Multi-Layer Cryogenic Insulation Market Report Scope & Overview:

Get more information on Multi-Layer Cryogenic Insulation Market - Request Sample Report

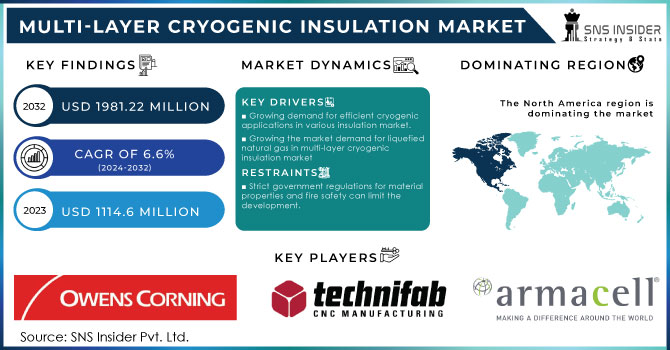

The Multi-Layer Cryogenic Insulation Market size was valued at USD 1114.6 Million in 2023 and is expected to reach USD 1981.22 Million by 2032, growing at a CAGR of 6.60% over the forecast period 2024-2032.

The multi-layer cryogenic insulation market overview highlights key aspects shaping the industry. our report covers supply chain analysis, identifying key players, and key regulations and standards impacting compliance. It examines cost structure and pricing trends, as well as end-user adoption trends driving demand. the report also identifies growth opportunities in emerging markets, outlines investment & funding activities, explores customer preferences and behaviour, and reviews trade and export-import data influencing global market dynamics.

Market Dynamics

Drivers

-

Growing Demand for Energy Efficiency in Cryogenic Applications Drives the Multi-Layer Cryogenic Insulation Market Growth

The shifting focus on improved energy efficiency in several vertical cryogenic applications is also one of the target areas, that drives the adoption of multi-layer cryogenic insulation. LNG storage, aerospace, and pharmaceuticals are some of the industries that strive for high-efficiency solutions that can cut down on operating expenses and environmental footprint. Because multi-layer insulation systems offer exceptional thermal resistance, they play a critical role in stabilizing temperatures during the storage and transport of cryogenic fluids. With an increase in energy consumption worldwide, firms are on a mission to make the most out of energy usage. This move towards energy efficiency is backed by regulation to cut down greenhouse gas emissions, thereby accelerating the technology adoption for advanced insulation. As a result, the multi-layer cryogenic insulation market will experience growth because industries are looking for solutions that are not only economical but also sustainable.

Restraints

-

High Initial Costs of Multi-Layer Cryogenic Insulation Solutions Limit Market Adoption in Some Industries

The high initial cost of multi-layer cryogenic insulation technology has been one of the major restraints for the overall market growth. Even though energy efficiency and low operation costs are ongoing benefits of multi-layer insulation, these strengths cannot be immediately seen by many industries, especially small-scale operations limited to certain budgets, due to the high capital expenditure needed upfront for these materials. This tricky barrier generally makes us cautious in the adoption of new technology, especially in sectors where conventional insulating materials remain in use. A further complication of the tangle of installation, and labors to specialize in the demonstration will also slow down applying steps to multi-layer cryogenic insulation systems. Consequently, we may see slower market development in those regions or segments where cost is a key driver and the value proposition of the advanced insulation solution can be limited.

Opportunities

-

Increasing Focus on Sustainable Energy Solutions Creates Demand for Multi-Layer Cryogenic Insulation Technologies

With the increasing focus of the world towards mitigating the impact of climate change, more and more sectors have started moving towards sustainable energy solutions. Multi-layer technologies for cryogenic insulation are well-suited for these sustainability efforts, significantly improving energy savings and avoiding greenhouse gas emissions. With manufacturers that produce, store, and transport cryogenic fluids constantly striving to achieve their sustainability targets, there is a growing demand for innovative insulation solutions. Manufacturers can produce sustainable insulation products along with their environmental advantages. Leveraging the increasing demand for sustainable technologies, the multi-layer cryogenic insulation market can enter various profitable avenues and create a wider customer base from organizations that seek to pursue environmental sustainability as a part of their operations.

Challenge

-

Technical Challenges in Manufacturing and Installation of Multi-Layer Cryogenic Insulation Systems Impact Market Growth

Technical challenges regarding the manufacturing and installation of these advanced systems will hinder the growth of the multi-layer cryogenic insulation market. High-quality insulation materials must be carefully engineered to meet strict quality standards, which can complicate manufacturing. Furthermore, these insulating materials require special skills to install multi-layer insulation systems, delaying the process and raising the costs. Such technical challenges may discourage end customers from adopting multi-layer cryogenic insulation solutions, especially in sectors more used to conventional insulation materials and methods. Addressing these challenges is critical to enabling growth in the market and the acceptance of multi-layer cryogenic insulation products in a wide variety of applications.

Segmental Analysis

By Type

Rigid Insulation dominated and had the highest market share in the Multi-Layer Cryogenic Insulation Market in 2023. Rigid Insulation held almost 65% of the entire market share. Polyurethane (PU) & Polyisocyanurate (PIR) are the two most significant raw materials used for rigid insulation which together contribute 55% market share to rigid insulation. Due to excellent insulation properties, superior durability, and withstanding temperatures at both cryogenic levels rigid insulation is considered superior for Cryogenic applications. In particular, PU & PIR materials have a higher thermal resistance with lower thermal conductivity, which makes them suitable for use in insulation environments such as LNG storage tanks and pipelines. These materials also ensure more energy efficiency because the heat loss is reduced, thus helping in the safe transportation and storage of cryogenic fluids. Their application in energy, chemicals, and metallurgy, among others, boosts their importance in the Multi-Layer Cryogenic Insulation Market, especially where infrastructure requires insulation services for extended durations.

By Product Type

Polyurethane (PU) & Polyisocyanurate (PIR) dominated and held the largest share of the Multi-Layer Cryogenic Insulation Market in 2023, taking up around 45% of the market share. Under the PU & PIR subsegment, Polyurethane (PU) was the most widely used material, at around 60%. PU insulation is highly sought after for its flexibility, high thermal performance, and cost-effectiveness. It provides low thermal conductivity that is very vital in cryogenic applications where the insulation has to be performed at extreme temperatures. Further, PU materials are very excellent in terms of moisture resistance which is fundamental in environments like LNG storage and transportation. The PU & PIR-based multi-layer cryogenic insulation finds application in allowing lower energy consumption, and consequently lesser heat transfer, in the demanding sectors such as LNG storage, petrochemical, and industrial gas industries. Ease of installation and long-term durability further boost the demand for such applications.

By Material

The rigid insulation segment dominated and held the highest revenue share in the Multi-Layer Cryogenic Insulation Market in 2023, accounting for nearly 55% of the market share. Its dominance can be ascribed to the best heat insulation characteristics that are required to keep the temperature stable in cryogenic developments. Rigid insulation is a common type used in industries such as LNG that you need to properly insulate to avoid losing energy. High-performance rigid insulation, in turn, is demanded by growing end-use application segments such as LNG storage & transportation systems. While the IEA states a variety of insulation technologies can lower energy consumption in LNG facilities, the organization's message still reinforces the use of rigid insulation in cryogenic environments.

By End-Use Industry

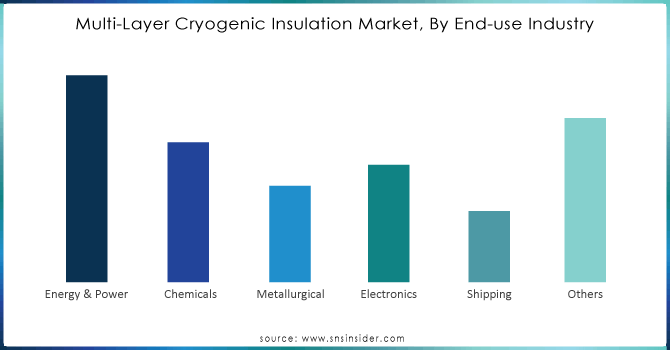

In 2023, the energy & power sector dominated the Multi-Layer Cryogenic Insulation Market, accounting for a 50% share of the total market. This is driven by the increasing global demand for liquefied natural gas (LNG) as well as other energy sources that need cryogenic insulation. Advanced cryogenic insulation solutions are gaining traction in response to the energy sector's need to minimize carbon footprints while improving energy efficiency in storage and transportation processes. The need for an economic shift to more sustainable energy sources has led to increased use of technologies such as cryogenic insulation to sustain energy efficiency, which is the primary reason for market growth within the sector, as per the International Energy Agency (IEA).

By Application

In 2023, the LNG storage tanks application segment accounted for about 60% of the Multi-Layer Cryogenic Insulation Market. In addition, during the storage of LNG, the insulation material is required to have ultra-low thermal conductivity and zero energy loss. One of the main factors driving the market is the worldwide expansion of the liquefied natural gas infrastructure, triggered by the growing tendency toward natural gas as a cleaner energy alternative. The increasing demand for insulation is fueled by the expansion of liquefied natural gas (LNG) storage capacity in different regions and LNG storage tanks are the key application in the cryogenic insulation market.

Get Customized Report as per your Business Requirement - Request For Customized Report

Regional Analysis

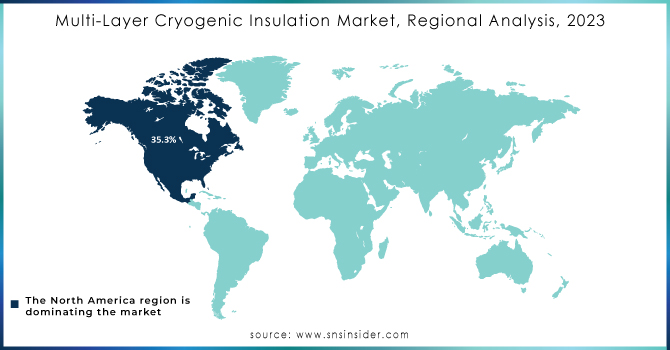

North America dominated and accounted for a market share of around 40% in the Multi-Layer Cryogenic Insulation Market in 2023. The ever-growing U.S. and Canadian LNG and energy sector needs this dominance. Projects that the U.S. Department of Energy supports, such as the Sabine Pass LNG Terminal, involve LNG infrastructure that requires state-of-the-art insulation. Furthermore, the increasing trend of sustainable energy in Canada and LNG production in Canada driving the growth of the market. Market players such as Owens Corning and Aspen Aerogels are developing innovative cryogenic insulation systems to keep North America relevant in the market.

In 2023, Europe accounted for the second-largest market share at 30% in the Multi-Layer Cryogenic Insulation Market. A large part of the growth in the region comes from substantial investment activities in LNG terminals, particularly in Norway, Russia, and the Netherlands. By encouraging energy efficiency in the building and construction sector, a pledge by the European Union to cut emissions drives demand for insulation materials that are energy efficient. As countries such as Germany put their money into renewable energy, they would need more of this cryogenic insulation via LNG storage and transportation. Demand for these solutions is bolstered further by supporting EU funding for sustainable LNG infrastructure.

The Asia Pacific, region emerged as the fastest growing region with the highest CAGR of 6.5% during the forecast period in the Multi-Layer Cryogenic Insulation Market. A major contributor to this growth is the expansion of China´s LNG imports complemented with investments in LNG infrastructure by companies such as CNPC. Demand for cryogenic insulation is further driven by India and Japan’s industrial sectors, especially automotive and electronics. As per the Asian Development Bank, the necessity of effective insulation brought about by the growth of the region for the construction of LNG import terminals will constantly drive the development of this market.

Key Players

-

Abhijit Enterprises (Cryogenic Insulation Materials, Multi-Layer Thermal Insulation)

-

Altrad (Cryogenic Insulation, Thermal Insulation Systems)

-

Armacell International Holding GmbH (Armaflex, ArmaSound)

-

Aspen Aerogels (Aerogel Insulation, Cryogel Z)

-

Cabot Corporation (Cabot Aerogel, Cryogenic Insulation Materials)

-

Callenberg Technology Company (Cryogenic Insulation Systems, Callenberg Cryofoam)

-

Dunmore Corporation (Multi-Layer Insulation, Cryogenic Films)

-

Herose Limited (Cryogenic Valves, Cryogenic Insulation Systems)

-

Hertel (Cryogenic Insulation Materials, Thermal Insulation Products)

-

Imerys S.A. (Thermal Insulation Materials, Insulation Coatings)

-

Isolatie Combinatie Beverwijk B.V. (Thermal Insulation, Cryogenic Insulation)

-

Kaefer (Cryogenic Insulation, Multi-Layer Thermal Insulation)

-

Lydall Inc. (Thermal Insulation Materials, Cryogenic Insulation Solutions)

-

NICHIAS Corporation (Cryogenic Insulation Materials, Thermal Insulation Products)

-

Norplex Micarta (Thermal Insulation Solutions, Cryogenic Insulation Products)

-

Rochling Industrial (Thermal Insulation Materials, Cryogenic Insulation Solutions)

-

Ruag (Cryogenic Insulation, Multi-Layer Thermal Insulation)

-

Technifab Products (Cryogenic Insulation, Thermal Insulation Systems)

-

Thermaxx Jackets (Thermal Insulation Jackets, Cryogenic Insulation Jackets)

-

Unifrax I LLC (Cryogenic Insulation, Thermal Insulation Products)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1114.6 Million |

| Market Size by 2032 | USD 1981.22 Million |

| CAGR | CAGR of 6.60% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Flexible Insulation, Rigid Insulation) •By Product Type (Polyurethane (PU) & Polyisocyanurate (PIR), Cellular Glass, Polystyrene, Fiberglass, Perlite, Others) •By Material (Glass Wool, Mineral Wool, Foam Plastics, Others) •By End-Use Industry (Energy & Power, Chemicals, Metallurgical, Electronics, Shipping, Others) •By Application (LNG Storage Tanks, Cryogenic Pipes, Cryogenic Pumps, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Owens Corning, Technifab Products, Armacell International Holding GmbH, Cabot Corporation, Lydall Inc., Aspen Aerogels, Dunmore Corporation, NICHIAS Corporation, Callenberg Technology Company, Rochling Industrial and other key players |