Medication Management Market Report Scope & Overview:

Get more information on Medication Management Market - Request Sample Report

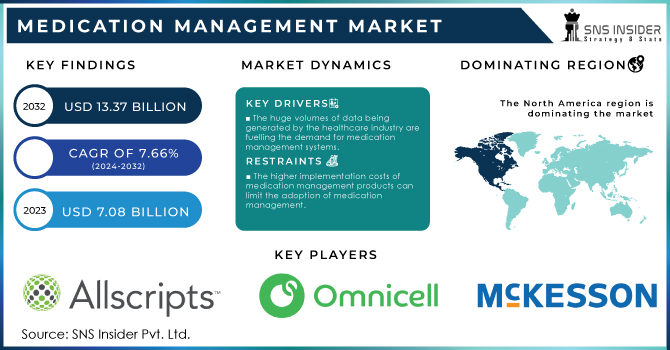

The Medication Management Market Size was valued at USD 7.08 Billion in 2023 and is expected to reach USD 13.37 Billion by 2032 and grow at a CAGR of 7.66% over the forecast period 2024-2032.

The growing need to reduce medication errors and the increasing number of prescriptions worldwide are key drivers for the growth of the medication management market. The main drivers are an increasing adoption of IT in healthcare, rising workloads, and workflow management systems that were adopted by pharmacists as automation solutions to manage their increased workload therefore driving the medication management system market while pushing from hospitals side to purchase new software for better efficiency during health care processes will steer its growth.

An increasing number of prescriptions at the global level is anticipated to drive the demand for medication management solutions in healthcare facilities. A report by the U.S. Department of Health and Human Services found that there were 4.76 billion prescription fills in the U.S. in the year 2022 up from 4.69 billion in 2021. Similarly, the American College of Clinical Pharmacy has stated that 4.83 billion prescriptions are to be filled in 2023. An increase in prescriptions also means more work for pharmacists and therefore will contribute to the rise of automated solutions that help manage workflows.

MARKET DYNAMICS:

KEY DRIVERS:

- The huge volumes of data being generated by the healthcare industry are fuelling the demand for medication management systems.

- Rising clinical trials are raising the demand for medication management systems propelling the market growth.

RESTRAINTS:

- Lack of awareness and infrastructure in developing countries regarding medication management systems are hindering market growth.

- The higher implementation costs of medication management products can limit the adoption of medication management.

OPPORTUNITY:

- Rising government focus on clinical research is offering a lucrative growth opportunity for medication management systems.

- Investment in R&D is responsible for the medication management system market growth during upcoming years.

KEY MARKET SEGMENTATION:

By Type

-

Software

-

Computerized Physician Order Entry

-

Clinical Decision Support System Solutions

-

Electronic Medication Administration Record

-

Inventory Management Solutions

-

Others

-

-

Services

-

Medication Analytics

-

Point-of-Care Verification

-

ADE Surveillance

-

By Mode of Delivery

-

On-Premise Solutions

-

Web-Based Solutions

-

Cloud-Based Solutions

Cloud-based solution was the largest market and held a 60.01% share of the overall revenue in 2023. Players are working on features such as cloud-based deployment to make it easy for the sharing of specific knowledge with clients and other stakeholders. Commercial cloud solutions, which make information readily retrievable from remote locations thanks to these advancements are expected to have mass acceptance in the coming years. Besides, the growing concern about patient data security and the implementation of regulations regarding it could be expected to strengthen the Manufacturer's Business in coming years.

Cloud technology is being adopted at a pretty much faster rate due to many of the security gaps seen across on-premises and web-based deployment. Some solutions cover all the risks and provide warranties against data losses and thefts available from cloud service providers. This is why this segment constitutes a major slice of the pie. Online-based solutions accounted for the second-largest share of the Medication management systems market in 2023. This is owing to the higher adoption of web-based technologies by physicians as these are more cost-effective than cloud-based ones.

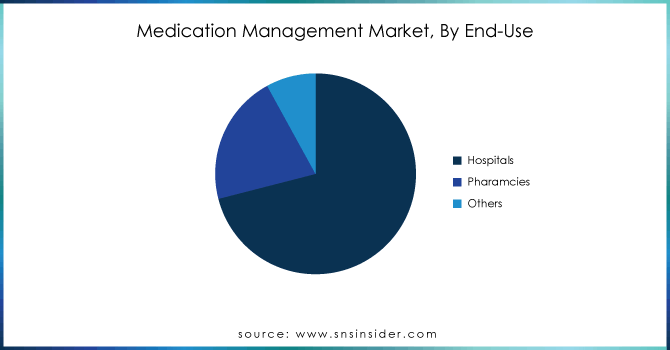

By End Use

-

Hospitals

-

Pharmacies

-

Others

The hospital's segment occupied 70.8% share of the total revenue generated in 2023 and the hospital is one of the largest end-users for IT solutions. Over the past few years, hospitals have spent billions of dollars in buying and upgrading their IT systems. With an emphasis on workflow efficiency, safe dispensing of medications, and a more streamlined clinical process. As a result of which, hospitals have attracted the most market share because they resort to such practices.

The pharmacy segment dominates the market as IT solutions are extensively used in pharmacies and are anticipated to grow at a CAGR of 11.10% over the forecast period Growing burden of prescriptions and limited pharmacists are some factors that have increased the demand for medication management solutions in pharmacies.

Solutions such as robotics in pharmacies are expected to reduce the workload of pharmacists and help manage prescriptions for patients more effectively. However, the growing prevalence of chronic and infectious diseases is expected to expand prescription volumes filled by pharmacies. This is expected to drive the demand for autonomous management solutions. Hospitals are driving the market, looking to streamline workflow efficiency and simplification of a plethora of complex clinical processes. Impact on pharmacies as chronic and infectious diseases increase along with the rise in prescriptions dispensed.

Need any customization research on Medication Management Market - Enquiry Now

REGIONAL ANALYSIS

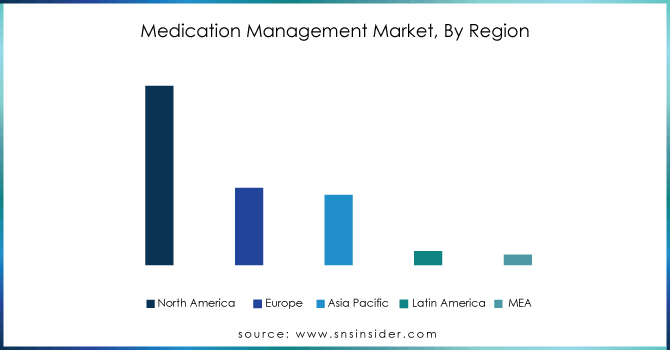

North America dominates the medication management market in the base year 2023, majorly because of rapid development in the IT sector and healthy adoption from the healthcare sector thus propelling the regional overall revenues also fuelled due to infections & chronic diseases. Precancerous or malignant colorectal abnormalities can be detected and removed before cancer develops, but endoscopy numbers have not kept pace with the increase in CRC incidence.

This is because of the new technology awareness that was high, many smaller players who had medication management solutions to hospitals and pharmacies widely available but there was a shortage of primary care physicians. For example, in March 2022, Hamilton Beach Brands Inc. and HealthBeacon plc launched the Smart Sharps Bin Injection Care Management System in the US. The Smart Sharps Bin; is a digitally connected, innovative life science tools medication management device with key features: smart reminders for your daily medications tracking of injection adherence live 24/7 customer support including safe and convenient used syringe disposal via USPS-approved mail-back program. This trend is expected to further drive the market for medication management systems in North America, with product launches of such products across the region on verticals.

The increasing healthcare expenditure in the region is also expected further to accelerate the market growth in this regional segment. For example, as of November 2021, the projected total collective health spending in Canada was expected to reach CDN$308 billion for the year 2021 - more than an estimated portion amounting to almost 12.7% percent of GDP (CIHI). Hence, based on these elements, North America is projected to register significant growth in the medication management systems market over the forecast period.

REGIONAL COVERAGE:

-

North America

-

US

-

Canada

-

Mexico

-

-

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

-

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

-

-

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

-

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

-

KEY PLAYERS:

The key market players include A-S Medication Solutions (Allscripts Healthcare Solutions Inc.), Omnicell, Inc., ARxIUM, McKesson Corporation, Becton, Dickinson and Company, Talyst, LLC (Psychiatric Solutions, Inc.), Cerner Corporation, BIQHS, GE Healthcare (General Electric Company), NEXUS AG and Other Players. The market is fragmented and competitive and has many players operating in the market. The market is majorly focusing on mergers and acquisitions, and issuance of solutions that are customized for expansion into the unexplored commercial markets. On the other hand, as a part of their commercialization strategy companies are putting a significant amount of money into building new products and platforms richer with newer features.

RECENT DEVELOPMENTS

- In October 2022, Omnicell, Inc. launched Specialty Pharmacy Services which provides a complete turnkey suite with tailored services rooted in best practices for the operation and growth of specialty pharmacy programs.

- In February 2022, Optum released the first offering on its generation two stack with the announcement of the launch of Optum Specialty Fusion to facilitate integrated patient care for complex conditions at a lower cost due to high-cost specialty drugs.

| Report Attributes | Details |

| Market Size by 2032 | US$ 13.37 Billion |

| CAGR | CAGR of 7.66% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Software & Services) •By Mode Of Delivery (On-premise, Web-based, Cloud-based) •By End-use (Hospitals, Pharmacies & Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | A-S Medication Solutions (Allscripts Healthcare Solutions Inc.), Omnicell, Inc., ARxIUM, McKesson Corporation, Becton, Dickinson and Company, Talyst, LLC (Psychiatric Solutions, Inc.), Cerner Corporation, BIQHS, GE Healthcare (General Electric Company), NEXUS AG among others |

| Key Drivers | •The huge volumes of data being generated by the healthcare industry are fuelling the demand for medication management systems. •Rising clinical trials are raising the demand for medication management systems propelling the market growth. |

| RESTRAINTS | •Lack of Awareness and Infrastructure in Developing Countries regarding medication management systems are hindering the market growth. •The higher implementation costs of Medication Management products can limit the adoption of medication management. |