Pacemakers Market Overview:

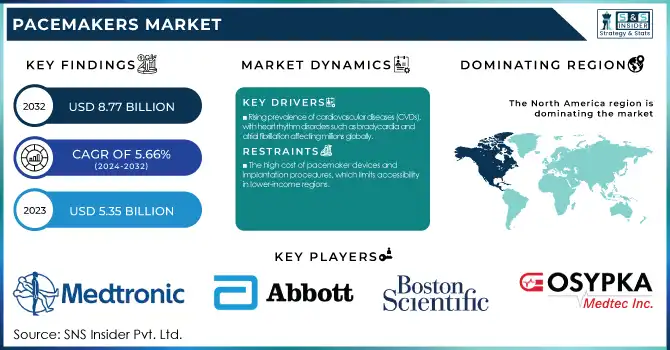

The Pacemakers Market size was valued at USD 5.35 Billion in 2023 and is projected to reach USD 8.77 Billion by 2032, growing at a CAGR of 5.66% from 2024 to 2032.

This Report identifies the growing incidence and prevalence of cardiovascular diseases, creating demand for pacemaker implantation in different regions. The research investigates technology development and innovation trends such as the creation of leadless pacemakers and AI-powered monitoring solutions, which are enhancing patient outcomes. Furthermore, it investigates healthcare expenditure on pacemakers, comparing government, commercial, private, and out-of-pocket spending across the major regions. The study also highlights remote monitoring and digital health technology adoption, which are improving patient management and post-implant care. In addition, it explores patient demographics and acceptance patterns, demonstrating how lifestyle, age, and awareness levels drive pacemaker adoption and market growth.

To Get more information on Pacemakers Market - Request Free Sample Report

Pacemakers Market Dynamics

Drivers

-

Rising prevalence of cardiovascular diseases (CVDs), with heart rhythm disorders such as bradycardia and atrial fibrillation affecting millions globally.

As per the World Health Organization (WHO), CVDs cause almost 32% of all deaths worldwide every year, generating demand for pacemakers. Advances in technology, including MRI-compatible and leadless pacemakers, have improved patient outcomes, increasing the appeal of these devices. The growing geriatric population, which is more prone to heart-related conditions, also fuels market growth. Second, the increasing number of remote patient monitoring systems that are being accepted in pacemakers enables the monitoring of the heart's status in real-time, lowering the number of visits to hospitals as well as making patients more convenient. Favorable reimbursement policies from developed nations further promote the increasing use of pacemakers as they become affordable. The availability of minimally invasive procedures further increased the installation of pacemakers, which patients prefer over faster recovery as well as safer surgery. In addition, growing investments in healthcare infrastructure and R&D activities by leading medical device companies have resulted in the launch of new pacemaker models with longer battery life and sophisticated sensing features. All these factors combined are responsible for the consistent growth of the pacemaker market.

Restraints

-

The high cost of pacemaker devices and implantation procedures, which limits accessibility in lower-income regions.

Conventional pacemakers may range from USD 2,500 to USD 10,000, apart from surgical and post-operative costs, rendering them inaccessible to the majority of patients. Where reimbursement policies are scarce in a nation, patient cost further hinders adoption. Battery life and replacement needs are another issue, with most pacemakers requiring replacement every 5-15 years, which entails further surgery and related risks. Additionally, regulatory barriers and strict approval procedures slow down the introduction of new pacemaker technologies. Medical device companies have to face long clinical trials and approvals from regulatory agencies like the U.S. FDA and the European Medicines Agency, which slows down the market penetration. Furthermore, risks involved in pacemaker implantation like infections, lead displacement, and malfunctions of the device discourage some patients and doctors from availing the procedure. The lack of qualified cardiac surgeons and other specialized medical practitioners in developing countries also restricts the mass acceptance of pacemakers, thereby inhibiting market growth in some areas.

Opportunities

-

The pacemaker market presents several opportunities, primarily driven by technological advancements and the growing adoption of leadless pacemakers.

Leadless pacemakers like Medtronic's Micra have transformed cardiology by eradicating the conventional leads, lowering complications, and providing minimal invasiveness during implantation. The growth of artificial intelligence and machine learning in cardiac monitoring is another potential growth area as intelligent pacemakers with embedded AI can decode heart rhythm patterns and forecast arrhythmias to enhance patient care. Further growth comes from enhancing healthcare access in developing economies. Governments of nations like India and Brazil are making additional investments in cardiac care facilities, facilitating increased adoption of pacemakers. The increased trend of remote monitoring and pacemaker integration with telemedicine enables real-time data transmission to healthcare providers, which decreases hospital visits and enhances long-term patient care. In addition, biodegradable pacemakers in development provide promising avenues, which can possibly prevent surgical removal. The rising number of partnerships and collaborations among medical device firms and healthcare facilities is also propelling innovation, resulting in new product releases and increased market penetration. All these factors cumulatively present lucrative opportunities for market growth and technological advancements in the pacemaker market.

Challenges

-

Cybersecurity risks in connected pacemakers, as an increasing number of devices are equipped with remote monitoring features.

Wireless communication vulnerabilities can leave pacemakers open to hacking, raising serious patient safety issues. Furthermore, restricted awareness and availability in rural and underdeveloped regions limit the large-scale implementation. Most patients in low-income areas go undiagnosed or untreated as a result of poor medical infrastructure and the absence of trained healthcare providers. A further significant problem is the technology constraint of batteries since even the latest pacemakers need replacement after a few years, and multiple surgeries with increasing costs across the lifetime of the patient. Post-implantation adverse events like fractures in the leads, infection in the device, and inappropriate pacing are additional hazards associated with pacemakers and sometimes require removal or revision of the device. Also, regulatory approval delays hinder innovation, with firms having to adhere to rigorous clinical testing and safety assessments prior to marketing new models. Ethical issues related to pacemaker implantation among terminally ill patients are also a challenge for healthcare professionals and caregivers. Mitigating these challenges involves ongoing investment in R&D, enhanced regulatory mechanisms, and expanded patient education programs to facilitate increased adoption and more secure use of pacemakers globally.

Pacemakers Market Segmentation Analysis

By Product

The implantable pacemakers market captured the largest market share of 65.0% in 2023, led mostly by its superiority in the control of chronic cardiac conditions and patient demand for minimal invasion solutions. While external pacemakers have a temporary function used in an acute environment, implantable pacemakers bring long-term solutions to the benefit of healthcare practitioners and patients. Advancements in technology, including leadless pacemakers, extended battery life, and MRI-compatible pacemakers, have further bolstered their market share. Also, the aging population, which is more prone to heart rhythm disorders, has driven the implantable pacemaker demand. The favorable reimbursement policy, rising healthcare expenditure, and the growing incidence of bradycardia and arrhythmias have also supported this segment's leadership.

The implantable pacemakers segment is also growing at the fastest rate, due to ongoing innovation and a growing patient base. With increased awareness of sophisticated pacemaker technologies, patients and medical professionals alike are increasingly turning towards implantable devices compared to external ones. Further, rising regulatory approvals for advanced pacemakers with remote monitoring features are accelerating their uptake. The movement towards minimally invasive procedures, combined with enhanced healthcare facilities in the developing markets, is poised to drive the growth of implantable pacemakers in the forthcoming years.

By Application

The bradycardia segment held the highest market share of 24.5% during 2023, reinforcing its position as the leading application of pacemakers. Bradycardia, or an abnormally low heart rate, is among the most prevalent conditions necessitating pacemaker implantation. The prevalence of bradycardia, especially in old people and individuals with inherent cardiovascular ailments, has been the cause behind the leadership of the segment. As pacemakers are the first line of treatment to control heart rhythm in bradycardia patients, their demand is always high in this segment. Moreover, improvements in diagnostic technology have increased early detection and treatment, thus fueling pacemaker adoption. The availability of established healthcare infrastructure in developed countries and reimbursement support has also contributed to the dominance of the bradycardia segment in the pacemaker market.

The arrhythmias segment is also expected to grow at the fastest rate, as the incidence of atrial fibrillation and other cardiac rhythm disorders increases. Improved diagnostics, higher awareness, and increased use of remote monitoring systems for arrhythmia management are some of the primary drivers contributing to this growth. Furthermore, continuous research and development in pacemaker technology, especially in the area of increasing adaptability for treating arrhythmias, will help fuel the growth of this segment in the coming years.

By End Use

Hospital segment led the pacemaker market in 2023 with a revenue share of 68.6%. Hospitals are still the most desirable environment for pacemaker implantation procedures because they can command access to sophisticated medical infrastructure, well-trained healthcare personnel, and emergency response mechanisms. Support for handling complicated cases and immediate post-procedure care further solidifies the hospital segment lead. Additionally, the majority of healthcare systems and insurance companies give precedence to hospital-based care for pacemaker implantation, which results in greater reimbursement than other healthcare facilities. The growth in cardiovascular surgeries and the growing population of elderly people, who generally need hospital-based treatment, have also driven the dominance of this segment. With development of technology in hospital units and more numbers of specialized cardiac hospitals, the hospitals are likely to continue their dominance in pacemaker markets.

Outpatient facilities sector will develop at the highest rate on account of the trend towards minimally invasive procedures and same-day discharge. Outpatient centers provide cost savings compared to in-hospital stays, which is an attractive prospect for both patients and healthcare providers. The increasing trend towards ambulatory surgical centers and specialty clinics, along with improved pacemaker implantation procedures that minimize recovery time, is likely to fuel the fast growth of outpatient facilities in the coming years.

Pacemakers Market Regional Insights

North America dominated the pacemakers market globally in 2023 with a major market share of 38.4%. The reason behind this domination is largely the high rate of cardiovascular diseases, a strong well-established healthcare network, and dominant pacemaker players like Medtronic, Abbott, and Boston Scientific. The increasing population of elderly people, who are more prone to bradycardia and arrhythmias, has increased demand for pacemakers further in North America. Moreover, favorable government policies and schemes for reimbursement and premium care for the heart have played a significant role in the widespread use of pacemaker devices. The area is also favored by early take-up of technological advancements in the form of MRI-compatible and leadless pacemakers, among others, and high research and development efforts in cardiac rhythm management.

The Asia-Pacific region is expected to be the fastest-growing segment during the forecast period in the pacemaker market. The growth is fueled by investments in healthcare, growing awareness about cardiovascular diseases, and enhanced access to sophisticated medical care. Markets like China, India, and Japan are experiencing a pacemaker adoption boom driven by the increasing geriatric population, the development of healthcare infrastructure, and government initiatives aimed at enhancing cardiac care services. Furthermore, an increase in lifestyle diseases, including hypertension and diabetes, is also anticipated to spur pacemaker demand in the Asia-Pacific region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Pacemakers Market

-

Medtronic – Micra, Azure, Advisa MRI SureScan

-

Abbott – Assurity MRI, Endurity, Accent MRI

-

Boston Scientific – ACCOLADE, ESSENTIO, ALTRUA

-

BIOTRONIK – Edora, Evity, Enitra

-

MicroPort Scientific Corporation – Rega, Kora 100

-

MEDICO S.R.L. – Symphony, Melody

-

Shree Pacetronix Ltd. – Single Chamber, Dual Chamber

-

OSYPKA MEDICAL – OSYPKA Pacemaker Systems

-

OSCOR Inc – Oscor External Pacemakers

-

Lepu Medical Technology – Ankang Series

Recent Developments

-

In Dec 2024, Boston Scientific faced an FDA safety communication regarding Accolade pacemakers due to a manufacturing issue with the battery cathode, which could cause devices to enter safety mode permanently. Initially, the company recalled a subset of affected devices, but the FDA worked with Boston Scientific to assess whether all Accolade pacemakers carried this risk, potentially requiring early replacements.

-

In Nov 2024, Abbott launched the AVEIR VR leadless pacemaker in India for patients with slow heart rhythms. The device has received approval from both the Central Drugs Standard Control Organisation (CDSCO) and the US FDA, marking a significant advancement in cardiac care.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 5.35 billion |

| Market Size by 2032 | USD 8.77 billion |

| CAGR | CAGR of 5.66% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [External pacemakers (Single Chamber, Dual Chamber), Implantable pacemakers (Conventional {Single Chamber, Dual Chamber, Biventricular Chamber} Leadless {Single Chamber, Dual Chamber})] • By Application [Bradycardia, Acute Myocardial Infarction, Arrhythmias (Atrial Fibrillation, Heart Block, Long QT Syndrome), Non-Congestive Heart Failure, Others] • By End Use [Hospitals, Outpatient Facilities] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic, Abbott, Boston Scientific, BIOTRONIK, MicroPort Scientific Corporation, MEDICO S.R.L., Shree Pacetronix Ltd., OSYPKA MEDICAL, OSCOR Inc, Lepu Medical Technology. |

Frequently Asked Questions

Ans: North America dominated the Pacemakers market.

Ans: The high cost of pacemaker devices and implantation procedures, which limits accessibility in lower-income regions.

Ans: Rising prevalence of cardiovascular diseases (CVDs), with heart rhythm disorders such as bradycardia and atrial fibrillation affecting millions globally.

Ans: The market is expected to reach USD 8.77 billion by 2032, increasing from USD 5.35 billion in 2023.

Ans: The Pacemakers market is anticipated to grow at a CAGR of 5.66% from 2024 to 2032.

Get in touch