Get more information on Medical Device Security Market - Request Sample Report

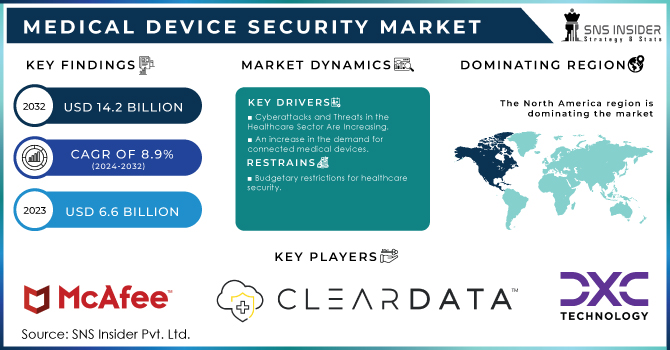

The Medical Device Security Market Size was valued at USD 6.6 billion in 2023 and is expected to reach USD 14.2 billion by 2032 and grow at a CAGR of 8.9% over the forecast period 2024-2032.

The Medical Device Security market has strong growth prospects due to increased growth of connected medical devices and awareness of cybersecurity risks in health care. Internet of Medical Things (IoMT) devices have made their way into hospitals and other healthcare organizations; more importantly, they necessitate adequately robust security measures. The proliferation of life-sustaining medical appliances such as infusion pumps, patient monitors, and imaging systems creates increased attack surfaces for cybercriminals, who would find healthcare facilities an attractive target for cyber-attacks. It thus requires effective medical device security solutions to ensure sensitive patient information is protected for uninterrupted care.

The rising reported cases of cyber incidents that damage healthcare organizations further fuel market demand. A Ponemon study indicates that 50% of the attacked organizations reported attacks in their supply chains, leading to care disruptions and worse health outcomes. Healthcare organizations, therefore, are committing to security in the area of cybersecurity to enhance their chances of countering cyber threats as demand for security products and services advances.

Supply-side factors have also come to the forefront in shaping the Medical Device Security market. Technological change is coming into the limelight in health care through cloud-based solutions and enhanced data analytics capabilities. Such advancements allow healthcare providers to implement strong security controls, such as real-time monitoring and assessment of vulnerabilities in connecting medical devices to avoid hacking. In addition, because of regulatory guidelines such as the FDA's guidelines and HIPAA, manufacturers and healthcare organizations are forced to invest highly in the cybersecurity of their operations. Due to this, there is increased demand for security solutions based on regulatory compliance.

The increase in cybersecurity threats, regulatory pressure, and growth in the adoption of connected medical devices are creating a very robust demand-supply dynamic in the Medical Device Security market. As an organization recognizes the critical importance of protecting medical devices from cyber risks, the market is likely to expand rapidly. It will then open doors for innovative security solutions as and when the healthcare sector develops future needs.

TABLE: Products and Players in Medical Device Security

| Product Category | Example Products | Key Players & Offerings |

|---|---|---|

| Network Security Solutions | Firewalls, Intrusion Detection Systems (IDS) | Palo Alto Networks, Fortinet, Cisco Systems (Comprehensive Network Security Solutions) |

| Endpoint Security Solutions | Antivirus Software, Device Management Systems | Symantec, Sophos, McAfee (Endpoint Protection for Medical Devices) |

| Application Security Tools | Web Application Firewalls (WAF), Secure SDLC Tools | Check Point Software Technologies, Imperva (Advanced Application Protection Tools) |

| Data Encryption Solutions | AES Encryption Tools, Secure Messaging Applications | IBM, CA Technologies, Cisco Systems (Data Protection and Encryption Solutions) |

| Security Assessment Tools | Vulnerability Scanners, Risk Assessment Software | ClearDATA, DXC Technology, Qualys (Risk Management & Security Assessments) |

| Cloud Security Solutions | Cloud Security Monitoring, Encryption, and Firewalls | ClearDATA, CloudPassage, FireEye (Cloud Protection Services for Medical Devices) |

| Incident Response Services | Managed Security Services, Incident Management Software | FireEye, IBM, Sophos (Comprehensive Incident Response Tools and Services) |

Drivers

Demand For Connected Medical Devices with Increased Awareness of Cybersecurity Vulnerabilities

The demand for connected medical devices in the healthcare industry is one of the leading factors. The rationale behind the surge in demand for such devices is that immediate monitoring and collection of data regarding patients can be ensured via them. So, the total security solutions that not only protect sensitive information but also ensure the integrity of the devices increase with healthcare providers' dependence on such IoT-oriented devices. An increased awareness of cybersecurity vulnerabilities through cyberattacks on telemedicine platforms has also reflected increased investment in healthcare organizations. High-profile cases have underlined the consequences of poor security measures regarding unauthorized access to an individual's health information and disruption of patient care services. Regulatory pressures also emphasize the need for having tight security mechanisms in place. Policies from companies like the FDA push manufacturers and healthcare providers to deploy proactive security measures, which drives the expansion of the market. The above factors together lead to positive demand for connectivity devices, cyber threats, and regulatory compliance, creating a dynamic environment that encourages innovation and expansion within the medical device security market. With the rapidly changing healthcare environment, addressing cyber risk challenges will form the primary basis for ensuring patient safety and the reliability of medical technologies.

Restraints

High Implementation Costs

Complexity of Integration

| Segment | Dominant Segment (2023) | Fastest Growing Segment (CAGR) | Key Players & Offerings |

|---|---|---|---|

| by Component | Solutions | Services | Cisco Systems (Firewalls, IDS), IBM (Data Encryption, Security Assessments), Palo Alto Networks (Network Security) |

| by Type | Application Security | Cloud Security | Check Point Software Technologies (Web Application Firewalls), Imperva (Application Security), Fortinet (Network Security Solutions) |

| by Device Type | Hospital Medical Devices | Wearable and External Medical Devices | GE Healthcare (Medical Device Solutions), Philips Healthcare (Hospital Devices Security), Medtronic (Device Security Integration) |

| by End User | Healthcare Providers | Medical Device Manufacturers | Siemens Healthineers (Device Security Solutions), Abbott Laboratories (IoT Device Security), Johnson & Johnson (Medical Device Protection) |

by Component

In 2023, solutions emerged as the dominant segment with a 54.2% share in the medical device security market, capturing a significant market share due to their essential role in protecting connected medical devices. This segment encompasses a wide array of security solutions, including antivirus software, intrusion detection systems, and encryption technologies. The increasing reliance of healthcare providers on IoT-oriented devices has underscored the necessity for robust security measures to safeguard sensitive patient data. As high-profile cyberattacks on healthcare institutions continue to make headlines, organizations are prioritizing investments in comprehensive security solutions. The robust demand for these solutions is expected to persist as healthcare facilities seek to enhance their cybersecurity frameworks and comply with stringent regulations.

The services segment is the fastest-growing area within the medical device security market, driven by the increasing complexity of healthcare environments and the need for specialized expertise. This segment includes consulting, managed security services, and incident response solutions tailored to meet the unique security needs of healthcare organizations.

by Type

In 2023, application security was the dominant segment with a 38.6% share of the medical device security market, reflecting the increasing reliance on software applications within healthcare settings. With the growing use of telemedicine and health management applications, the need for robust application security measures has become paramount. Healthcare providers are investing significantly in ensuring that the applications used in medical devices are secure, protecting them from vulnerabilities that could be exploited by cybercriminals. Regulatory requirements and the need for secure handling of patient data are driving this demand. As the healthcare landscape continues to evolve, the importance of application security will remain a priority, solidifying its position as a market leader.

Endpoint security is rapidly emerging as the fastest-growing segment within the medical device security market, driven by the proliferation of connected devices in healthcare environments. As healthcare organizations increasingly adopt remote patient monitoring and telehealth services, the number of endpoints has surged, highlighting the urgent need for comprehensive security solutions to protect these devices.

by Device Type

Hospital medical devices represented the largest segment with a 41.6% share in the medical device security market in 2023, driven by their critical role in patient care and the increasing connectivity of these devices. Devices such as imaging systems, surgical instruments, and patient monitoring equipment are essential to hospital operations and are increasingly integrated with hospital networks. The growing focus on patient safety, coupled with regulatory pressures to secure these devices, has prompted healthcare facilities to prioritize their cybersecurity measures. As hospitals continue to adopt advanced technologies, the demand for tailored security solutions to protect these medical devices is expected to sustain this segment's dominance.

The wearable and external medical devices segment is experiencing rapid growth over the forecast period, fueled by the increasing trend toward personalized healthcare and health monitoring. Devices such as fitness trackers, smartwatches, and portable monitoring devices are becoming more prevalent as consumers seek to manage their health proactively.

by End User

Healthcare providers dominated the medical device security market in 2023 with a 39.5% share, as they are the primary users of connected medical devices. Hospitals and clinics are increasingly prioritizing cybersecurity to safeguard patient data and ensure compliance with evolving regulations. The rise in cyberattacks targeting healthcare institutions has heightened awareness of security vulnerabilities, leading to significant investments in comprehensive security solutions. As healthcare providers recognize the critical importance of securing their connected devices, the demand for tailored security measures will remain strong, sustaining their dominance in the market.

Healthcare payers, including insurance companies and government health programs, are rapidly emerging as the fastest-growing segment in the medical device security market over the forecast period. As these organizations increasingly engage with connected healthcare technologies and face rising concerns regarding data security and compliance, they are prioritizing investments in security solutions to protect sensitive patient information.

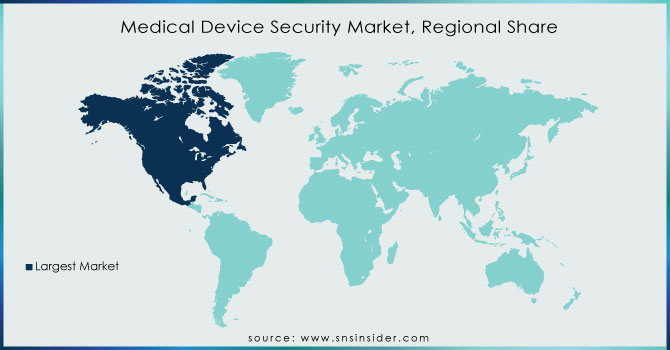

The medical device security market for North America had the highest share with 45.5% because of massive cyberattacks against medical devices, high adoption of connected medical technologies, and increasing awareness of cybersecurity amongst healthcare professionals. It is further supported by the government initiatives put in place in this region to introduce far-reaching security solutions into the health sector. The presence of these factors together provides North America with the most prominent position in the sector of medical device security.

Asia Pacific is likely to witness the highest compound annual growth rate (CAGR) during the forecast period. Several key factors such as increasing adoption of connected medical devices, growth in healthcare infrastructure, and rising awareness about PHI preservation would fuel this high growth rate. Increasing concern and incidents about cyberattacks on medical devices have increased the demand for effective solutions associated with medical device security. Consequently, the growing demand for security-related solutions for medical device security has, in turn, boosted the market for medical device security in the Asia Pacific region.

Need any customization research on Medical Device Security Market - Enquiry Now

Key Players

Check Point Software Technologies

Palo Alto Networks

IBM

GE Healthcare

Fortinet

Symantec

CA Technologies

Philips

DXC Technology

CloudPassage

FireEye

Sophos, and others.

Recent Developments

In December 2023, Cisco, a leader in enterprise networking and security, announced the Cisco AI Assistant for Security. This is an important step toward embedding AI much more broadly throughout Cisco's Security Cloud: a unified, AI-infused, cross-domain security platform. This AI assistant is to support customers in decision-making, improve their tools, and automate complex security tasks.

In July 2023, Cynerio and Check Point Software Technologies announced that they have formed a strategic partnership to bring comprehensive security solutions for the medical IoT devices of healthcare organizations. The 360 platform of Cynerio provides necessary features for securing IoT healthcare devices, such as device discovery, patch guidance, micro-segmentation, and attack detection.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 6.6 Billion |

| Market Size by 2032 | USD 14.2 Billion |

| CAGR | CAGR of 8.9% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Type (Application Security, Endpoint Security, Network Security, Cloud Security) • By Device Type (Hospital Medical Devices, Internally Embedded Medical Devices, Wearable and External Medical Devices) • By End User (Healthcare Providers, Medical Device Manufacturers, Healthcare Payers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia-Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia-Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Check Point Software Technologies, Palo Alto Networks, ClearDATA, Cisco Systems, IBM, GE Healthcare, Imperva, Fortinet, Symantec, CA Technologies, Philips, DXC Technology, CloudPassage, FireEye, Sophos, and Others |

| Key Drivers | • Demand For Connected Medical Devices with Increased Awareness of Cybersecurity Vulnerabilities |

| Restraints | • High Implementation Costs • Complexity of Integration |

Ans:The Medical Device Security Market Size was valued at USD 6.6 billion in 2023.

Ans: The Medical Device Security Market is to grow at a CAGR of 8.9% over the forecast period 2024-2032.

The need to agree with unofficial laws, and an increase in the demand for connected medical devices are all propelling the Medical Device Security market forward.

Asia-Pacific is anticipated to have considerable growth during the projected period due to the increase in connected medical device use in hospitals and increased awareness of medical device security solutions in Asia-developing Pacific's countries.

Mcafee, LLC, Clear data, DXC Technology Company, Check Point Software Technologies Ltd., Palo Alto Networks, Cisco Systems, Inc., are the key players of the Medical Device Security Market.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates, 2023

5.2 User Demographics, by User Type and Roles, 2023

5.3 Feature Analysis, by Feature Type

5.4 Cost Analysis, by Software

5.5 Integration Capabilities

5.6 Regulatory Compliance, by Region

6. Competitive Landscape

6.1 List of Major Companies, by Region

6.2 Market Share Analysis, by Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Medical Device Security Market Segmentation, by Component

7.1 Chapter Overview

7.2 Solutions

7.2.1 Solutions Market Trends Analysis (2020-2032)

7.2.2 Solutions Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 Services

7.3.1 Services Market Trends Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Million)

8. Medical Device Security Market Segmentation, by Type

8.1 Chapter Overview

8.2 Application Security

8.2.1 Application Security Market Trends Analysis (2020-2032)

8.2.2 Application Security Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Endpoint Security

8.3.1 Endpoint Security Market Trends Analysis (2020-2032)

8.3.2 Endpoint Security Market Size Estimates And Forecasts To 2032 (USD Million)

8.4 Network Security

8.4.1 Network Security Market Trends Analysis (2020-2032)

8.4.2 Network Security Market Size Estimates And Forecasts To 2032 (USD Million)

8.5 Cloud Security

8.5.1 Cloud Security Market Trends Analysis (2020-2032)

8.5.2 Cloud Security Market Size Estimates And Forecasts To 2032 (USD Million)

9. Medical Device Security Market Segmentation, by Device Type

9.1 Chapter Overview

9.2 Hospital Medical Devices

9.2.1 Hospital Medical Devices Market Trends Analysis (2020-2032)

9.2.2 Hospital Medical Devices Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Internally Embedded Medical Devices

9.3.1 Internally Embedded Medical Devices Market Trends Analysis (2020-2032)

9.3.2 Internally Embedded Medical Devices Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Wearable and External Medical Devices

9.4.1 Wearable and External Medical Devices Market Trends Analysis (2020-2032)

9.4.2 Wearable and External Medical Devices Market Size Estimates and Forecasts to 2032 (USD Million)

10. Medical Device Security Market Segmentation, by End User

10.1 Chapter Overview

10.2 Healthcare Providers

10.2.1 Healthcare Providers Market Trends Analysis (2020-2032)

10.2.2 Healthcare Providers Market Size Estimates and Forecasts to 2032 (USD Million)

10.3 Medical Device Manufacturers

10.3.1 Medical Device Manufacturers Market Trends Analysis (2020-2032)

10.3.2 Medical Device Manufacturers Market Size Estimates and Forecasts to 2032 (USD Million)

10.4 Healthcare Payers

10.4.1 Healthcare Payers Market Trends Analysis (2020-2032)

10.4.2 Healthcare Payers Market Size Estimates and Forecasts to 2032 (USD Million)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.2.3 North America Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.2.4 North America Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.5 North America Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.2.6 North America Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.2.7 USA

11.2.7.1 USA Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.2.7.2 USA Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.7.3 USA Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.2.7.4 USA Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.2.8 Canada

11.2.8.1 Canada Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.2.8.2 Canada Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.8.3 Canada Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.2.8.4 Canada Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.2.9 Mexico

11.2.9.1 Mexico Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.2.9.2 Mexico Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.2.9.3 Mexico Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.2.9.4 Mexico Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.1.3 Eastern Europe Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.4 Eastern Europe Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.5 Eastern Europe Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.6 Eastern Europe Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.3.1.7 Poland

11.3.1.7.1 Poland Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.7.2 Poland Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.7.3 Poland Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.7.4 Poland Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.3.1.8 Romania

11.3.1.8.1 Romania Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.8.2 Romania Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.8.3 Romania Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.8.4 Romania Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.9.2 Hungary Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.9.3 Hungary Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.9.4 Hungary Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.10.2 Turkey Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.10.3 Turkey Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.10.4 Turkey Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.1.11.2 Rest of Eastern Europe Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.1.11.3 Rest of Eastern Europe Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.1.11.4 Rest of Eastern Europe Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.3.2.3 Western Europe Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.4 Western Europe Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.5 Western Europe Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.6 Western Europe Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.7 Germany

11.3.2.7.1 Germany Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.7.2 Germany Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.7.3 Germany Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.7.4 Germany Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.8 France

11.3.2.8.1 France Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.8.2 France Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.8.3 France Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.8.4 France Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.9 UK

11.3.2.9.1 UK Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.9.2 UK Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.9.3 UK Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.9.4 UK Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.10 Italy

11.3.2.10.1 Italy Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.10.2 Italy Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.10.3 Italy Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.10.4 Italy Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.11 Spain

11.3.2.11.1 Spain Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.11.2 Spain Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.11.3 Spain Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.11.4 Spain Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.12.2 Netherlands Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.12.3 Netherlands Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.12.4 Netherlands Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.13.2 Switzerland Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.13.3 Switzerland Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.13.4 Switzerland Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.14 Austria

11.3.2.14.1 Austria Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.14.2 Austria Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.14.3 Austria Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.14.4 Austria Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.3.2.15.2 Rest of Western Europe Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.3.2.15.3 Rest of Western Europe Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.3.2.15.4 Rest of Western Europe Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.4.3 Asia Pacific Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.4 Asia Pacific Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.5 Asia Pacific Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.6 Asia Pacific Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.7 China

11.4.7.1 China Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.7.2 China Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.7.3 China Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.7.4 China Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.8 India

11.4.8.1 India Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.8.2 India Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.8.3 India Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.8.4 India Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.9 Japan

11.4.9.1 Japan Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.9.2 Japan Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.9.3 Japan Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.9.4 Japan Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.10 South Korea

11.4.10.1 South Korea Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.10.2 South Korea Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.10.3 South Korea Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.10.4 South Korea Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.11 Vietnam

11.4.11.1 Vietnam Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.11.2 Vietnam Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.11.3 Vietnam Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.11.4 Vietnam Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.12 Singapore

11.4.12.1 Singapore Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.12.2 Singapore Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.12.3 Singapore Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.12.4 Singapore Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.13 Australia

11.4.13.1 Australia Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.13.2 Australia Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.13.3 Australia Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.13.4 Australia Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.4.14.2 Rest of Asia Pacific Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.4.14.3 Rest of Asia Pacific Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.4.14.4 Rest of Asia Pacific Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.1.3 Middle East Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.4 Middle East Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.5 Middle East Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.6 Middle East Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.1.7 UAE

11.5.1.7.1 UAE Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.7.2 UAE Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.7.3 UAE Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.7.4 UAE Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.8.2 Egypt Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.8.3 Egypt Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.8.4 Egypt Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.9.2 Saudi Arabia Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.9.3 Saudi Arabia Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.9.4 Saudi Arabia Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.10.2 Qatar Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.10.3 Qatar Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.10.4 Qatar Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.1.11.2 Rest of Middle East Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.1.11.3 Rest of Middle East Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.1.11.4 Rest of Middle East Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.5.2.3 Africa Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.2.4 Africa Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.5 Africa Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.2.6 Africa Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.2.7.2 South Africa Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.7.3 South Africa Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.2.7.4 South Africa Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.2.8.2 Nigeria Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.8.3 Nigeria Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.2.8.4 Nigeria Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.5.2.9.2 Rest of Africa Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.5.2.9.3 Rest of Africa Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.5.2.9.4 Rest of Africa Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Medical Device Security Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

11.6.3 Latin America Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.6.4 Latin America Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.5 Latin America Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.6.6 Latin America Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.6.7 Brazil

11.6.7.1 Brazil Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.6.7.2 Brazil Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.7.3 Brazil Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.6.7.4 Brazil Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.6.8 Argentina

11.6.8.1 Argentina Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.6.8.2 Argentina Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.8.3 Argentina Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.6.8.4 Argentina Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.6.9 Colombia

11.6.9.1 Colombia Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.6.9.2 Colombia Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.9.3 Colombia Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.6.9.4 Colombia Medical Device Security Market Estimates and Forecasts, by End User(2020-2032) (USD Million)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Medical Device Security Market Estimates and Forecasts, by Component (2020-2032) (USD Million)

11.6.10.2 Rest of Latin America Medical Device Security Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

11.6.10.3 Rest of Latin America Medical Device Security Market Estimates and Forecasts, by Device Type (2020-2032) (USD Million)

11.6.10.4 Rest of Latin America Medical Device Security Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

12. Company Profiles

12.1 Check Point Software Technologies

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Palo Alto Networks

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 ClearDATA

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Cisco Systems

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 GE Healthcare

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Imperva

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 CA Technologies

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 DXC Technology

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 CloudPassage

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Philips

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segmentation

By Component

Solutions

Services

By Type

Application Security

Endpoint Security

Network Security

Cloud Security

By Device Type

Hospital Medical Devices

Internally Embedded Medical Devices

Wearable and External Medical Devices

By End User

Healthcare Providers

Medical Device Manufacturers

Healthcare Payers

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Image-guided Biopsy market size was USD 4.01 billion in 2023 and is expected to reach USD 6.98 billion by 2032 and grow at a CAGR of 6.35% over the forecast period of 2024-2032.

The Benign Prostatic Hyperplasia (BPH) Treatment Market Size was valued at USD 1.57 billion in 2023 and is expected to reach USD 3.38 billion by 2032 and grow at a CAGR of 8.92% over the forecast period 2024-2032.

The Parkinson’s Disease Treatment Market size was valued at USD 2.50 Billion in 2023 and is expected to reach USD 3.71 Billion by 2032 and grow at a CAGR of 4.53% over the forecast period 2024-2032.

The Medical Electrodes Market was valued at USD 2.07 billion in 2023 and is expected to reach USD 3.17 billion by 2032, growing at a CAGR of 4.89% from 2024 to 2032.

The Exosomes Market Size was valued at USD 136.16 Million in 2023 and is expected to reach USD 1,311.03 Million by 2032, growing at a CAGR of 28.62% over the forecast period of 2024-2032.

The Bio Detectors and Accessories Market was valued at USD 16.9 Billion in 2023 and is projected to hit USD 52.9 Billion by 2032, growing at a CAGR of 13.5%.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd