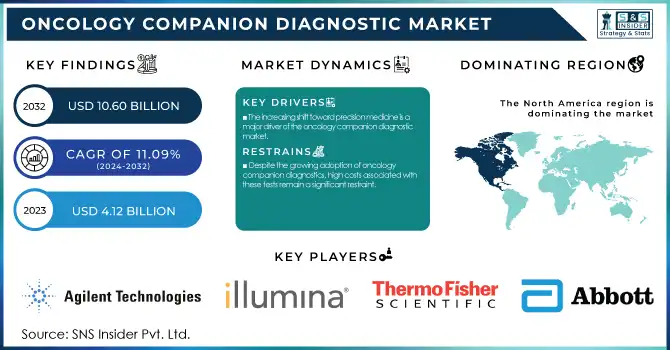

The Oncology Companion Diagnostic Market was Valued at USD 4.12 billion in 2023 and is projected to grow to USD 10.60 billion by 2032 with a CAGR of 11.09% during the forecast period of 2024-2032.

To get more information on Oncology Companion Diagnostic Market - Request Free Sample Report

This report points to the increasing incidence and prevalence of cancer by type and region, fueling the increasing use of companion diagnostics for tailored treatment strategies. The research analyzes healthcare expenditure on oncology diagnostics by different funding streams, such as government, commercial, private, and out-of-pocket spending, with a focus on regional differences in investment. In addition, it examines biomarker-specific test adoption and market trends, gauging how progress in point-of-care and laboratory testing is refining early detection and treatment accuracy. The report also examines the strategic partnerships and collaborations among diagnostic firms, pharmaceutical companies, and research organizations that are driving innovation in companion diagnostics. Furthermore, it analyzes emerging technologies in the market, highlighting their potential to transform cancer diagnostics and improve patient outcomes.

Drivers

The increasing shift toward precision medicine is a major driver of the oncology companion diagnostic market.

Companion diagnostics are instrumental in detecting biomarkers that assist in the personalization of treatment protocols, such that patients can receive the best-targeted treatments. With an increasing incidence of cancers, especially in lung, breast, and colon cancers, demand for tests like PD-L1, HER2, EGFR, and BRCA is rising. Companion diagnostic approvals along with targeted therapies have also boosted the market. For example, the FDA-cleared Guardant360 CDx liquid biopsy test assists in identifying mutations in non-small cell lung cancer (NSCLC) for treatment guidance with targeted inhibitors. Moreover, advancements in genomic technologies like Next-Generation Sequencing (NGS) and polymerase chain reaction (PCR) have enhanced the accuracy of tests, thus companion diagnostics have become more reliable and available. The increasing partnerships among pharmaceutical and diagnostic firms to co-develop companion diagnostics, e.g., the collaboration between Genentech and Roche for the VENTANA PD-L1 (SP142) Assay, continue to drive market growth. As more focus is placed on cancer treatments tailored to individual patients and more regulatory endorsement is given to precision medicine, the need for oncology companion diagnostics will grow further.

Restraints

Despite the growing adoption of oncology companion diagnostics, high costs associated with these tests remain a significant restraint.

More complex diagnostic tests, including Next-Generation Sequencing (NGS)-based companion diagnostics, may be costly, ranging from USD 2,000–to USD 5,000 per test, and thus remain inaccessible to a majority of patients, especially from low-income geographies. The cost issue is also aggravated by restrictive reimbursement policies in various nations. Most insurance companies cover full-fledged comprehensive genomic profiling (CGP) tests only partially, and since patients are required to pay cash in such cases, it limits market penetration. In the United States, while some FDA-approved companion diagnostics are reimbursed by Medicare, coverage differs depending on the type of cancer and the specificity of biomarkers. Regulatory complexity and rigorous approval mechanisms also slow new test market entry. For instance, the FDA demands rigorous clinical validation before companion diagnostic approvals, which further increases development expenses and duration. Small diagnostic firms face costly regulatory approvals, stifling market competition. The absence of standardization in companion diagnostic testing between laboratories and across regions also impacts test adoption. These economic and regulatory limitations remain challenging, especially in developing regions where healthcare budgets are limited.

Opportunities

The emergence of liquid biopsy-based companion diagnostics presents a major opportunity for the oncology companion diagnostic market.

In contrast to conventional tissue biopsies, liquid biopsies provide real-time and non-invasive monitoring of tumors, enhancing patient outcomes. Such tests as Guardant360 CDx and FoundationOne Liquid CDx are receiving regulatory clearances, enabling oncologists to identify mutations and direct targeted therapies without invasive procedures. Furthermore, Next-Generation Sequencing-based companion diagnostics are transforming cancer treatment by facilitating comprehensive genomic profiling of tumors, detecting multiple actionable mutations at once. The increasing use of multi-gene panel tests, including Illumina's TruSight Oncology 500, is fueling market growth. The growing incorporation of artificial intelligence and bioinformatics in genomic analysis further increases the precision and efficiency of companion diagnostics, thus making them more viable for clinical application. Partnerships between pharmaceutical and diagnostic firms for the co-development of companion diagnostics for immunotherapies and targeted therapies are also generating profitable growth opportunities. As more regulatory bodies continue to favor precision medicine programs and genomic research funding increases, demand for high-end companion diagnostic solutions will expand, providing new market opportunities.

Challenges

Navigating the complex regulatory landscape for test approval and commercialization.

Regulatory authorities such as the FDA and EMA necessitate extensive clinical proof to affirm the safety and effectiveness of companion diagnostics before approval for use in the clinic. It is time- and money-intensive and frequently slows entry to the market for novel tests. The FDA, for instance, demands co-development with individually targeted treatments such that any alteration in biomarker testing would involve re-approval. Also, the absence of worldwide standardization in biomarker testing and interpretation is a challenge. Differences in testing methods among laboratories may cause inconsistencies in results, impacting treatment. Most areas do not have clearly defined guidelines for NGS-based and liquid biopsy-based companion diagnostics, making regulatory compliance challenging for diagnostic manufacturers. In addition, physician awareness and adoption continue to be an issue, as oncologists need to be educated to read and apply companion diagnostic results. These regulatory and standardization barriers must be overcome for oncology companion diagnostics to be adopted and integrated into standard clinical practice.

By Product & Services

The Product segment led the oncology companion diagnostics market in 2023, holding a market share of 67.3%. Its leadership can be credited to the rising use of test kits, assay kits, and reagents based on biomarkers due to their necessary role in oncology precision medicine. They perform a significant role in deciding upon targeted treatments with the identification of genetic mutations and optimal choice selection for treatments for better outcomes. The increasing requirement for companion diagnostic assays, particularly those co-developed with targeted therapies, has also contributed to growth in the market. Moreover, technological progress in diagnostics, including high-throughput sequencing and automation, has improved test accuracy and efficiency, thus stimulating product uptake in healthcare institutions. Conversely, the services segment is likely to grow at the highest rate due to the rising demand for laboratory-developed tests (LDTs) and outsourced diagnostic services. With an increasing number of healthcare professionals looking for economical and specialty testing options, diagnostic service providers are extending their capacity to satisfy the demand.

By Technology

The Polymerase Chain Reaction (PCR) segment dominated the oncology companion diagnostic market in 2023 with a 23.3% market share. PCR is still a prevalent technology because it is highly sensitive, specific, and cost-effective in identifying genetic mutations of targeted therapies. It is extensively applied in clinical diagnostics for its capacity to amplify minute DNA or RNA samples, and hence it is a critical tool in the identification of cancer biomarkers such as EGFR, KRAS, and BRAF. The cost-effectiveness and short turnaround time of PCR-based companion diagnostics have been responsible for their extensive use in both laboratory and hospital environments. Yet, Next-Generation Sequencing (NGS) is expected to be the technology with the highest growth rate, as it facilitates whole-genome profiling through the simultaneous analysis of multiple genes. The growth in the use of NGS in oncology is fueled by the demand for personalized treatment approaches, particularly in complicated cancers that need multi-gene analysis. With declining costs and increased efficiency due to advances in sequencing technology, the adoption of NGS is likely to grow exponentially.

By Disease Type

Non-Small Cell Lung Cancer (NSCLC) held the largest portion of the oncology companion diagnostic market in 2023, with a 31.3% market share of the overall market. This can be attributed to the high incidence of NSCLC globally and the growing use of companion diagnostics to direct targeted therapy. EGFR, ALK, ROS1, and PD-L1 biomarkers are important in personalizing patient treatment options, and therefore companion diagnostics are imperative for making treatment choices. Regulatory approvals of targeted therapies like EGFR inhibitors and PD-L1 checkpoint inhibitors have also increased the demand for companion diagnostics in NSCLC. Breast cancer, on the other hand, is anticipated to be the most rapidly growing segment, driven by the growing adoption of HER2, BRCA, and multi-gene panel testing. The growing incidence of breast cancer, combined with advances in genetic screening for hereditary risk, has also increased demand for companion diagnostics. Moreover, increasing clinical guidelines suggesting precision medicine strategies are further fueling growth in this segment.

By End-Use

The hospital segment held the largest share in the oncology companion diagnostic market in 2023 with a 52.8% share. Hospitals remain the primary setting for cancer diagnosis and treatment because of the sophisticated laboratory setup, incorporation of oncology divisions, and availability of full-fledged testing centers. The fact that hospitals house multidisciplinary cancer care teams and specialized molecular diagnostic labs assures hassle-free adoption of companion diagnostic tests for tailored therapy. Moreover, reimbursement and government funding policies supporting hospital-based testing have also supported their market leadership. Nevertheless, the pathology/diagnostic laboratory segment is anticipated to witness the most rapid growth, owing to the growing need for high-throughput molecular diagnostic testing. Independent laboratories are more and more providing NGS-based and PCR-based oncology companion diagnostic services, decreasing the pressure on hospital facilities and allowing for quicker turnaround times. The increasing trend towards outsourcing advanced diagnostic testing to pathology laboratories is driving this segment's growth, particularly in geographies with insufficient hospital-based molecular testing infrastructure.

North America was dominant in the oncology companion diagnostic market in 2023, due to established healthcare systems, high levels of adoption of advanced diagnostics, and favorable reimbursement policies. Having major industry players, coupled with robust regulatory backing from bodies such as the FDA, has further driven market expansion. The rise in cancer incidence and the need for personalized treatment have also created widespread adoption of companion diagnostics across the region.

Europe accounted for a significant share of the market, fueled by government support of precision medicine, growth in molecular diagnostics, and a growing number of regulatory approvals for companion diagnostics. Germany, the UK, and France lead the region thanks to their developed healthcare infrastructure and high investment in cancer research.

Asia-Pacific (APAC) will witness the most rapid growth, driven by increased cancer incidence, growing healthcare access, and rising awareness of personalized medicine. Leaders among these countries include China, Japan, and India, which are experiencing investment growth in genomic research, advancing regulatory environments, and partnerships between drug companies and diagnostic players.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players and Their Oncology Companion Diagnostic Products:

Agilent Technologies, Inc.: Dako HER2 IQFISH pharmDx

Illumina, Inc.: TruSight Oncology 500

QIAGEN: therascreen EGFR RGQ PCR Kit

Thermo Fisher Scientific Inc.: Oncomine Dx Target Test

Foundation Medicine, Inc.: FoundationOne CDx

Myriad Genetics, Inc.: BRACAnalysis CDx

F. Hoffmann-La Roche Ltd.: VENTANA PD-L1 (SP142) Assay

BioMérieux: THxID-BRAF Kit

Abbott: PathVysion HER-2 DNA Probe Kit

Leica Biosystems: BOND Oracle HER2 IHC System

Guardant Health, Inc.: Guardant360 CDx

EntroGen, Inc.: EGFR Mutation Analysis Kit

Abbott Laboratories: Vysis ALK Break Apart FISH Probe Kit

Bio-Rad Laboratories: QXDx BCR-ABL %IS Kit

Biocartis: Idylla NRAS-BRAF Mutation Test

Exact Sciences: Oncotype DX

Genedrive: MT-RNR1 ID Kit

Genomic Health: Oncotype DX

Invivoscribe: LeukoStrat CDx FLT3 Mutation Assay

Sysmex Corporation: OncoBEAM RAS CRC Kit

Recent Developments

In Jan 2025, Roche received FDA approval for a label expansion of its PATHWAY anti-HER2/neu (4B5) Rabbit Monoclonal Primary Antibody, making it the first companion diagnostic to identify HER2-ultralow metastatic breast cancer patients eligible for ENHERTU treatment. ENHERTU, a HER2-directed antibody-drug conjugate (ADC), is jointly developed and commercialized by Daiichi Sankyo and AstraZeneca, marking a significant advancement in personalized cancer therapy.

In Dec 2024, Guardant Health, Inc. announced a collaboration with Boehringer Ingelheim to advance the regulatory approval and commercialization of the Guardant360 CDx liquid biopsy as a companion diagnostic for zongertinib, an investigational HER2-selective tyrosine kinase inhibitor (TKI) for non-small cell lung cancer (NSCLC). This partnership aims to enhance precision oncology by enabling targeted treatment selection for patients with specific HER2 mutations.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 4.12 billion |

| Market Size by 2032 | USD 10.60 billion |

| CAGR | CAGR of 11.09% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Services [Product (Instrument, Consumables, Software), Services] • By Technology [Polymerase Chain Reaction (PCR), Next-generation Sequencing (NGS), Immunohistochemistry (IHC), In Situ Hybridization (ISH)/Fluorescence In Situ Hybridization (FISH), Other Technologies] • By Disease Type [Breast Cancer, Non-small Cell Lung Cancer, Colorectal Cancer, Leukemia, Melanoma, Prostate Cancer, Others] • By End-Use [Hospital, Pathology/Diagnostic Laboratory, Academic Medical Center] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Agilent Technologies, Inc., Illumina, Inc., QIAGEN, Thermo Fisher Scientific Inc., Foundation Medicine, Inc., Myriad Genetics, Inc., F. Hoffmann-La Roche Ltd., BioMérieux, Abbott, Leica Biosystems, Guardant Health, Inc., EntroGen, Inc., Abbott Laboratories, Bio-Rad Laboratories, Biocartis, Exact Sciences, Genedrive, Genomic Health, Invivoscribe, Sysmex Corporation. |

Ans: The Oncology Companion Diagnostic market is projected to grow at a CAGR of 11.09% during the forecast period.

Ans: By 2032, the Oncology Companion Diagnostic market is expected to reach USD 10.60 Billion, up from USD 4.12 Billion in 2023.

Ans: The increasing shift toward precision medicine is a major driver of the oncology companion diagnostic market.

Ans: Despite the growing adoption of oncology companion diagnostics, high costs associated with these tests remain a significant restraint.

Ans: North America is the dominant region in the Oncology Companion Diagnostic market.

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence of Cancer (2023), by Type and Region

5.2 Adoption of Oncology Companion Diagnostics (2023), by Region and Cancer Type

5.3 Healthcare Spending on Oncology Companion Diagnostics, by Region (Government, Commercial, Private, Out-of-Pocket), 2023

5.4 Biomarker-Specific Market Trends and Test Adoption (2023)

5.5 Laboratory and Point-of-Care Testing Trends (2023-2032)

5.6 Partnership and Collaborations in Companion Diagnostics (2023)

5.7 Market Trends in Emerging Technologies for Companion Diagnostics (2023-2032)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and Promotional Activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Oncology Companion Diagnostic Market Segmentation, by Product & Services

7.1 Chapter Overview

7.2 Product

7.2.1 Product Market Trends Analysis (2020-2032)

7.2.2 Product Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Instrument

7.2.3.1 Instrument Market Trends Analysis (2020-2032)

7.2.3.2 Instrument Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.4 Consumables

7.2.4.1 Consumables Market Trends Analysis (2020-2032)

7.2.4.2 Consumables Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.5 Software

7.2.5.1 Software Market Trends Analysis (2020-2032)

7.2.5.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Services

7.3.1 Services Market Trends Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Oncology Companion Diagnostic Market Segmentation, By Technology

8.1 Chapter Overview

8.2 Polymerase Chain Reaction (PCR)

8.2.1 Polymerase Chain Reaction (PCR) Market Trends Analysis (2020-2032)

8.2.2 Polymerase Chain Reaction (PCR) Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Next-generation Sequencing (NGS)

8.3.1 Next-generation Sequencing (NGS) Market Trends Analysis (2020-2032)

8.3.2 Next-generation Sequencing (NGS) Market Size Estimates And Forecasts To 2032 (USD Billion)

8.4 Immunohistochemistry (IHC)

8.4.1 Immunohistochemistry (IHC) Market Trends Analysis (2020-2032)

8.4.2 Immunohistochemistry (IHC) Market Size Estimates And Forecasts To 2032 (USD Billion)

8.5 In Situ Hybridization (ISH)/Fluorescence In Situ Hybridization (FISH)

8.5.1 In Situ Hybridization (ISH)/Fluorescence In Situ Hybridization (FISH) Market Trends Analysis (2020-2032)

8.5.2 In Situ Hybridization (ISH)/Fluorescence In Situ Hybridization (FISH) Market Size Estimates And Forecasts To 2032 (USD Billion)

8.6 Other Technologies

8.6.1 Other Technologies Market Trends Analysis (2020-2032)

8.6.2 Other Technologies Market Size Estimates And Forecasts To 2032 (USD Billion)

9. Oncology Companion Diagnostic Market Segmentation, by Disease Type

9.1 Chapter Overview

9.2 Breast Cancer

9.2.1 Breast Cancer Market Trends Analysis (2020-2032)

9.2.2 Breast Cancer Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Non-small Cell Lung Cancer

9.3.1 Non-small Cell Lung Cancer Market Trends Analysis (2020-2032)

9.3.2 Non-small Cell Lung Cancer Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Colorectal Cancer

9.4.1 Colorectal Cancer Market Trends Analysis (2020-2032)

9.4.2 Colorectal Cancer Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Leukemia

9.5.1 Leukemia Market Trends Analysis (2020-2032)

9.5.2 Leukemia Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Melanoma

9.6.1 Melanoma Market Trends Analysis (2020-2032)

9.6.2 Melanoma Market Size Estimates and Forecasts to 2032 (USD Billion)

9.7 Prostate Cancer

9.7.1 Prostate Cancer Market Trends Analysis (2020-2032)

9.7.2 Prostate Cancer Market Size Estimates and Forecasts to 2032 (USD Billion)

9.8 Others

9.8.1 Others Market Trends Analysis (2020-2032)

9.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Oncology Companion Diagnostic Market Segmentation, By End Use

10.1 Chapter Overview

10.2 Hospital

10.2.1 Hospital Market Trends Analysis (2020-2032)

10.2.2 Hospital Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Pathology/Diagnostic Laboratory

10.3.1 Pathology/Diagnostic Laboratory Market Trends Analysis (2020-2032)

10.3.2 Pathology/Diagnostic Laboratory Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Academic Medical Center

10.4.1 Academic Medical Center Market Trends Analysis (2020-2032)

10.4.2 Academic Medical Center Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.2.4 North America Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.2.5 North America Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.2.6 North America Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.2.7.2 USA Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.2.7.3 USA Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.2.7.4 USA Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.2.8.2 Canada Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.2.8.3 Canada Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.2.8.4 Canada Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.2.9.2 Mexico Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.2.9.3 Mexico Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.2.9.4 Mexico Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.7.2 Poland Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.7.3 Poland Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.7.4 Poland Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.8.2 Romania Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.8.3 Romania Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.8.4 Romania Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.4 Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By Disease Type (2020-2032) (USD Billion)

11.3.2.5 Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Delivery Mode (2020-2032) (USD Billion)

11.3.2.6 Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.7.2 Germany Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.7.3 Germany Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.7.4 Germany Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.8.2 France Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.8.3 France Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.8.4 France Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.9.2 UK Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.9.3 UK Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.9.4 UK Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.10.2 Italy Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.10.3 Italy Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.10.4 Italy Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.11.2 Spain Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.11.3 Spain Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.11.4 Spain Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.14.2 Austria Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.14.3 Austria Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.14.4 Austria Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.4 Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.5 Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.6 Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.7.2 China Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.7.3 China Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.7.4 China Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.8.2 India Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.8.3 India Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.8.4 India Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.9.2 Japan Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.9.3 Japan Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.9.4 Japan Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.10.2 South Korea Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.10.3 South Korea Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.10.4 South Korea Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.11.2 Vietnam Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.11.3 Vietnam Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.11.4 Vietnam Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.12.2 Singapore Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.12.3 Singapore Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.12.4 Singapore Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.13.2 Australia Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.13.3 Australia Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.13.4 Australia Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.4 Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.5 Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.6 Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.7.2 UAE Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.7.3 UAE Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.7.4 UAE Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.2.4 Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.2.5 Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.2.6 Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.6.4 Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.6.5 Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.6.6 Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.6.7.2 Brazil Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.6.7.3 Brazil Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.6.7.4 Brazil Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.6.8.2 Argentina Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.6.8.3 Argentina Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.6.8.4 Argentina Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.6.9.2 Colombia Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.6.9.3 Colombia Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.6.9.4 Colombia Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, By Technology (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, by Disease Type (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Oncology Companion Diagnostic Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

12. Company Profiles

12.1 Agilent Technologies, Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Product / Services Offered

12.1.4 SWOT Analysis

12.2 Illumina, Inc.

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Product / Services Offered

12.2.4 SWOT Analysis

12.3 QIAGEN

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Product / Services Offered

12.3.4 SWOT Analysis

12.4 Thermo Fisher Scientific Inc.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Product / Services Offered

12.4.4 SWOT Analysis

12.5 Foundation Medicine, Inc.

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Product / Services Offered

12.5.4 SWOT Analysis

12.6 Myriad Genetics, Inc.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Product / Services Offered

12.6.4 SWOT Analysis

12.7 F. Hoffmann-La Roche Ltd.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Product / Services Offered

12.7.4 SWOT Analysis

12.8 BioMérieux

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Product / Services Offered

12.8.4 SWOT Analysis

12.9 Leica Biosystems

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Product / Services Offered

12.9.4 SWOT Analysis

12.10 Abbott

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Product / Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product & Services

Product

Instrument

Consumables

Software

Services

By Technology

Polymerase Chain Reaction (PCR)

Next-generation Sequencing (NGS)

Immunohistochemistry (IHC)

In Situ Hybridization (ISH)/Fluorescence In Situ Hybridization (FISH)

Other Technologies

By Disease Type

Breast Cancer

Non-small Cell Lung Cancer

Colorectal Cancer

Leukemia

Melanoma

Prostate Cancer

Others

By End-Use

Hospital

Pathology/Diagnostic Laboratory

Academic Medical Center

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Antibody Drug Conjugates [ADC] Market was valued at USD 10.28 billion in 2023 and is expected to reach USD 29.10 billion by 2032, growing at a CAGR of 12.29% from 2024-2032.

The Smart Bandages Market was valued at USD 767.6 million in 2023 and is expected to reach USD 2111.5 million in 2032 and grow at a CAGR of 11.9% over the forecast period of 2024-2032.

The Clinical Documentation Improvement Market Size was assessed to be worth USD 5.13 billion in 2023 and is expected to increase to USD 9.96 billion by 2032.

Pediatric Hospitals Market was valued at USD 159.3 billion in 2023 and is expected to reach USD 257.3 billion by 2032, growing at a CAGR of 5.5% over the forecast period 2024-2032.

The Healthcare Mobility Solutions Market Size was valued at USD 150.19 billion in 2023, and is expected to reach USD 1143.40 billion by 2032, and grow at a CAGR of 25.3% over the forecast period 2024-2032.

Capillary Blood Collection Devices Market size was estimated at USD 1.88 Billion in 2023 and is projected to reach USD 3.83 Billion by 2032 at a CAGR of 8.26%.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd