Get more information on Military Wearable Medical Device Market - Request Sample Report

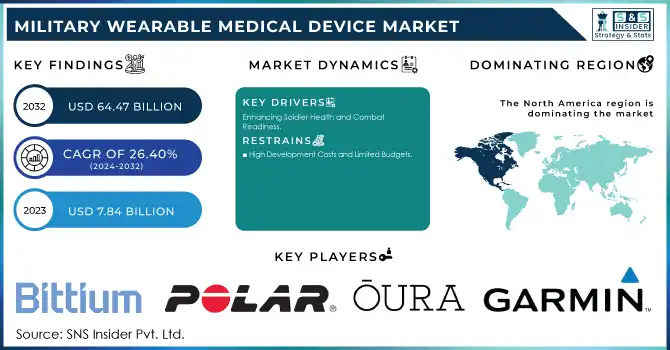

The Military Wearable Medical Device Market Size was valued at USD 7.84 billion in 2023 and is expected to reach USD 64.47 billion by 2032 and grow at a CAGR of 26.40% over the forecast period 2024-2032.

The military wearable medical device market is experiencing remarkable growth, driven by cutting-edge technologies and an increasing emphasis on soldier health and operational efficiency. Wearable medical devices, such as advanced biosensors, smart textiles, and health monitoring systems, are revolutionizing military healthcare by enabling real-time tracking of vital signs, injury detection, and performance metrics. For instance, the U.S. Department of Defense has adopted wearable sensor technology capable of monitoring hydration levels, heart rates, and stress levels in soldiers, enhancing their performance during critical operations. A study by the National Defense Medical College highlights that wearable devices can reduce the time to deliver life-saving interventions in combat zones by up to 30%, significantly improving survival rates. Additionally, smart bandages equipped with biosensors are being tested to monitor wound healing and detect infections early. These bandages transmit data wirelessly to medical teams, allowing timely and precise medical responses. A collaboration between the Pentagon and leading tech firms has further enabled the development of devices that predict disease outbreaks by analyzing soldiers' physiological data in real-time.

In large-scale combat operations, where prolonged care is often required, wearable medical devices have proven indispensable. For example, the U.S. Army has integrated fitness wearables into training programs to measure endurance, predict injuries, and optimize performance. Devices like Hexoskin biometric shirts are being employed to monitor respiratory rates and cardiac activity during high-stress drills.

Despite these advancements, challenges such as data security, interoperability with legacy systems, and the ruggedness of devices in extreme conditions remain. Addressing these issues through robust encryption, standardized protocols, and durable designs is vital for broader adoption. As the military continues to prioritize technology integration, wearable medical devices stand out as transformative tools in ensuring soldier readiness, enhancing survival rates, and maintaining operational superiority. These innovations not only protect soldiers on the battlefield but also pave the way for a more data-driven approach to military healthcare.

Drivers

Enhancing Soldier Health and Combat Readiness

The increasing focus on soldier safety and combat readiness is a significant driver of the military wearable medical device market. As modern warfare grows more complex, ensuring the physical and mental well-being of soldiers is paramount. Wearable medical devices, such as biosensors, smart textiles, and real-time health monitoring systems, provide actionable insights into vital signs like heart rate, hydration levels, and respiratory status. These devices enable early detection of injuries or illnesses, allowing for swift medical intervention on the battlefield. For instance, wearable health monitors can alert commanders to signs of dehydration or exhaustion, preventing potential health crises during critical missions. Additionally, wearable technology supports prolonged care in austere environments where immediate medical assistance might be unavailable, ensuring soldiers remain operational for extended periods. This proactive approach to health management not only improves individual performance but also enhances overall unit efficiency, making these devices indispensable in modern combat scenarios.

Technological Advancements in Wearable Solutions

Technological innovations are transforming the landscape of wearable medical devices for military applications. Advances in miniaturization, AI, and IoT have enabled the creation of compact, lightweight devices capable of tracking multiple health parameters simultaneously. For example, IoT-enabled devices can transmit data to command centers in real time, ensuring remote monitoring and informed decision-making. AI algorithms analyze this data to detect anomalies or predict potential health issues, providing a significant edge in mission planning and execution. Furthermore, rugged designs ensure these devices withstand extreme conditions, including heat, humidity, and mechanical stress. Innovations like smart bandages with embedded sensors for wound monitoring and wireless communication exemplify the cutting-edge applications of these technologies. Such advancements not only improve soldier health management but also streamline logistical and medical support during operations, making technology integration a critical driver of market growth.

Increased Investments and Focus on Mental Health

Rising investments in wearable medical technology by governments and defense organizations are a crucial driver of market expansion. Programs like the U.S. Department of Defense’s initiatives to integrate wearable sensors highlight the growing reliance on technology to enhance soldier readiness. These investments have led to the development of devices that monitor not only physical health but also mental well-being. Stress-monitoring wearables, for example, measure cortisol levels and heart rate variability to provide insights into a soldier’s mental state during high-pressure situations. Such devices are particularly valuable as military operations increasingly prioritize mental resilience alongside physical fitness. Collaboration between defense agencies and tech innovators has further accelerated the pace of development, ensuring that these devices meet the unique demands of military environments. By addressing mental health alongside physical readiness, wearable medical devices are helping create a holistic approach to soldier care, driving their adoption across defense sectors globally.

Restraints

High Development Costs and Limited Budgets

The development of advanced military wearable medical devices involves significant investment in research, prototyping, and testing to meet stringent performance and durability standards. For many nations, especially those with limited defense budgets, the high costs of adopting these cutting-edge technologies pose a challenge, restricting large-scale implementation.

Data Security and Privacy Concerns

Wearable medical devices often rely on wireless data transmission to provide real-time monitoring and analytics. This raises significant concerns about data security and the potential for cyberattacks.

By Application

The heart monitor segment emerged as the largest contributor to the military wearable medical device market in 2023, accounting for approximately 38.0% of the market share. This dominance is driven by the critical need to monitor soldiers' cardiovascular health during high-stress training and combat scenarios. Soldiers often face physically demanding environments and psychological pressures, making them susceptible to cardiovascular issues such as arrhythmias and heart strain. Wearable heart monitors provide real-time insights into heart rate variability and other vital metrics, enabling early detection of potential issues and timely medical intervention. The widespread adoption of these devices reflects the military's commitment to safeguarding soldier health and reducing fatalities caused by cardiovascular complications in the field.

The performance monitor segment is the fastest-growing application in the military wearable medical device market. These devices are increasingly being adopted to enhance soldiers’ operational readiness and physical performance. Performance monitors track key metrics such as fatigue, endurance, hydration, and physical strain, providing military personnel and commanders with real-time feedback to optimize training and mission execution. The rising demand for technologies that can prevent injuries and maximize efficiency during physically intensive operations is a key factor driving growth in this segment. Additionally, the integration of advanced analytics and seamless connectivity with centralized systems makes performance monitors an essential tool for modern military healthcare.

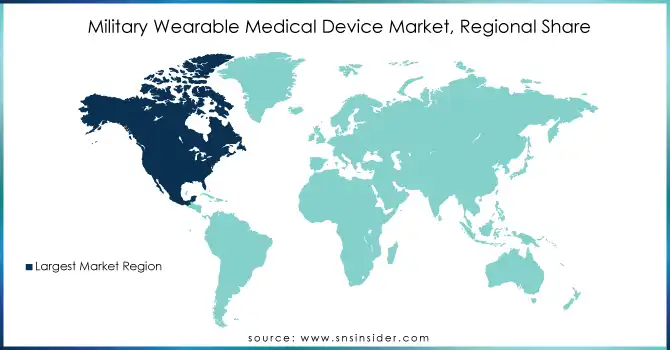

The North American region, particularly the United States, is the dominant player in the military wearable medical device market. This dominance is primarily due to significant investments in advanced defense technologies by the U.S. Department of Defense (DoD), which continually prioritizes soldier health, safety, and performance. The U.S. military is actively integrating wearable medical devices into its systems for real-time health monitoring and injury prevention, with programs that focus on enhancing physical and mental readiness. Furthermore, collaborations with leading tech companies in the wearable and healthcare sectors have accelerated the development and deployment of these devices, driving market growth in this region.

Europe followed closely, with countries like the United Kingdom, Germany, and France making substantial advancements in military health technologies. The European market is experiencing growth due to rising defense budgets, increasing military modernization efforts, and a heightened focus on soldier welfare. European nations are integrating wearables into their military operations to track vital signs, monitor physical performance, and improve mental health in combat situations.

In Asia-Pacific, particularly in China, India, and Japan, the market is expanding at a rapid pace, driven by increasing defense spending and technological advancements. These countries are adopting wearable technologies to enhance military capabilities and soldier safety. As the region focuses on modernizing its defense infrastructure, wearable medical devices are becoming integral to military health systems.

Need any customization research on Military Wearable Medical Device Market - Enquiry Now

Key Players

1. Bittium

Bittium Tough Mobile 2

Bittium BodyGuard 323

Polar H10 Heart Rate Sensor

3. Oura

Oura Ring

4. Garmin

Garmin Forerunner 945

Garmin Fenix 7

5. NeuroMetrix

Quell Wearable Pain Relief

6. GOQii

GOQii Smart Fitness Tracker

7. Apple Inc.

Apple Watch Series 8

Apple Watch Ultra

8. Samsung

Samsung Galaxy Watch 6

9. Fitbit

Fitbit Charge 5

Fitbit Sense

10. Zephyr Technology Corporation

Zephyr BioHarness 3

11. Camntech

SleepProfiler 4.0

Actiwatch Spectrum

Recent Developments

In June 2024, INVIZA Health was awarded a USD 2.3 million SEMI NBMC contract by the U.S. Air Force to enhance military and medical monitoring with its InvizaCare M1.0 platform. This innovative solution integrates machine learning, self-charging smart insoles, and secure cloud-based platforms for real-time health monitoring of airmen and military personnel.

In April 2023, The U.S. Department of Defense (DoD), through its Defense Innovation Unit (DIU), partnered with the private sector to develop wearable technology capable of rapidly detecting diseases, such as infections. This innovation proved highly effective during the COVID-19 pandemic, enhancing the ability to monitor and manage soldier health in real time.

In Nov 2023, Dallas-based Articulate Labs, in partnership with the Military Consortium, was awarded USD 1.3 million to conduct a clinical trial testing its innovative knee injury wearable technology. The funding will support efforts to accelerate the rehabilitation of service members, enabling faster recovery and a quicker return to duty.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 7.84 billion |

| Market Size by 2032 | USD 64.47 Billion |

| CAGR | CAGR of 26.40% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application [Heart Monitor (Sick Alert, Heart Rate Variability), Performance Monitor (Sleep-wake Cycle Alert, Core Body Temperature Monitoring)] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Bittium, Polar Electro, Oura, Garmin, NeuroMetrix, GOQii, Apple Inc., Samsung, Fitbit, Zephyr Technology Corporation, Camntech |

| Key Drivers | • Enhancing Soldier Health and Combat Readiness • Technological Advancements in Wearable Solutions • Increased Investments and Focus on Mental Health |

| Restraints | • High Development Costs and Limited Budgets • Data Security and Privacy Concerns |

Ans: The Military Wearable Medical Device Market size was valued at US$ 7.84 bn in 2023.

Ans: The Military Wearable Medical Device Market is to grow at a CAGR of 26.40% during the forecast period 2024-2032.

Due to technical improvements and increased R&D spending in military equipment, North America led the market in 2020 and is likely to continue to do so over the forecast period.

Military Wearable Medical Device Market is expected to reach USD 64.47 billion by 2032

key drivers of the Military Wearable Medical Device Market is Need for advance technology, Increase in R&D investment, need to improve in military performance

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Prescription Trends, (2023), by Region

5.3 Device Volume, by Region (2020-2032)

5.4 Healthcare Spending, by Region, (Government, Commercial, Private, Out-of-Pocket), 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Military Wearable Medical Device Market Segmentation, By Application

7.2 Heart Monitor

7.2.1 Heart Monitor Market Trends Analysis (2020-2032)

7.2.2 Heart Monitor Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Sick Alert

7.2.3.1 Sick Alert Market Trends Analysis (2020-2032)

7.2.3.2 Sick Alert Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.4 Heart Rate Variability

7.2.4.1 Heart Rate Variability Market Trends Analysis (2020-2032)

7.2.4.2 Heart Rate Variability Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Performance Monitor

7.3.1 Performance Monitor Market Trends Analysis (2020-2032)

7.3.2 Performance Monitor Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.3 Sleep-wake Cycle Alert

7.3.3.1 Sleep-wake Cycle Alert Market Trends Analysis (2020-2032)

7.3.3.2 Sleep-wake Cycle Alert Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.4 Core Body Temperature Monitoring

7.3.4.1 Core Body Temperature Monitoring Market Trends Analysis (2020-2032)

7.3.4.2 Core Body Temperature Monitoring Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Regional Analysis

8.1 Chapter Overview

8.2 North America

8.2.1 Trends Analysis

8.2.2 North America Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.2.3 North America Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.2.2 USA

8.2.2.1 USA Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.2.3 Canada

8.2.3.1 Canada Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.2.4 Mexico

8.2.4.1 Mexico Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3 Europe

8.3.1 Eastern Europe

8.3.1.1 Trends Analysis

8.3.1.2 Eastern Europe Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.3.1.3 Eastern Europe Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.1.4 Poland

8.3.1.4.1 Poland Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.1.5 Romania

8.3.1.5.1 Romania Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.1.6 Hungary

10.3.1.8.1 Hungary Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.1.7 Turkey

8.3.1.7.1 Turkey Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.1.8 Rest of Eastern Europe

8.3.1.8.1 Rest of Eastern Europe Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2 Western Europe

8.3.2.1 Trends Analysis

8.3.2.2 Western Europe Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.3.2.3 Western Europe Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.4 Germany

8.3.2.4.1 Germany Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.5 France

8.3.2.5.1 France Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.6 UK

8.3.2.6.1 UK Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.7 Italy

8.3.2.7.1 Italy Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.8 Spain

8.3.2.8.1 Spain Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.9 Netherlands

8.3.2.9.1 Netherlands Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.10 Switzerland

8.3.2.10.1 Switzerland Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.11 Austria

8.3.2.11.1 Austria Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.3.2.12 Rest of Western Europe

8.3.2.12.1 Rest of Western Europe Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4 Asia Pacific

8.4.1 Trends Analysis

8.4.2 Asia Pacific Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.4.3 Asia Pacific Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.4 China

8.4.4.1 China Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.5 India

8.4.5.1 India Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.6 Japan

8.4.6.1 Japan Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.7 South Korea

8.4.7.1 South Korea Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.8 Vietnam

8.4.8.1 Vietnam Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.9 Singapore

8.4.9.1 Singapore Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.10 Australia

8.4.10.1 Australia Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.4.11 Rest of Asia Pacific

8.4.11.1 Rest of Asia Pacific Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5 Middle East and Africa

8.5.1 Middle East

8.5.1.1 Trends Analysis

8.5.1.2 Middle East Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.1.4 UAE

8.5.1.4.1 UAE Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.1.5 Egypt

8.5.1.5.1 Egypt Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.1.6 Saudi Arabia

8.5.1.6.1 Saudi Arabia Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.1.7 Qatar

8.5.1.7.1 Qatar Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.1.8 Rest of Middle East

8.5.1.8.1 Rest of Middle East Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.2 Africa

8.5.2.1 Trends Analysis

8.5.2.2 Africa Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.5.2.3 Africa Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.2.4 South Africa

8.5.2.4.1 South Africa Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.2.5 Nigeria

8.5.2.5.1 Nigeria Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.5.2.6 Rest of Africa

8.5.2.6.1 Rest of Africa Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.6 Latin America

8.6.1 Trends Analysis

8.6.2 Latin America Military Wearable Medical Device Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

8.6.3 Latin America Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.6.4 Brazil

8.6.4.1 Brazil Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.6.5 Argentina

8.6.5.1 Argentina Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.6.6 Colombia

8.6.6.1 Colombia Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

8.6.7 Rest of Latin America

8.6.7.1 Rest of Latin America Military Wearable Medical Device Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9. Company Profiles

9.1 Bittium

9.1.1 Company Overview

9.1.2 Financial

9.1.3 Products/ Services Offered

9.1.4 SWOT Analysis

9.2 Polar Electro

9.2.1 Company Overview

9.2.2 Financial

9.2.3 Products/ Services Offered

9.2.4 SWOT Analysis

9.3 Oura

9.3.1 Company Overview

9.3.2 Financial

9.3.3 Products/ Services Offered

9.3.4 SWOT Analysis

9.4 Garmin

9.4.1 Company Overview

9.4.2 Financial

9.4.3 Products/ Services Offered

9.4.4 SWOT Analysis

9.5 NeuroMetrix

9.5.1 Company Overview

9.5.2 Financial

9.5.3 Products/ Services Offered

9.5.4 SWOT Analysis

9.6 GOQii

9.6.1 Company Overview

9.6.2 Financial

9.6.3 Products/ Services Offered

9.6.4 SWOT Analysis

9.7 Apple Inc.

9.7.1 Company Overview

9.7.2 Financial

9.7.3 Products/ Services Offered

9.7.4 SWOT Analysis

9.8 Samsung

9.8.1 Company Overview

9.8.2 Financial

9.8.3 Products/ Services Offered

9.8.4 SWOT Analysis

9.9 Fitbit

9.9.1 Company Overview

9.9.2 Financial

9.9.3 Products/ Services Offered

9.9.4 SWOT Analysis

9.10 Zephyr Technology Corporation

9.10.1 Company Overview

9.10.2 Financial

9.10.3 Products/ Services Offered

9.10.4 SWOT Analysis

10. Use Cases and Best Practices

11. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Application

Heart Monitor

Sick Alert

Heart Rate Variability

Performance Monitor

Sleep-wake Cycle Alert

Core Body Temperature Monitoring

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The 3D Printed Prosthetics Market Size was valued at USD 1.51 Billion in 2023 and is expected to reach USD 2.97 Billion by 2032, growing at a CAGR of 7.84% over the forecast period 2024-2032.

The Augmented and Virtual Reality Contact Lenses Market size was valued at USD 21.60 Million in 2023 and is expected to grow to USD 71.80 Million by 2031 and grow at a CAGR of 16.2 % over the forecast period of 2024-2031.

The Robotic Nurse Assistant Market Size was USD 1.27 Billion in 2023 and will reach USD 4.55 Billion by 2032 and grow at a CAGR of 15.27% by 2024-2032

Metastatic Lung Adenocarcinoma Treatment Market was valued at USD 4.35 billion in 2023 and is expected to reach USD 11.58 billion by 2032, growing at a CAGR of 11.54% from 2024-2032.

The Dental Prosthetics Market size was valued at USD 10.5 Billion in 2023 & is estimated to reach USD 21.16 Billion by 2032 and increase at a compound annual growth rate of 8.1% between 2024 and 2032.

The Research Antibodies Market Size was valued at USD 1.4 billion in 2023 and expected to reach USD 2.3 billion by 2032 and grow at a CAGR of 5.5%.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd