Get more information on Osteoporosis Treatment Market - Request Free Sample Report

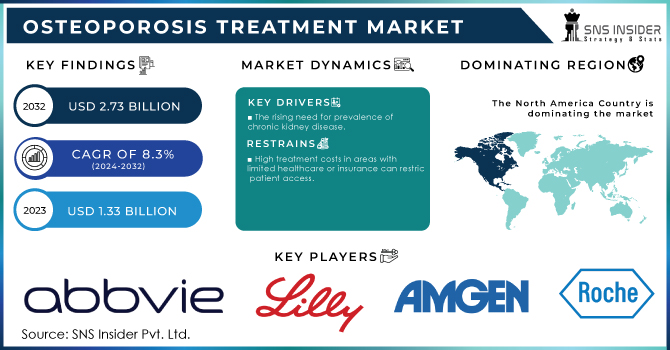

The Osteoporosis Treatment Market Size was valued at USD 13.28 billion in 2023, and is expected to reach USD 19.39 billion by 2032, and grow at a CAGR of 4.3% over the forecast period 2024-2032.

In recent times, there has been a rise in demand for osteoporosis therapy due to the widespread occurrence of the disease across the globe. Osteoporosis is a bone ailment that weakens the bones, causing low bone mass and deterioration of bone tissue structure, which makes bones fragile and increases the risk of fractures. The therapy options for osteoporosis include bisphosphonates, selective oestrogen receptor modulators (SERMs), monoclonal antibodies, and other medications.

The osteoporosis treatment market is expanding with the introduction of new treatments like low-intensity pulsed ultrasound (LIPUS) devices and bone growth stimulation technologies, in addition to traditional medications. LIPUS devices use sound waves to enhance bone density and structure, while bone growth stimulation technologies employ electrical and magnetic stimulation to promote bone development and repair. With increasing awareness, rapid economic development, and a growing elderly population, the osteoporosis treatment market is anticipated to experience growth in regions like Asia-Pacific.

DRIVERS

Population Ageing Raising Awareness Technological Progress Changes in lifestyle.

The worldwide ageing population is a major driving force in the osteoporosis treatment industry. Osteoporosis is increasingly common in older people, and as the elderly population grows, so does the demand for effective therapies. Growing public awareness of osteoporosis and its effects has resulted in increased rates of early diagnosis and treatment, fueling demand for osteoporosis drugs and treatments. Medical research and technological advancements have led to the creation of new and more effective osteoporosis treatment alternatives, thereby growing the market.

RESTRAIN

High treatment costs Adverse effects.

Patent Expirations.

OPPORTUNITY

Novel Therapy Development Emerging Markets

There is a constant focus on research and development to identify better, more effective, and safer osteoporosis medicines, which presents potential for pharmaceutical firms to bring revolutionary medications to market. The expanding healthcare infrastructure and increased awareness in emerging countries present potential for enterprises to extend their presence and fulfil the unmet requirements of osteoporosis patients in these locations.

CHALLENGES

Ensuring Adherence and Compliance, Addressing Gaps in Diagnosis and Awareness, and Overcoming Reimbursement Issues.

The uncertainties of war and economic instability can cause fluctuations in currency rates and inflation, which could result in the increased pricing of osteoporosis drugs. This may make it challenging for patients to afford their prescribed medications, resulting in noncompliance with treatment recommendations.

Furthermore, the conflict may put a strain on the healthcare infrastructure of both countries. Hospitals and clinics may face difficulties in providing adequate treatment for osteoporosis patients if resources are diverted to manage war-related injuries and crises. Additionally, prolonged hostilities in both nations may lead to disruptions in research and development operations, diverting funds and focus away from novel osteoporosis treatments and hindering progress.

IMPACT OF ONGOING RECESSION

During a recession, drug development may be delayed or reduced due to financial challenges faced by pharmaceutical companies. This can lead to a decline in the discovery and release of new osteoporosis medications. Additionally, smaller pharmaceutical companies may struggle to compete and may consolidate, resulting in fewer competitors in the osteoporosis therapy industry. Customers may also become more cost-conscious, putting pressure on pharmaceutical companies to lower the prices of osteoporosis drugs. This could potentially impact their profit margins and the availability of certain medications.

By Drug Class

Calcitonin

Bisphosphonate

Zoledronic Acid

Ibandronate

Alendronate

Risedronate

Other

RANK ligand (RANKL) Inhibitor

Parathyroid Hormone-Related Protein (PTHrP) Analog

Selective Estrogen Receptor Modulator (SERMs)

By Administration

Injectables

Oral

Others

By Distribution Channel

Online Pharmacies

Retail Pharmacies & Stores

Hospitals Pharmacies

REGIONAL ANALYSES

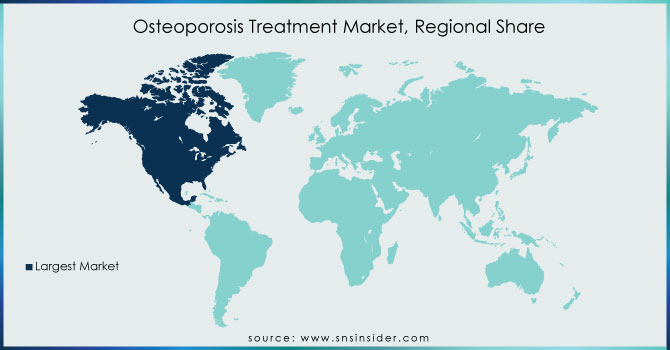

The North American market for osteoporosis medications holds the largest portion of revenue. This is because the region's elderly population is growing, obesity rates are increasing, there are more lifestyle-related disorders, and there are more cases of osteoporosis. Additionally, the United States experiences over 1.5 million osteoporotic fractures annually. Furthermore, with increased awareness of osteoporosis treatment, changing lifestyles, and high healthcare spending, the use of osteoporosis medications is on the rise in North America.

The market for osteoporosis treatment in Europe is expanding due to factors such as the growing elderly population, changing lifestyles, rapid urbanisation, and increased awareness. Europe accounts for over one-third of all osteoporotic fractures globally, which amounts to more than 9 million per year. Each year, osteoporotic fractures in Europe cause nearly 3 million disability-adjusted life years (DALYs), which is higher than hypertension or rheumatoid arthritis. The number of osteoporotic fractures is increasing in several European countries, partly due to longer lifespans. Although the overall population in the region is not expected to significantly increase in the next 25 years, the elderly population will increase by over 40%, particularly for women and more than 50% of males.

Need any customization research on Osteoporosis Treatment Market - Enquiry Now

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are AbbVie Inc., Eli Lilly and Company, Amgen Inc., F. Hoffmann-La Roche Ltd, Novartis AG, Sanofi, Pfizer Inc., Merck & Co., Inc., GlaxoSmithKline plc and others.

Enzene Biosciences Ltd: In August 2021, the medication Controller General of India (DCGI) granted Enzene Biosciences Ltd Marketing Authorization (MA) for their biosimilar medication, denosumab, which is recommended for the treatment of osteoporosis in adults.

Theramex: In January 2021, Theramex, a pharmaceutical firm based in London, has released the osteoporosis medication Livogiva in Europe.

| Report Attributes | Details |

| Market Size in 2023 | US$ 13.28 Bn |

| Market Size by 2032 | US$ 19.39 Bn |

| CAGR | CAGR of 4.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Class (Calcitonin, Bisphosphonate, Hormone Replacement Therapy, RANK ligand (RANKL) Inhibitor, Parathyroid Hormone-Related Protein (PTHrP) Analog, Selective Estrogen Receptor Modulator (SERMs)) • By Administration (Injectables, Oral, Others) • By Distribution Channel (Online Pharmacies, Retail Pharmacies & Stores, Hospitals Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | AbbVie Inc., Eli Lilly and Company, Amgen Inc., F. Hoffmann-La Roche Ltd, Novartis AG, Sanofi, Pfizer Inc., Merck & Co., Inc., GlaxoSmithKline plc |

| Key Drivers | • Population Ageing Raising Awareness Technological Progress Changes in lifestyle. |

| Market Restraints | • High treatment costs Adverse effects. • Patent Expirations. |

Ans: The Osteoporosis Treatment Market is expected to grow at 4.3% from 2024 to 2032.

Ans: The Osteoporosis Treatment Market is anticipated to reach USD 19.39 billion by 2032.

Ans: The market for osteoporosis therapy medications is expected to grow due to the rising incidence of this condition, as well as an increase in the number of innovative treatments being approved and released.

Ans: The leading participants in the Osteoporosis Treatment Market are AbbVie Inc., Eli Lilly and Company, Amgen Inc., F. Hoffmann-La Roche Ltd, Novartis AG, Sanofi, Pfizer Inc.

Ans: Yes, you may request customization based on your company's needs.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Ukraine- Russia War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Osteoporosis Treatment Market, By Drug Class

8.1 Calcitonin

8.2 Bisphosphonate

8.2.1 Zoledronic Acid

8.2.2 Ibandronate

8.2.3 Alendronate

8.2.4 Risedronate

8.2.5 Other

8.3 Hormone Replacement Therapy

8.4 RANK ligand Inhibitor

8.5 Parathyroid Hormone-Related Protein (PTHrP) Analog

8.6 Selective Estrogen Receptor Modulator (SERMs)

9. Osteoporosis Treatment Market, By Administration

9.1 Injectables

9.2 Oral

9.3 Others

10. Osteoporosis Treatment Market, By Distribution Channel

10.1 Online Pharmacies

10.2 Retail Pharmacies & Stores

10.3 Hospitals Pharmacies

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Osteoporosis Treatment Market by country

11.2.2North America Osteoporosis Treatment Market by Drug Class

11.2.3 North America Osteoporosis Treatment Market by Administration

11.2.4 North America Osteoporosis Treatment Market by Distribution Channel

11.2.5 USA

11.2.5.1 USA Osteoporosis Treatment Market by Drug Class

11.2.5.2 USA Osteoporosis Treatment Market by Administration

11.2.5.3 USA Osteoporosis Treatment Market by Distribution Channel

11.2.6 Canada

11.2.6.1 Canada Osteoporosis Treatment Market by Drug Class

11.2.6.2 Canada Osteoporosis Treatment Market by Administration

11.2.6.3 Canada Osteoporosis Treatment Market by Distribution Channel

11.2.7 Mexico

11.2.7.1 Mexico Osteoporosis Treatment Market by Drug Class

11.2.7.2 Mexico Osteoporosis Treatment Market by Administration

11.2.7.3 Mexico Osteoporosis Treatment Market by Distribution Channel

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Eastern Europe Osteoporosis Treatment Market by country

11.3.1.2 Eastern Europe Osteoporosis Treatment Market by Drug Class

11.3.1.3 Eastern Europe Osteoporosis Treatment Market by Administration

11.3.1.4 Eastern Europe Osteoporosis Treatment Market by Distribution Channel

11.3.1.5 Poland

11.3.1.5.1 Poland Osteoporosis Treatment Market by Drug Class

11.3.1.5.2 Poland Osteoporosis Treatment Market by Administration

11.3.1.5.3 Poland Osteoporosis Treatment Market by Distribution Channel

11.3.1.6 Romania

11.3.1.6.1 Romania Osteoporosis Treatment Market by Drug Class

11.3.1.6.2 Romania Osteoporosis Treatment Market by Administration

11.3.1.6.4 Romania Osteoporosis Treatment Market by Distribution Channel

11.3.1.7 Turkey

11.3.1.7.1 Turkey Osteoporosis Treatment Market by Drug Class

11.3.1.7.2 Turkey Osteoporosis Treatment Market by Administration

11.3.1.7.3 Turkey Osteoporosis Treatment Market by Distribution Channel

11.3.1.8 Rest of Eastern Europe

11.3.1.8.1 Rest of Eastern Europe Osteoporosis Treatment Market by Drug Class

11.3.1.8.2 Rest of Eastern Europe Osteoporosis Treatment Market by Administration

11.3.1.8.3 Rest of Eastern Europe Osteoporosis Treatment Market by Distribution Channel

11.3.2 Western Europe

11.3.2.1 Western Europe Osteoporosis Treatment Market by Drug Class

11.3.2.2 Western Europe Osteoporosis Treatment Market by Administration

11.3.2.3 Western Europe Osteoporosis Treatment Market by Distribution Channel

11.3.2.4 Germany

11.3.2.4.1 Germany Osteoporosis Treatment Market by Drug Class

11.3.2.4.2 Germany Osteoporosis Treatment Market by Administration

11.3.2.4.3 Germany Osteoporosis Treatment Market by Distribution Channel

11.3.2.5 France

11.3.2.5.1 France Osteoporosis Treatment Market by Drug Class

11.3.2.5.2 France Osteoporosis Treatment Market by Administration

11.3.2.5.3 France Osteoporosis Treatment Market by Distribution Channel

11.3.2.6 UK

11.3.2.6.1 UK Osteoporosis Treatment Market by Drug Class

11.3.2.6.2 UK Osteoporosis Treatment Market by Administration

11.3.2.6.3 UK Osteoporosis Treatment Market by Distribution Channel

11.3.2.7 Italy

11.3.2.7.1 Italy Osteoporosis Treatment Market by Drug Class

11.3.2.7.2 Italy Osteoporosis Treatment Market by Administration

11.3.2.7.3 Italy Osteoporosis Treatment Market by Distribution Channel

11.3.2.8 Spain

11.3.2.8.1 Spain Osteoporosis Treatment Market by Drug Class

11.3.2.8.2 Spain Osteoporosis Treatment Market by Administration

11.3.2.8.3 Spain Osteoporosis Treatment Market by Distribution Channel

11.3.2.9 Netherlands

11.3.2.9.1 Netherlands Osteoporosis Treatment Market by Drug Class

11.3.2.9.2 Netherlands Osteoporosis Treatment Market by Administration

11.3.2.9.3 Netherlands Osteoporosis Treatment Market by Distribution Channel

11.3.2.10 Switzerland

11.3.2.10.1 Switzerland Osteoporosis Treatment Market by Drug Class

11.3.2.10.2 Switzerland Osteoporosis Treatment Market by Administration

11.3.2.10.3 Switzerland Osteoporosis Treatment Market by Distribution Channel

11.3.2.11.1 Austria

11.3.2.11.2 Austria Osteoporosis Treatment Market by Drug Class

11.3.2.11.3 Austria Osteoporosis Treatment Market by Administration

11.3.2.11.4 Austria Osteoporosis Treatment Market by Distribution Channel

11.3.2.12 Rest of Western Europe

11.3.2.12.1 Rest of Western Europe Osteoporosis Treatment Market by Drug Class

11.3.2.12.2 Rest of Western Europe Osteoporosis Treatment Market by Administration

11.3.2.12.3 Rest of Western Europe Osteoporosis Treatment Market by Distribution Channel

11.4 Asia-Pacific

11.4.1 Asia-Pacific Osteoporosis Treatment Market by country

11.4.2 Asia-Pacific Osteoporosis Treatment Market by Drug Class

11.4.3 Asia-Pacific Osteoporosis Treatment Market by Administration

11.4.4 Asia-Pacific Osteoporosis Treatment Market by Distribution Channel

11.4.5 China

11.4.5.1 China Osteoporosis Treatment Market by Drug Class

11.4.5.2 China Osteoporosis Treatment Market by Administration

11.4.5.3 China Osteoporosis Treatment Market Distribution Channel

11.4.6 India

11.4.6.1 India Osteoporosis Treatment Market by Drug Class

11.4.6.2 India Osteoporosis Treatment Market by Administration

11.4.6.3 India Osteoporosis Treatment Market by Distribution Channel

11.4.7 Japan

11.4.7.1 Japan Osteoporosis Treatment Market by Drug Class

11.4.7.2 Japan Osteoporosis Treatment Market by Administration

11.4.7.3 Japan Osteoporosis Treatment Market by Distribution Channel

11.4.8 South Korea

11.4.8.1 South Korea Osteoporosis Treatment Market by Drug Class

11.4.8.2 South Korea Osteoporosis Treatment Market by Administration

11.4.8.3 South Korea Osteoporosis Treatment Market by Distribution Channel

11.4.9 Vietnam

11.4.9.1 Vietnam Osteoporosis Treatment Market by Drug Class

11.4.9.2 Vietnam Osteoporosis Treatment Market by Administration

11.4.9.3 Vietnam Osteoporosis Treatment Market by Distribution Channel

11.4.10 Singapore

11.4.10.1 Singapore Osteoporosis Treatment Market by Drug Class

11.4.10.2 Singapore Osteoporosis Treatment Market by Administration

11.4.10.3 Singapore Osteoporosis Treatment Market by Distribution Channel

11.4.11 Australia

11.4.11.1 Australia Osteoporosis Treatment Market by Drug Class

11.4.11.2 Australia Osteoporosis Treatment Market by Administration

11.4.11.3 Australia Osteoporosis Treatment Market by Distribution Channel

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Osteoporosis Treatment Market by Drug Class

11.4.12.2 Rest of Asia-Pacific Osteoporosis Treatment Market by Administration

11.4.12.3 Rest of Asia-Pacific Osteoporosis Treatment Market by Distribution Channel

11.5 Middle East & Africa

11.5.1 Middle East

11.5.1.1 Middle East Osteoporosis Treatment Market by country

11.5.1.2 Middle East Osteoporosis Treatment Market by Drug Class

11.5.1.3 Middle East Osteoporosis Treatment Market by Administration

11.5.1.4 Middle East Osteoporosis Treatment Market by Distribution Channel

11.5.1.5 UAE

11.5.1.5.1 UAE Osteoporosis Treatment Market by Drug Class

11.5.1.5.2 UAE Osteoporosis Treatment Market by Administration

11.5.1.5.3 UAE Osteoporosis Treatment Market by Distribution Channel

11.5.1.6 Egypt

11.5.1.6.1 Egypt Osteoporosis Treatment Market by Drug Class

11.5.1.6.2 Egypt Osteoporosis Treatment Market by Administration

11.5.1.6.3 Egypt Osteoporosis Treatment Market by Distribution Channel

11.5.1.7 Saudi Arabia

11.5.1.7.1 Saudi Arabia Osteoporosis Treatment Market by Drug Class

11.5.1.7.2 Saudi Arabia Osteoporosis Treatment Market by Administration

11.5.1.7.3 Saudi Arabia Osteoporosis Treatment Market by Distribution Channel

11.5.1.8 Qatar

11.5.1.8.1 Qatar Osteoporosis Treatment Market by Drug Class

11.5.1.8.2 Qatar Osteoporosis Treatment Market by Administration

11.5.1.8.3 Qatar Osteoporosis Treatment Market by Distribution Channel

11.5.1.9 Rest of Middle East

11.5.1.9.1 Rest of Middle East Osteoporosis Treatment Market by Drug Class

11.5.1.9.2 Rest of Middle East Osteoporosis Treatment Market by Administration

11.5.1.9.3 Rest of Middle East Osteoporosis Treatment Market by Distribution Channel

11.5.2 Africa

11.5.2.1 Africa Osteoporosis Treatment Market by country

11.5.2.2 Africa Osteoporosis Treatment Market by Drug Class

11.5.2.3 Africa Osteoporosis Treatment Market by Administration

11.5.2.4 Africa Osteoporosis Treatment Market by Distribution Channel

11.5.2.5 Nigeria

11.5.2.5.1 Nigeria Osteoporosis Treatment Market by Drug Class

11.5.2.5.2 Nigeria Osteoporosis Treatment Market by Administration

11.5.2.5.3 Nigeria Osteoporosis Treatment Market by Distribution Channel

11.5.2.6 South Africa

11.5.2.6.1 South Africa Osteoporosis Treatment Market by Drug Class

11.5.2.6.2 South Africa Osteoporosis Treatment Market by Administration

11.5.2.6.3 South Africa Osteoporosis Treatment Market by Distribution Channel

11.5.2.7 Rest of Africa

11.5.2.7.1 Rest of Africa Osteoporosis Treatment Market by Drug Class

11.5.2.7.2 Rest of Africa Osteoporosis Treatment Market by Administration

11.5.2.7.3 Rest of Africa Osteoporosis Treatment Market by Distribution Channel

11.6 Latin America

11.6.1 Latin America Osteoporosis Treatment Market by country

11.6.2 Latin America Osteoporosis Treatment Market by Drug Class

11.6.3 Latin America Osteoporosis Treatment Market by Administration

11.6.4 Latin America Osteoporosis Treatment Market by Distribution Channel

11.6.5 Brazil

11.6.5.1 Brazil America Wheelchair by Drug Class

11.6.5.2 Brazil America Wheelchair by Administration

11.6.5.3 Brazil America Wheelchair by Distribution Channel

11.6.6 Argentina

11.6.6.1 Argentina America Wheelchair by Drug Class

11.6.6.2 Argentina America Wheelchair by Administration

11.6.6.3 Argentina America Wheelchair by Distribution Channel

11.6.7 Colombia

11.6.7.1 Colombia America Wheelchair by Drug Class

11.6.7.2 Colombia America Wheelchair by Administration

11.6.7.3 Colombia America Wheelchair by Distribution Channel

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Wheelchair by Drug Class

11.6.8.2 Rest of Latin America Wheelchair by Administration

11.6.8.3 Rest of Latin America Wheelchair by Distribution Channel

12 Company profile

12.1 AbbVie Inc.

12.1.1 Company Overview

12.1.2 Financials

12.1.3 Drug Class/Services/Offerings

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Eli Lilly and Company.

12.2.1 Company Overview

12.2.2 Financials

12.2.3 Drug Class/Services/Offerings

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 Amgen Inc.

12.3.1 Company Overview

12.3.2 Financials

12.3.3 Drug Class/Services/Offerings

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 F. Hoffmann-La Roche Ltd.

12.4.1 Company Overview

12.4.2 Financials

12.4.3 Drug Class/Services/Offerings

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Novartis AG.

12.5.1 Company Overview

12.5.2 Financials

12.5.3 Drug Class/Services/Offerings

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Sanofi.

12.6.1 Company Overview

12.6.2 Financials

12.6.3 Drug Class/Services/Offerings

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 Pfizer Inc.

12.7.1 Company Overview

12.7.2 Financials

12.7.3 Drug Class/Services/Offerings

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 Merck & Co., Inc.

12.8.2 Financials

12.8.3 Drug Class/Services/Offerings

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Novartis AG.

12.9.1 Company Overview

12.9.2 Financials

12.9.3 Drug Class/Services/Offerings

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Pfizer Inc.

12.10.1 Company Overview

12.10.2 Financials

12.10.3 Drug Class/Services/Offerings

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Bench marking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The CyberKnife Market was valued at USD 542.14 million in 2023 and is expected to reach USD 2340.47 million by 2032, growing at a CAGR of 17.67% over the forecast period of 2024-2032.

The Protein Labeling Market size was estimated at USD 2.39 billion in 2023 and is expected to reach USD 4.83 billion by 2032 at a CAGR of 8.14% during the forecast period of 2024-2032.

The IoT Medical Devices Market Size was valued at USD 41.4 billion in 2023 and is expected to reach USD 503.6 billion by 2032 and grow at a CAGR of 32.0% over the forecast period 2024-2032.

Cell Lysis and Disruption Market was valued at USD 5.21 billion in 2023 and is expected to reach USD 10.92 billion by 2032, growing at a CAGR of 8.61% from 2024-2032.

Pet Grooming Services Market Size was valued at USD 6.33 Billion in 2023 and is expected to reach USD 12.05 Billion by 2032, growing at a CAGR of 7.42% over the forecast period 2024-2032.

The Antibody Drug Conjugates [ADC] Market was valued at USD 10.28 billion in 2023 and is expected to reach USD 29.10 billion by 2032, growing at a CAGR of 12.29% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd