Get more information on Operating Room Management Market - Request Sample Report

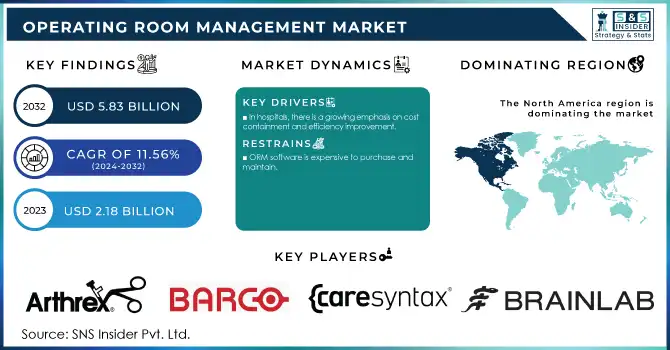

The Operating Room Management Market Size was valued at USD 2.18 billion in 2023, and is expected to reach USD 5.83 billion by 2032 and grow at a CAGR of 11.56% over the forecast period 2024-2032.

Operating room administration entails the use of software-based solutions to ensure that operating rooms run smoothly and efficiently. Multiple problems have become more prevalent as the world's senior population has grown. To combat this, operating rooms around the world are focusing on increasing cost-effectiveness and efficiency. The concentrate on the overall working room the board market gives a thorough investigation of the business. The exploration incorporates an intensive assessment of key market sections, patterns, drivers, limitations, cutthroat scene, and other significant factors.

The science of operating room administration focuses on the efficient management of operating room suites. Operating Rooms (ORs) are a critical hub in a hospital, and their resources must be managed effectively to maintain high-performance output and patient safety.

DRIVERS

In hospitals, there is a growing emphasis on cost containment and efficiency improvement.

EHRs and other HCIT solutions are becoming increasingly popular.

Supportive government policies and initiatives in the healthcare field

Projects for redevelopment and investment to promote OR infrastructure

RESTRAINTS

ORM software is expensive to purchase and maintain.

Issues concerning interoperability

OPPORTUNITIES

Emerging markets and growing medical tourism

Technological advances in hospitals

CHALLENGES

Incorporated operating rooms have a scarcity of experienced surgeons.

Healthcare providers are being merged.

IMPACT OF COVID-19

The COVID-19 pandemic has unleashed ruin on many individuals' lives and organizations for a monstrous scope. However, if there is one area that has benefited from this catastrophe, it is the healthcare IT sector. While many businesses are struggling to stay afloat, those who have chosen operating room management solutions are doing just well. The pandemic has resulted in a temporary restriction on elective surgeries all over the world, resulting in elective surgery cancellations all over the world. According to a paper issued by CovidSurg Collaborative experts, roughly 28 million procedures were cancelled around the world during the COVID-19 pandemic's peak interruption period of 12 weeks.

Hospitals are extending OR hours and concentrating on greater OR utilisation to deal with the rising surgery loads. The ORM programming business sector will profit from the COVID-19. It will boost ORM software usage because most hospitals would now focus on improving capacity by leveraging technology to boost efficiency.

By Component Type

Software and services make up the operating room management market. The software category is likely to dominate the market. Moreover, during the projection period, this category is expected to increase at the highest CAGR. The expanding installation of ORM software is responsible for the big share and rapid expansion.

By Solutions Type

Data and communication management solutions, anesthesia management systems, workplace management solutions, operating room planning solutions, performance management solutions, and other solutions are all part of the solution phase. Because of the advantages such as easy sharing of patient status in patient care sections, schedule compliance, and sharing of media and information related to cases within separate operating rooms or outpatient departments, data management and communication solutions account for the largest component of the operating room management market.

By Delivery Mode

On-premise solutions, cloud-based solutions, and web-based solutions are the three categories in which the market is divided. During the projection period, the market for cloud-based solutions is predicted to grow at the fastest rate. This segment's rapid expansion is due to benefits such as scalable data storage, scalable processing power, machine-learning capabilities, and speedier data movement between cloud platforms' enterprises.

By End User

Hospitals and surgical centers are two types of services on the market. Due to the growing need for effective disease management, the increasing number of surgical procedures in hospitals, and the growing number of hospitals established in developing countries, hospitals are a major part of the global market for operating room operating systems.

KEY MARKET SEGMENTATION:

By Component Type

Software

Services

By Solutions Type

Data management and communication solutions

Anesthesia information management systems

Operating room supply management solutions

Operating room scheduling solutions

Performance management solutions

By Delivery Mode

On-premise solutions

Cloud-based solutions

By End User

Hospitals

Ambulatory surgery centers

Because of the speedier adoption of new technologies, the presence of well-developed hospital infrastructure in the United States and Canada, the highest number of multi-specialty hospitals, and other factors, North America, led by the United States, commands the largest market share. Europe is the second largest market, with Germany, France, and the United Kingdom leading the way.

Japan, China, and India are expected to expand at the quickest CAGR in the Asia Pacific area. Due to weak social and economic conditions, particularly in Africa, the Middle East and African region is predicted to grow at a slow pace. The Gulf economy, on the other hand, are predicted to grow rapidly due to the region's faster expansion of healthcare and the creation of big hospital complexes like the King Fahd hospitals in Riyadh.

Need any customization research on Operating Room Management Market - Enquiry Now

REGIONAL COVERAGE:

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

south Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

KEY PLAYERS:

Some of the major key players of Operating Room Management Market are as follows: Arthrex, Inc., Barco, Care Syntax, Braiblab AG, Dragerwerk AG & Co. KGaA, Getinge AB, Olympus, Stryker, KARL STORZ SE & CO. KG, Steris and Other Players.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 2.18 Billion |

| Market Size by 2032 | USD 5.83 Billion |

| CAGR | CAGR of 11.56% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type (Software, Services) • By Solutions Type (Data management and communication solutions, Anesthesia information management systems, Operating room supply management solutions, Operating room scheduling solutions, Performance management solutions) • By Delivery Mode (On-premise solutions, Cloud-based solutions) • By End User (Hospitals, Ambulatory surgery centers) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Arthrex, Inc., Barco, Care Syntax, Braiblab AG, Dragerwerk AG & Co. KGaA, Getinge AB, Olympus, Stryker, KARL STORZ SE & CO. KG, and Steris. |

| Drivers | • In hospitals, there is a growing emphasis on cost containment and efficiency improvement. • EHRs and other HCIT solutions are becoming increasingly popular. • Supportive government policies and initiatives in the healthcare field • Projects for redevelopment and investment to promote OR infrastructure |

| Restraints | • ORM software is expensive to purchase and maintain. • Issues concerning interoperability |

Ans: The Operating Room Management Market size is expected to reach USD 5.83 Bn by 2032.

Ans: The Operating Room Management Market is to grow at a CAGR of 11.56% over the forecast period 2024-2032.

The by Delivery Mode is divided into two sub segments is On-premise solutions, Cloud-based solution.

The challenges faced by Particle Counter market is Incorporated operating rooms have a scarcity of experienced surgeons.

Top-down, bottom-up, Quantitative, Qualitative Research, Descriptive, Analytical, Applied, Fundamental Research.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 COVID-19 Impact Analysis

4.2 Impact of Ukraine- Russia war

4.3 Impact of ongoing Recession

4.3.1 Introduction

4.3.2 Impact on major economies

4.3.2.1 US

4.3.2.2 Canada

4.3.2.3 Germany

4.3.2.4 France

4.3.2.5 United Kingdom

4.3.2.6 China

4.3.2.7 Japan

4.3.2.8 South Korea

4.3.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Operating Room Management Market Segmentation, By Component Type

8.1 Software

8.2 Services

9. Operating Room Management Market Segmentation, By Solutions Type

9.1 Data management and communication solutions

9.2 Anesthesia information management systems

9.3 Operating room supply management solutions

9.4 Operating room scheduling solutions

9.5 Performance management solutions

10. Operating Room Management Market Segmentation, By Delivery Mode

10.1 On-premise solutions

10.2 Cloud-based solutions

11. Operating Room Management Market Segmentation, By End User

11.1 Hospitals

11.2 Ambulatory surgery centers

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 USA

12.2.2 Canada

12.2.3 Mexico

12.3 Europe

12.3.1 Germany

12.3.2 UK

12.3.3 France

12.3.4 Italy

12.3.5 Spain

12.3.6 The Netherlands

12.3.7 Rest of Europe

12.4 Asia-Pacific

12.4.1 Japan

12.4.2 South Korea

12.4.3 China

12.4.4 India

12.4.5 Australia

12.4.6 Rest of Asia-Pacific

12.5 The Middle East & Africa

12.5.1 Israel

12.5.2 UAE

12.5.3 South Africa

12.5.4 Rest

12.6 Latin America

12.6.1 Brazil

12.6.2 Argentina

12.6.3 Rest of Latin America

13. Company Profiles

13.1 Arthrex, Inc.

13.1.1 Financial

13.1.2 Products/ Services Offered

13.1.3 SWOT Analysis

13.1.4 The SNS view

13.2 Barco

13.3 Care Syntax

13.4 Braiblab AG

13.5 Dragerwerk AG & Co. KGaA

13.6 Getinge AB

13.7 Olympus

13.8 Stryker

13.9 KARL STORZ SE & CO. KG

13.10 Steris.

14. Competitive Landscape

14.1 Competitive Benchmark

14.2 Market Share Analysis

14.3 Recent Developments

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Immunomodulators Market size was USD 224.17 Billion in 2023 and is expected to Reach USD 391.78 Billion by 2032 and grow at a CAGR of 6.4% over the forecast period of 2024-2032.

The Cardiovascular Devices Market size was estimated at USD 51.97 billion in 2023 and is expected to reach USD 97.16 billion by 2032 at a CAGR of 7.2% during the forecast period of 2024-2032.

The Medical Supply Delivery Service Market was valued at USD 65.67 billion in 2023 and is expected to reach USD 126.92 billion by 2032, growing at a CAGR of 7.57% from 2024-2032.

The Feminine Hygiene Products Market Size was valued at USD 27.05 billion in 2023 and will reach USD 47.98 billion by 2032 and with CAGR of 6.60% by 2032

The Process Analytical Technology Market Size was valued at USD 3.50 Billion in 2023, and is expected to reach USD 10.19 Billion by 2032, and grow at a CAGR of 13.29%.

The ATP Assays Market Size was valued at USD 299.64 Million in 2023 and is expected to reach USD 564.76 Million by 2032, growing at a CAGR of 7.30% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd