Get more information on Machine Learning Market - Request Sample Report

Machine Learning Market was valued at USD 42.24 billion in 2023 and is expected to reach USD 666.16 billion by 2032, growing at a CAGR of 35.93% from 2024-2032.

The Machine Learning (ML) market is experiencing rapid growth, due to the increasing adoption of advanced technologies across industries. As organizations recognize the potential of ML to drive efficiency and innovation, they are integrating it into their core operations. This trend is further fueled by the surge in global data creation, which is forecast to reach 149 zettabytes in 2024. Additionally, 75% of generative AI users aim to automate tasks and improve work communications. With the rise in data volume, advancements in computational power, and improved algorithms, ML is becoming more accessible, helping businesses solve complex challenges. By leveraging these technologies, companies can gain valuable insights and enhance operational performance, positioning them for long-term success.

The growing demand for machine learning is evident in its application to real-time data processing, known as flow. Industries like manufacturing, logistics, and smart cities are leveraging ML to process large volumes of data, enabling instant decision-making. In healthcare, ML applications such as predictive analytics are driving annual growth exceeding 40%, improving patient outcomes and optimizing operations. Companies integrating ML into their operations can automate processes, optimize workflows, and enhance customer experiences. For instance, ML algorithms in supply chain management predict demand fluctuations and optimize delivery routes, resulting in cost reductions of 20-25%. In manufacturing, predictive analytics reduce downtime by anticipating equipment failures and boosting productivity. Additionally, the December 2024 launch of Boltz-1, an open-source AI model for predicting biomolecular structures, showcases ML's expanding potential across diverse sectors, revolutionizing industries beyond traditional applications.

Looking forward, the future opportunities for machine learning (ML) in flow are vast, especially as technologies like edge computing and 5G continue to evolve. With 5G coverage expected to reach 51% of the world’s population by 2024, and edge computing enabling faster data processing closer to its source, ML will see reduced latency and improved decision-making capabilities. As AI governance frameworks mature, 46% of organizations already have frameworks in place, whether dedicated or integrated into other governance structures. Industries will increasingly demand more transparent and explainable models, particularly in sectors like healthcare, where ML can personalize treatment plans, and finance, where it enhances fraud detection. Together, these advancements will drive innovation and unlock transformative opportunities across industries.

DRIVERS

As businesses strive to enhance productivity and reduce costs, the adoption of machine learning (ML) technologies to automate processes is becoming increasingly essential. Small to large businesses alike are embracing ML on a massive scale, with 65% believing the technology will help them analyze data and make better decisions. ML enables organizations to automate routine tasks, freeing up human resources for more complex activities and improving operational efficiency. By leveraging ML for real-time data analysis, businesses can make more informed, faster decisions, reducing delays and human error. In customer service, ML-powered chatbots and personalized recommendation systems elevate the user experience. Additionally, AI-driven payroll analytics improve accuracy by 25–30% compared to traditional methods. In manufacturing, ML supports predictive maintenance, preventing costly downtimes by anticipating equipment failures. This shift toward ML-driven automation fosters long-term growth by enhancing productivity and operational agility across industries.

The availability of open-source ML frameworks like TensorFlow and PyTorch, combined with user-friendly platforms such as automated machine learning (AutoML) tools, has made machine learning more accessible than ever before. TensorFlow 2.18, released in October 2024, introduces major updates, including support for NumPy 2.0, a transition to the LiteRT repository, CUDA optimizations for newer GPUs, and Hermetic CUDA for more reproducible builds. These tools simplify the process of building and deploying models, enabling non-experts to harness ML for their business needs. Companies can leverage these platforms to quickly develop custom solutions without requiring extensive expertise in data science. The reduction in technical barriers has accelerated ML adoption across industries, enabling advanced analytics, automation, and predictive capabilities more efficiently. As these tools evolve, they expand ML's potential applications, driving innovation and business process improvements.

RESTRAINTS

The cost of developing and deploying machine learning (ML) solutions can be a significant barrier, especially for small and medium-sized businesses with limited financial resources. Implementing ML requires investments in advanced infrastructure, specialized technology, and skilled personnel, all of which can be prohibitively expensive. Training large models can cost millions of dollars due to the high computing power required, with one example costing around $4 million for 3 million GPU hours. Additionally, data preparation and annotation can take up 15-25% of the total cost, with data sourcing alone potentially exceeding USD 70,000. High-complexity projects may range from USD 20,000 to over USD 500,000. These expenses, along with ongoing maintenance costs, can delay or prevent the adoption of ML technologies for organizations with tight budgets. This financial constraint limits accessibility, slowing overall market growth and innovation.

The need for large volumes of data to train machine learning (ML) models raises significant concerns regarding data privacy and security. Sensitive information, particularly in sectors like healthcare, finance, and government, is at risk of exposure if proper safeguards are not in place. The increasing frequency of data breaches and the complexity of adhering to privacy regulations, such as GDPR, make it difficult for organizations to implement ML solutions without compromising privacy. These concerns create hesitation among businesses to fully embrace ML technologies, as they must balance the benefits of automation and analytics with the responsibility to protect personal data. As a result, the adoption of ML is often slowed by the need to ensure compliance and security in handling sensitive information.

BY ENTERPRISE SIZE

In 2023, the Large Enterprises segment dominated the machine learning market, accounting for approximately 69% of the total revenue share. This dominance can be attributed to the significant financial resources and infrastructure that large organizations possess, enabling them to invest heavily in advanced ML technologies. These enterprises often have access to vast amounts of data, which enhances the effectiveness of ML models, and they are keen to leverage automation and data-driven decision-making to maintain a competitive edge.

The Small and Medium Enterprise (SME) segment is expected to grow at the fastest CAGR of about 38.04% from 2024 to 2032. This rapid growth is fueled by the increasing accessibility of affordable cloud-based machine learning solutions and the growing number of user-friendly ML platforms. SMEs are now able to adopt ML technologies without heavy upfront investments, empowering them to optimize operations, improve customer experiences, and remain competitive in their respective industries.

BY COMPONENT

In 2023, the Services segment led the machine learning market with the highest revenue share of approximately 52%. This dominance is driven by the increasing demand for customized ML solutions, which require consulting, implementation, and ongoing support services. Organizations are increasingly relying on expert services to ensure seamless integration, optimization, and maintenance of machine learning systems, especially as they scale their AI initiatives to achieve business objectives and enhance operational efficiencies.

The Software segment is projected to grow at the fastest CAGR of about 37.06% from 2024 to 2032. This rapid expansion can be attributed to the rising demand for advanced ML-powered software tools that automate tasks, improve data analytics, and drive innovation across industries. As businesses increasingly seek to integrate machine learning into their core software systems, the development of user-friendly, scalable ML software platforms is set to accelerate, fostering broader adoption and fueling the segment's remarkable growth in the coming years.

BY END-USER

In 2023, the BFSI (Banking, Financial Services, and Insurance) segment dominated the machine learning market, holding the largest revenue share of approximately 24.56%. This dominance is driven by the growing need for advanced analytics in fraud detection, risk management, customer personalization, and automation of financial processes. ML technologies allow BFSI companies to enhance decision-making, optimize operations, and provide improved services, making them a key driver of market growth in this sector.

The Healthcare and Life Sciences segment is expected to grow at the fastest CAGR of about 38.54% from 2024 to 2032. This rapid growth is fueled by the increasing demand for ML-driven solutions to enhance diagnostics, drug discovery, patient care, and personalized treatment plans. As healthcare organizations seek to improve efficiency and outcomes through data-driven insights, the potential of machine learning to transform clinical practices and research is attracting significant investments, thereby driving this segment's accelerated expansion.

BY DEPLOYMENT

In 2023, the Cloud segment dominated the machine learning market with the highest revenue share of approximately 74% and is projected to grow at the fastest CAGR of about 36.99% from 2024 to 2032. The dominance of the Cloud is driven by its scalability, flexibility, and cost-effectiveness, enabling organizations to leverage machine learning without investing heavily in on-premise infrastructure. Cloud platforms provide easy access to powerful computing resources, advanced algorithms, and vast data storage capabilities, making them ideal for ML adoption across industries. As businesses increasingly embrace cloud-based ML solutions for faster implementation and lower operational costs, the segment’s rapid growth is fueled by the rising demand for real-time analytics, automation, and AI-driven insights. This makes the Cloud segment a central enabler of the broader machine learning market expansion.

REGIONAL ANALYSIS

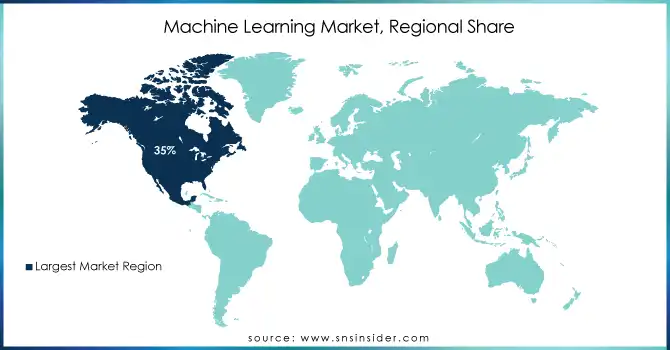

In 2023, North America led the machine learning market with the highest revenue share of approximately 35%. This dominance is largely due to the region's strong technological infrastructure, significant investments in AI research, and a high concentration of leading technology companies. The presence of major players in industries such as healthcare, finance, and manufacturing has accelerated the adoption of machine learning, enabling North American businesses to capitalize on advanced analytics, automation, and innovation.

The Asia Pacific region is expected to grow at the fastest CAGR of about 39.52% from 2024 to 2032. This rapid growth can be attributed to the increasing digitalization of industries, government initiatives supporting AI adoption, and the expanding startup ecosystem in countries like China, India, and Japan. As businesses in Asia Pacific seek to leverage machine learning for enhanced productivity, efficiency, and competitive advantage, the region’s growing focus on technological advancements is set to drive substantial market expansion.

Need any customization research/data on Machine Learning Market - Enquiry Now

KEY PLAYERS

Google Inc. (TensorFlow, Google Cloud AI Platform)

Amazon (Amazon SageMaker, AWS Deep Learning AMIs)

Intel Corporation (OpenVINO Toolkit, Intel AI Analytics Toolkit)

Facebook Inc. (PyTorch, Deepfake Detection Challenge Tools)

Microsoft Corporation (Azure Machine Learning, Microsoft Cognitive Toolkit (CNTK))

IBM Corporation (IBM Watson Studio, IBM Watson Machine Learning)

Wipro Limited (HOLMES AI Platform, Data Discovery Platform)

Nuance Communications (Dragon Speech Recognition, Nuance Mix AI Tooling)

Apple Inc. (Core ML, Create ML)

Cisco Systems (Cisco AI Endpoint Analytics, Cisco DNA Spaces AI)

Amazon Web Services (AWS) (AWS SageMaker, AWS Personalize)

Baidu Inc. (PaddlePaddle, Baidu AI Cloud)

H2O.AI (H2O Driverless AI, H2O-3)

Hewlett Packard Enterprise Development LP (HPE Ezmeral ML Ops, HPE InfoSight)

SAS Institute Inc. (SAS Visual Data Mining and Machine Learning, SAS Viya)

SAP SE (SAP Data Intelligence, SAP Predictive Analytics)

NVIDIA Corporation (CUDA, NVIDIA Deep Learning AI)

Oracle Corporation (Oracle AI Platform, Oracle Cloud Infrastructure AI)

Salesforce (Einstein Analytics, Salesforce AI Research)

Accenture (myConcerto, Accenture AI Platform)

Alibaba Group (Alibaba Cloud Machine Learning Platform, Aliyun AI)

Qualcomm Incorporated (AI Engine, Qualcomm Neural Processing SDK)

LATEST NEWS-

In October 2024, Google unveiled several AI updates, including the launch of Gemini 1.5 and advancements in language models, aimed at enhancing efficiency, security, and scalability across applications.

In December 2024, Amazon made significant strides in artificial intelligence by announcing a USD 110 million investment in the "Build on Trainium" research program, which focuses on advancing generative AI.

On April 9, 2024, Intel introduced the Gaudi 3 AI accelerator, promising significant improvements in performance, efficiency, and cost over competitors like Nvidia's H100.

On December 12, 2024, Apple partnered with Broadcom to develop a custom AI chip for its "Baltra" project. The new chip, aimed at enhancing AI features across Apple’s devices, is expected to enter mass production by 2026

| Report Attributes | Details |

| Market Size in 2024 | USD 42.24 billion |

| Market Size by 2032 | USD 666.16 billion |

| CAGR | CAGR of 35.93% from 2024-2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Enterprise Size (SMEs, Large Enterprises) • By Deployment (Cloud, On-Premises) • By End-user (Healthcare and Life Sciences, BFSI, Retail and E-commerce, Manufacturing and Supply Chain, Information Technology and Telecommunications) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Google Inc., Amazon, Intel Corporation, Facebook Inc., Microsoft Corporation, IBM Corporation, Wipro Limited, Nuance Communications, Apple Inc., Cisco Systems, Amazon Web Services (AWS), Baidu Inc., H2O.AI, Hewlett Packard Enterprise Development LP, SAS Institute Inc., SAP SE, NVIDIA Corporation, Oracle Corporation, Salesforce, Accenture, Alibaba Group, Qualcomm Incorporated |

| Key Drivers | • Growing Demand for Automation and Efficiency Through Machine Learning in Business Operations • Enhanced Access to Machine Learning Through Improved Tools and Frameworks |

| Challenges | • High Implementation Costs Hindering Widespread Adoption of Machine Learning • Data Privacy and Security Challenges Limiting Machine Learning Adoption |

ANS- North America led the ML market with approximately 35% of the revenue share in 2023.

ANS- The Asia Pacific region is expected to grow at a CAGR of about 39.52% from 2024 to 2032.

ANS- The Cloud segment is projected to grow at a CAGR of about 36.99% from 2024 to 2032.

ANS- Small and medium enterprises (SMEs) are expected to grow at about 18.81% CAGR.

ANS- Machine Learning Market was valued at USD 42.24 billion in 2023 and is expected to reach USD 666.16 billion by 2032, growing at a CAGR of 35.93% from 2024-2032.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 User Demographics, 2023

5.3 Cloud Services Usage, by Region

5.4 Integration Capabilities, by Software, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Machine Learning Market Segmentation, By Component

7.1 Chapter Overview

7.2 Hardware

7.2.1 Hardware Market Trends Analysis (2020-2032)

7.2.2 Hardware Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Software

7.3.1 Software Market Trends Analysis (2020-2032)

7.3.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Services

7.4.1 Services Market Trends Analysis (2020-2032)

7.4.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Machine Learning Market Segmentation, By Enterprise Size

8.1 Chapter Overview

8.2 Large Enterprises

8.2.1 Large Enterprises Market Trends Analysis (2020-2032)

8.2.2 Large Enterprises Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Small and Medium Enterprise

8.3.1 Small and Medium Enterprise Market Trends Analysis (2020-2032)

8.3.2 Small and Medium Enterprise Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Machine Learning Market Segmentation, By End-user

9.1 Chapter Overview

9.2 Healthcare and Life Sciences

9.2.1 Healthcare and Life Sciences Market Trends Analysis (2020-2032)

9.2.2 Healthcare and Life Sciences Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 BFSI

9.3.1 BFSI Market Trends Analysis (2020-2032)

9.3.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Manufacturing and Supply Chain

9.4.1 Manufacturing and Supply Chain Market Trends Analysis (2020-2032)

9.4.2 Manufacturing and Supply Chain Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Retail and E-commerce

9.5.1 Retail and E-commerce Market Trends Analysis (2020-2032)

9.5.2 Retail and E-commerce Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Information Technology and Telecommunications

9.6.1 Information Technology and Telecommunications Market Trends Analysis (2020-2032)

9.6.2 Information Technology and Telecommunications Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Machine Learning Market Segmentation, By Deployment

10.1 Chapter Overview

10.2 Cloud

10.2.1 Cloud Market Trends Analysis (2020-2032)

10.2.2 Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 On-Premises

10.3.1 On-Premises Market Trends Analysis (2020-2032)

10.3.2 On-Premises Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.4 North America Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.2.5 North America Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.2.6 North America Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.7.2 USA Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.2.7.3 USA Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.2.7.4 USA Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.8.2 Canada Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.2.8.3 Canada Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.2.8.4 Canada Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.9.2 Mexico Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.2.9.3 Mexico Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.2.9.4 Mexico Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.7.2 Poland Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.7.3 Poland Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.7.4 Poland Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.8.2 Romania Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.8.3 Romania Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.8.4 Romania Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.4 Western Europe Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.5 Western Europe Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.6 Western Europe Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.7.2 Germany Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.7.3 Germany Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.7.4 Germany Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.8.2 France Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.8.3 France Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.8.4 France Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.9.2 UK Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.9.3 UK Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.9.4 UK Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.10.2 Italy Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.10.3 Italy Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.10.4 Italy Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.11.2 Spain Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.11.3 Spain Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.11.4 Spain Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.14.2 Austria Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.14.3 Austria Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.14.4 Austria Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.4 Asia Pacific Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.5 Asia Pacific Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.6 Asia Pacific Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.7.2 China Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.7.3 China Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.7.4 China Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.8.2 India Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.8.3 India Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.8.4 India Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.9.2 Japan Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.9.3 Japan Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.9.4 Japan Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.10.2 South Korea Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.10.3 South Korea Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.10.4 South Korea Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.11.2 Vietnam Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.11.3 Vietnam Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.11.4 Vietnam Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.12.2 Singapore Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.12.3 Singapore Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.12.4 Singapore Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.13.2 Australia Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.13.3 Australia Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.13.4 Australia Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.4 Middle East Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.5 Middle East Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.6 Middle East Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.7.2 UAE Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.7.3 UAE Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.7.4 UAE Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.4 Africa Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.2.5 Africa Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.2.6 Africa Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Machine Learning Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.4 Latin America Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.6.5 Latin America Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.6.6 Latin America Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.7.2 Brazil Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.6.7.3 Brazil Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.6.7.4 Brazil Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.8.2 Argentina Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.6.8.3 Argentina Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.6.8.4 Argentina Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.9.2 Colombia Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.6.9.3 Colombia Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.6.9.4 Colombia Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Machine Learning Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Machine Learning Market Estimates and Forecasts, By Enterprise Size (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Machine Learning Market Estimates and Forecasts, By End-user (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Machine Learning Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

12. Company Profiles

12.1 Google Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Amazon.com

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Intel Corporation

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Facebook Inc.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Microsoft Corporation

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 IBM Corporation

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Wipro Limited

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Nuance Communications

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Apple Inc.

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Cisco Systems

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Hardware

Software

Services

By Enterprise Size

Large Enterprises

Small and Medium Enterprise

By Deployment

Cloud

On-Premises

By End-user

Healthcare and Life Sciences

BFSI

Retail and E-commerce

Manufacturing and Supply Chain

Information Technology and Telecommunications

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Social Gaming Market was valued at USD 29.48 billion in 2023 and is expected to reach USD 110.74 billion by 2032, growing at a CAGR of 15.90% from 2024-2032.

B2B E-Commerce Market was valued at USD 19,805 billion in 2023 and is expected to reach USD 82,473 billion by 2032, growing at a CAGR of 17.24% from by 2032.

The Advanced Analytics Market was valued at USD 62.2 Billion in 2023 and will reach USD 554.3 Billion by 2032, growing at a CAGR of 24.54% by 2032.

The Self-Service Analytics Market was valued at USD 4.5 billion in 2023 and will reach USD 19.75 billion by 2032, growing at a CAGR of 17.90% by 2032.

Conversational AI Market Size was valued at USD 10.1 Billion in 2023 and is expected to reach USD 64.5 Billion by 2032 and grow at a CAGR of 22.89 % over the forecast period 2024-2032.

The Custom Software Development Market Size was valued at USD 34.84 Billion in 2023 and will reach USD 206.61 Billion by 2032 and grow at a CAGR of 21.9% by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd