To Get More Information on Neonatal Critical Care Equipment Market - Request Sample Report

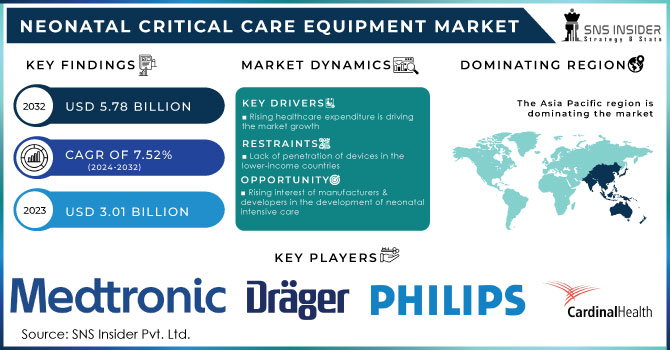

The Neonatal Critical Care Equipment Market size was estimated at USD 3.01 billion in 2023 and is expected to reach USD 5.78 billion by 2032 with a growing CAGR of 7.52% during the forecast period of 2024-2032.

Neonates are cared for using specialized equipment due to prenatal abnormalities or premature births, neonates are cared for using specialized equipment. For the neonates born prematurely, incubators are in high demand in the NICU facilities. The WHO estimates that 15 million babies are born prematurely each year around the world. Neonatal admissions to the NICU have increased as a result of this larger number. Additionally, if neonatal diseases become more prevalent, end users may need more care equipment. Additionally, it is projected that increased R&D by medical device businesses and the introduction of cutting-edge products will raise market potential throughout the forecast period.

DRIVERS

Because of the rising expense of healthcare, the market for neonatal intensive care is expanding significantly. Due to increased funding for healthcare, particularly in developing countries, new care facilities can now be expanded and improved. As a result, there is a greater need for goods and services connected to neonatal intensive care. A rise in healthcare funding has made it possible to build neonatal intensive care units (NICUs) with modern amenities and additional beds. These facilities require large infrastructure, medical equipment, and staffing investments. When there are more NICU beds available, a greater number of neonates in need of intensive care can be admitted and treated. This growth is a response to the growing need for neonatal intensive care services, particularly in regions with a higher incidence of preterm births and neonatal diseases.

RESTRAIN

OPPORTUNITY

The Neonatal Intensive Care Industry is expanding as a result of manufacturers and developers increased interest in the development of neonatal intensive care equipment and the newest product launches. For instance, following the U.S. Food and Drug Administration's (FDA) marketing permission, Medtronic plc, a multinational medical technology company, announced the U.S. commercial launch of the Carpediem Cardio-Renal Pediatric Dialysis Emergency Machine in November 2021. The joint efforts of manufacturers to establish a presence in new markets also help to the expansion of the Neonatal Intensive Care Market.

CHALLENGES

The rise of neonatal intensive care is likely to be constrained by factors such as a lack of awareness, economic restraints, and declining birth rates in industrialized countries. The biggest and most important challenge to market expansion will be the absence of regulatory approval for critical care equipment.

According to the United Nations Population Fund (UNPFA), an estimated 265,000 pregnant women who were unable to get maternal care when the violence started. This is corroborated by the fact that several hospitals have been hastily moved into bomb shelters and underground metro stations as they become inoperable or inaccessible. Numerous infants are delivered in bomb shelters without a stable power source. The risk of difficulties, illness, and death for mothers and newborns will rise due to filthy circumstances during deliveries underground caused by attacks on hospitals and healthcare institutions, according to the WHO external status report. According to UNICEF, the medical staff at the subpar underground medical center is working under extreme strain and filling various responsibilities because to a labor shortage. The likelihood of premature deliveries has been observed in recent reports. Preterm infants need specialized care, which is probably not available at such crucial times.

IMPACT OF ONGOING RECESSION

As a result of COVID-19, economic recession has happened in practically all nations. Previous studies have shown that these financial crises have a disproportionately negative impact on children's health and mortality in low- and middle-income countries (but not in high-income ones), and that these impacts are probably independent of whether or not children have COVID-19 disease. The cumulative impacts of environmental contamination, nutrient inadequacy, maternal factors, injury, and personal sickness control are thought to be the mechanisms linking social health variables like GDP per capita to child mortality in low- and middle-income nations. For instance, as households attempt to overcome poverty by moving to less-than-ideal housing with poorer sanitation and greater crowding, as well as by changing their diets away from expensive sources of protein and micronutrients, reductions in household income can unleash dual effects of environmental contamination and nutrient deficiency.

By Type

Thermoregulation Equipment

Infant Warmers

Incubators

Phototherapy Equipment

Neonatal Monitoring Devices

Cardiac Monitors

Capnographs

Integrated Monitoring Devices

Respiratory Devices

Neonatal Ventilators

Continuous Positive Airway Pressure (CPAP) Devices

Oxygen Analyzers and Monitors

Resuscitators

Others

Others

In 2022, thermoregulation equipment segment is accounted the largest market share of 33.2% during the forecast period. The demand for thermoregulation equipment is anticipated to rise throughout the projected period due to the rising prevalence of newborn hypothermia and greater awareness of the high mortality and morbidity associated with it. The prevalence of hypothermia is higher in developing nations, where it affects between 34% and 87% of neonates born in hospitals and between 13% and 94% of those born at home, according to a research article published in the National Library of Medicine in September 2021.

By End User

Hospitals

Clinics

Others

In 2022, the hospitals segment is expected to held the highest market share of 58.1% during the forecast period, the segment is anticipated to develop the fastest by opening new centers and collaborating with other groups, hospitals that offer newborn critical care are increasing their treatment options. For instance, the Motherhood Hospitals network opened five virtual Neonatal Intensive Care Units (NICUs) in India in April 2023. The addition of cutting-edge treatments to a hospital's service portfolio helps it to gain market share.

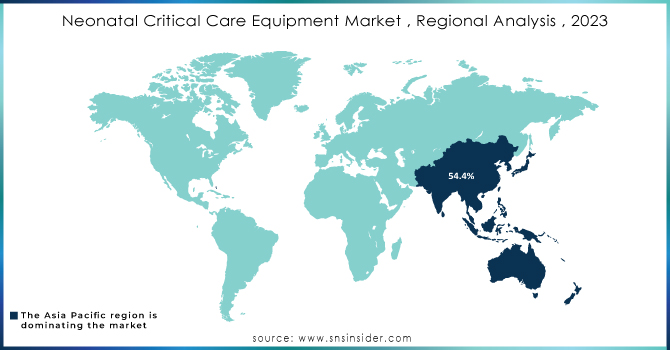

Asia Pacific held a significant market share of 54.4% in 2022 owing to the technological developments in neonatal critical care equipment and an increase in preterm deliveries. A UNICEF database shows that in South Asia, the newborn mortality rate was 22.993 per 1,002 live births in 2021, which resulted in 801,695 neonatal fatalities in this region. Therefore, growth throughout the forecast period is likely to be driven by the availability of a sizable patient pool, rising awareness regarding neonatal care, and the expanding presence of global players.

Middle East & Africa is witness to expand fastest market share during the forecast due to preterm births are becoming more common in Africa. Infections and illnesses are known to be more contagious in preterm babies. According to a JAMA Network article, the majority of preterm births (approximately 60%) take place in Africa and South Asia. Therefore, fetal incubators and fetal monitors must be used to keep an eye on these neonates. The demand for monitoring tools and equipment is predicted to rise as a result of these causes, accelerating technical development.

Do You Need any Customization Research on Neonatal Critical Care Equipment Market - Enquire Now

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major players are Drägerwerk AG & Co. KGaA, Cardinal Health, Koninklijke Philips N.V., Medtronic, GE Healthcare, Fisher & Paykel Healthcare Limited, Masimo, Phoenix Medical Systems (P) Ltd., Natus Medical Incorporated, Utah Medical Products, Inc., Inspiration Healthcare Group plc, Atom Medical Corp, and Others.

In July 2023, Evita V800, V600, and Babylog VN800 ventilators made by Drägerwerk AG & Co. KGaA have been given FDA 510(k) approval for use on both adults and newborns.

In May 2023, Sibel Health's Anne One platform for newborn and baby monitoring has gained U.S. FDA 510(k) clearance. It is an adult, infant, and neonate-specific wireless, clinical-grade, continuous monitoring solution

| Report Attributes | Details |

| Market Size in 2023 | US$ 3.01 billion |

| Market Size by 2032 | US$ 5.78 billion |

| CAGR | CAGR of 7.52% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Thermoregulation Equipment, Phototherapy Equipment, Neonatal Monitoring Devices, Respiratory Devices, Others) • By End User (Hospitals, Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Texas Instruments (US), Skyworks Solutions, Inc. (US), Analog Devices (US), Broadcom Inc. (US), and Infineon Technologies (Germany), ON Semiconductor (U.S.), Murata Manufacturing Company Ltd (Japan), STMicroelectronics N.V. (Switzerland), NXP Semiconductors N.V. (the Netherlands), Vicor Corporation (U.S.) |

| Key Drivers | • Rising healthcare expenditure is driving the market growth |

| Market Challenges | • Lack of penetration of devices in the lower-income countries |

Ans: The growth rate of the neonatal critical care equipment market is expected to grow USD 5.78 billion by 2032.

Ans: Neonatal critical care equipment market is anticipated to expand by 7.52% from 2024 to 2032.

Ans: Neonatal critical care equipment market size was valued at USD 3.01 billion in 2023.

Ans: Asia Pacific segment is expected to held the highest market share in 2023.

Ans: Lack of penetration of devices in the lower-income countries.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Russia-Ukraine War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Neonatal Critical Care Equipment Market Segmentation, By Type

8.1 Thermoregulation Equipment

8.1.1 Infant Warmers

8.1.2 Incubators

8.2 Phototherapy Equipment

8.2.1 Neonatal Monitoring Devices

8.2.2 Blood Pressure Monitors

8.2.3 Cardiac Monitors

8.2.4 Pulse Oximeters

8.2.5 Capnographs

8.2.6 Integrated Monitoring Devices

8.3 Respiratory Devices

8.3.1 Neonatal Ventilators

8.3.2 Continuous Positive Airway Pressure (CPAP) Devices

8.3.3 Oxygen Analyzers and Monitors

8.3.4 Resuscitators

8.3.5 Others

8.4 Others

9. Neonatal Critical Care Equipment Market Segmentation, By End User

9.1 Hospitals

9.2 Clinics

9.3 Others

10. Regional Analysis

10.1 Introduction

10.2 North America

10.2.1 North America Neonatal Critical Care Equipment Market by Country

10.2.2North America Neonatal Critical Care Equipment Market by Type

10.2.3 North America Neonatal Critical Care Equipment Market by End User

10.2.4 USA

10.2.4.1 USA Neonatal Critical Care Equipment Market by Type

10.2.4.2 USA Neonatal Critical Care Equipment Market by End User

10.2.5 Canada

10.2.5.1 Canada Neonatal Critical Care Equipment Market by Type

10.2.5.2 Canada Neonatal Critical Care Equipment Market by End User

10.2.6 Mexico

10.2.6.1 Mexico Neonatal Critical Care Equipment Market by Type

10.2.6.2 Mexico Neonatal Critical Care Equipment Market by End User

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Eastern Europe Neonatal Critical Care Equipment Market by Country

10.3.1.2 Eastern Europe Neonatal Critical Care Equipment Market by Type

10.3.1.3 Eastern Europe Neonatal Critical Care Equipment Market by End User

10.3.1.4 Poland

10.3.1.4.1 Poland Neonatal Critical Care Equipment Market by Type

10.3.1.4.2 Poland Neonatal Critical Care Equipment Market by End User

10.3.1.5 Romania

10.3.1.5.1 Romania Neonatal Critical Care Equipment Market by Type

10.3.1.5.2 Romania Neonatal Critical Care Equipment Market by End User

10.3.1.6 Hungary

10.3.1.6.1 Hungary Neonatal Critical Care Equipment Market by Type

10.3.1.6.2 Hungary Neonatal Critical Care Equipment Market by End User

10.3.1.7 Turkey

10.3.1.7.1 Turkey Neonatal Critical Care Equipment Market by Type

10.3.1.7.2 Turkey Neonatal Critical Care Equipment Market by End User

10.3.1.8 Rest of Eastern Europe

10.3.1.8.1 Rest of Eastern Europe Neonatal Critical Care Equipment Market by Type

10.3.1.8.2 Rest of Eastern Europe Neonatal Critical Care Equipment Market by End User

10.3.2 Western Europe

10.3.2.1 Western Europe Neonatal Critical Care Equipment Market by Country

10.3.2.2 Western Europe Neonatal Critical Care Equipment Market by Type

10.3.2.3 Western Europe Neonatal Critical Care Equipment Market by End User

10.3.2.4 Germany

10.3.2.4.1 Germany Neonatal Critical Care Equipment Market by Type

10.3.2.4.2 Germany Neonatal Critical Care Equipment Market by End User

10.3.2.5 France

10.3.2.5.1 France Neonatal Critical Care Equipment Market by Type

10.3.2.5.2 France Neonatal Critical Care Equipment Market by End User

10.3.2.6 UK

10.3.2.6.1 UK Neonatal Critical Care Equipment Market by Type

10.3.2.6.2 UK Neonatal Critical Care Equipment Market by End User

10.3.2.7 Italy

10.3.2.7.1 Italy Neonatal Critical Care Equipment Market by Type

10.3.2.7.2 Italy Neonatal Critical Care Equipment Market by End User

10.3.2.8 Spain

10.3.2.8.1 Spain Neonatal Critical Care Equipment Market by Type

10.3.2.8.2 Spain Neonatal Critical Care Equipment Market by End User

10.3.2.9 Netherlands

10.3.2.9.1 Netherlands Neonatal Critical Care Equipment Market by Type

10.3.2.9.2 Netherlands Neonatal Critical Care Equipment Market by End User

10.3.2.10 Switzerland

10.3.2.10.1 Switzerland Neonatal Critical Care Equipment Market by Type

10.3.2.10.2 Switzerland Neonatal Critical Care Equipment Market by End User

10.3.2.11 Austria

10.3.2.11.1 Austria Neonatal Critical Care Equipment Market by Type

10.3.2.11.2 Austria Neonatal Critical Care Equipment Market by End User

10.3.2.12 Rest of Western Europe

10.3.2.12.1 Rest of Western Europe Neonatal Critical Care Equipment Market by Type

10.3.2.12.2 Rest of Western Europe Neonatal Critical Care Equipment Market by End User

10.4 Asia-Pacific

10.4.1 Asia Pacific Neonatal Critical Care Equipment Market by Country

10.4.2 Asia Pacific Neonatal Critical Care Equipment Market by Type

10.4.3 Asia Pacific Neonatal Critical Care Equipment Market by End User

10.4.4 China

10.4.4.1 China Neonatal Critical Care Equipment Market by Type

10.4.4.2 China Neonatal Critical Care Equipment Market by End User

10.4.5 India

10.4.5.1 India Neonatal Critical Care Equipment Market by Type

10.4.5.2 India Neonatal Critical Care Equipment Market by End User

10.4.6 Japan

10.4.6.1 Japan Neonatal Critical Care Equipment Market by Type

10.4.6.2 Japan Neonatal Critical Care Equipment Market by End User

10.4.7 South Korea

10.4.7.1 South Korea Neonatal Critical Care Equipment Market by Type

10.4.7.2 South Korea Neonatal Critical Care Equipment Market by End User

10.4.8 Vietnam

10.4.8.1 Vietnam Neonatal Critical Care Equipment Market by Type

10.4.8.2 Vietnam Neonatal Critical Care Equipment Market by End User

10.4.9 Singapore

10.4.9.1 Singapore Neonatal Critical Care Equipment Market by Type

10.4.9.2 Singapore Neonatal Critical Care Equipment Market by End User

10.4.10 Australia

10.4.10.1 Australia Neonatal Critical Care Equipment Market by Type

10.4.10.2 Australia Neonatal Critical Care Equipment Market by End User

10.4.11 Rest of Asia-Pacific

10.4.11.1 Rest of Asia-Pacific Neonatal Critical Care Equipment Market by Type

10.4.11.2 Rest of Asia-Pacific APAC Neonatal Critical Care Equipment Market by End User

10.5 Middle East & Africa

10.5.1 Middle East

10.5.1.1 Middle East Neonatal Critical Care Equipment Market by Country

10.5.1.2 Middle East Neonatal Critical Care Equipment Market by Type

10.5.1.3 Middle East Neonatal Critical Care Equipment Market by End User

10.5.1.4 UAE

10.5.1.4.1 UAE Neonatal Critical Care Equipment Market by Type

10.5.1.4.2 UAE Neonatal Critical Care Equipment Market by End User

10.5.1.5 Egypt

10.5.1.5.1 Egypt Neonatal Critical Care Equipment Market by Type

10.5.1.5.2 Egypt Neonatal Critical Care Equipment Market by End User

10.5.1.6 Saudi Arabia

10.5.1.6.1 Saudi Arabia Neonatal Critical Care Equipment Market by Type

10.5.1.6.2 Saudi Arabia Neonatal Critical Care Equipment Market by End User

10.5.1.7 Qatar

10.5.1.7.1 Qatar Neonatal Critical Care Equipment Market by Type

10.5.1.7.2 Qatar Neonatal Critical Care Equipment Market by End User

10.5.1.8 Rest of Middle East

10.5.1.8.1 Rest of Middle East Neonatal Critical Care Equipment Market by Type

10.5.1.8.2 Rest of Middle East Neonatal Critical Care Equipment Market by End User

10.5.2 Africa

10.5.2.1 Africa Neonatal Critical Care Equipment Market by Country

10.5.2.2 Africa Neonatal Critical Care Equipment Market by Type

10.5.2.3 Africa Neonatal Critical Care Equipment Market by End User

10.5.2.4 Nigeria

10.5.2.4.1 Nigeria Neonatal Critical Care Equipment Market by Type

10.5.2.4.2 Nigeria Neonatal Critical Care Equipment Market by End User

10.5.2.5 South Africa

10.5.2.5.1 South Africa Neonatal Critical Care Equipment Market by Type

10.5.2.5.2 South Africa Neonatal Critical Care Equipment Market by End User

10.5.2.6 Rest of Africa

10.5.2.6.1 Rest of Africa Neonatal Critical Care Equipment Market by Type

10.5.2.6.2 Rest of Africa Neonatal Critical Care Equipment Market by End User

10.6 Latin America

10.6.1 Latin America Neonatal Critical Care Equipment Market by Country

10.6.2 Latin America Neonatal Critical Care Equipment Market by Type

10.6.3 Latin America Neonatal Critical Care Equipment Market by End User

10.6.4 Brazil

10.6.4.1 Brazil Neonatal Critical Care Equipment Market by Type

10.6.4.2 Brazil Africa Neonatal Critical Care Equipment Market by End User

10.6.5 Argentina

10.6.5.1 Argentina Neonatal Critical Care Equipment Market by Type

10.6.5.2 Argentina Neonatal Critical Care Equipment Market by End User

10.6.6 Colombia

10.6.6.1 Colombia Neonatal Critical Care Equipment Market by Type

10.6.6.2 Colombia Neonatal Critical Care Equipment Market by End User

10.6.7 Rest of Latin America

10.6.7.1 Rest of Latin America Neonatal Critical Care Equipment Market by Type

10.6.7.2 Rest of Latin America Neonatal Critical Care Equipment Market by End User

11. Company Profile

11.1 Drägerwerk AG & Co. KGaA

11.1.1 Company Overview

11.1.2 Financials

11.1.3 Product/Services Offered

11.1.4 SWOT Analysis

11.1.5 The SNS View

11.2 Cardinal Health

11.2.1 Company Overview

11.2.2 Financials

11.2.3 Product/Services Offered

11.2.4 SWOT Analysis

11.2.5 The SNS View

11.3 Koninklijke Philips N.V.

11.3.1 Company Overview

11.3.2 Financials

11.3.3 Product/Services Offered

11.3.4 SWOT Analysis

11.3.5 The SNS View

11.4 Medtronic

11.4 Company Overview

11.4.2 Financials

11.4.3 Product/Services Offered

11.4.4 SWOT Analysis

11.4.5 The SNS View

11.5 GE Healthcare

11.5.1 Company Overview

11.5.2 Financials

11.5.3 Product/Services Offered

11.5.4 SWOT Analysis

11.5.5 The SNS View

11.6 Fisher & Paykel Healthcare Limited

11.6.1 Company Overview

11.6.2 Financials

11.6.3 Product/Services Offered

11.6.4 SWOT Analysis

11.6.5 The SNS View

11.7 Masimo

11.7.1 Company Overview

11.7.2 Financials

11.7.3 Product/Services Offered

11.7.4 SWOT Analysis

11.7.5 The SNS View

11.8 Phoenix Medical Systems (P) Ltd.

11.8.1 Company Overview

11.8.2 Financials

11.8.3 Product/Services Offered

11.8.4 SWOT Analysis

11.8.5 The SNS View

11.9 Natus Medical Incorporated

11.9.1 Company Overview

11.9.2 Financials

11.9.3 Product/Services Offered

11.9.4 SWOT Analysis

11.9.5 The SNS View

11.10 Utah Medical Products, Inc.

11.10.1 Company Overview

11.10.2 Financials

11.10.3 Product/Services Offered

11.10.4 SWOT Analysis

11.10.5 The SNS View

11.11 Inspiration Healthcare Group plc

11.11.1 Company Overview

11.11.2 Financials

11.11.3 Product/Services Offered

11.11.4 SWOT Analysis

11.11.5 The SNS View

11.12 Atom Medical Corp

11.12.1 Company Overview

11.12.2 Financials

11.12.3 Product/Services Offered

11.12.4 SWOT Analysis

11.12.5 The SNS View

12. Competitive Landscape

12.1 Competitive Benchmarking

12.2 Market Share Analysis

12.3 Recent Developments

12.3.1 Industry News

12.3.2 Company News

12.3.3 Mergers & Acquisitions

13. USE Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Brain Computer Interface Market size was valued at USD 2.23 billion in 2023 and is expected to reach USD 8.36 billion by 2032 and grow at a CAGR of 15.81% over the forecast period of 2024-2032.

The Whole Genome Sequencing Market Size USD 4.13 billion in 2023 and will reach USD 22.2 billion by 2032 and grow at a CAGR of 20.6% by 2024-2032.

The Anxiety Disorder Treatment Market Size was estimated at US$ 12.4 billion in 2023 and is projected to reach at US$ 16.4 billion by 2031 with a growing CAGR of 3.95% Over the Forecast Period of 2024-2031.

The Biohacking Market size was valued at USD 23.5 billion in 2023 and is expected to reach USD 97.07 billion by 2031 and grow at a CAGR of 19.4% over the forecast period of 2024-2031.

The Radiation Dose Optimization Software Market was valued at USD 3.80 Billion in 2023 and will reach USD 8.06 Billion by 2032, with a growing CAGR of 8.7% during 2024-2032.

The Capnography Devices Market size was valued at USD 605.37 million in 2023 and is expected to reach USD 1460.84 million by 2032 and grow at a CAGR of 10.28% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd