To Get More Information on Live Cell Encapsulation Market - Request Sample Report

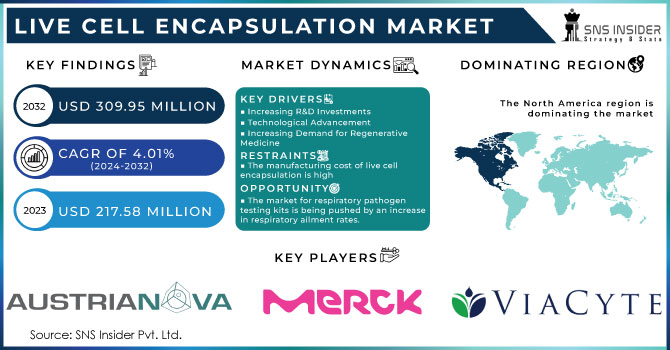

The Live Cell Encapsulation Market size was estimated at USD 217.58 million in 2023 and is expected to reach USD 309.95 million by 2032 wit a growing CAGR of 4.01% during the forecast period of 2024-2032.

Live cell encapsulation has been regarded as a solution to several therapeutic difficulties in the current period. The primary applications of live cell encapsulation include cell transplantation, cell-based medicinal delivery, and controlled drug delivery. The method envelopes live cells in biocompatible capsules for protection. These capsules protect living cells from immune system damage. Because of cell encapsulation, compounds of interest can be supplied for a longer period of time. Using live cell encapsulation reduces the need for surgical procedures.

DRIVERS

Increasing R&D Investments

Technological Advancement

Increasing Demand for Regenerative Medicine

Regenerative medicine is a new area that tries to repair or replace damaged or diseased tissues and organs. In regenerative medicine, live cell encapsulation is critical. Because it allows for the transfer of living cells to specific areas where they can restore damaged tissues. The regenerative medicine market's rapid expansion is generating demand for live cell encapsulation technology.

RESTRAIN

The manufacturing cost of live cell encapsulation is high

The production cost of live cell encapsulation might be relatively high due to a variety of reasons. The manufacture of capsules or microspheres necessitates specific equipment and skill, both of which can be expensive. Furthermore, the cells utilized in the encapsulation process are frequently sensitive and require careful handling and processing, which adds to the manufacturing cost. Another aspect that contributes to the expense of live cell encapsulation is the regulatory requirements that must be met to ensure the finished product's safety and efficacy. This can entail considerable testing and validation, which can be time consuming and costly.

OPPORTUNITY

Significant expenditures in research and development are being made by governments and financial institutions

The market for respiratory pathogen testing kits is being pushed by an increase in respiratory ailment rates.

CHALLENGES

Limited availability

As alternative treatment methods become more extensively used, the live cell encapsulation market is projected to be hampered by a scarcity of high-quality raw materials.

Despite Russia's war on Ukraine, with its relentless bombardment and shelling of cities, including schools, universities, and R&D institutes, despite the destruction and death, science in Ukraine remains active, and many chemists continue to work in their Ukrainian laboratories. They are currently operating in extremely tough conditions, frequently without access to grants and other critical financing and unable to obtain the reagents and supplies they require or repair war-damaged equipment. However, the collective and personal support they receive from the civilized world is critical for all of us to trust in triumph and return to normal life and scientific activity.

By Polymer Type

Natural Polymers

Alginate

Chitosan

Cellulose

Others

Synthetic Polymers

In 2023, natural polymers segment is expected to held the highest market share of 69.9% during the forecast period. Natural polymers are the preferred encapsulating material. Natural polymers are large molecular weight macromolecules generated from nature that are chosen for their biodegradability, low toxicity, biocompatibility, renewability, and adaptability. Because they are of natural origin, such as microbes, animals, and plants, they can interact with cells and tissues, displaying some qualities that the body recognizes and, as a result, are not treated as foreign bodies. As a result, natural polymers such as lipids, proteins, and polysaccharides have been used as an encapsulation for encapsulating hydrophobic or hydrophilic active substances that might be solid, liquid, or gaseous in order to transport and deliver them to the appropriate sites.

By Method

Macroencapsulation

Nanoencapsulation

In 2023, the microencapsulation segment is expected to dominate the market growth of 64.2% during the forecast period. The microencapsulation technique is the process of encapsulating a bioactive material in a particle size of 1-1000 m in diameter for sustained and controlled administration as well as protection of the encapsulated bioactive ingredient from the surrounding environment. Microencapsulation offers a number of therapeutic uses in the treatment of diseases such as tuberculosis, cancer, diabetes, rheumatoid arthritis, and respiratory tract infection. Islets of Langerhans, for example, are microencapsulated and implanted in the body for long-term therapy of diabetes or other diseases that necessitate organ transplantation.

By Application

Drug Delivery

Regenerative Medicine

Cell Transplantation

Others

In 2023, the drug delivery segment is expected to dominate the market growth of 44.7% during the forecast period. For effective medication delivery, living cell encapsulation technology is employed in the production of capsules, tablets, and parenteral dosage forms. Controllable drug delivery offers enormous potential in many diseases with a progressive course. The segment is being driven by the benefits of regulated drug administration by live cell encapsulation, such as increased therapeutic effects, reduced drug dose, less cytotoxicity, improved patient convenience, and compliance. Furthermore, throughout the projection period, the regenerative medicine category is expected to rise at a rapid CAGR.

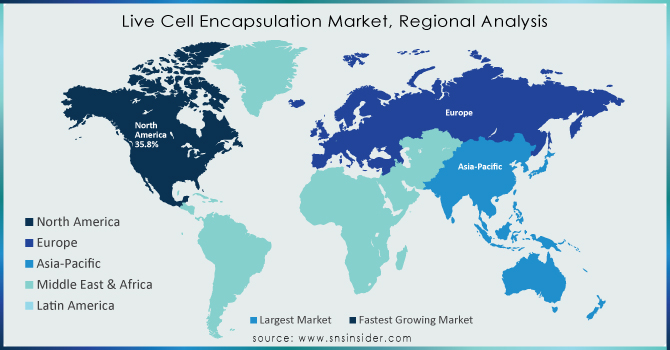

North America held a significant market share of over 35.8% in 2023. This significant percentage can be attributable to growing private-sector funding, favorable rules, and government aid. The region is primarily focused on drug discovery research, which is pushing industry expansion. The presence of innovators and important operational players has resulted in greater product penetration in the region. For example, ViaCyte, Inc. announced the start of a phase 2 clinical investigation using encapsulated cell therapy to treat type 1 diabetic patients in February 2022.

Asia-Pacific is witness to expand fastest CAGR rate during the forecast period owing to the rapid increase can be ascribed to advancements in emerging economies such as India and China's biotechnology and pharmaceutical industries. This region's profitable expansion can also be ascribed to continuous government backing for emerging countries' pharmaceutical sectors. Furthermore, current research in the realms of cancer and infectious diseases, such as COVID-19, is likely to fuel significant growth in the region's live cell encapsulation market.

Do You Need any Customization Research on Live Cell Encapsulation Market - Enquire Now

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major players are AUSTRIANOVA, Merck KGaA, Sphere Fluidics Ltd., ViaCyte, Inc., Blacktrace Holdings Ltd. (Dolomite Microfluidics), BIO INX, Living Cell Technologies Ltd., Sigilon Therapeutics, Inc., Isogen, Diatranz Otsuka Ltd., Arsenal Biosciences, and Others.

BIO INX, in November 2022, Hydrobio INX N400, the first commercially available bioresin that supports live cell encapsulation with high-resolution biofabrication, was introduced by BIO INX.

Arsenal Biosciences, in September 2022, Arsenal Biosciences secured USD 220 million in series B funding to enhance its pipeline of therapeutic candidates and cell therapy research activities for solid tumor malignancies.

ViaCyte, Inc., in February 2021, ViaCyte, Inc. announced the start of a phase 2 clinical trial utilizing encapsulated cell therapy for the treatment of type 1 diabetic patients.

| Report Attributes | Details |

| Market Size in 2023 | US$ 217.58 Million |

| Market Size by 2032 | US$ 309.95 Million |

| CAGR | CAGR of 4.01% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Polymer Type (Natural Polymers, Synthetic Polymers) • By Method (Microencapsulation, Macroencapsulation, Nanoencapsulation) • By Application (Drug Delivery, Regenerative Medicine, Cell Transplantation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | AUSTRIANOVA, Merck KGaA, Sphere Fluidics Ltd., ViaCyte, Inc., Blacktrace Holdings Ltd. (Dolomite Microfluidics), BIO INX, Living Cell Technologies Ltd., Sigilon Therapeutics, Inc., Isogen, Diatranz Otsuka Ltd., Arsenal Biosciences |

| Key Drivers | • Increasing R&D Investments • Technological Advancement • Increasing Demand for Regenerative Medicine |

| Market Restrain | • The manufacturing cost of live cell encapsulation is high |

Ans: Natural polymers segment is expected to held the highest market share of 69.9% in 2022.

Ans: Live Cell Encapsulation Market is anticipated to expand by 4.01% from 2024 to 2032.

Ans: The growth of Live Cell Encapsulation Market is expected to grow to USD 309.95 million by 2032.

Ans: Live Cell Encapsulation Market size was valued at USD 217.58 million in 2023.

Ans: Rising demand for regenerative medicine.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Ukraine- Russia War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Microcarriers Market Segmentation, By Polymer Type

8.1 Natural Polymers

8.1.1 Alginate

8.1.2 Chitosan

8.1.3 Cellulose

8.1.4 Others

8.2 Synthetic Polymers

9. Microcarriers Market Segmentation, By Method

9.1 Microencapsulation

9.2 Macroencapsulation

9.3 Nanoencapsulation

10. Microcarriers Market Segmentation, By Application

10.1 Drug Delivery

10.2 Regenerative Medicine

10.3 Cell Transplantation

10.4 Others

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Live Cell Encapsulation Market by Country

11.2.2North America Live Cell Encapsulation Market by Polymer Type

11.2.3 North America Live Cell Encapsulation Market by Method

11.2.4 North America Live Cell Encapsulation Market by Application

11.2.5 USA

11.2.5.1 USA Live Cell Encapsulation Market by Polymer Type

11.2.5.2 USA Live Cell Encapsulation Market by Method

11.2.5.3 USA Live Cell Encapsulation Market by Application

11.2.6 Canada

11.2.6.1 Canada Live Cell Encapsulation Market by Polymer Type

11.2.6.2 Canada Live Cell Encapsulation Market by Method

11.2.6.3 Canada Live Cell Encapsulation Market by Application

11.2.7 Mexico

11.2.7.1 Mexico Live Cell Encapsulation Market by Polymer Type

11.2.7.2 Mexico Live Cell Encapsulation Market by Method

11.2.7.3 Mexico Live Cell Encapsulation Market by Application

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Eastern Europe Live Cell Encapsulation Market by Country

11.3.1.2 Eastern Europe Live Cell Encapsulation Market by Polymer Type

11.3.1.3 Eastern Europe Live Cell Encapsulation Market by Method

11.3.1.4 Eastern Europe Live Cell Encapsulation Market by Application

11.3.1.5 Poland

11.3.1.5.1 Poland Live Cell Encapsulation Market by Polymer Type

11.3.1.5.2 Poland Live Cell Encapsulation Market by Method

11.3.1.5.3 Poland Live Cell Encapsulation Market by Application

11.3.1.6 Romania

11.3.1.6.1 Romania Live Cell Encapsulation Market by Polymer Type

11.3.1.6.2 Romania Live Cell Encapsulation Market by Method

11.3.1.6.4 Romania Live Cell Encapsulation Market by Application

11.3.1.7 Turkey

11.3.1.7.1 Turkey Live Cell Encapsulation Market by Polymer Type

11.3.1.7.2 Turkey Live Cell Encapsulation Market by Method

11.3.1.7.3 Turkey Live Cell Encapsulation Market by Application

11.3.1.8 Rest of Eastern Europe

11.3.1.8.1 Rest of Eastern Europe Live Cell Encapsulation Market by Polymer Type

11.3.1.8.2 Rest of Eastern Europe Live Cell Encapsulation Market by Method

11.3.1.8.3 Rest of Eastern Europe Live Cell Encapsulation Market by Application

11.3.2 Western Europe

11.3.2.1 Western Europe Live Cell Encapsulation Market by Polymer Type

11.3.2.2 Western Europe Live Cell Encapsulation Market by Method

11.3.2.3 Western Europe Live Cell Encapsulation Market by Application

11.3.2.4 Germany

11.3.2.4.1 Germany Live Cell Encapsulation Market by Polymer Type

11.3.2.4.2 Germany Live Cell Encapsulation Market by Method

11.3.2.4.3 Germany Live Cell Encapsulation Market by Application

11.3.2.5 France

11.3.2.5.1 France Live Cell Encapsulation Market by Polymer Type

11.3.2.5.2 France Live Cell Encapsulation Market by Method

11.3.2.5.3 France Live Cell Encapsulation Market by Application

11.3.2.6 UK

11.3.2.6.1 UK Live Cell Encapsulation Market by Polymer Type

11.3.2.6.2 UK Live Cell Encapsulation Market by Method

11.3.2.6.3 UK Live Cell Encapsulation Market by Application

11.3.2.7 Italy

11.3.2.7.1 Italy Live Cell Encapsulation Market by Polymer Type

11.3.2.7.2 Italy Live Cell Encapsulation Market by Method

11.3.2.7.3 Italy Live Cell Encapsulation Market by Application

11.3.2.8 Spain

11.3.2.8.1 Spain Live Cell Encapsulation Market by Polymer Type

11.3.2.8.2 Spain Live Cell Encapsulation Market by Method

11.3.2.8.3 Spain Live Cell Encapsulation Market by Application

11.3.2.9 Netherlands

11.3.2.9.1 Netherlands Live Cell Encapsulation Market by Polymer Type

11.3.2.9.2 Netherlands Live Cell Encapsulation Market by Method

11.3.2.9.3 Netherlands Live Cell Encapsulation Market by Application

11.3.2.10 Switzerland

11.3.2.10.1 Switzerland Live Cell Encapsulation Market by Polymer Type

11.3.2.10.2 Switzerland Live Cell Encapsulation Market by Method

11.3.2.10.3 Switzerland Live Cell Encapsulation Market by Application

11.3.2.11.1 Austria

11.3.2.11.2 Austria Live Cell Encapsulation Market by Polymer Type

11.3.2.11.3 Austria Live Cell Encapsulation Market by Method

11.3.2.11.4 Austria Live Cell Encapsulation Market by Application

11.3.2.12 Rest of Western Europe

11.3.2.12.1 Rest of Western Europe Live Cell Encapsulation Market by Polymer Type

11.3.2.12.2 Rest of Western Europe Live Cell Encapsulation Market by Method

11.3.2.12.3 Rest of Western Europe Live Cell Encapsulation Market by Application

11.4 Asia-Pacific

11.4.1 Asia-Pacific Live Cell Encapsulation Market by Country

11.4.2 Asia-Pacific Live Cell Encapsulation Market by Polymer Type

11.4.3 Asia-Pacific Live Cell Encapsulation Market by Method

11.4.4 Asia-Pacific Live Cell Encapsulation Market by Application

11.4.5 China

11.4.5.1 China Live Cell Encapsulation Market by Polymer Type

11.4.5.2 China Live Cell Encapsulation Market by Application

11.4.5.3 China Live Cell Encapsulation Market by Method

11.4.6 India

11.4.6.1 India Live Cell Encapsulation Market by Polymer Type

11.4.6.2 India Live Cell Encapsulation Market by Method

11.4.6.3 India Live Cell Encapsulation Market by Application

11.4.7 Japan

11.4.7.1 Japan Live Cell Encapsulation Market by Polymer Type

11.4.7.2 Japan Live Cell Encapsulation Market by Method

11.4.7.3 Japan Live Cell Encapsulation Market by Application

11.4.8 South Korea

11.4.8.1 South Korea Live Cell Encapsulation Market by Polymer Type

11.4.8.2 South Korea Live Cell Encapsulation Market by Method

11.4.8.3 South Korea Live Cell Encapsulation Market by Application

11.4.9 Vietnam

11.4.9.1 Vietnam Live Cell Encapsulation Market by Polymer Type

11.4.9.2 Vietnam Live Cell Encapsulation Market by Method

11.4.9.3 Vietnam Live Cell Encapsulation Market by Application

11.4.10 Singapore

11.4.10.1 Singapore Live Cell Encapsulation Market by Polymer Type

11.4.10.2 Singapore Live Cell Encapsulation Market by Method

11.4.10.3 Singapore Live Cell Encapsulation Market by Application

11.4.11 Australia

11.4.11.1 Australia Live Cell Encapsulation Market by Polymer Type

11.4.11.2 Australia Live Cell Encapsulation Market by Method

11.4.11.3 Australia Live Cell Encapsulation Market by Application

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Live Cell Encapsulation Market by Polymer Type

11.4.12.2 Rest of Asia-Pacific Live Cell Encapsulation Market by Method

11.4.12.3 Rest of Asia-Pacific Live Cell Encapsulation Market by Application

11.5 Middle East & Africa

11.5.1 Middle East

11.5.1.1 Middle East Live Cell Encapsulation Market by Country

11.5.1.2 Middle East Live Cell Encapsulation Market by Polymer Type

11.5.1.3 Middle East Live Cell Encapsulation Market by Method

11.5.1.4 Middle East Live Cell Encapsulation Market by Application

11.5.1.5 UAE

11.5.1.5.1 UAE Live Cell Encapsulation Market by Polymer Type

11.5.1.5.2 UAE Live Cell Encapsulation Market by Method

11.5.1.5.3 UAE Live Cell Encapsulation Market by Application

11.5.1.6 Egypt

11.5.1.6.1 Egypt Live Cell Encapsulation Market by Polymer Type

11.5.1.6.2 Egypt Live Cell Encapsulation Market by Method

11.5.1.6.3 Egypt Live Cell Encapsulation Market by Application

11.5.1.7 Saudi Arabia

11.5.1.7.1 Saudi Arabia Live Cell Encapsulation Market by Polymer Type

11.5.1.7.2 Saudi Arabia Live Cell Encapsulation Market by Method

11.5.1.7.3 Saudi Arabia Live Cell Encapsulation Market by Application

11.5.1.8 Qatar

11.5.1.8.1 Qatar Live Cell Encapsulation Market by Polymer Type

11.5.1.8.2 Qatar Live Cell Encapsulation Market by Method

11.5.1.8.3 Qatar Live Cell Encapsulation Market by Application

11.5.1.9 Rest of Middle East

11.5.1.9.1 Rest of Middle East Live Cell Encapsulation Market by Polymer Type

11.5.1.9.2 Rest of Middle East Live Cell Encapsulation Market by Method

11.5.1.9.3 Rest of Middle East Live Cell Encapsulation Market by Application

11.5.2 Africa

11.5.2.1 Africa Transfusion Diagnostics Market by Country

11.5.2.2 Africa Live Cell Encapsulation Market by Polymer Type

11.5.2.3 Africa Live Cell Encapsulation Market by Method

11.5.2.4 Africa Live Cell Encapsulation Market by Application

11.5.2.5 Nigeria

11.5.2.5.1 Nigeria Live Cell Encapsulation Market by Polymer Type

11.5.2.5.2 Nigeria Live Cell Encapsulation Market by Method

11.5.2.5.3 Nigeria Live Cell Encapsulation Market by Application

11.5.2.6 South Africa

11.5.2.6.1 South Africa Live Cell Encapsulation Market by Polymer Type

11.5.2.6.2 South Africa Live Cell Encapsulation Market by Method

11.5.2.6.3 South Africa Live Cell Encapsulation Market by Application

11.5.2.7 Rest of Africa

11.5.2.7.1 Rest of Africa Live Cell Encapsulation Market by Polymer Type

11.5.2.7.2 Rest of Africa Live Cell Encapsulation Market by Method

11.5.2.7.3 Rest of Africa Live Cell Encapsulation Market by Application

11.6 Latin America

11.6.1 Latin America Live Cell Encapsulation Market by Country

11.6.2 Latin America Live Cell Encapsulation Market by Polymer Type

11.6.3 Latin America Live Cell Encapsulation Market by Method

11.6.4 Latin America Live Cell Encapsulation Market by Application

11.6.5 Brazil

11.6.5.1 Brazil Live Cell Encapsulation Market by Polymer Type

11.6.5.2 Brazil Live Cell Encapsulation Market by Method

11.6.5.3 Brazil Live Cell Encapsulation Market by Application

11.6.6 Argentina

11.6.6.1 Argentina Live Cell Encapsulation Market by Polymer Type

11.6.6.2 Argentina Live Cell Encapsulation Market by Method

11.6.6.3 Argentina Live Cell Encapsulation Market by Application

11.6.7 Colombia

11.6.7.1 Colombia Live Cell Encapsulation Market by Polymer Type

11.6.7.2 Colombia Live Cell Encapsulation Market by Method

11.6.7.3 Colombia Live Cell Encapsulation Market by Application

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Live Cell Encapsulation Market by Polymer Type

11.6.8.2 Rest of Latin America Live Cell Encapsulation Market by Method

11.6.8.3 Rest of Latin America Live Cell Encapsulation Market by Application

12. Company Profile

12.1 AUSTRIANOVA

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Product / Services Offered

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Merck KGaA

12.2.1 Company Overview

12.2.2 Financials

12.2.3 Product/Services Offered

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 Sphere Fluidics Ltd.

12.3.1 Company Overview

12.3.2 Financials

12.3.3 Product/Services Offered

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 ViaCyte, Inc.

12.4.1 Company Overview

12.4.2 Financials

12.4.3 Product/Services Offered

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Blacktrace Holdings Ltd. (Dolomite Microfluidics)

12.5.1 Company Overview

12.5.2 Financials

12.5.3 Product/Services Offered

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 BIO INX

12.6.1 Company Overview

12.6.2 Financials

12.6.3 Product/Services Offered

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 Living Cell Technologies Ltd.

12.7.1 Company Overview

12.7.2 Financials

12.7.3 Product/Services Offered

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 Sigilon Therapeutics, Inc.

12.8.1 Company Overview

12.8.2 Financials

12.8.3 Product/Services Offered

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Isogen

12.9.1 Company Overview

12.9.2 Financials

12.9.3 Product/Services Offered

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Diatranz Otsuka Ltd.

12.10.1 Company Overview

12.10.2 Financials

12.10.3 Product/Services Offered

12.10.4 SWOT Analysis

12.10.5 The SNS View

12.11 Arsenal Biosciences

12.11.1 Company Overview

12.11.2 Financials

12.11.3 Product/Services Offered

12.11.4 SWOT Analysis

12.11.5 The SNS View

12.11 Others

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Emergency Department Information System Market was valued at USD 1 billion in 2023 and is expected to reach USD 3.40 billion by 2032, at a CAGR of 14.60%.

The PET Scanners Market Size was valued at USD 2.6 Billion in 2023, and is expected to reach USD 4.9 Billion by 2032, and grow at a CAGR of 7.7%.

The Smart Healthcare Market size was USD 166 Billion in 2023 and is expected to Reach USD 441.30 Billion by 2031 and grow at a CAGR of 13% over the forecast period of 2024-2031.

The Medical Coding Market, valued at USD 18.41 billion in 2023, is anticipated to achieve a valuation of USD 40.55 billion by 2032, experiencing a compound annual growth rate of 9.21% over the forecast from 2024 to 2032.

The DNA Synthesizer Market size valued at USD 270.40 million in 2023 and is expected to reach USD 922.11 million by 2032 with a CAGR of 14.62% during the forecast period of 2024-2032.

The Dura Substitutes Market was valued at USD 215 million in 2023 and is expected to reach USD 320.07 million by 2032, growing at a CAGR of 4.54% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd