility aids. The World Health Organisation (WHO) predicts that by 2030, one in six people will be 60 years of age or older. Therefore, a significant increase in the number of elderly people worldwide will increase the demand for patient management equipment.

RESTRAIN

Lack of instruction given to healthcare professionals regarding the proper use of patient handling equipment

The time that healthcare professionals spent on patient handling tasks in various healthcare facilities was considerable. Since patient handling takes up the bulk of time, it's critical to put in place efficient training programmes to raise knowledge of safe patient handling practises and reduce the possibility of accidents while handling patients. When lifting patients with particular conditions, such as those with pressure sores or burns, as well as bariatric patients, training is crucial. If carers aren't properly trained, they could transport patients more slowly.

OPPORTUNITY

Demand for home healthcare services is rising

Government rules and regulations are being put into place on a global scale to shorten and lower the cost of medical treatments. In general, giving care at the patient's home is less expensive than doing so in a facility, particularly if the informal care that is already available is effectively utilised. Furthermore, the home care market is anticipated to have considerable expansion in the next few years due to the proliferation of innovative technologies, such as remote patient monitoring. In the future, there will be a rise in the need for equipment such as mobility aids, patient transfer devices, and medical beds that is necessary for treating patients in home care settings.

CHALLENGES

Aesthetically unsound healthcare facility designs

In order to provide supportive workspaces for workers in healthcare settings and advance patients' health and well-being, the physical environment is crucial. The physical environment might limit motion and positioning, according to the American Nursing Association (ANA). Structures like ramps and lifts, patient care and procedure rooms, hallways, ramps, floor materials, door sizes and locations, and the size and condition of storage rooms are all included in the design, placement, and access of the facility. It also includes the location of the facility. Evidence-based design is a method that bases design decisions on the best information currently available from research and practise, as well as the assessment of existing structures.

Financial Uncertainty Conflict and geopolitical tension can cause economic uncertainty, which can undermine consumer and corporate confidence. Patient handling equipment purchases by healthcare organisations can become more cautious, which could stall the market or reduce demand. Budget restrictions brought on by unpredictable economic conditions may have an impact on hospitals' purchasing selections.

Export and Import Restrictions Export and import limitations may be the outcome of trade disputes and conflict. The transportation of patient handling equipment and associated parts may be affected if nations apply sanctions or embargoes. This may restrict the supply of particular goods in particular areas, sometimes leading to shortages or higher prices. World Market Attitude Geopolitical unrest may have an effect on investor confidence and the general market mood. Healthcare providers' capacity to invest in new equipment and their ability to maintain their financial stability could be impacted by stock market movements and currency depreciation.

IMPACT OF ONGOING RECESSION

Reduced Healthcare Costs Budget restrictions are a common occurrence during a recession for governments, healthcare organisations, and private citizens. Patient handling equipment investments may decline if healthcare spending is cut or shifted to vital services. Hospitals and healthcare facilities can postpone or reduce their plans to buy equipment, which would impact market demand. Healthcare facilities have the option of postponing or delaying capital expenditures, such as the acquisition of new patient handling equipment. Reduced sales for this equipment's producers and suppliers may result from this. Spending priorities for hospitals and clinics may include hiring staff, purchasing pharmaceuticals, and purchasing basic medical supplies. Economic Downturns Can Put Financial Stress on Healthcare providers. Economic downturns can put financial stress on the industry. Tighter budgets could result from declining patient volumes, difficulties with payment, and increased expenditures.

Innovation and development are impacted Budget cuts brought on by the recession may have an impact on the industry of patient handling equipment's research and development. Budgets for R&D may be cut or redirected by manufacturers, which could delay the release of novel and creative products. Supply-Chain Breakdowns Global supply chains may be disrupted by a recession, which could cause delays in the manufacture and delivery of patient handling equipment. It may be difficult for manufacturers to find raw materials and components, which will limit their ability to satisfy customer needs. Consumer Behaviour Changes During a Recession, Patients and Healthcare Professionals may Become More Price Sensitive. This could result in a rise in the demand for cost-efficient or affordable patient handling solutions, which could have an impact on the market for more expensive or high-end equipment.

By Type

Patient Transfer Devices

Patient Lifts

Ceiling lifts

Steel and wheelchair lifts

Mobile lifts

Sit-to-stand lifts

Bath and pool lifts

Slings

Air-assisted Lateral Transfer Mattresses

Reusable air assisted mattresses

Single-patient use air assisted mattresses

Sliding sheets

Accessories

Medical Beds

Medical Beds, By Type

Electric Beds

Manual Beds

Semi-electric Beds

Medical Beds, By Application

Acute Care

Long-term Care

Rehabilitation

Bariatric Care

Mobility Devices

Wheelchairs and Mobility Scooters

Powered Wheelchairs

Mobility Scooters

Manual Wheelchairs

Ambulatory Aids

Bathroom and Toilet Assist Equipment

Stretchers and Transport Chairs

By End User

Hospitals

Home-care settings

Other End Users

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

REGIONAL ANALYSES

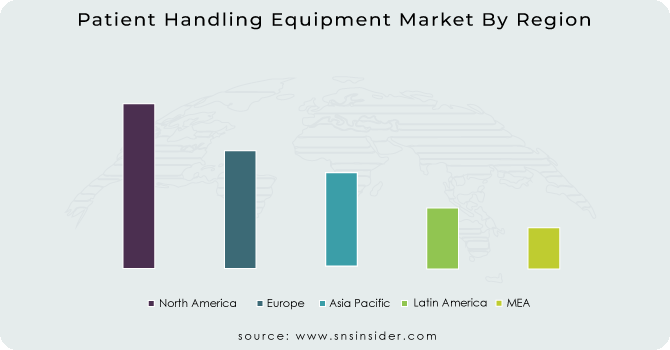

Due to its advanced healthcare infrastructure, high healthcare spending, and growing emphasis on patient injury prevention, North America is predicted to have a relatively larger share of the global market for patient handling equipment. Due to its greater patient population, expanding healthcare infrastructure, and longer hospital stays, Asia-Pacific is predicted to have a significantly higher CAGR.

In 2023, Europe had the largest market with a $5 billion valuation. This is largely attributed to the rise in activities done by both government and non-government organisations regarding the implementation of patient management apparatus in various medical facilities. Furthermore, the regional market is expanding as a result of the presence of significant and important players and their numerous strategic initiatives, including product launches, alliances, partnerships, collaborations, mergers, and acquisitions.

Do You Need any Customization Research on Patient Handling Equipment Market - Enquire Now

The major players are Invacare Corporation, Sunrise Medical (US) LLC, Permobil AB, Medline Industries Inc, Yuwell-Jiangsu Yuyue medical equipment & supply Co. Ltd., Ottobock SE & Co KGaA, Pride Mobility Products Corporation, MEYRA GmbH, Hoveround Corporation, MATSUNAGA MANUFACTORY Co. Ltd., Ki Mobility, Etac AB and others

Handicare: In Sep 2022, Handicare has a wider range of goods available, such as the 4000 curved stairlifts and the Garaventa Lift line of wheelchair platform lifts.

Birdie Evo XPLUS: In May 2022, Birdie Evo XPLUS, an avant-garde patient lift system for post-acute care facilities, was introduced by Invacare. It offers cutting-edge technology that helps maximise comfort and security whether lifting or transferring a patient to or from a bed, chair, or floor. It has a sleek and contemporary style.

Stryker: In March 2022, In order to prevent patients from slipping during tilt treatments and to protect nurses during pre- and post-surgical lateral transfers, Stryker introduced the Multi-Position MATS Mobile Air Transfer System.

| Report Attributes | Details |

| Market Size in 2023 | US$ 10.94 Bn |

| Market Size by 2031 | US$ 17.85 Bn |

| CAGR | CAGR of 6.3 % From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Patient Transfer Devices, Patient Lifts, Slings, Air-assisted Lateral Transfer Mattresses, Medical Beds, Mobility Devices, Bathroom and Toilet Assist Equipment, Stretchers and Transport Chairs) • By End User (Hospitals, Home-care settings, Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Invacare Corporation, Sunrise Medical (US) LLC, Permobil AB, Medline Industries Inc, Yuwell-Jiangsu Yuyue medical equipment & supply Co. Ltd., Ottobock SE & Co KGaA, Pride Mobility Products Corporation, MEYRA GmbH, Hoveround Corporation, MATSUNAGA MANUFACTORY Co. Ltd., Ki Mobility, Etac AB |

| Key Drivers | • Increasingly older and obese populations. |

| Market Restraints | • Lack of instruction given to healthcare professionals regarding the proper use of patient handling equipment. |

Ans: The Patient Handling Equipment Market is expected to grow at 6.3% CAGR from 2024 to 2031.

Ans: According to our analysis, the Patient Handling Equipment Market is anticipated to reach USD 17.85 Billion By 2031.

Ans: The leading participants in the, Invacare Corporation, Sunrise Medical (US) LLC, Permobil AB, Medline Industries Inc, Yuwell-Jiangsu Yuyue medical equipment & supply Co. Ltd.

Ans: The ageing and bariatric populations, expanding chronic illness prevalence, and government healthcare spending all contribute to the growth of the patient handling equipment market.

Ans: Yes, you may request customization based on your company's needs.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Russia-Ukraine War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Patient Handling Equipment Market, By Type

8.1 Patient Transfer Devices

8.2 Patient Lifts

8.3 Slings

8.4 Air-assisted Lateral Transfer Mattresses

8.5 Medical Beds

8.6 Mobility Devices

8.7 Bathroom and Toilet Assist Equipment

8.8 Stretchers and Transport Chairs

9. Patient Handling Equipment Market, By End User

9.1 Hospitals

9.2 Home-care settings

9.3 Other End Users

10. Regional Analysis

10.1 Introduction

10.2 North America

10.2.1 North America Patient Handling Equipment Market, by Country

10.2.2North America Patient Handling Equipment Market, By Type

10.2.3 North America Patient Handling Equipment Market, By End-user

10.2.4 USA

10.2.4.1 USA Patient Handling Equipment Market, By Type

10.2.4.2 USA Patient Handling Equipment Market, By End-user

10.2.5 Canada

10.2.5.1 Canada Patient Handling Equipment Market, By Type

10.2.5.2 Canada Patient Handling Equipment Market, By End-user

10.2.6 Mexico

10.2.6.1 Mexico Patient Handling Equipment Market By Type

10.2.6.2 Mexico Patient Handling Equipment Market By End-user

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Eastern Europe Patient Handling Equipment Market by Country

10.3.1.2 Eastern Europe Patient Handling Equipment Market By Type

10.3.1.3 Eastern Europe Patient Handling Equipment Market By End-user

10.3.1.4 Poland

10.3.1.4.1 Poland Patient Handling Equipment Market By Type

10.3.1.4.2 Poland Patient Handling Equipment Market By End-user

10.3.1.5 Romania

10.3.1.5.1 Romania Patient Handling Equipment Market By Type

10.3.1.5.2 Romania Patient Handling Equipment Market By End-user

10.3.1.6 Hungary

10.3.1.6.1 Hungary Patient Handling Equipment Market By Type

10.3.1.6.2 Hungary Patient Handling Equipment Market By End-user

10.3.1.7 Turkey

10.3.1.7.1 Turkey Patient Handling Equipment Market By Type

10.3.1.7.2 Turkey Patient Handling Equipment Market By End-user

10.3.1.8 Rest of Eastern Europe

10.3.1.8.1 Rest of Eastern Europe Patient Handling Equipment Market By Type

10.3.1.8.2 Rest of Eastern Europe Patient Handling Equipment Market By End-user

10.3.2 Western Europe

10.3.2.1 Western Europe Patient Handling Equipment Market by Country

10.3.2.2 Western Europe Patient Handling Equipment Market By Type

10.3.2.3 Western Europe Patient Handling Equipment Market By End-user

10.3.2.4 Germany

10.3.2.4.1 Germany Patient Handling Equipment Market By Type

10.3.2.4.2 Germany Patient Handling Equipment Market By End-user

10.3.2.5 France

10.3.2.5.1 France Patient Handling Equipment Market By Type

10.3.2.5.2 France Patient Handling Equipment Market By End-user

10.3.2.6 UK

10.3.2.6.1 UK Patient Handling Equipment Market By Type

10.3.2.6.2 UK Patient Handling Equipment Market By End-user

10.3.2.7 Italy

10.3.2.7.1 Italy Patient Handling Equipment Market By Type

10.3.2.7.2 Italy Patient Handling Equipment Market By End-user

10.3.2.8 Spain

10.3.2.8.1 Spain Patient Handling Equipment Market By Type

10.3.2.8.2 Spain Patient Handling Equipment Market By End-user

10.3.2.9 Netherlands

10.3.2.9.1 Netherlands Patient Handling Equipment Market By Type

10.3.2.9.2 Netherlands Patient Handling Equipment Market By End-user

10.3.2.10 Switzerland

10.3.2.10.1 Switzerland Patient Handling Equipment Market By Type

10.3.2.10.2 Switzerland Patient Handling Equipment Market By End-user

10.3.2.11 Austria

10.3.2.11.1 Austria Patient Handling Equipment Market By Type

10.3.2.11.2 Austria Patient Handling Equipment Market By End-user

10.3.2.12 Rest of Western Europe

10.3.2.12.1 Rest of Western Europe Patient Handling Equipment Market By Type

10.3.2.12.2 Rest of Western Europe Patient Handling Equipment Market By End-user

10.4 Asia-Pacific

10.4.1 Asia Pacific Patient Handling Equipment Market by Country

10.4.2 Asia Pacific Patient Handling Equipment Market By Type

10.4.3 Asia Pacific Patient Handling Equipment Market By End-user By Type

10.4.4 China

10.4.4.1 China Patient Handling Equipment Market By Type

10.4.4.2 China Patient Handling Equipment Market By End-user

10.4.5 India

10.4.5.1 India Patient Handling Equipment Market By Type

10.4.5.2 India Patient Handling Equipment Market By End-user

10.4.6 Japan

10.4.6.1 Japan Patient Handling Equipment Market By Type

10.4.6.2 Japan Patient Handling Equipment Market By End-user

10.4.7 South Korea

10.4.7.1 South Korea Patient Handling Equipment Market By Type

10.4.7.2 South Korea Patient Handling Equipment Market By End-user

10.4.8 Vietnam

10.4.8.1 Vietnam Patient Handling Equipment Market By Type

10.4.8.2 Vietnam Patient Handling Equipment Market By End-user

10.4.9 Singapore

10.4.9.1 Singapore Patient Handling Equipment Market By Type

10.4.9.2 Singapore Patient Handling Equipment Market By End-user

10.4.10 Australia

10.4.10.1 Australia Patient Handling Equipment Market By Type

10.4.10.2 Australia Patient Handling Equipment Market By End-user

10.4.11 Rest of Asia-Pacific

10.4.11.1 Rest of Asia-Pacific Patient Handling Equipment Market By Type

10.4.11.2 Rest of Asia-Pacific Patient Handling Equipment Market By End-user

10.5 Middle East & Africa

10.5.1 Middle East

10.5.1.1 Middle East Patient Handling Equipment Market by Country

10.5.1.2 Middle East Patient Handling Equipment Market By Type

10.5.1.3 Middle East Patient Handling Equipment Market By End-user

10.5.1.4 UAE

10.5.1.4.1 UAE Patient Handling Equipment Market By Type

10.5.1.4.2 UAE Patient Handling Equipment Market By End-user

10.5.1.5 Egypt

10.5.1.5.1 Egypt Patient Handling Equipment Market By Type

10.5.1.5.2 Egypt Patient Handling Equipment Market By End-user

10.5.1.6 Saudi Arabia

10.5.1.6.1 Saudi Arabia Patient Handling Equipment Market By Type

10.5.1.6.2 Saudi Arabia Patient Handling Equipment Market By End-user

10.5.1.7 Qatar

10.5.1.7.1 Qatar Patient Handling Equipment Market By Type

10.5.1.7.2 Qatar Patient Handling Equipment Market By End-user

10.5.1.8 Rest of Middle East

10.5.1.8.1 Rest of Middle East Patient Handling Equipment Market By Type

10.5.1.8.2 Rest of Middle East Patient Handling Equipment Market By End-user

10.5.2 Africa

10.5.2.1 Africa Patient Handling Equipment Market by Country

10.5.2.2 Africa Patient Handling Equipment Market By Type

10.5.2.3 Africa Patient Handling Equipment Market By End-user

10.5.2.4 Nigeria

10.5.2.4.1 Nigeria Patient Handling Equipment Market By Type

10.5.2.4.2 Nigeria Patient Handling Equipment Market By End-user

10.5.2.5 South Africa

10.5.2.5.1 South Africa Patient Handling Equipment Market By Type

10.5.2.5.2 South Africa Patient Handling Equipment Market By End-user

10.5.2.6 Rest of Africa

10.5.2.6.1 Rest of Africa Patient Handling Equipment Market By Type

10.5.2.6.2 Rest of Africa Patient Handling Equipment Market By End-user

10.6 Latin America

10.6.1 Latin America Patient Handling Equipment Market by Country

10.6.2 Latin America Patient Handling Equipment Market By Type

10.6.3 Latin America Patient Handling Equipment Market By End-user

10.6.4 Brazil

10.6.4.1 Brazil Patient Handling Equipment Market By Type

10.6.4.2 Brazil Patient Handling Equipment Market By End-user

10.6.5 Argentina

10.6.5.1 Argentina Patient Handling Equipment Market By Type

10.6.5.2 Argentina Patient Handling Equipment Market By End-user

10.6.6 Colombia

10.6.6.1 Colombia Patient Handling Equipment Market By Type

10.6.6.2 Colombia Patient Handling Equipment Market By End-user

10.6.7 Rest of Latin America

10.6.7.1 Rest of Latin America Patient Handling Equipment Market By Type

10.6.7.2 Rest of Latin America Patient Handling Equipment Market By End-user

11. Company Profile

11.1 Invacare Corporation.

11.1.1 Company Overview

11.1.2 Financials

11.1.3 Type/Services Offered

11.1.4 SWOT Analysis

11.1.5 The SNS View

11.2 Sunrise Medical (US) LLC.

11.2.1 Company Overview

11.2.2 Financials

11.2.3 Type/Services Offered

11.2.4 SWOT Analysis

11.2.5 The SNS View

11.3 Permobil AB.

11.3.1 Company Overview

11.3.2 Financials

11.3.3 Type/Services Offered

11.3.4 SWOT Analysis

11.3.5 The SNS View

11.4 Medline Industries Inc.

11.4 Company Overview

11.4.2 Financials

11.4.3 Type/Services Offered

11.4.4 SWOT Analysis

11.4.5 The SNS View

11.5 Yuwell-Jiangsu.

11.5.1 Company Overview

11.5.2 Financials

11.5.3 Type/Services Offered

11.5.4 SWOT Analysis

11.5.5 The SNS View

11.6 Ottobock SE & Co KGaA.

11.6.1 Company Overview

11.6.2 Financials

11.6.3 Type/Services Offered

11.6.4 SWOT Analysis

11.6.5 The SNS View

11.7 Pride Mobility Types Corporation

11.7.1 Company Overview

11.7.2 Financials

11.7.3 Type/Services Offered

11.7.4 SWOT Analysis

11.7.5 The SNS View

11.8 MEYRA GmbH.

11.8.1 Company Overview

11.8.2 Financials

11.8.3 Type/Services Offered

11.8.4 SWOT Analysis

11.8.5 The SNS View

11.9 Hoveround Corporation

11.9.1 Company Overview

11.9.2 Financials

11.9.3 Type/ Services Offered

11.9.4 SWOT Analysis

11.9.5 The SNS View

11.10 Yuyue medical equipment & supply Co. Ltd

11.10.1 Company Overview

11.10.2 Financials

11.10.3 Type/Services Offered

11.10.4 SWOT Analysis

11.10.5 The SNS View

12. Competitive Landscape

12.1 Competitive Benchmarking

12.2 Market Share Analysis

12.3 Recent Developments

12.3.1 Industry News

12.3.2 Company News

12.3.3 Mergers & Acquisitions

13. USE Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Cell Freezing Media Market was valued at $ 152.14 billion in 2023 and is expected to reach $ 333.29 billion by 2032, growing at a CAGR of 9.15% from 2024-2032.

The Compression Therapy Market size was valued at USD 4.06 Billion in 2023 & is estimated to reach USD 7.86 Billion by 2032 with a growing CAGR of 7.63% over the forecast period of 2024-2032.

The Global Vitamin D Testing Market valued at USD 919.38 million in 2023, is projected to reach USD 1,887.61 million by 2032, growing at a CAGR of 8.34% over the forecast period 2024-2032.

The Magnetic Resonance Imaging (MRI) Market size was valued at USD 5.92 billion in 2023 and is expected to reach USD 9.8 billion by 2032, and grow at a CAGR of 5.78%.

The Inflation Devices Market was USD 577.91 million in 2023 and is expected to reach USD 937.09 million by 2032, growing at a CAGR of 5.01% by 2024-2032.

The Multi-Cancer Early Detection Market was valued at USD 1.07 billion in 2023 and is expected to reach USD 4.40 billion by 2032, growing at a CAGR of 17.04% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd