Medical Device Connectivity Market Size & Overview:

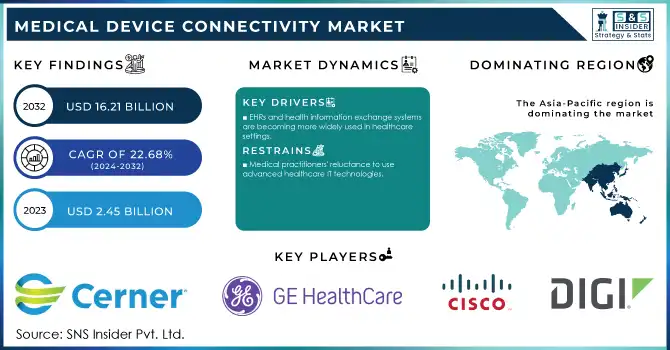

The Medical Device Connectivity Market was valued at USD 2.45 billion in 2023 and is expected to reach USD 16.21 billion by 2032 and grow at a CAGR of 22.68% over the forecast period of 2024-2032.

Get more information on Medical Device Connectivity Market - Request Sample Report

The Medical Device Connectivity Market is experiencing significant growth, fueled by the increasing demand for integrated healthcare solutions, the rise of chronic diseases, and technological advancements in digital health. According to a report by the Healthcare Information and Management Systems Society, over 80% of healthcare organizations have begun adopting connected medical devices in some capacity, demonstrating the sector’s growing reliance on connectivity. These technologies enable medical devices to interface with healthcare systems like Electronic Health Records and cloud platforms, allowing for real-time data collection, analysis, and patient monitoring. By ensuring that healthcare providers have immediate access to patient data, these solutions improve patient outcomes, streamline workflows, and reduce costs.

A major driver of this market is the increasing prevalence of chronic diseases. For instance, the World Health Organization reports that chronic diseases account for 71% of all deaths globally, with conditions such as diabetes, cardiovascular diseases, and respiratory disorders requiring ongoing monitoring. Connected medical devices, such as continuous glucose monitors and wearable ECG monitors, allow for consistent tracking of vital health metrics, reducing the need for in-person visits. A study by the American Heart Association found that remote patient monitoring devices can reduce hospital readmissions by up to 30% in patients with chronic heart conditions.

Telemedicine adoption, especially post-pandemic, is another key factor driving this market. According to the U.S. Department of Health and Human Services, telehealth utilization increased by 154% in 2020 compared to pre-pandemic levels. Devices such as smart pulse oximeters, blood pressure monitors, and thermometers enable healthcare professionals to remotely monitor patients, offering convenient care options while ensuring that data is captured accurately and promptly. For example, Philips’ IntelliVue patient monitoring system connects multiple medical devices to provide continuous real-time data on patient vitals, helping healthcare providers detect changes in conditions before they worsen.

Technological advancements like the integration of Artificial Intelligence, Machine Learning, and the Internet of Things are enhancing the capabilities of connected medical devices. For instance, AI-enabled devices can analyze patient data to predict potential health issues, offering early interventions. The expansion of cloud computing also facilitates secure data storage, making patient information accessible to authorized medical professionals from anywhere, thus improving efficiency and patient care.

Medical Device Connectivity Market Dynamics

Drivers

-

The transition from fee-for-service to value-based care models is a significant driver of the Medical Device Connectivity Market.

This shift emphasizes patient outcomes over volume of care, prompting healthcare providers to seek more efficient, data-driven solutions to enhance patient management. Connected medical devices play a crucial role in this transition by enabling continuous monitoring of patient health, which is particularly beneficial for managing chronic conditions. For example, devices like wearable glucose monitors or blood pressure trackers allow for remote patient monitoring, reducing hospital readmissions and ensuring timely interventions. With real-time data access, healthcare professionals can detect potential health issues early, facilitating proactive treatment. Additionally, by automating data collection, connected devices reduce administrative burdens, leading to lower operational costs for healthcare providers and improving overall care quality.

-

Patient empowerment is one of the main catalysts driving the growth of the Medical Device Connectivity Market.

With rising healthcare costs and a shift toward more personalized care, patients are seeking more control over their health management. The availability of connected devices, such as wearable fitness trackers, smart thermometers, and at-home ECG monitors, empowers patients to actively monitor and manage their health outside of clinical settings. These devices, paired with mobile health apps, offer real-time insights into vital metrics, allowing patients to make informed decisions about their well-being. Moreover, the growing trend of consumer health devices that sync with electronic health records (EHRs) helps patients and providers collaborate more efficiently. This trend is enhancing patient engagement, as individuals are taking proactive steps toward managing chronic conditions, improving treatment adherence, and reducing unnecessary hospital visits.

-

Technological advancements are revolutionizing the Medical Device Connectivity Market, with innovations such as Artificial Intelligence, Internet of Things, and 5G wireless technology leading the way.

These technologies enable connected devices to deliver more precise data and improve clinical decision-making processes. AI and machine learning algorithms embedded in medical devices are capable of analyzing real-time patient data, identifying patterns, and providing predictive insights that assist healthcare professionals in making faster, more accurate diagnoses. IoT allows for seamless integration between medical devices, enabling constant communication and data sharing between devices, healthcare systems, and patients. Furthermore, the roll-out of 5G networks is enhancing connectivity, and providing faster, more reliable data transmission, which is essential for remote monitoring and telemedicine applications. These advancements are ensuring that connected medical devices can operate more effectively, improving both patient outcomes and healthcare delivery efficiency.

Restraints

-

Growing Concern Over Data Security and Privacy

As medical devices become more connected, vast amounts of sensitive patient data are being transmitted and stored across various platforms, increasing the risk of cyberattacks and unauthorized access. This creates significant challenges for healthcare providers and device manufacturers in ensuring the data remains protected and compliant with strict regulations like the Health Insurance Portability and Accountability Act in the U.S. and the General Data Protection Regulation in Europe. Any data breach could lead to severe legal consequences, loss of patient trust, and reputational damage for healthcare organizations. Additionally, integrating multiple devices and platforms further complicates the issue of data privacy, as secure communication between disparate systems is often difficult to maintain. This has led to hesitancy in adopting connected medical devices, particularly in regions with less stringent regulatory frameworks.

Medical Device Connectivity Market Segmentation Analysis

By Product & Services

Medical Device Connectivity Solutions emerged as the dominant segment in 2023, accounting for over 50% of the market share. These solutions include software platforms and interfaces that facilitate seamless data exchange between devices and healthcare systems, such as Electronic Health Records. The dominance of this segment is attributed to the increasing adoption of EHR systems globally and the demand for interoperable devices that enhance workflow efficiency in hospitals and clinics. Furthermore, these solutions are critical for real-time monitoring and remote patient care, which has seen heightened importance post-pandemic due to the rise of telehealth and remote healthcare delivery.

The Medical Device Connectivity Services segment is projected to register the fastest growth during the forecast period. This segment includes installation, integration, training, and maintenance services, which are essential for the successful deployment of connectivity solutions. The increasing complexity of medical device ecosystems and the need for technical expertise to ensure seamless integration are driving the demand for these services. Additionally, as more healthcare providers adopt advanced connectivity solutions, the reliance on ongoing maintenance and upgrades further fuels this segment's rapid growth.

By Technology

Wireless technologies dominated the market in 2023, holding 55% of the market share. The growth of this segment is driven by This segment's growth in wireless connectivity in healthcare settings, which offers greater flexibility and ease of deployment compared to wired alternatives. Wireless technologies enable real-time data transmission, making them ideal for remote patient monitoring and telemedicine applications. The widespread adoption of Wi-Fi, Bluetooth, and other wireless protocols, combined with advancements in 5G technology, further solidified their market dominance.

Hybrid technologies, which combine wired and wireless connectivity, are the fastest-growing segment in the market. These technologies offer the benefits of both systems, including reliability from wired connections and flexibility from wireless ones. Hybrid solutions are particularly appealing in complex healthcare environments, where certain critical systems require stable wired connections while others benefit from wireless mobility. The rising demand for adaptable and secure connectivity solutions in healthcare facilities has been a key driver for this segment’s rapid growth.

Medical Device Connectivity Market Regional Outlook

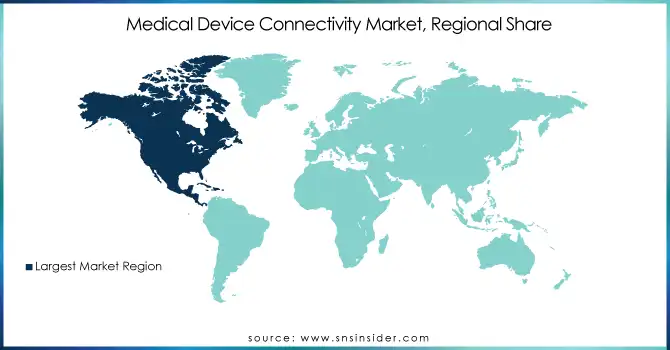

North America maintained its position as the dominant region in 2023. This is largely due to its robust healthcare infrastructure, early adoption of advanced technologies, and supportive government initiatives promoting digital health solutions. The U.S. leads this growth, driven by widespread implementation of electronic health records (EHRs), telehealth services, and a strong presence of key market players. These factors, coupled with significant investments in healthcare IT, have cemented North America’s leadership in the market.

Europe ranked as the second-largest market, with its growth fueled by a patient-centric approach to healthcare and strict regulatory standards. Countries like Germany, the UK, and France are at the forefront of adopting connected medical devices to improve patient outcomes and enhance operational efficiency. The region's emphasis on interoperability and compliance with digital health regulations continues to drive its expansion.

Asia-Pacific, on the other hand, is emerging as the fastest-growing market. The region's rapid digital transformation, rising healthcare expenditure, and increasing prevalence of chronic diseases are key growth drivers. Economies such as China, India, and Japan are experiencing a surge in the adoption of telemedicine, remote patient monitoring, and other connectivity solutions, supported by government initiatives to modernize healthcare systems. The growing awareness of connected technologies and expanding access to healthcare services further amplify Asia-Pacific’s market potential, making it a crucial region for future growth in the industry.

Need any customization research on Medical Device Connectivity Market - Enquiry Now

Medical Device Connectivity Market Companies and Their Product Offerings

-

Baxter International Inc. – Sigma Spectrum Infusion System

-

Iatric Systems Inc. – EasyConnect

-

Silex Technology – SX-570 Wi-Fi Module

-

Digi International Inc. – Digi ConnectPort

-

True Process – Vines Platform

-

Koninklijke Philips N.V. – IntelliBridge Enterprise

-

GE Healthcare – Carescape One

-

Stryker Corporation – Connected OR Solutions

-

iHealth Labs Inc. – iHealth Wireless BP Monitor

-

Cisco Systems – Cisco Healthcare Network

-

Lantronix Inc. – XPort Embedded Device Server

-

TE Connectivity – Medical-grade connectors and Sensors

-

Bridge-Tech Medical – Bridge-Med Device Interface

-

Medicollector LLC – BedMasterEx

-

Oracle Corporation – Oracle Health Data Platform

-

Medtronic plc – CareLink Network

-

Masimo – Masimo Root

-

Infosys – Connected Health Platform

-

S3 Connected Health – Enterprise Connected Health Solutions

-

Spectrum Medical Ltd. – Quantum Perfusion Systems

-

Drägerwerk AG & Co. KGaA – Infinity Acute Care System

-

Honeywell International – Honeywell Smart Sensor

-

Ascom Holdings AG – Digistat Suite

-

Wipro Ltd. – Healthcare IoT Solutions

Recent Developments

In Oct 2024, Glassbeam, Inc., a leader in predictive analytics for connected medical devices, partnered with the Department of Veterans Affairs (VA) Healthcare Technology Management (HTM) program. This collaboration aims to enhance real-time data capabilities and predictive analytics across a broader range of medical systems.

In Sept 2023, Mindray launched the TE Air Wireless Handheld Ultrasound, a groundbreaking compact device designed to enhance ultrasound accessibility. This innovative solution allows healthcare professionals to conduct comprehensive scans on the go, offering seamless connectivity to mobile devices or the TE X Ultrasound System for expanded utility.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 2.45 Billion |

| Market Size by 2032 | US$ 16.21 Billion |

| CAGR | CAGR of 22.68% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Services (Medical Device Connectivity Solutions, Peripheral Technologies/ Medical Devices, Medical Device Connectivity Services) • By Technology (Wired technologies, Wireless technologies, Hybrid technologies) • By Application (Vital signs & patient monitors, Ventilators, Anesthesia Machines, Infusion Pump, Imaging Systems, Respiratory Devices, Others) • By End User (Hospitals & Surgical Centers, Maternity & Fertility Care, Trauma & emergency care, Tertiary Care Centers , Home care settings, Ambulatory & OPD, Imaging & Diagnostic Centers, Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Baxter International Inc., Iatric Systems Inc., Silex Technology, Digi International Inc., True Process, Koninklijke Philips N.V. , GE Healthcare, Stryker Corporation, iHealth Labs Inc., Cisco Systems, Lantronix Inc. |

| DRIVERS | • The transition from fee-for-service to value-based care models is a significant driver of the Medical Device Connectivity Market. • Patient empowerment is one of the main catalysts driving the growth of the Medical Device Connectivity Market. • Technological advancements are revolutionizing the Medical Device Connectivity Market, with innovations such as Artificial Intelligence, Internet of Things, and 5G wireless technology leading the way. |

| RESTRAINTS | • Growing Concern Over Data Security and Privacy |